Automated Endoscope Reprocessors (AER) Market Size, Share & Industry Analysis, By Type (Single Basin and Dual Basin), By Loading Type (Top-Loading and Front-Loading), By Type of Endoscope Reprocessed (Flexible and Hybrid), By Portability (Stationary and Mobile), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

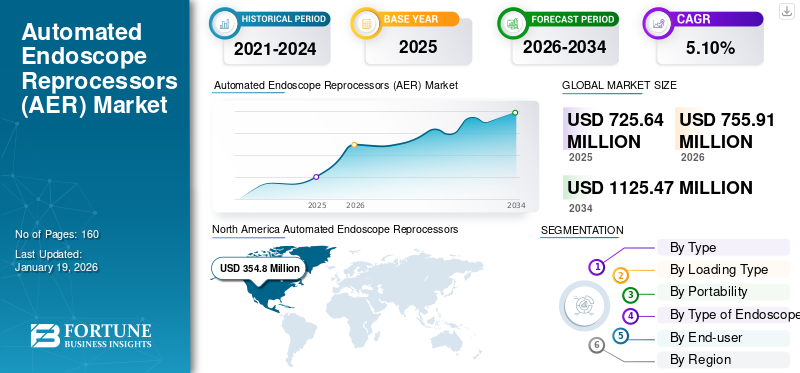

The global automated endoscope reprocessors (AER) market size was valued at USD 725.6 million in 2025. The market is projected to grow from USD 755.91 million in 2026 to USD 1,125.47 million by 2034, exhibiting a CAGR of 4.8% during the forecast period. North America dominated the automated endoscope reprocessors (AER) market with a market share of 48.89% in 2025.

Endoscope reprocessors are devices used in healthcare settings to clean and disinfect reusable endoscopes. These machines automate the process of high-level disinfection, ensuring consistent and effective sterilization of endoscopes to prevent infection transmission.

The increasing number of endoscopic procedures in healthcare settings is fueling the adoption of automated endoscope reprocessors (AER) to disinfect the devices and avoid spreading infections. This stimulates key companies to increase the supply of products globally, which is expected to drive market growth.

The prominent players in the market include Steris, Getinge, and others. These players focus on product advancements and strategic acquisitions to capitalize on the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increased Number of Endoscopic Procedures to Drive Automated Endoscope Reprocessor (AER) Demand

Recently, the growing incidence of conditions, such as gastrointestinal issues, respiratory diseases, and various types of cancer, has driven the demand for endoscopic diagnosis and treatment. This directly increases the demand for endoscopes and the need for efficient reprocessing solutions, including automated endoscope reprocessors (AER).

- For instance, according to the data published by the NCBI in May 2024, more than 17.7 million gastrointestinal (GI) endoscopic procedures are performed annually in the U.S.

Furthermore, an increasingly aging global population contributes to the rise in endoscopic procedures, as older individuals are more susceptible to various health conditions requiring endoscopic interventions. Such a scenario will drive the global automated endoscope reprocessors (AER) market growth during the forecast period.

Market Restraints

Limited Skilled Staff in Low-Income Countries May Hinder Market Growth

Adequate training for staff on proper reprocessing procedures is essential for efficacy and compliance, but this training can also be costly and time-consuming. As a result, a limited number of trained staff in low-income countries can operate such equipment.

- For instance, as of June 2024, the Royal Australian College of General Practitioners (RACGP) mentioned that healthcare practices must ensure that staff involved in reprocessing have received adequate training.

This factor may favor the manual cleaning and disinfection of endoscopes over advanced equipment such as automated endoscope reprocessors, thereby limiting their adoption and hampering the market growth.

Market Opportunities

Emerging Markets and Growing Investments to Represent Lucrative Growth Opportunity

Recently, there has been an increasing awareness of the risks associated with HAIs in emerging economies across Asia Pacific, Latin America, and the Middle East. AERs play a crucial role in reducing these risks by effectively disinfecting endoscopes. As the hospitals in these regions expand their surgical procedures and diagnostic capacities, the demand for minimally invasive surgeries and safe & efficient endoscope reprocessing has surged.

