Auto Catalyst Market Size, Share & Industry Analysis, By Application (LDV-Diesel, LDV-Gasoline, HDV), and Regional Forecast, 2026-2034

Auto Catalyst Market Overview

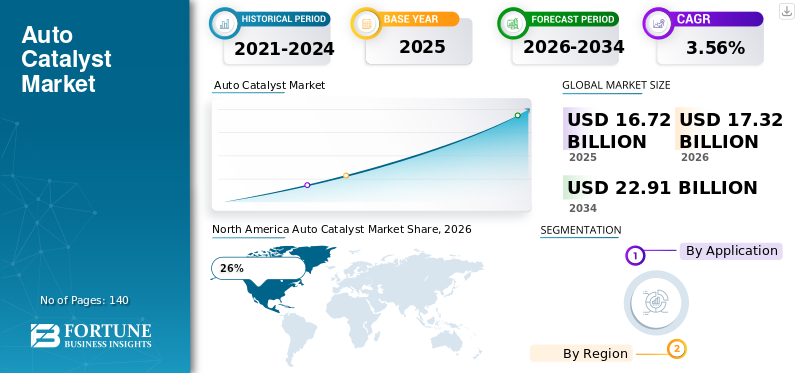

auto catalyst market size was valued at USD 16.72 billion in 2025. The market is projected to grow from USD 17.32 billion in 2026 to USD 22.91 billion by 2034, exhibiting a CAGR of 3.56% during the forecast period.

The auto catalyst market plays a critical role in the global automotive emission control industry by reducing harmful exhaust emissions generated by gasoline and diesel vehicles. Auto catalysts are widely used in catalytic converters to transform toxic pollutants such as nitrogen oxides, hydrocarbons, and carbon monoxide into less harmful gases before release into the atmosphere. Increasing environmental regulations, stricter vehicle emission standards, and growing awareness regarding air pollution control are significantly supporting auto catalyst market Growth worldwide. Automotive manufacturers are increasingly integrating advanced catalyst technologies into passenger vehicles and commercial vehicles to comply with global emission mandates. Rising automobile production and advancements in precious metal catalyst formulations continue driving market expansion globally.

The United States auto catalyst market remains one of the largest and technologically advanced sectors due to strict environmental regulations and high vehicle ownership rates. Federal emission standards continue encouraging automakers to utilize high-efficiency catalyst systems across gasoline and diesel vehicle categories. auto catalyst market Analysis in the U.S. highlights strong demand for catalytic converters in passenger cars, light-duty trucks, and heavy commercial vehicles. Increasing investments in hybrid vehicle technologies and clean mobility solutions are also supporting catalyst innovation throughout the country. The presence of major automotive manufacturers and advanced emission control technology providers continues strengthening the market landscape across the United States automotive industry.

Download Free sample to learn more about this report.

Key Takeaways

Market Size & Growth

- Global market size 2025: USD 16.72 billion

- Global market size 2034: USD 22.91 billion

- CAGR (2025–2034): 3.56%

Market Share – Regionals

- North America: 26%

- Europe: 31%

- Asia-Pacific: 35%

- Rest of World: 8%

Country-Level Shares

- Germany: 29% of Europe’s market

- United Kingdom: 16% of Europe’s market

- Japan: 22% of Asia-Pacific market

- China: 43% of Asia-Pacific market

Auto Catalyst Market Latest Trends

The auto catalyst market Trends indicate substantial technological advancements focused on improving catalyst efficiency and reducing vehicle emissions. Automotive manufacturers are increasingly adopting advanced three-way catalysts, selective catalytic reduction systems, and diesel oxidation catalysts to meet stringent environmental regulations globally. The growing production of hybrid vehicles is also influencing catalyst innovation because hybrid engines require optimized emission control systems capable of operating efficiently under varying driving conditions. auto catalyst market Research Report findings reveal increasing demand for palladium-rich catalyst formulations due to improved gasoline engine performance and reduced emissions.

Download Free sample to learn more about this report.

