Automotive Artificial Intelligence (AI) Market Size, Share & Industry Analysis, By Application (Advanced Driver Assistance Systems (ADAS), Autonomous Driving Systems, Driver & Occupant Monitoring Systems, Predictive Maintenance & Vehicle Diagnostics, and Infotainment & Voice Assistants & Personalization), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Propulsion Type (ICE and Electric), By Level of Driving Automation (Level 1–2, Level 3, and Level 4 & Above), By Offering (Hardware, Software, and AI Services & Data Platforms), and Regional Forecast, 2026-2034

Automotive Artificial Intelligence Market Overview

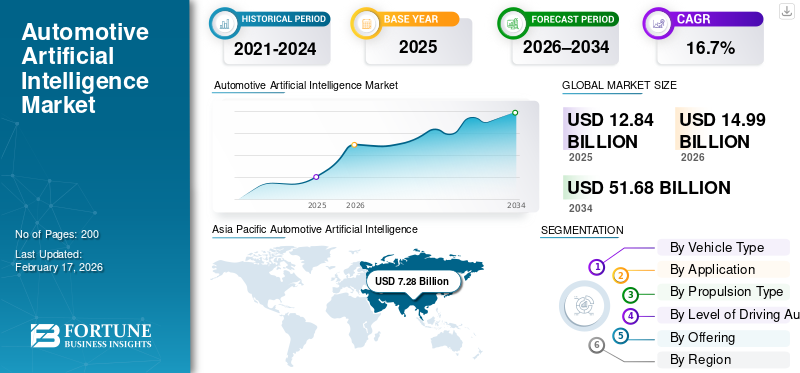

The global automotive Artificial Intelligence (AI) market size was valued at USD 12.84 billion in 2025. The market is projected to grow from USD 14.99 billion in 2026 to USD 51.68 billion by 2034, exhibiting a CAGR of 16.7% during the forecast period. Asia Pacific dominated the Automotive artificial intelligence market with a market share of 56.7% in 2025.

Automotive Artificial Intelligence (AI) refers to the use of machine learning, computer vision, and data-driven algorithms, allowing vehicles to perceive, decide, learn, and optimize driving, safety, diagnostics, and user experiences. Key market drivers include rising ADAS and autonomous adoption, vehicle electrification, connected cars, stricter safety regulations, demand for personalization, real-time data analytics, and OEM focus on software-defined vehicles.

Major players in the market include NVIDIA, Qualcomm, Bosch, Continental, Intel (Mobileye), and Microsoft, competing through advanced AI chips, autonomous driving software, edge computing, cloud platforms, and data-driven vehicle intelligence solutions.

Download Free sample to learn more about this report.

AUTOMOTIVE ARTIFICIAL INTELLIGENCE (AI) MARKET TRENDS

Edge AI and In-Vehicle Computing to Transform Vehicle Architectures

One of the key trends is the rapid shift toward edge AI and centralized in-vehicle computing architectures. Processing AI workloads directly within vehicles reduces latency, improves reliability, and supports real time decision-making for safety-critical functions. Automakers are consolidating electronic control units into domain and zonal architectures powered by AI accelerators. This trend supports advanced perception, sensor fusion, and autonomous capabilities while reducing system complexity and long-term software maintenance costs.

- In January 2026, NVIDIA unveiled the Alpamayo family of open-source AI driven models, simulation tools, and extensive datasets to accelerate safe, neural networks, and reasoning-based Level 4 autonomous vehicle development, including a 10B-parameter vision language action model and 1,700+ hours of edge-case data. Alpamayo integrates with NVIDIA DRIVE compute for robust simulation, human-like reasoning, and improved decision transparency across rare driving scenarios.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of ADAS and Autonomous Features to Drive AI Demand

The growing integration of ADAS and autonomous functionalities is a major driver for automotive artificial intelligence (AI) market demand. Features such as lane-keeping assistance, adaptive cruise control, automatic emergency braking, and driver monitoring systems rely heavily on AI algorithms. Automakers are increasingly embedding AI technology to enhance safety, comply with regulatory mandates, and differentiate vehicles through intelligent features. Rising consumer awareness for safety and convenience further accelerates OEM investment in AI-powered perception, decision-making, and real-time vehicle control systems.

- In January 2026, Texas Instruments expanded its automotive portfolio with TDA5 SoCs delivering up to 1200 TOPS edge AI with greater than 24 TOPS/W efficiency, an AWR2188 eight-by-eight 4D radar transceiver with 30% faster detection (>350 m), and a DP83TD555J-Q1 10BASE-T1S Ethernet PHY to simplify networking, accelerating advanced driver assistance systems adas, Level 3 autonomy, and software-defined vehicles.

