Automotive Collision Repair Market Size, Share & Industry Analysis, By Repair Type (Minor Scratch Repairs, Bumper Repair/Replacement, Front-end Repairs, Rear End Repairs, Side Impact Repairs, and Frame Damage), By Vehicle Type (Passenger Cars (Sedan/Hatchback and SUVs) and Commercial Vehicles (LCVs and HCVs)), By Service Channel (OEM Certified Repair Shops and General Auto Body Repair Shops), By Vehicle Propulsion (ICE, PHEV, and Electric), By Solution (Service and Parts), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

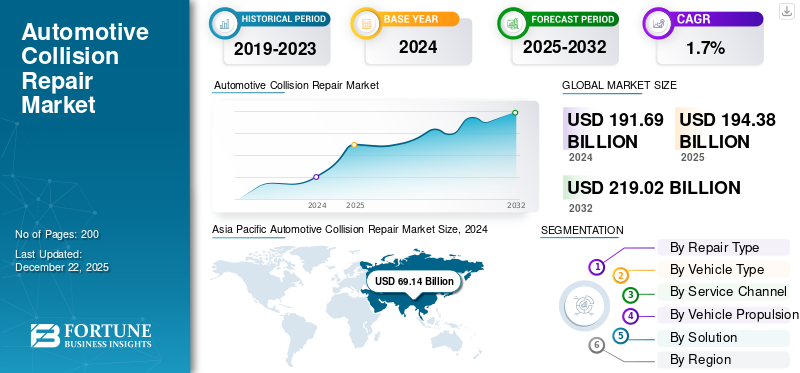

The global automotive collision repair market size was valued at USD 194.38 billion in 2025 and is projected to grow from USD 197.25 billion in 2026 to USD 228.23 billion by 2034, exhibiting a CAGR of 1.84% during the forecast period. Asia Pacific dominated the global market with a share of 36.19% in 2025.

Automotive collision repair refers to the correction of a vehicle’s body, structure, and safety features after the vehicle is hit or witnesses a collision or accident. The repair is done to maintain the integrity of the vehicle and passenger protection.

The increasing number of vehicles on the road drives the global market, as more vehicles on the roads lead to increased accidents and collisions. The rising complexity of modern vehicles, which requires special repair techniques, fuels market development. Failure in the operation of autonomous vehicles, such as driverless taxis, also caters to the market. Moreover, the influence of insurance has shifted consumers to repair their vehicles more often, claiming insurance, thereby increasing the market demand over the forecast period.

Major leading players in the market include Caliber Collision, Gerber Collision, and Service King Collision, among others. These companies focus on developing repair technologies, automation, and improving service quality. The reduction in repair time and skill training plays a crucial role in the development of the market and creates a competitive edge among the players operating in the market.

Download Free sample to learn more about this report.

Automotive Collision Repair Market Key Takeaways

- 2025 Market Size: USD 194.38 billion

- 2026 Market Size: USD 197.25 billion

- 2034 Forecast Market Size: USD 228.23 billion

- CAGR: 1.84% from 2026–2034

- Asia Pacific dominated the automotive collision repair market with a 36.19% share in 2025.

- The passenger cars segment is projected to account for 74.28% of the market share in 2026.

- The general auto body repair shops segment is expected to hold 57.93% of the global market share in 2026.

Asia Pacific

Asia Pacific generated USD 70.34 billion in revenue in 2025 and is projected to reach USD 71.61 billion in 2026

North America

North America accounted for 33.23% of the global market in 2025 and is expected to reach USD 65.66 billion in 2026.

Europe

Europe captured 15.82% of global revenue in 2025 and is projected to reach USD 30.96 billion in 2026.

U.S.

The U.S. automotive collision repair market is projected to reach USD 56.03 billion by 2026.

Japan

Japan’s automotive collision repair market is projected to reach USD 14.99 billion by 2026.

Read More

Market Dynamics

Market Drivers

Increasing Number of Vehicles on Road Drives Market Growth

As the number of vehicles on the road increases, the number of accidents and collisions also increases. People at intersections where traffic signals are not installed or do not work properly cause vehicles to collide several times. More vehicles on the road lead to more traffic, which sometimes causes bumping into the vehicle in front, or sometimes by the side. This causes vehicle damage, which requires collision repair to maintain the vehicle and keep it operational. As the number of vehicles increases, the number of vehicles for repair also increases, which is anticipated to fuel the automotive collision repair market growth over the forecast period. According to OICA, in 2024, around 95.3 million vehicles were sold, up by 2.7% as compared to the previous year, 2023, which recorded a vehicle sale of 92.9 million units.