- For instance, in April 2025, Yashoda Hospitals launched a Center of Excellence for Robotic Neurosurgery and Neuro Endoscopy in Secunderabad, India.

Government-funded healthcare modernization programs, increasing awareness of hospital-acquired infections, and growing private sector investment fuel the need for high-performance automated reprocessors. This is expected to represent a significant opportunity for manufacturers to introduce cost-effective, compact, and portable reprocessing systems that cater to smaller healthcare facilities.

Market Challenges

High Initial Investment in Automated Endoscope Reprocessors (AER) to Limit Market Expansion

Advanced automated endoscope reprocessors (AER) require a significant upfront investment, which many smaller hospitals and clinics may be unable to afford. Additionally, this advanced equipment may necessitate upgrades to infrastructure, such as dedicated space, water supply, and ventilation, further increasing the overall cost.

Moreover, the recurring costs of high-level disinfectants and maintenance further increase the overall costs, making them less accessible and affordable to small healthcare facilities, which is expected to limit market expansion.

Automated Endoscope Reprocessors (AER) Market Trends

Advancement in Automated Endoscope Reprocessors (AER) Leads to New Market Trends

Healthcare facilities are moving away from manual disinfection methods due to inefficiency and a higher risk of human error. Automated endoscope reprocessors (AERs) offer consistent, high-level disinfection while minimizing technician exposure to harmful chemicals. In addition, there is a rising interest in smart reprocessors equipped with digital tracking, data logging, and connectivity features that support traceability and regulatory compliance. These systems integrate with hospital IT infrastructures, enabling real-time monitoring and documentation of the reprocessing cycle.

- For instance, in June 2022, Getinge released an updated version of its ED-Flow automated endoscope reprocessor, incorporating enhanced digital connectivity and data management features.

Moreover, as healthcare providers face growing pressure to prevent healthcare-associated infections (HAIs), adopting advanced AERs is becoming a critical component of infection control protocols. This trend is further supported by stricter guidelines from global bodies such as the CDC, ESGE, and FDA, which mandate standardized and validated reprocessing procedures for reusable medical instruments, including endoscopes.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

High-Level Disinfecting Ability Fueled Dual Basin Segment Growth

Based on type, the market is segmented into single basin and dual basin.

The dual basin segment held the largest market share in 2024. Dual-basin automated endoscope reprocessors (AERs) are generally more prevalent and preferred due to their ability to minimize cross-contamination risks and enhance disinfection efficacy. They allow for a dual-basin design that allows separate chambers for cleaning and disinfection, leading to improved hygiene and reduced potential for infection transmission.

- For instance, as of June 2025, STERIS mentioned that the dual basins offer high-level disinfection in either simultaneous or independent cycles.

The single basin segment accounted for the second-largest share of the global market in 2024. Single-basin systems are more compact, making them suitable for facilities with limited space. Moreover, they are less expensive than dual-basin systems, making them a more affordable option for smaller clinics. These factors are expected to boost the segment’s growth.

By Loading Type

Front-Loading Systems Led Due to Their Compatibility with Various Endoscopes

Based on loading type, the market is divided into top-loading and front-loading.

The front-loading segment dominated the market in 2024. Front-loading models are generally more widely adopted due to their integration into standard workflows, compatibility with various endoscopes, and capacity for high-throughput processing. In consideration of this, key players are focusing on the development and presentation of their products, thereby contributing to the market growth.

- For instance, in September 2021, Steelco S.p.A. presented EW 1 S MAXI, the latest AER in the global market at the forefront of innovation.

The top-loading segment held the second-largest share in 2024. Top-loading models offer advantages in limited space or specialized needs, which is driving their demand among smaller clinics. This is expected to fuel the segment’s growth in the forthcoming years.

