Aseptic Sampling Market Size, Share & Industry Analysis, By Product Type (Manual and Automated), By Sampling Technique (Valve-Based Sampling, Needle & Septum-Based Sampling, Bag-Based Sampling, and Others), By Application (Downstream Processing and Upstream Processing), By End-user (Pharmaceutical & Biopharmaceutical Manufacturers, CMOs / CDMOs, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

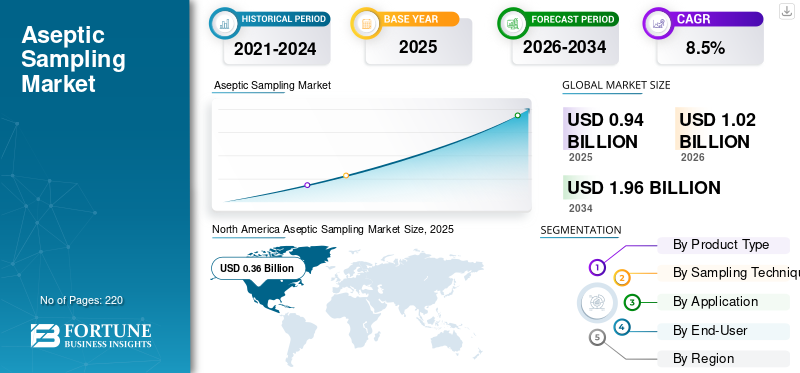

The global aseptic sampling market size was valued at USD 0.94 billion in 2025. The market is projected to grow from USD 1.02 billion in 2026 to USD 1.96 billion by 2034, exhibiting a CAGR of 8.5% during the forecast period. North America dominated the global aseptic sampling market with a market share of 38.3% in 2025.

Aseptic sampling is the collection of processed samples in order to avoid the introduction of unwanted contamination into the product or the sample. The process is used in upstream and downstream bioprocessing, sterile manufacturing, QC checks, and routine process monitoring. The growth is attributed to extensively expanding biopharma pipelines, rising batch values, and strict emphasis on microbial control programs. Moreover, companies are moving toward single-use assemblies and more repeatable sampling steps to reduce operator dependency.

- For instance, in June 2024, Shionogi & Co., Ltd. announced expansion of its antimicrobial research program in order to address current and possible health threats.

Furthermore, several major companies, including Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc., and Cytiva, emphasize the development of different cutting-edge technologies to offer better efficiency.

Download Free sample to learn more about this report.

Aseptic Sampling Market Key Takeaways

- 2025 Market Size: USD 0.94 billion

- 2026 Market Size: USD 1.02 billion

- 2034 Forecast Market Size: USD 1.96 billion

- CAGR: 8.5% from 2026–2034

- North America dominated the aseptic sampling market with a 38.3% share in 2025.

- The automated segment is projected to grow at a CAGR of 9.5% during the forecast period.

- The bag-based sampling segment is expected to register a CAGR of 9.2% over the forecast period.

North America

North America generated USD 0.36 billion in revenue in 2025.

Europe

Europe is projected to reach USD 0.30 billion by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 0.25 billion by 2026.

U.S.

The U.S. aseptic sampling market is projected to reach approximately USD 0.33 billion by 2026.

Japan

Japan’s aseptic sampling market is projected to reach USD 0.04 billion by 2026.

Read More

ASEPTIC SAMPLING MARKET TRENDS

Rising Preference for Equipment with Faster Processing and Compact Designs is an Important Trend Observed in Market

Manufacturing companies are increasingly preferring designs that reduce open exposure, simplify disconnection, and protect the sample integrity during transfer and handling. In addition, there is considerable demand and adoption of automation along with hassle-free processing. Due to these trends, market players emphasize introducing new equipment with these functionalities, which is further projected to propel its adoption.

- For instance, in October 2025, Avantor, Inc. announced the launch of its next-generation sterile aseptic sampling platform. The new platform allows manufacturers better flexibility and scaled bioprocessing.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Pharmaceutical and Biopharmaceutical Manufacturing to Boost Market Growth

Growing volumes of pharmaceutical and biopharmaceutical manufacturing are expected to have a positive impact on the global aseptic sampling market growth. As pharmaceutical and biopharmaceutical production expands, the number of batches, lines, and routine in-process checks will eventually increase. Moreover, a rise in production automatically leads to more sampling, raw material checks, and quality monitoring. This directly increases demand for aseptic sampling tools, as companies focus on the quick collection of samples without risking contamination.

MARKET RESTRAINTS

Higher Cost Compared to Basic Sampling Methods to Restrict Market Growth

High initial investment required for aseptic sampling solutions compared to conventional or open sampling methods is one of the prominent restraints hampering the market growth. Specialized valves, assemblies, and sterile components increase equipment and consumable costs, which can limit adoption in cost-sensitive manufacturing environments. For routine or lower-risk processes, some manufacturers prefer to continue with existing sampling practices to avoid additional capital and operating expenses. This cost consideration is particularly relevant for smaller facilities or mature plants where budgets are tightly controlled, slowing the pace of transition to advanced aseptic sampling solutions.