Electric Vehicle Adoption Drives Market Advancement

Recently, the electric vehicle industry witnessed a substantial growth in the overall automotive market. Several fleet operators in various industries are incorporating electric vehicles to meet sustainability and zero-emission goals. For instance, in January 2025, Amazon added 140 electric vehicles to its delivery network. This includes around 120 Mercedes-Benz eActros 600 trucks and eight Volvo FM Battery Electric trucks. Moreover, collision repair providers are focusing on developing their technology to cater to the growing adoption of electric vehicles on the road, which advances the market over the projected period.

Failure in Operation of Autonomous Vehicles Drives Market Growth

In some countries, driverless cars are not yet in operation. However, in major economies where fully autonomous vehicles are used, there is still the potential for issues and disruptions in traffic flow, which can lead to accidents and collisions. For instance, in June 2025, Tesla tested its robotaxi in Texas. The car faced many issues, such as entering the wrong lane, dropping passengers in the middle of multiple lane roads or at an intersection, sudden braking, driving over the curb, and speeding. At an intersection, suddenly the steering wheel of the vehicle wobbled, and the car proceeded straight into the intersection, instead of turning left into its desired direction. These events can lead to traffic chaos and multiple collisions.

Market Restraints

Increasing Vehicle Complexity Hampers Market Growth

Major OEMs are developing modern vehicles, incorporating many features such as ADAS and others. Components such as radar sensors, lane-keeping cameras, and automatic emergency braking require specialized calibration after a collision, which increases the vehicle's cost and repair time. The vehicle body is installed with several sensors, which are also damaged by the collision. Installing the sensors, with OEM configuration, poses a challenge to the repair shops, hampering the development in the market. According to AAA, the average replacement cost of Advanced Driver Assistance Systems (ADAS) components from a minor front collision repair is estimated to reach USD 1,540, representing 13.2% of the total repair cost, which is USD 11,708.

Market Opportunities

Augmented Reality and Automation in Repair Technologies Provide Market Opportunity

With the help of augmented reality, technicians can visualize a vehicle's internal components, which helps diagnose issues and find efficient solutions for the repairs. The technology guides repairers step-by-step to perform complex procedures with accuracy. This helps the players in the market to tackle major challenges, which include the skill gap among workers in modern vehicle repair. Additionally, many major players in the market are adopting automated tools in the workshop to automate standard services such as painting and coating, wheel alignment, calibrations, and others effectively and more accurately. This provides a great opportunity for the market to develop over the forecast period.

Market Challenges

Skill Gap Among Workers Poses Challenges in Market

Today’s vehicles are developed with advanced technologies and complex integration of components, which makes it difficult for shops to work on. For this, highly skilled labor is required that has the expertise in the vehicle and its components, and can repair efficiently while saving time. However, the market witnesses a shortage of skilled labor, which poses a significant challenge to the repair shop owners. Technologies such as ADAS, having components including cameras, radars, sensors, and others, require a proper specialized person, whose shortage prohibits market growth.

Automotive Collision Repair Market Trends

Insurance-Led Repair Drives Demand for Market

Governments or dedicated authorities of road transport have made it mandatory for vehicle owners to insure their vehicles, and failure to do this or a renewal will be penalized. Due to this, the market has observed an increase in people buying vehicle insurance and using it to repair their vehicles without the hesitation of cost constraints. Several insurance companies providing vehicle insurance are expanding their partnerships with workshops within the countries to provide efficient services for their customers to avail insurance benefits. Thus, insured vehicle owners tend to repair their vehicles after collisions, which significantly drives the market adoption. In June 2025, Michigan Senate Bill 328 was introduced, which proposes a mandatory 10% auto insurance premium cut on new and renewed policies.

Download Free sample to learn more about this report.

Impact of Tariffs

Tariff Disrupts Supply Chain and Delays Repair Process

The tariff imposed by the U.S. on the import of goods from all around the world disrupts supply chains, leading to delays in the repair of vehicles. Longer waiting period for spare parts results in its cost increase, impacting the operators and discouraging the consumers from repairing. In June 2025, the U.S. imposed a tariff of 25% on the import of automobiles and spare parts, which created a supply chain issue in the repair industry.

Segmentation Analysis

By Repair Type

Reverse Parking and Rear End Collisions by Other Vehicles Boosted Rear End Repairs Segment Growth

The market segment by repair type is categorized into minor scratch repairs, bumper repair/replacement, front-end repairs, rear end repairs, side impact repairs, and frame damage.