By Portability

Stationary AERs Dominated, Driven by Their High Efficiency

Based on portability, the market is bifurcated into stationary and mobile.

The stationary segment dominated the market in 2024. The growth of the segment can be attributed to its high efficiency, improved consistency, and better infection control, primarily through automation and standardization of the reprocessing steps. This may increase their adoption in the global healthcare facilities.

The mobile segment held a substantial market share in 2024. The growth is attributable to increasing preference for mobile over stationary devices due to their portability and flexibility, allowing for easier movement and usage in a healthcare facility, especially in a busy environment.

By Type of Endoscope Reprocessed

Flexible Segment Held Dominance Due to Rising Preference by Healthcare Professionals

Based on the type of endoscope reprocessed, the market is bifurcated into flexible and hybrid.

The flexible segment dominated the market in 2024. The growth of this segment can be attributed to the high usage of flexible endoscopes in several procedures. This may increase the requirement for disinfection of flexible endoscopes through AERs in several healthcare settings.

The hybrid segment held a substantial market share in 2024. Healthcare professionals are opting for the hybrid model of AER to fulfill the need to disinfect both rigid and flexible endoscopes in the same system. This can save space and expenses. Such benefits of the hybrid model are expected to drive the segment’s growth in the coming years.

By End-user

Hospitals & ASCs Led Market Due to Rising Cases of HAIs in These Settings

Based on end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

The hospital & ASCs segment dominated the market in 2024. The growth is attributed to the increasing incidence of HAIs in patients undergoing endoscopies in these settings. This is increasing the usage of automated endoscope reprocessors (AER) to sterilize the endoscopes in these settings.

The specialty clinics segment accounted for the second-largest global market share in 2024. The growth can be attributed to the increasing number of cardiology, gastroenterology, and other specialty clinics as well as professionals, which is expected to contribute to many endoscopy procedures globally. This is anticipated to drive the segment’s growth in the coming years.

- For instance, according to the data published by the American Heart Association in September 2023, there were 47,225 cardiologists in the U.S. in the same year.

AUTOMATED ENDOSCOPE REPROCESSORS (AER) MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Automated Endoscope Reprocessors (AER) Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America Dominated Market Owing to Well-established Healthcare Infrastructure

The North America market accounted for USD 354.8 million in 2025, representing 48.89% of the global industry, and is expected to reach USD 368.87 million in 2026. The North America automated endoscope reprocessors (AER) market size stood at USD 341.9 million in 2024. The region’s growth is attributed to a well-established healthcare infrastructure, contributing to many endoscopic procedures in the region. This may boost the demand for disinfection solutions such as endoscopic reprocessors in the regional market.

In the U.S., gastrointestinal (GI) endoscopic procedures are contributing to automated endoscope reprocessors (AER) for disinfection of the device, which is expected to drive the market growth.

- For instance, according to the article published by the NCBI in May 2022, gastrointestinal (GI) endoscopic procedures contribute to over 68.0% of all endoscopic procedures in the U.S.

Europe

Europe recorded a market size of USD 208.94 million in 2025, capturing 28.79% of the global market share, and is projected to reach USD 218.55 million in 2026. Strong regulatory frameworks and a focus on patient safety in the region are expected to bolster the region's growth. Moreover, increasing investments in public healthcare systems and hospital hygiene initiatives are creating a favorable environment for replacing the older manual reprocessing methods with standardized, automated solutions that ensure consistent disinfection outcomes.

- For instance, according to the data published by Queen Margaret University in January 2024, the NHS annual budget has increased by 3.4% in the past five years.

Asia Pacific

In 2025, Asia Pacific represented USD 102.92 million, accounting for 14.18% of the worldwide market, and is projected to grow to USD 108.29 million in 2026. The region's increasing bronchoscopy procedures and growing private hospitals are increasing the need for disinfection solutions for medical devices, including endoscopes. This is further expected to spur the usage of automated endoscope reprocessors, driving the region’s market growth in the forthcoming years.