MARKET RESTRAINTS

High Development Costs and Talent Shortage to Restrain Market Adoption

Automotive Artificial Intelligence (AI) development requires significant investment in high-performance computing hardware, large datasets, simulation environments, and specialized engineering talent. The shortage of skilled AI and automotive software professionals increases development timelines and costs. Smaller OEMs and Tier-2 suppliers often struggle to justify high upfront investments, slowing adoption. Additionally, long validation cycles and stringent automotive safety standards further limit rapid deployment, particularly for advanced autonomous and self-learning AI applications.

MARKET CHALLENGES

Data Privacy, Cybersecurity, and Regulatory Complexity to Challenge Market Growth

Managing data privacy, cybersecurity, and regulatory compliance remains a critical challenge in automotive automotive artificial intelligence (AI) market growth. AI powered systems process vast amounts of driver behavior, vehicle, and location data, increasing exposure to cyber threats and misuse. Differing regulations across regions complicate global AI deployment strategies for OEMs. Ensuring secure data handling, transparent AI decision-making, and compliance with evolving safety and privacy regulations adds complexity and cost, particularly for connected and autonomous vehicle applications.

MARKET OPPORTUNITIES

Software-Defined Vehicles to Create New Revenue Opportunities

The shift toward software-defined vehicles presents strong opportunities for automotive automotive Artificial Intelligence (AI) vendors. AI enables continuous feature upgrades, over-the-air updates, predictive maintenance, and data monetization across a vehicle’s lifecycle. OEMs can generate recurring revenues through subscription-based services, AI-driven infotainment, and personalized user experiences. This transition also opens opportunities for cloud providers, AI platform developers, and data analytics firms to partner with automakers and expand their automotive digital ecosystems.

- In January 2026, Volkswagen Group and Qualcomm signed a Letter of Intent for a long-term supply agreement to deliver Snapdragon Digital Chassis high-performance SoCs for advanced infotainment and connectivity in Volkswagen’s zonal Software-Defined Vehicle (SDV) architecture, starting 2027, also supporting highly automated driving through the Automated Driving Alliance partnership.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Strong Demand for AI-Driven Safety, Personalization, and Connectivity to Sustain Passenger Cars Segment’s Dominance

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment dominates the market due to high production volumes and rapid integration of AI-powered features such as ADAS, driver monitoring, voice assistants, and personalized infotainment. Mass-market and premium passenger vehicles increasingly embed AI to enhance safety, comfort, and user experience. Strong consumer demand, regulatory safety mandates, and faster adoption of software-defined architectures in passenger cars support sustained AI deployment and continuous feature upgrades across global markets.

- In December 2025, Rivian detailed its autonomous driving AI for the upcoming R2 SUV, featuring an in-house Rivian Autonomy Processor (RAP1) with 1600 trillion operations per second, a 5 nm chip, and LiDAR plus 11 cameras and five radars to enable hands-free, Level 4-capable driving via over-the-air updates and a new autonomy+ software subscription.

The commercial vehicles segment is the fastest growing, expanding at a CAGR of 17.6%. Rising fleet electrification, connected logistics, and demand for AI-enabled predictive maintenance, route optimization, and driver monitoring accelerate AI adoption in LCVs, particularly across e-commerce and last-mile delivery applications.

By Application

Safety Regulations and Mass Adoption of Driver Assistance Features to Propel ADAS Segment’s Dominance

Based on application, the market is segmented into Advanced Driver Assistance Systems (ADAS), autonomous driving systems, driver & occupant monitoring systems, predictive maintenance & vehicle diagnostics, and infotainment & voice assistants & personalization.

The ADAS segment dominates the market due to widespread regulatory mandates and high consumer acceptance of safety-enhancing features. AI-powered functions such as automatic emergency braking, lane-keeping assist, adaptive cruise control, and driver monitoring are increasingly getting standardized across vehicle classes. High deployment volumes, proven safety benefits, and cost-effective scalability enable ADAS to achieve faster penetration than fully autonomous systems, sustaining its dominant share globally.

- In January 2026, Hyundai Mobis and Qualcomm signed an MoU at CES 2026 to co-develop ADAS and SDV solutions, initially using the Snapdragon Ride Flex SoC for advanced driving and parking systems, combining sensor fusion, system integration, and high-performance SoC expertise for emerging markets such as India.