The rear end repairs segment is expected to hold the largest market share of 30.57% in 2026 and to continue its dominance over the forecast period. Vehicles often collide while driving backwards, reverse parking, and the impact of vehicles coming from behind in a sudden braking situation. Rear structures are not as tough as the front structure, due to which the rear end gets impacted more, which generates the demand for rear-end repairs over the period.

The front-end repairs segment is projected to grow at the highest CAGR during the forecast period. Rapid urbanization, traffic congestion, and violent crossing of intersections tend to cause vehicles to collide with each other from different directions, such as a T-bone collision or head-on collision, damaging the front-end parts of the vehicles, which require repair afterwards. According to the AAA, driver distraction and inattention contributed 8% to 12% of tow-away crashes. Moreover, sudden obstruction on roads while driving at high-speed causes significant damage to the vehicles, which drives the demand for the segment over the forecast timeframe.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Rising Vehicle Ownership Among Individuals Led to Market Dominance of Passenger Cars

The market is characterized by vehicle type into passenger cars and commercial vehicles. The passenger cars segment includes sedan/hatchback and SUVs; the commercial vehicle segment includes LCVs and HCVs.

The passenger cars segment is expected to hold the dominant market share of 74.28% in 2026 and to develop at the fastest CAGR during the forecast period. The SUVs sub-segment under passenger cars drives the largest market share throughout the projected timeframe. The growth of the segment is driven by increasing vehicle ownership. The rising disposable income created interest among consumers to buy their own vehicle. Due to this, the traffic of vehicles increased on the road, which resulted in a greater tendency for accidents and collisions. Thus, increased vehicle ownership among individuals drives the growth of the segment during the predicted period. In 2024, according to OICA, around 67.5 million passenger cars, including hatchbacks, sedans, and SUVs, were sold, witnessing a rise of around 3.3% compared to 2023, which was 65.4 million.

The commercial vehicles segment holds a sustainable share of the market. HCVs hold a majority share in the segment. Commercial vehicles often struggle to navigate through traffic and on congested roads. These vehicles running on long-distance routes such as highways witness rear-end collisions by speeding cars, and brake failures cause front-end collisions. This develops the need for the repair of the bodies of commercial vehicles after a collision for the easy operation of the vehicles.

By Service Channel

Wide Availability, Lower Repair Cost, and Flexibility in Vehicle Models Drive Dominance of General Auto Body Repair Shops Segment

The market is divided by service channel into OEM certified repair shops and general auto body repair shops.

The general auto body repair shops segment is projected to dominate the market of 57.93% in 2026. These shops are situated at a range of locations within an area, offer lower repair costs, and can service all vehicle makes and models. They are especially prevalent in developing regions where cost-conscious consumers and a large base of aging vehicles drive demand. These shops also cater to vehicles that are no longer under warranty, making them the preferred choice for a broad customer base, which fuels the dominance of the market.

The OEM certified repair shops maintained a sustainable share of the market in 2024. These shops are expected to be the fastest-growing segment, driven by the increasing use of advanced technologies such as ADAS, EVs, and lightweight materials, which require specialized tools and trained technicians. OEMs and insurers are promoting certified facilities to ensure repair quality, safety, and warranty compliance, especially in developed markets where customer preference for brand-backed service is rising. In September 2024, ProColor Collision Adams, formerly Lee’s Collision Center in Adams, California, opened as the first of three planned franchise locations. The shop is I-CAR Gold certified and holds MOPAR, Hyundai, and Kia certifications, offering advanced collision repair and strong insurer relationships.

By Vehicle Propulsion

ICE Segment Led Due to Its Established Infrastructure

The market is divided by vehicle propulsion into ICE, PHEV, and electric.

The ICE segment dominated the market in 2024. ICE vehicles have an advantage over electric vehicles due to their established infrastructure and ease of maintenance and repair. Due to this, several people still prefer ICE vehicles, which fuels the dominance of the segment globally. Developing economies where ICE vehicles are most preferred due to convenience and ease of repair drive the growth of the segment over the forecast period.

The electric segment is expected to develop at the fastest CAGR during the forecast period 2026-2034. Despite the established infrastructure of ICE vehicles, electric vehicles are gaining popularity due to their operational efficiency. Commercial fleet operators, in order to achieve sustainability goals, are adopting electric vehicles. Along with this, major repair shops are developing the technologies and skills required to cater to the collision repairs of electric vehicles, which drives the adoption of EVs in the market. According to the IEA, sales of Electric Light Commercial Vehicles (eLCVs) rose by around 40% in 2024, reaching 6 million units, owning a share of 7%, compared to 5% in 2023.

