Automotive Composites Market Size, Share & Industry Analysis, By Fiber (Glass, Carbon and Natural), By Resin Type (Thermoset and Thermoplastics), By Application (Exterior, Interior, Structure & Power train, and Other), and Regional Forecast, 2026-2034

Automotive Composites Market Size and Industry Overview

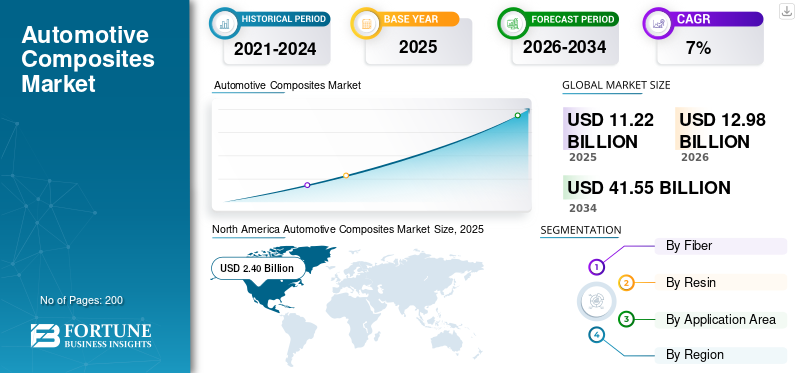

The global automotive composites market size was valued at USD 11.22 billion in 2025. The market is projected to grow from USD 12.98 billion in 2026 to USD 41.55 billion by 2034, exhibiting a CAGR of 15.66% during the forecast period. North America dominated the automotive composites market with a market share of 31.29% in 2025. Moreover, the U.S. automotive composites market is projected to reach USD 3.22 billion by 2026, driven by the trend of lightweighting and improved fuel efficiency.

The automotive composites market size reflects a structurally expanding materials segment embedded within global vehicle manufacturing value chains. Adoption spans passenger vehicles, light commercial platforms, and performance-oriented models, with demand distributed across major automotive production regions. North America and Europe represent established demand centers, while Asia-Pacific increasingly shapes incremental volume through scale manufacturing and platform diversification.

Historically, the automotive composites market progressed from niche applications toward broader structural and semi-structural use. Early adoption focused on weight reduction in premium vehicles. Over time, improved processing methods and material consistency supported wider integration. The market currently operates in a scaling phase, where penetration deepens across mass-market platforms rather than remaining limited to high-end models.

Several momentum indicators support this trajectory. Original equipment manufacturers increasingly embed composites at the design stage rather than as retrofits. Supplier investment in localized production improves responsiveness and cost control. Inflection points emerge where regulatory pressure, performance requirements, and manufacturing readiness converge, reinforcing the automotive composites market share within vehicle bill-of-materials across regions.

Automotive composites are lightweight materials that are primarily used in trucks, cars, and other vehicles, primarily under the hood and in the interiors. Composites are preferred materials for weight reduction in automobiles, and hence, composites are used for many automotive interior and exterior applications. The usage of composite materials in the automotive industry has increased in the past few years due to their excellent dimensional stability. Properties of composites, such as shape retention, low coefficient of thermal expansion, resistance to corrosion for performance in dry and wet conditions, ease of manufacturing, and low weight to reduce overall vehicle mass, make them preferred materials.

Download Free sample to learn more about this report.

AUTOMOTIVE COMPOSITES MARKET Key Takeaways

- 2025 Market Size: USD 11.22 billion

- 2026 Market Size: USD 12.98 billion

- 2034 Forecast Market Size: USD 41.55 billion

- CAGR: 15.66% from 2026–2034

- North America dominated the automotive composites market with a market share of 31.29% in 2025.

- The Exterior segment is expected to hold a 43.47% share in 2018.

- The demand for thermoset is higher than that from the thermoplastic resin segment.

North America

North America emphasizes lightweighting to support fuel efficiency and electric vehicle range targets. Composite adoption remains strongest in structural, battery enclosure, and pickup truck applications.

Asia Pacific

Asia Pacific is the largest and fastest-growing region in this market, owing to the highest number of vehicles present in this region, especially in countries like China, India, and Thailand.

Europe

The growth opportunities for the European automotive composites market are governed by the usage of automotive composites, which is environmentally friendly. Furthermore, various OEMs present in Europe are focusing on natural composites to support government policies.

U.S.

