Automotive Ceramics Market Size, Share & Industry Analysis, By Types (Zirconia Oxide Ceramics, Alumina Oxide Ceramics, Titanate Oxide Ceramics, Others), By Application (Automotive Engine Parts, Automotive Electronics, Automotive Exhaust Systems, Others), and Regional Forecast, 2026-2034

Automotive Ceramics Market Size and Industry Overview

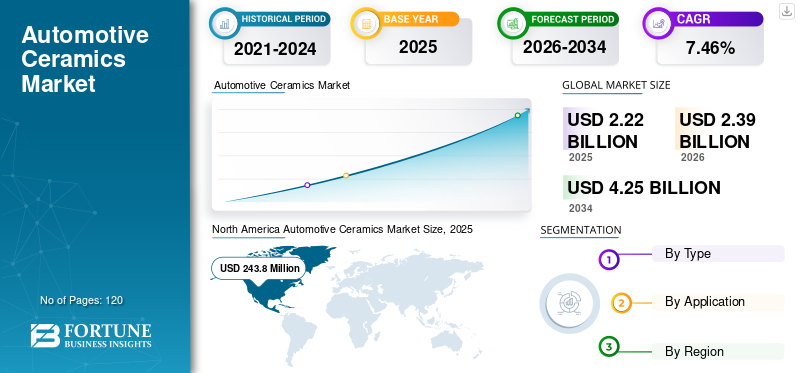

The global automotive ceramics market size was valued at USD 2.22 billion in 2025. The market is projected to grow from USD 2.39 billion in 2026 to USD 4.25 billion by 2034, exhibiting a CAGR of 7.46% during the forecast period. North America dominated the automotive ceramics market with a market share of 16.59% in 2025. Moreover, the U.S. automotive ceramics market is projected to reach USD 263.70 million by 2027, supported by rising adoption in sensors, brakes, and engine components.

Each component of an automobile has specific technical requirements, and the selection of these materials is directed by cost efficiency, maximizing energy, and acceptable reliability properties. These are incorporated into the automotive design to meet the demanding conditions required by the material that is reliable and robust. The electrical and thermal properties of ceramic materials make them suitable for mechanical seals, a variety of sensors, valves, and ceramic bearings. Ceramics are cost-efficient as compared to metals, more durable than plastics, and can be found throughout the automotive industry for advanced car manufacturing that requires high complexity in automotive components.

Download Free sample to learn more about this report.

Global Automotive Ceramics Market Overview

Market Size & Forecast:

- 2025 Market Size: USD 2.22 billion

- 2026 Market Size: USD 2.39 billion

- 2034 Forecast Market Size: USD 4.25 billion

- CAGR: 7.46% during 2026–2034

Market Share:

- North America dominated the market with a 16.59% share in 2025, driven by rising adoption of ceramics in sensors, brakes, and engine components.

- By Type: Zirconia Oxide Ceramics is expected to hold the largest share due to its high resistance to crack propagation and widespread application in engine and exhaust systems.

Key Country Highlights:

- United States: Expected to reach USD 263.7 million by 2027, driven by demand in glow plugs, fuel pumps, and emission control devices.

- Germany (Europe): Leading producer of vehicles, accounting for over 29% of the EU’s automobile market. Strong government support for innovation and environmental compliance.

- China & India (Asia Pacific): Fast-growing middle-class demand and expanded automotive manufacturing base are driving ceramic adoption.

- Brazil & Mexico (Latin America): Improving credit access, rising vehicle demand, and exports support regional growth.

- UAE, Saudi Arabia (MEA): Adoption of modern technologies like IoT and high disposable incomes propel automotive advancements.

The adoption of technical ceramic products having properties such as superior mechanical strength, high-edge stability, density, dimensional stability, and abrasion by the manufacturers is propelling the product demand. Additionally, high resistance to chemical corrosion, good thermal conductivity, and electrical insulation across varying temperatures are leading to increased adoption of ceramic products for automotive applications. Ceramics are used in components such as spark plug insulators, emission control devices, and heat sensors. The growing automotive industry and high demand for lightweight vehicles are expected to favour market growth.

Download Free sample to learn more about this report.

AUTOMOTIVE CERAMICS MARKET GROWTH FACTORS

Increasing Demand for Metals and Plastics Alternatives to Augment Demand

Changing consumer preferences has limited the availability of raw materials for automakers, along with performance standards and safety, which has caused a limited ability to reduce automobile weight. Light-weight components of every potential vehicle have been under investigation. Material substitution for heavier steel and iron with advanced composites such as plastics, ceramics, magnesium, aluminium, are essentially boosting the vehicle fuel economy. Material substitution majorly depends on the cost, mechanical properties, manufacturing capabilities, and design. Additionally, for the reduction of fuel consumption, enabling weight reduction is essential. Ceramics have better insulation and thermal properties and are cost-efficient, supporting the consumer demand for light-weight automobiles. These properties, combined with advanced production & research methodologies and structures, play an important role in reducing the total weight of the engine and other heat sensor parts of vehicles. Technological advancement further supports the use of advanced ceramics as an alternative material for automotive manufacturing.