MARKET OPPORTUNITIES

Growing Demand for Ready-to-Use Sampling Solutions to Offer Market Growth Opportunities

Rising demand for ready-to-use sampling technologies is estimated to offer a lucrative opportunity for the market. Pharmaceutical and biopharmaceutical manufacturers are preferring products that arrive pre-assembled, sterile, and easy to deploy without complex setup. This reduces preparation time, lowers handling risk, and helps production teams stay focused on output targets. Moreover, along with these factors, as manufacturing volumes rise, companies are looking for sampling tools that are quick to install, easy to replace, and consistent across batches. This generates demand for ready-to-use and compact sampling technologies.

- For instance, in October 2025, Co-Diagnostics, Inc. announced the launch of its new sample preparation instrument for point-of-care testing.

MARKET CHALLENGES

Ensuring Consistent Supplier Availability and Continuity to Pose a Critical Challenge to Market Growth

There is a common challenge observed in the aseptic sampling market is ensuring consistent availability of sampling components from approved suppliers. Moreover, pharmaceutical and biopharmaceutical manufacturers rely on qualified vendors, and switching suppliers is not easy due to internal approval and qualification processes. If a preferred supplier faces production delays or capacity constraints, manufacturers may struggle to source alternatives quickly. This dependency on a limited supplier base can create planning uncertainty, especially for high-volume or multi-site operations, and puts pressure on vendors to maintain reliable supply and long-term continuity.

Segmentation Analysis

By Product Type

Manual Segment to Lead Market Due to Its Cost Efficiency and Easy Deployment

Based on the product type, the market is divided into manual and automated.

The manual segment is anticipated to account for the largest aseptic sampling market share. The high segmental share is primarily attributed to its lower price and easy deployment. In addition, manual systems also fit early-stage manufacturing and smaller batch operations where the ROI for full automation is unclear.

- For instance, in May 2022, In May 2022, CPC launched the AseptiQuik G DC series connector, which enables biopharma manufacturers to perform sterile connections. The newly introduced device supports routine manufacturing and sampling-related activities.

The automated segment is anticipated to rise with a CAGR of 9.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Sampling Technique

Easier Handling and Operations Offered by Valve-based Sampling Technique Accelerated Segment Growth

Based on the sampling technique, the market is segmented into valve-based sampling, needle & septum-based sampling, bag-based sampling, and others.

In 2025, the valve-based sampling segment dominated the global market. This dominance of the segment was due to the higher operational efficiency offered by the technique. Moreover, valve-based sampling is also preferred as it supports routine, repeated sampling during a batch with less disruption to operations.

- For instance, in March 2025, Alfa Laval expanded its hygienic valve portfolio with new valve introductions and additional sizes, which support safe processing and protect product integrity in various industries.

The bag-based sampling segment is projected to grow at a CAGR of 9.2% over the forecast period.

By Application

Requirement of High Purity in Downstream Process to Boost Segment Growth

Based on the application, the market is segmented into upstream processing and downstream processing.

The downstream segment is anticipated to witness a dominating market share over the forecast period. Downstream processing has high sampling intensity as product quality attributes and process performance must be monitored across multiple critical steps. Sampling here directly supports yield tracking, impurity control, and release readiness. Also, downstream failures can be very expensive as the product is already concentrated and of high value.

The upstream processing segment is projected to grow at a CAGR of 7.7% over the forecast period.

By End-User

Contamination Prevention in Sample Preparation by Pharmaceutical and Biopharmaceutical Manufacturers Fueled Segment Growth

Based on end-user, the market is segmented into pharmaceutical & biopharmaceutical manufacturers, CMOs / CDMOs, and others.

The pharmaceutical & biopharmaceutical manufacturers dominated the global market. These manufacturers carry the highest compliance burden and the highest cost-of-failure, so they invest more in aseptic sampling infrastructure than most other industries. Their workflows demand repeatable sampling, strong documentation, and compatibility with validated cleaning/sterilization practices. Furthermore, the segment is set to hold a 62.2% share in 2026.

In addition, CMOs / CDMOs are projected to grow at a CAGR of 8.9% during the study period.

Aseptic Sampling Market Regional Outlook

By region, the market is divided into Asia Pacific, North America, Latin America, Europe, and the Middle East & Africa.

North America

North America Aseptic Sampling Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, North America emerged as the clear market leader, recording revenues of USD 0.33 billion, and further strengthening its dominance in 2025 with a valuation of USD 0.36 billion. The region’s growth is driven by the accelerating pace of biopharmaceutical production, backed by significant R&D spending. Well-established healthcare systems and rapid technological advancements continue to act as strong growth enablers.

U.S Aseptic Sampling Market

Based on North America’s strong contribution and the U.S. dominance within the region, the market can be analytically approximated at around USD 0.33 billion by 2026, accounting for roughly 32.3% of global aseptic sampling sales.

Europe

Europe is expected to witness robust expansion, registering a growth rate of 8.0% over the projected period, the second-fastest across regions, and reaching USD 0.30 billion by 2026. This growth momentum is attributed to the scaling up of pharmaceutical manufacturing capabilities and the commissioning of new production plans.