The U.S. automotive composites market is projected to reach USD 3.22 billion by 2026, driven by the trend of lightweighting and improved fuel efficiency.

Japan

Japan prioritizes material efficiency, reliability, and manufacturability. Glass fiber composites dominate high-volume models, while carbon fiber use expands selectively in electric and hybrid platforms.

Read More

AUTOMOTIVE COMPOSITES MARKET TRENDS

Download Free sample to learn more about this report.

Virtual Network to Utilize Composites in the Automotive Industry at Full Potential

The automotive composites industry has an undeniable bright future, with the forthcoming improvements in technology and manufacturing processes, raw materials, and composite materials can be used in more and more components, replacing steel and aluminum. A virtual network of automotive composites manufacturers and researchers has been set up to conduct the research effectively. At the same time, the virtual network will bring together all industry experts, which helps to bring all the parts of the automotive composites value chain together to advance the industry and material into mainstream acceptance.

The automotive composites market is undergoing structural transformation as vehicle manufacturers reassess design priorities, production economics, and sustainability obligations. Composites are no longer confined to niche performance models; they are increasingly embedded across mainstream vehicle platforms.

One defining shift is the integration of lightweight engineering into early vehicle architecture. Automakers now design platforms around composite compatibility rather than treating composites as substitute materials. This approach improves structural efficiency while reducing downstream reengineering costs.

Manufacturing transformation is another critical trend. Automation, compression molding, and high-speed resin transfer processes are improving cycle times and consistency. These advances narrow the historical cost gap between composites and conventional metals, supporting higher-volume applications.

Sustainability considerations are reshaping material selection and sourcing strategies. Regulatory pressure on emissions and lifecycle impact is accelerating interest in recyclable thermoplastics and natural fiber composites. OEMs increasingly evaluate composites based on end-of-life recoverability, not only performance.

AUTOMOTIVE COMPOSITES MARKET GROWTH FACTORS

Growing Demand for Lightweight Vehicles Is Expected To Drive the Automotive Composites Market

The market for automotive composites is driven by the heavy demand for lightweight components in automotive parts for the sake of better fuel efficiency and to reduce emissions in order to comply with the EU legislation. Composites offer weight reduction benefits by 15-20% using glass fiber composites and 25-40% for carbon fiber composites, as compared with other structural metallic materials such as steel, iron, and aluminum. Moreover, to support the usage of composites in the automotive sector, various public-private partnership initiatives have already been launched in EU member states. Such initiatives include the establishment of composites and automotive lightweight materials innovation clusters, collaborations with the automotive and chemical industries to support the investment, and supply chain analysis of the automotive carbon fiber composites market.

Increase in Demand for Electric Vehicles is Driving the Market for Automotive Composites

Many experts consider that electric vehicles will allow higher costs per kilo of weight saved in the vehicle weight reduction strategies. Normal IC engine-driven cars can only afford to pay 2-3 per kg of weight saved, but electric vehicles can save 7-8/kg. General vehicles consume more energy while accelerating in the standard drive cycles, and are also able to recover higher amounts of kinetic energy through brake energy recovery. In electric vehicles, a lower-weight vehicle body allows downsizing batteries while maintaining range. Reducing vehicle body and battery pack weight then leads to a compounding effect on weight reduction of the overall vehicle by enabling the downsizing of other parts, such as the brake system and driven train parts. In ICE-driven vehicles, the lower weight reduces emissions and improves performance at equal drivetrain power and torque levels.

The automotive composites market growth is shaped by a combination of demand-side pressure, supply-side capability expansion, and external structural catalysts. On the demand side, vehicle manufacturers face sustained pressure to reduce weight while maintaining structural integrity and safety performance. Lightweighting directly improves energy efficiency, extends driving range in electric vehicles, and supports emission reduction targets. Consumer expectations around vehicle performance, durability, and design flexibility further reinforce composite adoption across multiple vehicle segments.

From the supply perspective, advances in composite manufacturing technologies act as strong enablers. Automated fiber placement, resin transfer molding, and faster curing thermoplastics improve cycle times and production consistency. These developments lower per-unit costs and improve scalability, making composites viable beyond limited production runs. Capital investment by material suppliers and tier-one manufacturers strengthens supply reliability and supports broader platform integration.