Low-Cost Production Technologies to Bode Well for Market Growth

Companies are continuously focusing on the development of low-cost technologies to help contribute towards the high demand for light-weight and affordable vehicles. Ceramics are used in various products such as knock sensors, valve systems, exhaust pipes, and others. Owing to their high melting point and durability, ceramics are ideal materials to use to develop new technologies and reduce the manufacturing cost and weight of vehicles. The introduction of advanced and beneficial technologies are further driving the market growth.

RESTRAINING FACTORS

High Cost of Ceramics to Restrain Growth

The material cost of ceramics is higher than that of metal and other alloys. This may hinder the adoption of ceramics used in automobile manufacturing. High demand for affordable vehicles acts as a restraining factor for the market growth. Technologies supporting low-cost production techniques to reduce the cost of the vehicle also risk the high adoption of ceramics into the automotive industry. Furthermore, the recycling of ceramics is difficult and adds to the issue regarding the use of ceramics in the automotive industry. Thereby restraining the global market of automotive ceramics.

SEGMENTATION ANALYSIS

By Type

To know how our report can help streamline your business, Speak to Analyst

Zirconia Oxide Ceramics Segment to Hold a Significant Share

Based on type, the automotive ceramics market is segmented into zirconia oxide ceramics, alumina oxide ceramics, titanate oxide ceramics, and others. The zirconia oxide segment holds a major automotive ceramics market share owing to its increasing application in automobile exhaust and engine systems. Zirconium oxide or zirconia is a high resistance material to prevent crack propagation. Zirconium oxide ceramics are thermally expanding and are often the material choice for linking steel and ceramic. Zirconia is frequently used as an electrolyte in oxygen sensor applications owing to the high oxygen ion conduction at raised temperatures. Additionally, some zirconium oxide ceramics materials can conduct oxygen ions and are significantly more expensive than regular zirconia ceramics. Properties of zirconia are supporting the high use of ceramics in the automotive industry, which in turn is driving the overall automotive ceramics industry growth.

Alumina oxide is a white amorphous material used in the automotive industry owing to its good electrical insulation, excellent corrosion resistance, and low dielectric constant properties. These properties contribute a significant application in the automotive industry which are automotive sensors and electrical or electronic insulators in automobiles. Technological advancements in making vehicles safer for consumers are supporting market growth.

By Application

Automotive Engine Parts Segment to hold the Dominant Share

Based on the application, the market for automotive ceramics is segmented into automotive engine parts, automotive electronics, automotive exhaust systems, and others. The automotive engine parts segment will dominate the market during the forecast period. This is attributable to the increasing adoption of the product for the manufacturing of glow plugs, spark plugs, electronic fuel pumps, high-pressure pumps, sealing & insulation rings, valves, and others. The use of ceramic materials in automobiles helps to maintain engine efficiency through the protection of the engine parts. This is the factor that drives the high consumption of ceramics in the automotive industry, thereby leading to market growth.

Automotive ceramics in the exhaust system offer an effective way of purifying vehicle emissions and improving air quality by making the environment cleaner. Ceramic exhaust systems are attached to many diesel vehicles, such as large trucks and heavy machinery, designed specifically to be highly durable and easy to maintenance. A worldwide stringent regulation over vehicular gas emissions is leading to a high demand for the use of ceramics in the exhaust systems of vehicles.

REGIONAL AUTOMOTIVE CERAMICS MARKET ANALYSIS

North America Automotive Ceramics Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

The automotive ceramics market size in North America stood at USD 243.8 million in 2019. Owing to the presence of a large urban population and higher living standards in the region, the market is projected to witness a strong CAGR growth during the forecast period. Companies such as General Motors have, in the past year, witnessed plant layoffs and closures in 2019 with more alliances, investments into electric vehicles, and other new advanced technologies. The U.S. automotive industry has suffered from higher duties on aluminium and steel imports after April 2019 on account of a 90-day suspension of high tariffs on imports from China.

Europe

The European region may witness considerable market growth due to the region being the world’s leading producer of automobiles. The automotive industry is the most significant donor to the economy of the European Union. The European Commission aims to identify and assess the policy issues to encourage healthy competition in the automotive industry and recommend feasible solutions by taking into account the environmental, social, and economic goals. The effort to improve the internal market regulation of the automotive industry is expected to favour market growth. Germany is one of the leading automobile producers and accounts for more than 29% of the total European Union automobile market share. Germany produces around 6 million vehicles, including commercial and passenger vehicles, every year. Moreover, German automobile companies have accounted for the manufacturing of 5.5 million automobile units in overseas markets.