Another significant trend shaping the auto catalyst industry Report is the rising adoption of lightweight catalyst substrates designed to improve fuel efficiency and reduce vehicle weight. Manufacturers are investing heavily in nanotechnology and advanced coating techniques to enhance catalyst durability and thermal resistance. Recycling of precious metals such as platinum, palladium, and rhodium from used catalytic converters is becoming increasingly important because of fluctuating raw material prices and sustainability concerns.

Auto Catalyst Market Dynamics

DRIVER

Stringent Vehicle Emission Regulations Worldwide

The implementation of strict environmental and vehicle emission regulations remains the primary growth driver for the auto catalyst market. Governments across North America, Europe, and Asia-Pacific are continuously strengthening emission standards to reduce air pollution caused by automotive exhaust gases. auto catalyst market Growth is being fueled by increasing demand for catalytic converters capable of reducing nitrogen oxide emissions, hydrocarbons, and carbon monoxide from gasoline and diesel engines. Automotive manufacturers are investing heavily in advanced catalyst technologies to comply with evolving regulatory frameworks. Rising public awareness regarding environmental sustainability and urban air quality is also encouraging the adoption of efficient automotive emission control systems. Commercial vehicles, passenger cars, and hybrid vehicles increasingly require advanced catalyst systems to meet global clean transportation initiatives and emission compliance standards.

RESTRAINT

Volatility in Precious Metal Prices

One of the major restraints impacting the auto catalyst market is the fluctuating cost of precious metals such as platinum, palladium, and rhodium used in catalyst manufacturing. These metals are essential components in catalytic converters due to their ability to accelerate chemical reactions and reduce harmful emissions. However, unstable supply chains, mining limitations, and geopolitical uncertainties significantly influence raw material pricing. auto catalyst market Analysis indicates that rising precious metal costs increase manufacturing expenditures for catalyst producers and automotive companies. Smaller manufacturers often face profitability challenges because of higher procurement costs associated with advanced catalyst formulations. In addition, dependence on limited mining regions for precious metal supply creates procurement risks and operational instability across the automotive catalyst industry globally.

OPPORTUNITY

Growth in Hybrid and Low-Emission Vehicles

The increasing adoption of hybrid and low-emission vehicles presents substantial growth opportunities for the auto catalyst market. Hybrid vehicles continue to rely on internal combustion engines for partial operation, creating ongoing demand for advanced emission control technologies. auto catalyst market Opportunities are also expanding through the development of next-generation catalyst systems capable of operating efficiently under varying engine temperatures and driving cycles. Automotive companies are investing in lightweight catalyst materials and high-performance substrate technologies to improve fuel efficiency and environmental compliance. Emerging economies are witnessing rising automobile ownership and stricter emission policies, creating additional market expansion opportunities. The growing emphasis on sustainable transportation and cleaner mobility solutions is encouraging manufacturers to develop innovative catalyst systems with improved durability and reduced precious metal dependency.

CHALLENGE

Rising Transition toward Fully Electric Vehicles

The rapid transition toward battery electric vehicles presents a significant challenge for the auto catalyst market because fully electric vehicles do not require catalytic converters. Governments worldwide are promoting electric mobility through subsidies, infrastructure development, and emission reduction targets, potentially reducing long-term demand for automotive catalyst systems. Auto Catalyst Industry Analysis suggests that increasing penetration of electric vehicles within passenger transportation segments could gradually impact catalyst consumption. Additionally, catalyst manufacturers face technological pressure to innovate rapidly while maintaining profitability in a changing automotive landscape. Intense competition among global automotive suppliers and ongoing research into alternative emission reduction technologies further increase market complexity. Maintaining stable supply chains and adapting to evolving vehicle technologies remain major operational challenges for industry participants.

Auto Catalyst Market Segmentation

By Application

LDV-Diesel catalysts account for approximately 22% of the auto catalyst market Share due to continued demand for diesel-powered light-duty vehicles in several European and commercial transportation markets. Diesel catalyst systems are specifically designed to reduce nitrogen oxide emissions, particulate matter, and hydrocarbons generated by diesel combustion engines. auto catalyst market Research Report findings indicate increasing adoption of diesel oxidation catalysts and selective catalytic reduction technologies within modern diesel passenger vehicles. Automotive manufacturers are focusing on improving catalyst thermal stability and durability to comply with stringent diesel emission standards globally. Growing use of advanced after-treatment systems and particulate filters is further supporting segment growth.