External catalysts play a decisive role in accelerating automotive composites market trends. Regulatory frameworks focused on fuel efficiency and lifecycle emissions indirectly favor lightweight materials over traditional metals. Electrification strategies adopted by global automakers increase reliance on composites to balance battery weight and structural demands. At the same time, innovation waves in materials science deliver improved fiber-resin combinations that enhance crash performance and thermal stability.

Additional growth momentum emerges from platform standardization and modular vehicle architectures. Composites offer design freedom that supports part consolidation and functional integration, reducing assembly complexity. Global supply chain diversification also encourages localized composite production, improving responsiveness to regional demand. Together, these forces reinforce sustained automotive composites market share expansion as composites shift from optional enhancements to essential structural materials across vehicle categories.

RESTRAINING FACTORS

Recycling Challenges Are Expected to Hamper the Market

The recycling challenges in the automotive composites market are not as simple and straightforward as recycling for metallic materials. The reason behind this is that the fiber reinforcement parts are often joined to the other parts, such as fixing with metal. The complexity in disassembly, separation, and de-bonding from automotive components to be recycled is the major obstacle. Furthermore, even if the parts can be separated from each other, it is difficult to extract individual materials from the composite. This is due to the fact that composites are a mix of different materials and cannot be melted down and recycled. Thus, the various recycling laws on the plastic and composites market and their cost-ineffective recycling process are hindering the market.

Despite favorable automotive composites market growth dynamics, several structural challenges continue to limit adoption at scale. High initial capital requirements remain a primary barrier, particularly for small and mid-sized suppliers. Composite manufacturing demands specialized equipment, tooling, and process expertise, increasing upfront investment and extending return timelines. These constraints slow entry for new participants and restrict rapid capacity expansion.

Regulatory and compliance risks also shape market development. Automotive composites must meet stringent safety, recyclability, and durability standards across regions. Certification processes can be lengthy and costly, especially for structural applications. Differences in regional regulatory frameworks further complicate product standardization and increase compliance overhead for global manufacturers.

Operational challenges persist across the value chain. Skilled labor shortages in composite engineering, design, and manufacturing limit production efficiency. Process variability and quality control remain more complex than conventional metal stamping. Repairability concerns also affect aftermarket acceptance, as composite components often require specialized repair protocols.

Market saturation risks emerge in select applications where composites already dominate, such as premium exterior panels. Pricing pressure intensifies as more suppliers enter these segments, compressing margins. Additionally, volatility in raw material availability, particularly carbon fiber, exposes manufacturers to supply disruptions. These combined constraints influence the automotive composites market size expansion, requiring sustained investment in process innovation, workforce development, and supply chain resilience to maintain long-term competitiveness.

AUTOMOTIVE COMPOSITES MARKET SEGMENTATION ANALYSIS

By Fiber Analysis

Glass Fiber to Hold the Largest Share in this Market

Based on fiber type, the global market study on automotive composites is classified into glass, carbon, and natural automotive composites.

Glass fiber composites are mainly used in the automotive industry due to properties such as high strength, stiffness, flexibility, and resistance to chemical harm. In the past few years, there has been a remarkable demand for lightweight materials to increase fuel efficiency due to the demand for emission reduction. As glass fiber composites are affordable than carbon and natural fiber, they are heavily used in the automotive industry.

Glass fiber composites represent the broadest adoption base. They balance mechanical strength, corrosion resistance, and cost efficiency, making them suitable for high-volume vehicle programs. Exterior panels, underbody shields, and semi-structural components increasingly rely on glass fiber systems. Although margins remain moderate, scale-driven demand sustains a stable automotive composites market share.

Moreover, automotive body parts such as engine hood, storage tanks, and dashboards are manufactured using natural fiber composites to reduce the use of other metals such as steel and aluminum, and to promote the application and region of the bio-based material in the automotive industry.

Carbon fiber composites occupy the premium performance segment. Their high strength-to-weight ratio supports structural and powertrain applications where mass reduction directly improves efficiency. Adoption remains selective due to cost and processing constraints, but value density is high. Automakers deploy carbon fiber strategically in electric vehicles and performance-oriented platforms, where lightweighting delivers measurable range and handling benefits.

Natural fiber composites are emerging as a differentiated sustainability segment. Applications include interior panels, trims, and non-load-bearing components. While mechanical limits restrict structural use, natural fibers offer lifecycle advantages and lower environmental impact. Value creation here is driven by regulatory alignment and brand positioning rather than pure performance.

By Resin Type

Thermoset Segment to Account for the Major Share during the Forecast Period

In terms of resin, the market is segmented into thermoset and thermoplastics.