Autonomous driving systems represent the fastest-growing segment, expanding at a CAGR of 19.4% during the forecast period. Advancements in AI perception, sensor fusion, simulation, and computing platforms, combined with robotaxi pilots and commercial autonomy programs, are accelerating adoption despite phased regulatory approvals.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

ICE Segment Leads with Large Installed Base and Gradual AI Integration

By propulsion type, the market is divided into ICE and electric.

The ICE segment dominates the market of automotive Artificial Intelligence (AI) due to its vast global vehicle parc and continued production across emerging and developed markets. Automakers are steadily integrating AI-driven ADAS, diagnostics, predictive maintenance, and infotainment into ICE vehicles to meet safety regulations and consumer expectations. Increasing AI adoption in existing ICE platforms, combined with longer model lifecycles and high sales volumes, sustains strong and stable demand for automotive Artificial Intelligence (AI) solutions.

The electric vehicle segment is the fastest growing, expanding at a 21.4% CAGRduring the forecast period. Software-centric architectures, centralized computing, battery optimization, and autonomous-ready platforms make EVs ideal for technology advanced AI deployment, accelerating adoption across passenger and commercial electric vehicles.

- In 2024, according to IEA, global electric vehicle sales surpassed 17 million units, accounting for over 20% of total global passenger vehicle sales.

By Level of Driving Automation

Regulatory Acceptance and Cost-Effective Deployment to Drive Level 1–2’s Dominance

By level of driving automation, the market is categorized into Level 1–2, Level 3, and Level 4 & above.

Level 1–2 driving automation level dominates the market due to broad regulatory approval, affordability, and mass-market applicability. AI-enabled features such as adaptive cruise control, lane centering, and collision avoidance are widely deployed across vehicle segments. OEMs prioritize these systems to enhance safety and meet compliance requirements while maintaining manageable costs, resulting in high production volumes and consistent AI integration across global vehicle platforms.

Level 4 and above level of driving automation is the fastest-growing segment, expanding at a CAGR of 20.6%. Progress in AI perception, computing power, and controlled-environment deployments such as robotaxis and autonomous logistics vehicles is accelerating commercialization.

- In January 2026, Lucid announced that its Level 4 autonomous driving technology, developed with Uber and Nuro and built on the Lucid Gravity EV platform, will be expanded into future retail electric vehicles, aiming to bring robotaxi-grade AI and sensor systems to consumer models starting in 2027. Early prototypes are in real-world testing with advanced sensor arrays and scalable autonomy software.

By Offering

High Demand for Robust Computing, Sensors, and Edge Processing Boosts Hardware Segment’s Leadership

By offering, the market is trifurcated into hardware, software, and AI services & data platforms.

Hardware holds the largest share in the market due to strong demand for AI chips, GPUs, domain controllers, cameras, radar, LiDAR, and high-performance ECUs. Advanced driver assistance and autonomous functions require robust onboard computing and sensor fusion at the vehicle level. Continuous upgrades in processing power, real-time inference capabilities, and safety-certified hardware platforms drive sustained investment by OEMs and Tier-1 suppliers.

- In December 2025, Bosch unveiled its AI-Cockpit at CES, featuring an NPU-accelerated central domain controller with multimodal voice, face and gesture recognition, enhanced AI assistants, and predictive personalization. The platform integrates sensor fusion, real-time AI workloads, and OTA updates to enable safe, intuitive HMI while reducing electrical complexity across vehicle functions.

AI services and data platforms are the fastest-growing segment, expanding at a CAGR of 18.2%. Growing reliance on cloud analytics, simulation, fleet learning, deep learning, over-the-air updates, and data monetization accelerates demand beyond vehicle hardware.

Automotive Artificial Intelligence (AI) Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Artificial Intelligence (AI) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the automotive Artificial Intelligence (AI) market share due to its massive vehicle production base, strong presence of EV manufacturers, and rapid adoption of connected and software-defined vehicles. China, Japan, and South Korea lead the AI integration in ADAS, autonomous driving, and smart cockpits. Government support for EVs and intelligent mobility, expanding semiconductor ecosystems, and cost-efficient manufacturing further accelerate AI deployment across passenger and commercial vehicles in the region. The region is also the fastest growing in the global market.

- In October 2025, the Taiwan AI Automotive Alliance was launched by 12 leading Taiwanese firms to accelerate automotive AI ecosystems, focusing on AI chips, perception software, V2X connectivity, and standards development. The alliance aims to strengthen local supply chains, foster joint R&D, and enhance Taiwan’s role in global intelligent vehicle platforms, leveraging collective expertise in semiconductors and automotive electronics.

