Automotive Balance Shaft Market Size, Share & Industry Analysis, By Engine Type (Inline 3 Cylinder, Inline 4 Cylinder, Inline 5 Cylinder, and V6 Cylinder), By Manufacturing Process (Forging and Casting), By Vehicle Type (Passenger Cars, LCV, and HCV), and Regional Forecast, 2026-2034

AUTOMOTIVE BALANCE SHAFT MARKET SIZE AND FUTURE OUTLOOK

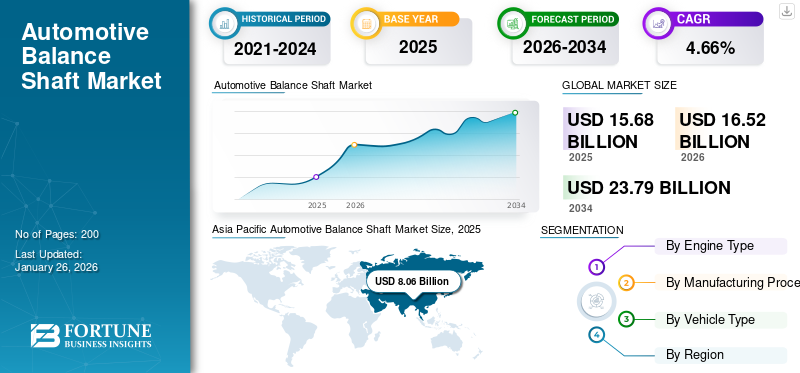

The automotive balance shaft market size was valued at USD 15.68 billion in 2025. The market is projected to grow from USD 16.52 billion in 2026 to USD 23.79 billion by 2034, exhibiting a CAGR of 4.66% Asia Pacific dominated the global market with a share of 51.42% in 2025.

Automotive balance shafts are essential parts in internal combustion engines, mainly intended to minimize vibrations created by the engine's functioning. Their primary function is to neutralize unbalanced dynamic forces, which improves engine stability and efficiency. Balance shafts are made up of a pair of weighted shafts that rotate in opposite directions at double the engine's speed. This arrangement produces centrifugal forces that counterbalance the vertical second-order forces generated by the engine, resulting in smoother operation.

The market growth is anticipated to grow at a significant in upcoming years owing to the increasing demand for passenger cars, light commercial vehicles, and heavy commercial vehicles. For instance, in 2024 year, new car registrations increased slightly by 0.8%, totaling approximately 10.6 million units. Spain continued to demonstrate resilience with a robust growth rate of 7.1%.

The global automotive balance shaft market is fragmented, with several global and regional market players involved in this industry. Prominent key players such as MAT Foundry Group Ltd., Musashi Seimitsu Industry Co., Ltd., American Axle & Manufacturing, Inc., Otics Corporation, SAC Engine Components Pvt. Ltd., and others.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Consumer Demand for Quieter Vehicles to Fuel the Growth of the Market

The growth of the automotive balance shaft market is anticipated to be driven by the increasing importance of noise, vibration, and harshness (NVH), shaped by evolving standards and technological advancements. With a growing emphasis on quieter and more comfortable driving experiences, vehicle manufacturers are being pushed to improve their designs to comply with stringent NVH benchmarks.

In today’s market, consumers expect vehicles that deliver a serene and smooth ride. This demand prompts manufacturers to concentrate on lowering NVH levels, which can be effectively addressed by implementing balance shafts into engine designs. Balance shafts are instrumental in reducing vibrations that lead to noise and discomfort inside the vehicle, making them vital for achieving NVH compliance.

In addition, automotive manufacturers must adhere to various NVH regulations to ensure both vehicle safety and passenger comfort. Failing to meet these standards can result in poor sales and harm to brand image. Therefore, the inclusion of balance shafts is crucial in engine design, as they are essential for controlling vibrations that could surpass acceptable thresholds.

The continues innovations in NVH testing technologies enable more accurate measurements and evaluations of vehicle performance across various operating conditions. This has heightened the awareness of balance shafts play in addressing particular NVH challenges, motivating manufacturers to invest in their development and application.

Furthermore, the shift towards a comprehensive vehicle design approach, where every component is fine-tuned for optimal performance, has led to balance shafts being recognized as vital elements of the overall NVH strategy. This focus is driving advancements in balance shaft technology, leading to more enhanced designs that meet effectively ever-evolving NVH requirements.

Market Restraints

Increasing Shift Toward Electric Vehicles (EVs) May Hamper Market Growth

The shift toward electric vehicles (EVs) has significantly impacted the automotive balance shaft market due to the fundamental differences between traditional internal combustion engines (ICE) and electric powertrains.