LDV-Gasoline catalysts hold nearly 46% share of the auto catalyst market, making them the largest segment globally. The dominance of gasoline-powered passenger cars in North America, Asia-Pacific, and several emerging economies significantly contributes to segment expansion. Gasoline vehicle catalysts primarily utilize three-way catalyst technology to convert carbon monoxide, hydrocarbons, and nitrogen oxides into less harmful emissions. auto catalyst market Trends indicate rising demand for palladium-based catalyst formulations because gasoline engines increasingly require high-performance emission control systems. Manufacturers are continuously developing lightweight and compact catalyst substrates to improve fuel efficiency and vehicle performance.

To know how our report can help streamline your business, Speak to Analyst

HDV catalysts contribute around 32% share of the auto catalyst market due to growing emission control requirements within heavy-duty commercial transportation sectors. Heavy-duty vehicles such as trucks, buses, construction vehicles, and industrial transport fleets generate substantial exhaust emissions, creating strong demand for high-capacity catalyst systems. auto catalyst market Analysis indicates increasing adoption of selective catalytic reduction systems and diesel particulate filters across commercial vehicle fleets worldwide. Governments are implementing stricter regulations for freight transportation emissions, encouraging fleet operators to upgrade exhaust after-treatment technologies. Manufacturers are focusing on durable catalyst formulations capable of withstanding high operating temperatures and extended driving conditions.

Auto Catalyst Market Regional Outlook

North America

North America Auto Catalyst Market Share, 2026 (%)

To get more information on the regional analysis of this market, Download Free sample

North America holds approximately 26% share of the auto catalyst market and remains a major region for automotive emission control technologies due to strict environmental regulations and strong automobile production capacity. The United States dominates regional demand because federal emission standards require advanced catalytic converter systems across passenger and commercial vehicle categories. auto catalyst market Analysis indicates rising adoption of high-performance gasoline catalysts and selective catalytic reduction technologies throughout the region. Automotive manufacturers are increasingly investing in hybrid vehicle production, creating additional demand for optimized catalyst systems capable of operating under varying engine conditions. Canada also contributes significantly to market growth due to increasing environmental awareness and stricter transportation emission policies. Rising investments in clean mobility technologies and advanced exhaust after-treatment systems continue strengthening regional market development. Commercial transportation fleets across North America are rapidly upgrading heavy-duty vehicle catalyst systems to comply with emission standards for freight and logistics operations. auto catalyst market Trends further reveal increasing demand for lightweight catalyst substrates and durable ceramic honeycomb technologies.

Europe

Europe accounts for nearly 31% share of the auto catalyst market and remains one of the most technologically advanced regions for automotive emission control systems. Strict European vehicle emission regulations have significantly accelerated adoption of advanced catalyst technologies across passenger and heavy-duty vehicle categories. auto catalyst market Research Report findings indicate strong demand for diesel oxidation catalysts and selective catalytic reduction systems due to the region’s long-standing diesel vehicle infrastructure. Germany, France, Italy, and the United Kingdom remain key contributors to regional market growth because of their strong automotive manufacturing industries. Increasing investments in low-emission transportation systems and hybrid vehicle technologies are further supporting catalyst innovation throughout Europe. auto catalyst market Trends also highlight growing adoption of palladium-rich catalyst formulations designed for gasoline-powered passenger cars.

Germany auto catalyst market

Germany represents nearly 29% share of the Europe auto catalyst market due to its dominant automotive manufacturing sector and advanced emission control technology development. The country is home to major automobile producers and automotive component suppliers focusing heavily on vehicle efficiency and environmental sustainability. auto catalyst market Analysis in Germany highlights strong demand for gasoline and diesel catalyst systems integrated into passenger vehicles, luxury automobiles, and heavy commercial fleets. Manufacturers are investing significantly in selective catalytic reduction systems and lightweight catalyst substrates to comply with evolving European emission regulations. Hybrid vehicle development is also supporting demand for advanced catalyst formulations. Germany continues to lead innovation in catalyst durability, thermal resistance, and precious metal optimization technologies within the European automotive industry.