China Automotive Artificial Intelligence (AI) Market

The China market in 2026 is estimated to be around USD 4.90 billion, accounting for roughly 32.7% of global market revenues. China shows dominance in the Asia Pacific market, driven by autonomous driving pilots, strong EV penetration, and heavy investments in AI chips and software platforms.

Japan Automotive Artificial Intelligence (AI) Market

The Japan market in 2026 is estimated to be around USD 1.26 billion, accounting for roughly 8.4% of global market revenues. Growth of the country’s market is supported by ADAS innovation, robotics expertise, OEM-led AI integration, and safety-focused regulations.

India Automotive Artificial Intelligence (AI) Market

The India market in 2026 is estimated at around USD 0.96 billion, accounting for roughly 6.4% of global market revenues. Rapid growth in India stems from connected vehicles, cost-optimized ADAS adoption, EV startups, and digital mobility initiatives.

Europe

Europe holds the second-largest share of the market, growing at a CAGR of 14.9%. The Europe market growth is driven by stringent vehicle safety regulations and high adoption of advanced driver assistance systems. Premium and luxury automakers actively integrate AI for autonomous features, driver monitoring, and personalization. Strong R&D capabilities, early technology adoption, and regulatory emphasis on safety, emissions reduction, and smart mobility support steady AI investments across the region.

- In October 2025, PlusAI and IVECO launched Southern Europe’s first Level 4 autonomous trucking program, integrating PlusAI’s SuperDrive AI virtual driver into two IVECO S-Way heavy-duty trucks for multi-year tests on a 300 km freight corridor between Madrid and Zaragoza with safety operators aboard. The initiative accelerates autonomous freight deployment and expands PlusAI’s commercial roadmap toward factory-built autonomous trucks.

Germany Automotive Artificial Intelligence (AI) Market

The Germany market in 2026 is estimated at around USD 0.73 billion, accounting for roughly 4.9% of global market revenues. Germany market is fueled by premium OEMs, industry 4.0 integration, autonomous testing, and strong supplier ecosystems.

U.K. Automotive Artificial Intelligence (AI) Market

The U.K. market in 2026 is estimated at around USD 0.17 billion, accounting for roughly 1.1% of global market revenues. Expansion of the market U.K. is driven by AI software development, autonomous trials, mobility services, and supportive regulatory frameworks.

North America

North America ranks as the third-largest in the global market, supported by strong innovation ecosystems and early adoption of autonomous and connected vehicle technologies. The region benefits from the presence of leading AI chipmakers, software firms, and autonomous driving developers. High consumer demand for advanced safety features, extensive testing of self-driving technologies, and growing commercial fleet digitization to sustain market expansion across passenger and commercial vehicle segments.

- In October 2025, General Motors launched an AI-powered conversational assistant supporting eyes-off driving, integrating natural language processing with ADAS and hands-free Super Cruise. The system enables voice-based navigation, vehicle control, and contextual responses while maintaining safety compliance across GM’s software-defined vehicle platform.

U.S. Automotive Artificial Intelligence (AI) Market

The U.S. market in 2026 is estimated at around USD 1.86 billion, accounting for roughly 12.4% of global market revenues. The U.S. dominates the North American market due to strong presence of AI software firms, semiconductor leaders, and autonomous vehicle developers. High ADAS penetration, extensive robotaxi trials, and large connected fleet deployments drive sustained AI adoption.

Rest of the World

The Rest of the World market is expanding steadily as emerging economies adopt connected vehicle technologies and basic AI-enabled safety systems. Growth is supported by improving digital infrastructure, rising vehicle ownership, and gradual regulatory alignment with global safety standards. Commercial fleets increasingly adopt AI for telematics, predictive maintenance, and driver monitoring. However, adoption remains selective due to cost sensitivity and limited autonomous readiness across several developing regions.

- In October 2025, at GITEX Global 2025, the UAE unveiled fully electric AI-powered patrol cars equipped with six high-resolution cameras and advanced AI to scan up to 10 m around the vehicle, perform real-time facial and license-plate recognition, cross-reference immigration databases, and instantly alert authorities to visa or residency violations. The system integrates heat-map analytics and live dashboards for officers, with deployment in Dubai set for early 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Platforms, Autonomous Innovation, and Software Ecosystems Powered by the Key Market Players Define the Competitive Intensity

The automotive Artificial Intelligence (AI) market is moderately consolidated, led by global technology firms and Tier-1 automotive suppliers with strong software, semiconductor, and data capabilities. Key players such as NVIDIA, Qualcomm, Bosch, Continental, Intel (Mobileye), and Microsoft, compete through AI compute platforms, autonomous driving stacks, and cloud-based vehicle intelligence. Competitive advantage is driven by scalable AI architectures, OEM partnerships, and end-to-end software ecosystems. Companies focus on edge AI, over-the-air updates, and data platforms.