By Solution

Rising Need for Replacement Components Boosts Parts Segment Growth

The market is divided into the solution segment by service and parts.

Parts currently projected to dominate the market share of 52.13% in 2026, due to the high cost and critical need for replacement components such as bumpers, lights, windshields, and body panels in most collision repairs. OEM, aftermarket, and recycled parts make up a significant portion of repair expenses. Thus, the frequency of part replacements, especially with increasing minor accidents and aging vehicle fleets, drives the dominance of this segment.

The service segment is expected to rise at a CAGR of 2.0% during the forecast period 2026-2034. This growth is driven by the rising complexity of vehicles, which require skilled labor, diagnostics, and calibration. As technology evolves, repair services are becoming more specialized, increasing labor demand and costs. Additionally, insurers and OEMs are pushing for high service quality and certified repairs, accelerating the segment's growth over the projected timeframe.

Automotive Collision Repair Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Collision Repair Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the Asia Pacific market stood at USD 70.34 billion, representing 36.19% of global demand, and is projected to grow to USD 71.61 billion in 2026. The region consists of strong automotive sales, with China having the largest share. The growing urbanization and driver behavior are some of the major factors for the regional market’s growth. India is witnessing an increase in drunk driving, road rage, and other factors that lead to vehicle collisions and accidents. For instance, in July 2024, around 12,000 persons were booked for drunk driving, witnessing a surge of nearly 27% as compared to the previous year. Traffic violations such as driving in the wrong direction, leading to head-on collisions from vehicles in the opposite direction, are some of the common factors that drive the market’s growth in the region. The Japan market is projected to reach USD 14.99 billion by 2026, the China market is projected to reach USD 22.55 billion by 2026, and the India market is projected to reach USD 18.08 billion by 2026.

North America

The market in North America reached USD 64.6 billion in 2025, representing 33.23% of total market revenue, and is projected to reach USD 65.66 billion in 2026. The growth of the market is primarily attributed to the abrupt weather conditions, which affect the surface of roads. In harsh winter, roads are covered with layers of ice, which can cause vehicles to slip in case of sudden braking. This, in turn, leads to accidents and collisions, which further need repair. Moreover, major players in the market are advancing their technology to cater to the rising innovations in modern vehicles, which also fuels market growth in the region.

The U.S. holds the largest share of the North American region. The U.S. market is projected to reach USD 56.03 billion by 2026. This is due to the dominance of vehicle sales and their usability on roads. Crowded cities such as New York and others face traffic due to urbanization, which leads to accidents and collisions. Moreover, harsh winter in the country makes the roads slippery, which leads to mishandling of the vehicle, causing vehicle damage, which creates the need for automotive collision repair in the country.

Europe

Europe contributed approximately USD 30.74 billion to the global market in 2025, accounting for 15.82% share, and is expected to reach USD 30.96 billion in 2026. European countries often have narrow streets and roads, leading to traffic issues and minor collisions between vehicles. The region is aggressively adopting electric vehicles, creating growth opportunities in the electric vehicle collision repair sector. Moreover, Germany has higher road speed limits, which is also proportional to the cause of vehicle accidents and collisions. This fuels the demand for the market in the region. According to the U.S. Embassy & Consulates in Germany, speed limits in cities and towns are 50 km per hour and 100 km on the highway unless, which is otherwise marked as “there is no speed limit on the Autobahn”, although the German authorities recommend a top speed of 130 km per hour. The UK market is projected to reach USD 4.69 billion by 2026, and the Germany market is projected to reach USD 5.53 billion by 2026.

Rest of the World

Rest of the World recorded a market size of USD 28.7 billion in 2025, capturing 14.76% of the global market share, and is projected to reach USD 29.02 billion in 2026. The rest of the world comprises South America, the Middle East, and the African sub-regions. Poor road conditions in many parts of the region contribute to higher accident rates, fueling demand for collision repairs. Rising middle-class income levels and urbanization have led to a growing number of vehicles on the road, increasing accident risks and repair demand in the region.