Thermoset composites continue to dominate automotive applications. Epoxy and polyester systems provide dimensional stability and durability under thermal stress. These materials support complex geometries and are widely compatible with established manufacturing lines. Their market position benefits from process familiarity and predictable performance.

The demand for thermoset is higher than that from the thermoplastic resin segment. The thermoset materials are used in a wide range of automobile applications, such as headlamp housing, under the hood, electrical, and heat shielding components, and exterior and interior structural parts. Moreover, the thermoset resins have a low coefficient of thermal expansion, high impact strength, excellent dimensional stability, and many other composite properties.

Thermoplastic composites are gaining momentum as production priorities shift toward recyclability and shorter cycle times. Their ability to be reshaped and welded supports modular assembly and end-of-life recovery. Although material costs remain higher, thermoplastics unlock long-term automotive composites market growth through scalable manufacturing and sustainability compliance.

Furthermore, the main advantage of thermoplastic resin over thermoset resins is that they are tougher, more recyclable, and have the ability to deliver a fast manufacturing process, but due to their higher melt viscosity than thermoset, the infusion process could lead to improper impregnation.

By Application Area Analysis

To know how our report can help streamline your business, Speak to Analyst

Exterior Segment to Hold The Largest Share In The Global Automotive Composites Industry

Based on the application area, the market is segmented into the exterior, interior, structural, and power train, and others.

The exterior type holds the largest share in the global market. Automotive composites are widely used in exterior automotive applications such as headlamps, heat shielding components, and others. Many OEMs are also focusing on incorporating composites in their car bodies. For instance, recent development confirms that reinforced thermoplastics could be the next wave. BMW’s i3 is the first mass-produced car to have thermoplastic composites in its exterior parts.

Exterior applications generate consistent demand as composites replace steel and aluminum for panels, hoods, and aerodynamic components. Benefits include corrosion resistance, design flexibility, and surface quality. Margins improve when composites enable part consolidation and tooling reduction.

The automotive industry has been using more and more natural composites in the interior parts of the vehicles as an alternative to glass fiber as a light-weighting solution. The Exterior segment is expected to hold a 43.47% share in 2018.

Interior applications emphasize comfort, acoustics, and aesthetics. Composites deliver lightweight structures with integrated features, supporting premium cabin experiences. Value creation here is closely tied to consumer expectations rather than regulatory pressure.

Structural and powertrain applications represent the highest value potential. Battery enclosures, load-bearing frames, and crash structures increasingly incorporate composites to manage weight and safety simultaneously. These applications drive long-term automotive composites market trends, though adoption requires close collaboration between material suppliers and OEM engineering teams.

REGIONAL ANALYSIS

North America Automotive Composites Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America emphasizes lightweighting to support fuel efficiency and electric vehicle range targets. Composite adoption remains strongest in structural, battery enclosure, and pickup truck applications. Regulatory focus on emissions and safety supports steady material substitution, while localized supply chains strengthen supplier resilience. North America witnessed a growth from USD 2.30 billion in 2017 to USD 2.40 billion in 2018.

United States

The United States automotive composites market centers on performance optimization and manufacturing scalability. Composites see strong uptake in pickup trucks, sport utility vehicles, and electric platforms. Domestic OEMs prioritize composites for battery protection, crash management, and corrosion resistance. Federal emissions standards and state-level electric vehicle incentives reinforce adoption. Supplier competition favors vertically integrated players with proximity to OEM assembly plants and strong tooling capabilities.

Asia Pacific

The automotive composites market size in the Asia Pacific stood at USD 2.03 billion in 2018. Asia Pacific is the largest and fastest-growing region in this market, owing to the highest number of vehicles present in this region, especially in countries like China, India, and Thailand. Moreover, India, Indonesia, Thailand, and China are expected to have the highest number of vehicles on the road, and India and China have the largest market for four-wheelers, which shall further drive the growth of the market. The market in North America is characterized by substantial government support for energy-saving automotive composites, such as natural fiber composites.

Asia-Pacific represents the largest volume opportunity. High vehicle production scale drives demand for cost-efficient glass fiber composites. China accelerates composite use in electric vehicles, while Japan focuses on precision engineering and material innovation. Regional growth balances scale with selective high-performance adoption.