Asia Pacific

Asia Pacific dominates the market and is expected to grow at a faster rate during the forecast period. This is ascribable to the increasing spending habits of consumers in the middle-class category. This growth can be associated with rapid economic expansion in developing countries such as China, India, and Malaysia. Additionally, automotive ceramics manufacturers from the Western region are shifting to the Asia Pacific region on account of leveraging lucrative opportunities, and availability of cheap labor, and less competition. This shift can also be due to an increase in the automotive manufacturing activities within the region, and a cost-effective production hub available is further expected to drive the market.

Latin America

Latin America is primarily driven by the demand for passenger cars, lower interest rates, and improving economic status of the consumers in countries such as Mexico, Argentina, and Brazil. In Brazil, improved economic conditions and the rising availability of credit will favor the sales of lightweight vehicles. Furthermore, growing investment and increasing demand for export will contribute to the growth of automotive sales. This is expected to lead to market growth in the forthcoming years. The Middle East and Africa market is expected to grow due to the adoption of modern technologies such as internet of things (IoT) in the region. Several public and private companies in the region are digitalizing the business operations to improve productivity. The highly disposable income in gulf countries such as Qatar, Saudi Arabia, and the UAE is a significant factor behind the growth of the automobile industry in the region.

KEY INDUSTRY PLAYERS

Product Innovation by Major Companies Such as IBIDEN to Augur Growth

Product innovation & efficient capacity utilization that leads to problem-solving with innovative technologies cater to the growing demand for automotive ceramics products. IBIDEN is one of the prominent companies related to automotive ceramics. The major companies are forming new strategies constantly that include developing new technologies and creating new products according to consumer demand. Additionally, companies are adopting digital marketing strategies for revenue-boosting.

LIST OF KEY COMPANIES PROFILED IN AUTOMOTIVE CERAMICS MARKET:

- CeramTec (Germany)

- IBIDEN (Japan)

- KYOCERA Corporation (Japan)

- NGK SPARK PLUGS (INDIA) PVT. LTD. (Japan)

- CoorsTek Inc. (U.S.)

- Morgan Advanced Materials (UK)

- Corning Incorporated (U.S.)

- Saint-Gobain Ceramics (U.S.)

- Elan Technology (U.S.)

- Ceradyne, Inc. (U.S.)

- Other Key Players

KEY INDUSTRY DEVELOPMENTS:

- In April 2021 – NGK Spark Plug, manufacturers of automotive spark plugs, announced a $100 million fund to invest in startups and find potential merger and acquisition deals. The company’s corporate venture fund is an opportunity to work with startups and expand into new businesses.

- In April 2020 – Murata Manufacturing Co., Ltd. started mass production of two new multilayer ceramic capacitors for automotive applications. This is a step towards expanding the lineup to meet market needs and contributing to automotive performance and features.

REPORT COVERAGE

The automotive ceramics market research report provides detailed market analysis and focuses on crucial aspects such as leading companies, applications, and types. Also, the report offers insights into market trends and forecasts as well as highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the high growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Million Ton) |

|

Segmentation |

Type; Application; and Geography |

|

By Type

|

|

|

By Application

|

|

|

By Geography

|

|

Frequently Asked Questions

The global automotive ceramics market size is valued at USD 2.39 billion in 2026, projected to reach USD 4.25 billion by 2034 at a CAGR of 7.46% during 2026-2034.

The growth is driven by increasing demand for lightweight, durable materials in automotive manufacturing, especially as alternatives to metals and plastics. Ceramics offer thermal stability, corrosion resistance, and electrical insulation, making them ideal for engine, exhaust, and electronic applications.

Growing at a CAGR of 7.46%, the ceramics will exhibit steady growth during the forecast period (2026-2034).

Common types include zirconia oxide ceramics, alumina oxide ceramics, and titanate oxide ceramics. Zirconia is widely used for exhaust and engine components due to its high resistance to cracking and heat, while alumina is popular for electrical insulators and sensors.

Automotive ceramics are used in engine parts (like spark plugs and glow plugs), electronics (sensors, capacitors), and exhaust systems. Their unique properties improve performance, fuel efficiency, and emission control.

The main challenges include the high cost of ceramic materials, limited recyclability, and the need for cost-effective manufacturing. These factors can restrict adoption, especially in low-budget vehicle segments.

Top companies include CeramTec (Germany), KYOCERA (Japan), NGK Spark Plug (Japan), CoorsTek (U.S.), Corning Incorporated (U.S.), and Saint-Gobain (U.S.). These players are investing in innovation, cost reduction, and strategic partnerships to maintain market share.

Asia Pacific dominates the market due to the rapid growth of the automotive sector in countries like China, India, and Japan. The region benefits from low-cost labor, expanding middle-class demand, and increasing investments in automotive production.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us