United Kingdom auto catalyst market

The United Kingdom accounts for approximately 16% share of the Europe auto catalyst market due to increasing focus on emission reduction technologies and sustainable automotive manufacturing. auto catalyst market Trends indicate rising demand for catalytic converters in passenger cars, commercial vans, and hybrid vehicles across the country. Government policies targeting urban air pollution reduction are encouraging adoption of advanced exhaust after-treatment systems. Automotive manufacturers and component suppliers in the UK are investing in catalyst technologies that improve fuel efficiency and reduce nitrogen oxide emissions. Demand for palladium-based gasoline catalysts is increasing due to the strong presence of gasoline-powered passenger vehicles. Recycling activities involving used catalytic converters are also growing rapidly across the United Kingdom automotive sector.

Asia-Pacific

Asia-Pacific holds approximately 35% share of the auto catalyst market and remains the largest regional automotive manufacturing hub globally. Countries such as China, Japan, India, and South Korea produce substantial volumes of passenger and commercial vehicles, creating strong demand for catalyst systems. auto catalyst market Insights reveal increasing implementation of stringent emission standards across emerging Asian economies to reduce urban air pollution and improve environmental sustainability. China dominates regional demand because of its massive automobile production capacity and rapidly evolving environmental regulations. Japan and South Korea continue investing heavily in advanced hybrid vehicle technologies and high-efficiency catalyst systems. Rising vehicle ownership rates and rapid urbanization are also contributing significantly to market expansion throughout Asia-Pacific. auto catalyst market Trends indicate increasing demand for lightweight catalysts, palladium-based formulations, and advanced ceramic substrates within the region. Manufacturers are expanding production facilities and investing in research activities focused on reducing precious metal dependency while improving catalyst performance.

Japan auto catalyst market

Japan contributes nearly 22% share of the Asia-Pacific auto catalyst market due to its advanced automotive engineering capabilities and strong hybrid vehicle production industry. Japanese automotive manufacturers are global leaders in fuel-efficient vehicle technologies, creating strong demand for high-performance catalyst systems. auto catalyst market Analysis indicates increasing adoption of lightweight and thermally durable catalyst substrates within passenger and hybrid vehicle categories. The country’s strict environmental regulations continue encouraging development of advanced catalytic converter technologies capable of minimizing emissions under varying driving conditions. Manufacturers are heavily investing in nanotechnology-based catalyst coatings and reduced precious metal formulations to improve operational efficiency and sustainability. Japan remains a key innovation center for automotive catalyst technology research and development throughout the Asia-Pacific region.

China auto catalyst market

China represents approximately 43% share of the Asia-Pacific auto catalyst market due to its dominant automobile manufacturing industry and rapidly strengthening environmental regulations. Increasing passenger vehicle production and rising commercial transportation activities are significantly supporting demand for advanced catalyst systems across the country. auto catalyst market Forecast studies indicate strong adoption of gasoline vehicle catalysts and selective catalytic reduction systems within both urban and industrial transportation fleets. Government initiatives focused on reducing air pollution are encouraging automakers to integrate advanced exhaust treatment technologies into newly manufactured vehicles. Domestic catalyst manufacturers are rapidly expanding production capacity and investing in improved precious metal recovery technologies. China continues to remain one of the largest growth markets for automotive catalyst systems globally.

Rest of World

The Rest of World region accounts for nearly 8% share of the auto catalyst market and includes growing automotive markets across Latin America, the Middle East, and Africa. Increasing urbanization, industrialization, and vehicle ownership are supporting rising demand for emission control technologies throughout these regions. auto catalyst market Analysis indicates that governments are gradually implementing stricter vehicle emission standards to reduce air pollution and improve environmental sustainability. Brazil and Mexico remain key contributors within Latin America because of expanding automobile manufacturing and commercial transportation sectors. Demand for gasoline and diesel catalyst systems is increasing due to rising passenger car sales and logistics activities. In the Middle East, growing infrastructure projects and freight transportation operations are supporting commercial vehicle catalyst demand. auto catalyst market Trends also reveal increasing investments in local catalyst manufacturing and automotive component production across emerging economies.