- For instance, according to the data published by the NCBI in November 2023, around 10.0 – 20.0% of admitted patients are affected by nosocomial infections in India.

Middle East & Africa

Middle East & Africa contributed 2.94% to the global market in 2025, with a valuation of USD 21.34 million, and is projected to reach USD 21.74 million in 2026. Middle East & Africa automated endoscope reprocessors (AER) market accounted for a lower share in 2024 compared to other regions. The rising awareness of infection control and investments in hospital hygiene are gradually driving the adoption of automated reprocessing systems, particularly in urban centers across Brazil and Mexico. The countries in the Gulf Cooperation Council are witnessing an increase in endoscopic procedural volumes and infrastructure upgrades as part of healthcare diversification plans.

Latin America

The Latin America market was valued at USD 37.64 million in 2025, capturing 5.19% of global revenue, and is estimated to reach USD 38.46 million in 2026.

COMPETITIVE LANDSCAPE

Key Market Players

Strong Focus on New Product Innovations to Enhance Market Share of STERIS and Getinge

STERIS and Getinge held the largest global automated endoscope reprocessors (AER) market share in 2024. The dominance is attributed to their high focus on updating existing products and launching new ones to diversify their portfolios.

Furthermore, other players such as ASP (Fortive), Olympus Corporation, and others focus on strategic alliances and geographic expansions to expand their global product reach. Such initiatives will help these players gain a significant market share in the coming years.

LIST OF KEY AUTOMATED ENDOSCOPE REPROCESSOR (AER) COMPANIES PROFILED

- STERIS (U.S.)

- Getinge (Sweden)

- ASP (Fortive) (U.S.)

- Olympus Corporation (Japan)

- Steelco S.p.A. (Italy)

- ARC Healthcare Solutions Inc. (Canada)

- CHOYANG (South Korea)

- NUOVA SB SYSTEM S.R.L. (Italy)

KEY INDUSTRY DEVELOPMENTS

- September 2024– Olympus Corporation announced the opening of “Sapphire,” the first flexible endoscope sterilization facility located in Melbourne, Australia, to provide sterilization services to Clinical facilities.

- March 2023 – Getinge announced the U.S.-based Ultra Clean Systems acquisition for USD 16.0 million. With the addition of Ultra Clean’s expertise and technology, Getinge expanded its offering to sterile reprocessing departments in North America.

- January 2021 – STERIS signed a definitive agreement to acquire Cantel Medical and enter the automated endoscope reprocessors (AER) market.

- October 2020– Olympus Corporation announced the market availability of the OER-Elite, its next-generation automated endoscope reprocessor (AER) in the global market.

- April 2019 – Fortive completed the acquisition of the ASP business from Ethicon, Inc. for around USD 2.7 million to enter the automated endoscope reprocessors (AER) market.

REPORT COVERAGE

The global automated endoscope reprocessors market report provides a detailed analysis of key aspects, such as major companies, competitive landscape, type, portability, loading type, type of endoscope reprocessed, and end-user. Additionally, it includes market dynamics and insights into the latest market trends and highlights key industry developments. Furthermore, the report provides a detailed analysis of several factors driving the market's growth in the coming years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.10% from 2026-2034 |

|

Unit |

Value (USD million) |

|

Segmentation |

By Type

|

|

By Loading Type

|

|

|

By Portability

|

|

|

By Type of Endoscope Reprocessed

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 725.6 million in 2025 and is projected to record a valuation of USD 1,125.47 million by 2034.

In 2025, the market value stood at USD 725.64 million.

The market will exhibit a steady CAGR of 5.10% during the forecast period of 2026-2034.

By type, the dual basin segment led the market.

The rising number of endoscopic procedures and technological advancements are expected to drive the market growth.

STERIS and Getinge are the major players in the market.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us