- In September 2025, at IAA Mobility 2025 in Munich, NVIDIA showcased its cloud-to-car AI platform redefining vehicles as AI-defined machines, with an end-to-end compute stack (DGX, Omniverse/Cosmos, DRIVE AGX) enabling real-time sensor processing, high-fidelity simulation, and unified safety via NVIDIA Halos, accelerating safer autonomous driving and software-defined vehicles globally.

LIST OF KEY AUTOMOTIVE ARTIFICIAL INTELLIGENCE (AI) COMPANIES PROFILED

- NVIDIA (U.S.)

- Intel Mobileye (Israel)

- Qualcomm Technologies (U.S.)

- Bosch (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Aptiv PLC (Ireland)

- Valeo (France)

- DENSO Corporation (Japan)

- Hyundai Mobis (South Korea)

- Baidu (China)

- Huawei Intelligent Automotive Solutions (China)

- XPeng Motors (China)

- Tesla, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Mobileye announced the acquisition of Mentee Robotics to accelerate its Physical AI roadmap, combining autonomous driving intelligence with humanoid robotics capabilities, strengthening perception, planning, and real-world decision-making technologies beyond vehicles into embodied AI systems.

- January 2026: Sony Honda Mobility announced advancements for AFEELA, integrating next-generation AI, real-time sensing, and immersive digital experiences. The platform emphasizes AI-powered interaction, cloud connectivity, and autonomous-ready architectures ahead of commercial rollout of its flagship electric vehicle.

- January 2026:ai and BAIC BJEV launched an expanded strategic partnership to scale Level 4 autonomous driving, focusing on robotaxi fleet expansion, mass-production validation, and AI-driven perception and planning systems for optimizing urban Chinese traffic environments.

- January 2026: XPeng outlined its 2026 flagship vehicle launch strategy, highlighting strong sales momentum and major AI breakthroughs in autonomous driving, large-model AI, and smart cockpits, reinforcing its ambition to evolve from an EV maker into a global AI-driven mobility technology company.

- September 2025: Sonatus unveiled AI Director, an edge AI orchestration platform enabling scalable, in-vehicle intelligence. The solution dynamically manages AI workloads across ECUs, supporting real-time perception, personalization, and OTA-deployed AI applications in software-defined vehicles.

- September 2025: ECARX powered the global launch of Geely Galaxy M9, delivering next-generation smart cockpit and ADAS capabilities using high-performance SoCs, AI voice interaction, multi-screen integration, and centralized computing for software-defined vehicle architectures.

- March 2025: General Motors announced expanded collaboration with NVIDIA, adopting DRIVE AGX platforms for future vehicles to enable AI-powered autonomous driving, advanced simulation, and centralized vehicle computing across GM’s next-generation software-defined vehicle programs.

- February 2025: Stellantis strengthened its strategic partnership with Mistral AI to deploy generative AI across customer experience, vehicle engineering, and manufacturing, leveraging large language models to enhance design efficiency, in-car assistants, and operational productivity.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 16.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Application, By Propulsion Type, By Level of Driving Automation, By Offering, and By Region |

|

By Vehicle Type |

· Passenger Cars · Commercial Vehicles |

|

By Application |

· Advanced Driver Assistance Systems (ADAS) · Autonomous Driving Systems · Driver & Occupant Monitoring Systems · Predictive Maintenance & Vehicle Diagnostics · Infotainment & Voice Assistants & Personalization |

|

By Propulsion Type |

· ICE · Electric |

|

By Level of Driving Automation |

· Level 1–2 · Level 3 · Level 4 & Above |

|

By Offering |

· Hardware · Software · AI Services & Data Platforms |

|

By Region |

· North America (By Vehicle Type, By Application, By Propulsion Type, By Level of Driving Automation, By Offering, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Vehicle Type, By Application, By Propulsion Type, By Level of Driving Automation, By Offering, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Vehicle Type, By Application, By Propulsion Type, By Level of Driving Automation, By Offering, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Vehicle Type, By Application, By Propulsion Type, By Level of Driving Automation, and By Offering) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 12.84 billion in 2025 and is projected to reach USD 51.68 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 7.28 billion.

The market is expected to exhibit a CAGR of 16.7% during the forecast period.

The passenger cars segment leads the market in terms of vehicle type.

Rising adoption of ADAS and autonomous features to drive AI demand.

Key players in the market include NVIDIA, Qualcomm, Bosch, Continental, Intel (Mobileye), and Microsoft.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us