List of Top Auto Catalyst Companies

- BASF SE

- CDTi Advanced Materials Inc.

- Cataler Corporation

- Clariant Ltd.

- Corning Incorporated

- DCL International Inc.

- Eberspächer Group

- Ecocat India Pvt. Ltd.

- Faurecia (Forvia SE)

- Heraeus Precious Metals

- Honeywell International Inc.

- IBIDEN Co. Ltd

- Interkat Catalyst GmbH

- Johnson Matthey plc

- Klarius Products Ltd.

- Marelli Holdings

- NGK Insulators Ltd

Top Two Companies by Market Share

- BASF SE – Approximately 17% market share

- Johnson Matthey plc – Approximately 15% market share

Investment Analysis and Opportunities

The auto catalyst market is attracting substantial investments due to increasing environmental regulations and rising demand for advanced automotive emission control technologies. Automotive manufacturers and catalyst producers are investing heavily in research activities focused on improving catalyst efficiency, durability, and thermal resistance. auto catalyst market Opportunities are particularly strong in hybrid vehicle technologies, selective catalytic reduction systems, and lightweight catalyst substrate development.

Investments in precious metal recycling technologies are also increasing significantly because manufacturers aim to reduce dependency on newly mined platinum group metals. auto catalyst market Research Report findings reveal strong investment activity in nanotechnology-based catalyst coatings and alternative catalyst materials designed to improve performance while minimizing raw material costs. Emerging economies across Asia-Pacific and Latin America are witnessing expanding automotive production infrastructure, creating long-term investment opportunities for catalyst manufacturers and automotive component suppliers.

New Product Development

New product development within the auto catalyst market is heavily focused on improving emission reduction efficiency, reducing precious metal usage, and enhancing catalyst durability under extreme operating conditions. Manufacturers are increasingly developing advanced three-way catalyst systems capable of improving gasoline engine performance while reducing harmful exhaust emissions. auto catalyst market Trends indicate growing innovation in lightweight ceramic substrates and metallic catalyst supports designed to improve fuel economy and thermal efficiency.

Manufacturers are further focusing on sustainability through catalyst recycling technologies and environmentally friendly production methods. New palladium-rich catalyst formulations are gaining popularity due to increasing gasoline vehicle production globally. Research into low-temperature catalyst activation systems and improved exhaust treatment technologies continues accelerating innovation across the automotive catalyst sector. Smart catalyst monitoring technologies integrated with vehicle diagnostic systems are also emerging as an important product development trend.

Five Recent Developments (2023-2025)

- BASF SE expanded its automotive catalyst production capabilities for hybrid vehicle applications in 2024.

- Johnson Matthey plc introduced advanced low-emission catalyst technologies for gasoline passenger vehicles in 2025.

- Corning Incorporated developed lightweight ceramic substrate solutions designed for improved fuel efficiency in 2023.

- Faurecia (Forvia SE) strengthened investments in commercial vehicle exhaust after-treatment technologies in 2024.

- NGK Insulators Ltd expanded research activities focused on high-durability catalyst substrate materials in 2025.

Report Coverage of Auto Catalyst Market

The auto catalyst market Report provides comprehensive analysis of market trends, technological advancements, competitive landscape, regional performance, and future growth opportunities across the global automotive emission control industry. The report evaluates major catalyst types including LDV-Diesel, LDV-Gasoline, and HDV catalyst systems while examining their applications within passenger vehicles and commercial transportation sectors. auto catalyst market Research Report coverage includes detailed analysis of emission regulations, automotive production trends, and advancements in catalytic converter technologies influencing market expansion.

Request for Customization to gain extensive market insights.

The report further examines key growth drivers such as rising environmental concerns, stricter vehicle emission standards, and increasing hybrid vehicle adoption. Market restraints related to precious metal price volatility and supply chain complexities are also analyzed extensively. auto catalyst market Insights additionally highlight opportunities associated with low-emission transportation technologies, catalyst recycling systems, and advanced substrate innovations.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us