Rising demand and adoption of the EVs is expected to decrease the demand for balance shafts as these components are not used in electric drivetrains.

According to International Energy Agency 2023 report, nearly 14 million new electric cars were registered globally, bringing the total number of electric vehicles on the roads to 40 million. Electric car sales in 2023 saw an increase of 3.5 million compared to 2022, reflecting a 35% year-on-year growth. This figure is more than six times higher than sales in 2018.

In 2023, over 250,000 new electric car registrations occurred each week, exceeding the total annual registrations from 2013. Electric cars account for approximately 18% of all cars sold, increase from 14% in 2022 and just 2% in 2018.

Market Opportunity

Implementation of Stringent Emission Regulations to Present Significant Growth Opportunities

As consumers place greater importance on fuel efficiency due to escalating fuel prices and environmental issues, the need for automotive balance shafts is projected to increase. Balance shafts improve engine performance, minimize vibrations, and enhance fuel efficiency, making them appealing to manufacturers looking to satisfy consumer demands and comply with regulatory standards.

Ongoing advancements in balance shaft technology, such as the use of lighter materials and refined designs, can further boost performance and efficiency. Manufacturers investing in research and development to create advanced balance shaft systems can capitalize on these technological improvements to secure a competitive advantage in the industry.

The implementation of stringent emission regulations worldwide is also prompting manufacturers to incorporate technologies that lessen emissions from internal combustion engines. Balance shafts are essential in optimizing engine performance, which helps manufacturers meet these regulatory obligations and strengthen their position in the market.

Additionally, there is an increasing need for vehicles equipped with inline-4 cylinder engines, which typically use balance shafts to minimize vibrations and enhance smooth operation. This trend is expected to boost the balance shaft market, as more manufacturers prioritize the production of these engines. Collaborative efforts between automotive producers and balance shaft providers may result in innovative product advancements and broader market penetration. Such collaborations allow companies utilize each other's strengths to improve their product lines and secure a stronger presence in the market, fueling automotive balance shaft market growth.

Automotive Balance Shaft Market Trends

Advancement in Manufacturing Technologies to Catalyze Market Growth

The use of lightweight materials in balance shaft manufacturing is becoming increasingly popular. This transition aims to improve fuel efficiency and overall vehicle performance by lessening the weight of engine components. Innovative materials such as aluminum and composites are being explored to meet these goals, resulting in better handling and decreased emissions.

In addition, advances in manufacturing techniques, including precision machining and additive manufacturing (3D printing), are facilitating the creation of more intricate and efficient balance shaft designs. These technologies provide opportunities for enhanced customization, lower production costs, and better quality control, all of which improve the functionality of balance shafts across different engine types.

As automotive manufacturers concentrate on creating smaller, more efficient engines, the integration of balance shafts for effective vibration management is becoming more common. The rising demand for inline-4 cylinder engines, known for their cost-effectiveness and fuel efficiency, typically incorporate balance shafts, further driving advancements in balance shaft technology.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Engine Type

V6 Cylinder Engines Segment Increasing Due to Cost-Effectiveness and Fuel Efficiency Fuel the Segmental Growth

By engine type, the market is classified into Inline 3 Cylinder, Inline 4 Cylinder, Inline 5 Cylinder, and V6 Cylinder.

The v6 cylinder segment is estimated to be the fastest-growing segment during the forecast period (2025-2032). The rising demand for v6 cylinder engines is driven by their cost-effectiveness, improved performance and efficiency, smoother operation, environmental compliance, versatility in applications, technological advancements, and renewed interest from automotive enthusiasts.

The inline 4 cylinder segment accounted for the largest market share 38.44% in 2026. The increasing demand for inline 4 cylinder engines can be attributed to several key factors such as more fuel-efficient compared to larger V5, V6 and V8 engines. With rising fuel prices and growing environmental concerns, consumers are increasingly seeking vehicles that offer better gas mileage. The efficiency of inline 4 engines makes them an attractive option for buyers looking to reduce fuel costs and minimize their carbon footprint. In addition, the growing preference for inline-4 cylinder engines is due to their cost-effectiveness, compact design, improved performance through turbocharging, compliance with emissions regulations, alignment with market trends, and versatility across vehicle types. These factors collectively make inline-4 engines an increasingly popular choice among consumers and manufacturers alike.

To know how our report can help streamline your business, Speak to Analyst

By Manufacturing Process

Forging Segment Dominated due to Its Performance Advantages

The market is classified by manufacturing process into forging and casting.