U.K Aseptic Sampling Market

The U.K. market is estimated at around USD 0.05 billion by 2026, representing roughly 4.7% of global aseptic sampling revenues.

Germany Aseptic Sampling Market

Germany is projected to reach approximately USD 0.07 billion by 2026, equivalent to around 6.6% of global aseptic sampling sales.

Asia Pacific

The Asia Pacific market is predicted to touch USD 0.25 billion by 2026, securing its place as the third-largest regional market. India and China are projected to contribute significantly, with market values of USD 0.06 billion and USD 0.08 billion, respectively, in 2026, supported by rising investments and capacity additions.

Japan Aseptic Sampling Market

The market in Japan is estimated at around USD 0.04 billion by 2026, accounting for roughly 4.3% of global aseptic sampling revenues.

China Aseptic Sampling Market

China is projected to be one of the largest markets globally, with 2026 revenues estimated at around USD 0.08 billion, representing roughly 8.1% of global aseptic sampling sales.

India Aseptic Sampling Market

The India market is projected to reach around USD 0.06 billion by 2026, accounting for roughly 5.4% of global aseptic sampling revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to grow at a measured pace. Latin America is projected to achieve revenues of USD 0.05 billion in 2026, while the GCC region within the Middle East & Africa is anticipated to reach USD 0.01 billion over the same period.

South Africa Aseptic Sampling Market

The South Africa market is projected to reach around USD 0.005 billion by 2026, representing roughly 0.48% of global aseptic sampling revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Top Companies Emphasize Distribution Channel Expansion to Bolster Market Expansion

The structure of the global aseptic sampling market is semi-consolidated, including top players such as Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc., and Cytiva. These companies account for moderate growth, attributed to the implementation of several strategic activities, such as partnerships, mergers, and acquisitions.

- For instance, in October 2024, Thermo Fisher Scientific showcased its expanded portfolio of biopharmaceutical services at CPHI Milan.

Other top producers comprise Pall Corporation, GEA Group AG, Keofitt A/S, and Alfa Laval AB. They emphasize expansion of the distribution channel along with prioritizing capacity extension.

LIST OF KEY ASEPTIC SAMPLING COMPANIES PROFILED

- Merck KGaA (Germany)

- Sartorius AG (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- Cytiva (U.S.)

- Pall Corporation (U.S.)

- GEA Group AG (Germany)

- Keofitt A/S (Denmark)

- Alfa Laval AB (Sweden)

- Mettler-Toledo International Inc. (Switzerland)

- Flownamics Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: Fujifilm announced its plan to invest USD 1.2 billion in order to expand its biopharmaceutical manufacturing facility in North Carolina.

- June 2023: Alfa Laval announced the launch of its new streamlined Unique Mixproof CIP and process valves.

- May 2022: QualiTru Sampling Systems announced receiving of ISO 9001:2015 certification related to aseptic sampling products, systems, and services.

- September 2021: Sartorius announced its plan to expand business operations in North America. This strategic step was taken to consolidate the supply of single-use components in biopharma manufacturing.

- April 2021: Sartorius announced the opening of a new Customer Interaction Center in Beijing to support biopharma customers and single-use product needs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Sampling Technique, Application, End-User, and Region |

|

By Product Type |

· Manual · Automated |

|

By Sampling Technique |

· Valve-Based Sampling · Needle & Septum-Based Sampling · Bag-Based Sampling · Others |

|

By Application |

· Downstream Processing · Upstream Processing |

|

By End-User |

· Pharmaceutical & Biopharmaceutical Manufacturers · CMOs / CDMOs · Others |

|

By Region |

· North America (By Product Type, Sampling Technique, Application, End-User, and Country) o U.S. § Product Type o Canada § Product Type · Europe (By Product Type, Sampling Technique, Application, End-User, and Country/Sub-region) o Germany § Product Type o U.K. § Product Type o France § Product Type o Spain § Product Type o Italy § Product Type o Scandinavia § Product Type o Rest of Europe § Product Type · Asia Pacific (By Product Type, Sampling Technique, Application, End-User, and Country/Sub-region) o China § Product Type o Japan § Product Type o India § Product Type o Australia § Product Type o Southeast Asia § Product Type o Rest of Asia Pacific § Product Type · Latin America (By Product Type, Sampling Technique, Application, End-User, and Country/Sub-region) o Brazil § Product Type o Mexico § Product Type o Rest of Latin America § Product Type · Middle East & Africa (By Product Type, Sampling Technique, Application, End-User, and Country/Sub-region) o GCC § Product Type o South Africa § Product Type o Rest of Middle East & Africa § Product Type |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 0.94 billion in 2025 and is projected to reach USD 1.96 billion by 2034.

In 2025, the market value stood at USD 0.36 billion.

The market is expected to exhibit a CAGR of 8.5% during the forecast period of 2026-2034.

By product type, the manual segment is expected to lead the market.

The increasing investments for pharmaceutical and biopharma production are driving market expansion.

Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc., and Cytiva are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us