Competitive Landscape

Key Market Players

Partnerships with Insurance and OEM Firms Drive Competitive Edge

The global automotive collision repair industry is highly competitive and fragmented, with the presence of numerous local and international players. Key companies include Caliber Collision, Gerber Collision, and Service King Collision, among others, that lead the global market. The competition is driven by technological advancements, cost efficiency, and strategic partnerships with insurance firms and OEMs. Players are focusing on expanding their service networks, investing in advanced repair tools, and offering sustainable solutions such as eco-friendly paint coatings. Consolidation trends are emerging, especially in developed markets, through mergers and acquisitions. Digitalization, telematics, and AI-driven damage assessments are also reshaping the market, intensifying competition across segments.

List of Key Automotive Collision Repair Companies Profiled

- Gerber Collision & Glass (Canada)

- Caliber Collision (U.S.)

- Crash Champions (U.S.)

- Service King (U.S.)

- Classic Collision (U.S.)

- Fix Auto (U.S.)

- Procolor Collision (Canada)

- VIVE Collision (U.S.)

- Vehicle Service Group (U.S.)

- Collision Right (Ireland)

- Car-o-Liner (Sweden)

- Penske Collision Repair (U.S.)

- Graham Collision (U.S.)

Key Industry Developments

- In June 2025, VIVE Collision acquired Lamon Auto Body Shop of Mt. Holly, New Jersey, and rebranded it as Lamon Auto Body Powered by VIVE. VIVE plans significant investment in technician training, equipment, and OME certifications to enhance repair quality and service standards. The acquisition expands VIVE’s Northeast footprint, supporting markets with limited certified collision repair centers.

- In June 2025, Classic Collision expanded in Alabama by acquiring Advanced Collision of Semmes, Inc., a locally owned shop with over 23 years of service and a reputation for integrity, quality workmanship, and family-friendly customer care. The acquisition strengthens Classic’s regional presence and complements its network of 339 facilities nationwide, leveraging community roots and trusted expertise.

- In June 2025, VIVE Collision acquired Lund Collision. The 11,000 sqft, I-CAR certified facility nearly doubled revenue through investments in modern equipment, workforce development, and insurer internships. The acquisition aligns with VIVE’s Northeast expansion strategy, enhancing advanced repair capabilities and technician development across its growing regional MSO network.

- In June 2025, Wren’s Collision expanded to 18 locations with the acquisition of Ray’s Collision in Columbus. The rebranded facility, centrally located, offers full collision repair services, such as frame repair, painting, refinishing, and insurance claims support.

- In September 2024, I-CAR was designated a Registered Apprenticeship Hub and awarded a U.S. Department of Labor Apprenticeship Building America grant. This includes over USD 7 million in funding across four years to expand Registered Apprenticeship Programs (RAPs) in high-demand collision repair fields. The initiative will strengthen educational programs, reduce the technician shortage, and standardize training across repair centers.

Investment Analysis and Opportunities

Innovation in Repair Technology and Market Expansion Attract Investment Opportunities

The global automotive collision repair market presents strong investment opportunities driven by rising vehicle ownership, increasing road accidents, and demand for repair solutions. Investors are attracted to innovation such as AI-powered diagnostics, 3D printing of parts, and eco-friendly repair materials. Growth potential is notable in emerging markets such as South America, the Middle East, and Asia Pacific, where vehicle fleets are expanding rapidly. Strategic investments in digital platforms, mobile repair services, and OEM-authorized repair centers are gaining traction. Additionally, partnerships with insurers and fleet operators provide recurring revenue streams. The shift toward electric and connected vehicles further opens new investment avenues in specialized repair services.

Report Coverage

The global automotive collision repair market report analyzes the market in depth. It highlights crucial aspects such as prominent companies, market scope, competitive landscape, repair type, vehicle type, service channel, vehicle propulsion, and solution. Besides this, the market research reports provide insights into the market trends and highlight significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 1.84% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Repair Type

By Vehicle Type

By Service Channel

By Vehicle Propulsion

By Solution

By Region

|

Frequently Asked Questions

Fortune Business Insights says the global market was valued at USD 197.25 billion in 2026 and is anticipated to reach USD 228.23 billion by 2034.

The market will exhibit a CAGR of 1.84% over the forecast period (2026-2034).

By service channel, the general auto body repair shops segment dominated the global market.

The rising number of vehicles on roads, driver behavior, urbanization, traffic violations, and weather affecting roads result in collisions, thus generating demand for repairs. Moreover, the adoption of EVs and the advancement of repair technology with automation drive market growth.

Caliber Collision, Gerber Collision, and Service King Collision lead the global market.

In 2025, the Asia Pacific region led the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us