The forging segment accounted for the largest market share 76.57% in 2026 and is estimated to be the fastest-growing during the forecast period. The trend of using forged balance shafts in the automotive industry due to their performance advantages and compliance with modern vehicle efficiency and emissions requirement is boosting the demand in the segment. As manufacturers prioritize lightweight materials and enhanced performance characteristics, forging is expected to dominate the market for automotive balance shaft production. Th segment is estimated to capture 76.38% of the market share in 2025.

The casting segment is expected to grow considerably in the upcoming years due to automation of casting processes which has improved production capacity and consistency. Foundries can achieve higher yields with automated systems, making it feasible to meet growing demand in the automotive sector efficiently. This segment is likely to grow with a CAGR of 4.10% during the forecast period (2025-2032).

By Vehicle Type

Passenger Cars Segment to Display Fastest-growth due to Rising Urbanization and Disposable Incomes

The market is classified by vehicle type into passenger cars, LCV, and HCV.

The passenger car segment is estimated to be the fastest-growing during the forecast period (2025-2032). The growth is driven by ongoing urbanization and the rise in disposable incomes worldwide, leading to increased consumers demand for personal vehicles. This heightened demand for passenger cars is directly related to the growing necessity for automotive balance shafts, which are crucial for improving engine performance and minimizing vibrations. Moreover, elements like the growing inclination towards personal vehicles, focus on fuel efficiency and decreased emissions, advancements in technology, the popularity of inline-4 engines, market robustness post-pandemic, and the development of opportunities in emerging markets all play a role in the swift expansion of this segment. This segment is anticipated to grow with a considerable CAGR of 5.80% during the forecast period (2025-2032).

The LCV (Light Commercial Vehicle) segment accounted for the largest market share in 2025. The expansion of e-commerce and logistics services has significantly heightened the need for light commercial vehicles, which are essential for transportation and delivery services. This has prompted manufacturers to boost LCV production, incorporating balance shafts to ensure smoother operation and minimize vibrations. Furthermore, LCVs are utilized in a range of sectors, such as construction, delivery, and services. This adaptability leads to a steady demand for balance shafts as manufacturers strive to address varied industry requirements while maintaining vehicle performance and reliability. The segment is likely to hold 44.73% of the market share in 2026.

Automotive Balance Shaft Market Regional Outlook

The market is classified by region into North America, Europe, Asia Pacific, and Rest of World.

Asia Pacific

Asia Pacific Automotive Balance Shaft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 8.06 billion in 2025, representing 51.42% of the global industry, and is expected to reach USD 8.47 billion in 2026. The automotive sector in in countries such as China and India is undergoing considerable expansion, fueled by a rise in vehicle production and sales. This rise increases the need for balance shafts, which are vital for engine performance and smooth operations. The Chinese market is expected to expand with a valuation of USD 4.88 billion in 2026.

The economic advancement in emerging markets across the region is leading to higher disposable incomes, which results in higher rates of vehicle ownership. This pattern further propels the demand for automotive components such balance shafts as increasing number of consumers look for personal transportation solutions. India is foreseen to hold USD 1.07 billion in 2026, while Japan is predicted to gain USD 1.27 billion in the same year.

Europe

In 2025, Europe generated USD 2.18 billion, contributing 13.93% to global market revenue, and is projected to grow to USD 2.35 billion in 2026. The region is estimated to be the fastest-growing region during the forecast period (2025-2032). European governments are implementing strict regulations aimed at reducing greenhouse gas emissions and improving fuel efficiency. The U.K. market continues to grow, projected to reach a market value of USD 0.12 billion in 2026. These policies encourage automakers to adopt advanced technologies, such as balance shafts, which enhance engine performance and help meet emission standards.

The growing demand for eco-friendly vehicles is driving the need for balance shafts in the region. Europe has a well-developed automotive infrastructure, including a strong supply chain and advanced manufacturing capabilities. This infrastructure supports the efficient production and integration of balance shafts into various vehicle models, contributing to market growth. Germany is poised to be valued at USD 0.46 billion in 2026, while France is expected to reach USD 2.66 billion in the same year.

North America

North America maintained a strong presence in the global market, reaching USD 4.48 billion in 2025, accounting for 28.60% share, and is expected to reach USD 4.73 billion in 2026. North America market is likely to witness considerable growth during the forecast period. The area is home to several major automotive manufacturers such as General Motors, Ford, and Stellantis. These companies have built a robust market presence and continually push the boundaries of innovation, leading to an increased demand for automotive components such as balancer shafts that improve vehicle performance and comfort.

The region is leading the way in technological advancements in automotive engineering. New materials and manufacturing techniques for balancer shafts are being developed to improve their effectiveness in reducing noise, vibration, and harshness (NVH). This commitment to innovation fosters the growth of the balance shaft market in North America. The U.S. market is estimated to be worth USD 3.28 billion in 2026.

Rest of World

Rest of the World accounted for USD 0.95 billion in 2025, representing 6.05% of the global market share, and is projected to reach USD 0.98 billion in 2026. The Rest of World encompasses Latin America, and Middle East & Africa, is experiencing an uptick in vehicle production. As regional automotive sectors evolve and expand, the need for balance shafts is anticipated to rise alongside vehicle manufacturing. Countries in the RoW are making investments in automotive infrastructure, including production facilities and supply chains to bolster local vehicle manufacturing. This progress enhances the availability of balance shafts, as manufacturers aim to enhance vehicle performance and meet growing market demands.

Competitive Landscape

Key Market Players

Leading Players Are Focusing on Innovation to Gain Strong Foothold

The market for automotive balance shafts is marked by fierce competitiveness among major companies seeking to boost their market presence through innovation, strategic alliances, and broadening their product lines. Firms are making significant investments in research and development to produce lightweight, durable, and efficient balance shafts. Innovations such as forged balance shafts are gaining popularity due to their compact size and effective natural damping properties. Additionally, as regulatory pressures to lower greenhouse gas emissions rise, manufacturers are concentrating on creating balance shafts that enhance fuel efficiency and decrease vehicle emissions. This trend is encouraging the use of balance shafts in both passenger cars and commercial vehicles.

List of Key Automotive Balance Shaft Companies Profiled:

- Hitachi Astemo Americas, Inc. (U.S.)

- Marposs S.p.A. (Italy)

- MAT Foundry Group Ltd. (Germany)

- SAC Engine Components Pvt. Ltd. (India)

- American Axle & Manufacturing, Inc. (U.S.)

- SHW AG (Germany)

- OTICS Corp. (U.S.)

- Engine Power Components, Inc. (U.S.)

- Sansera Engineering Limited (India)

- TFO Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

January 2025 - Cummins introduced the 6.7-liter turbo diesel engine for the 2025 Ram Heavy Duty vehicle. Cummins and Stellantis confirmed the continuation of their collaboration to provide engines for the Ram brand by 2030. This 6.7-liter turbo diesel engine, described as the most advanced diesel engine for pickups to date, will be available in the newly revealed 2025 Ram 2500 and 3500 Heavy Duty pickups, and the Ram 3500, 4500, and 5500 Chassis Cab trucks.

January 2025 - Tata Motors plans to begin testing hydrogen internal combustion engines trucks in the first quarter of March. This pilot projects aims to produce substantial data to enhance both the product development and hydrogen fuel infrastructure.

May 2024 - Subaru Corporation, Toyota Motor Corporation, and Mazda Motor Corporation joined hands to create new engines optimized for electrification with the focus on carbon neutrality. Through these new engines, all three companies intend to enhance the compatibility with motors, batteries, and other electric drive components. As they redesign vehicle layouts with more compact engines, these initiatives will also work toward reducing emissions from internal combustion engines (ICEs) by enabling them to be used with a variety of carbon-neutral (CN) fuels.

May 2024 - Volvo Trucks is developing hydrogen-powered combustion engine trucks. On-road testing of these hydrogen-fueled trucks will commence in 2026, with a commercial rollout expected by the end of this decade.

February 2024 - Indian conglomerate Reliance Industries announced plans to convert nearly 5,000 trucks to operate on hydrogen internal combustion engines (ICEs) within the coming months.

REPORT COVERAGE

The research report provides a detailed analysis of the market insights and focuses on important aspects, such as key players, device type, vehicle type, and applications depending on various regions and countries. Moreover, it offers deep insights into the market global automotive balance shaft market trends, competitive landscape, market competition, comparative analysis, and market status, and highlights key industry developments. Also, it encompasses several direct and indirect factors that have contributed to the expansion of global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.66% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Engine Type

|

|

By Manufacturing Process

|

|

|

By Vehicle Type

|

|

|

By Region

|

Frequently Asked Questions

The automotive balance shaft market size was valued at USD 15.68 billion in 2025. The market is projected to grow from USD 16.52 billion in 2026 to USD 23.79 billion by 2034

The market is likely to grow at a CAGR of 4.66% over the forecast period.

The top players in the industry are Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG., CalAmp Corporation, Geotab Inc., HeLLA GmbH & Co. KGaA, and others.

Asia Pacific dominated the market in 2025 with USD 8.06 billion.

Europe region is estimated to be the fastest growing during the forecast period.

China dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us