Japan

Japan prioritizes material efficiency, reliability, and manufacturability. Glass fiber composites dominate high-volume models, while carbon fiber use expands selectively in electric and hybrid platforms. Domestic suppliers emphasize continuous improvement in processing speed and defect reduction. Automotive composites market growth aligns closely with hybrid vehicle penetration and export-oriented production.

China

China represents the fastest-expanding opportunity within the automotive composites market. Electric vehicle production accelerates composite adoption in battery housings, underbody shields, and lightweight structures. Government policy encourages local material sourcing, intensifying competition among domestic composite suppliers. Scale-driven manufacturing supports rapid diffusion of cost-effective composite solutions.

Europe

Furthermore, considerable awareness among the people in the region is expected to keep the market up and moving for natural composites. The growth opportunities for the European automotive composites market are governed by the usage of automotive composites, which is environmentally friendly. Furthermore, various OEMs present in Europe are focusing on natural composites to support government policies.

Europe leads in sustainability-driven composite adoption. Strict emissions regulations and circular economy policies accelerate thermoplastic and recyclable composite use. Automotive composites market trends favor carbon fiber and advanced hybrid materials, particularly in premium and electric vehicle platforms.

Germany

Germany anchors Europe’s high-performance composite ecosystem. Premium vehicle manufacturers deploy carbon fiber and hybrid composites extensively in structural and exterior applications. Engineering-led procurement emphasizes stiffness-to-weight ratios, lifecycle durability, and precision tolerances. Automotive composites market share in Germany skews toward advanced materials, supported by strong research institutes and collaborative supplier–OEM development models.

United Kingdom

The United Kingdom market benefits from niche vehicle manufacturing and motorsport-derived innovation. Composites adoption focuses on lightweight structures, luxury interiors, and limited-volume electric vehicles. Smaller production runs favor high-value composite solutions over scale-driven cost optimization. Government-backed innovation programs support material development and advanced manufacturing.

Latin America and the Middle East & Africa

The market in Latin America and the Middle East & Africa is in the growth stage of the life cycle, thus it shall gain market share during the forecast period. The growth of the automotive industry in these regions is expected to fuel the market. Therefore, the market in these regions will show more attractive growth during the forecast period.

How competitive is the market?

Key Players Are Adopting Merger and Acquisition Growth Strategies to Maintain Their Dominance in this Market

The competitive landscape of this market depicts a consolidated market with the top 10 companies accounting for about 50% of the global market revenue. Major players in the market have invested a considerable amount of resources in research and development of several automotive composite products. A diversified product portfolio, supported by superior operational efficiency, and safe & novel technology development for composite applications, are the strategies used by the market leaders for their growth.

Furthermore, small and medium-scale companies have adopted the strategy of mergers and partnerships with larger enterprises to improve their offering portfolio and other related services. This trend is projected to positively impact the global market during the forecast period, as the smaller companies can gain a lot from the experience of the market leaders.

The automotive composites market features a competitive landscape shaped by material specialization, manufacturing scale, and engineering depth. Large multinational suppliers dominate structural and high-performance applications, leveraging long-term OEM relationships and integrated material portfolios.

Mid-sized challengers compete by offering application-specific expertise, rapid prototyping, and cost-optimized solutions for regional markets. Emerging players focus on thermoplastics, natural fibers, and recyclable composites, aligning with sustainability-driven procurement.

Market share concentration remains moderate, as OEMs favor multi-sourcing strategies to reduce supply risk. Partnerships between material producers, processors, and tooling specialists are common, supporting integrated value delivery. Merger and acquisition activity targets capability expansion in automation, simulation, and sustainable materials rather than pure capacity growth.

Artificial intelligence supports defect detection, process optimization, and predictive maintenance in composite manufacturing. Data-driven quality control enhances consistency, critical for structural automotive applications.

Emerging bio-based resins and hybrid fiber systems address sustainability requirements without sacrificing performance. These technologies expand composite use beyond premium segments into higher-volume platforms, strengthening competitive positioning for early adopters.

What are the opportunities for growth and investment?

Attractive opportunities in the automotive composites market concentrate where regulation, electrification, and manufacturing innovation intersect.

Key opportunity areas include:

- Structural composites for electric vehicle platforms

- Recyclable thermoplastic systems aligned with circular economy policies

- Battery enclosures and thermal management components

- High-growth Asia-Pacific electric vehicle supply chains

- Integrated design–manufacturing service models

White-space opportunities exist in mid-priced vehicles, where cost-efficient composites can replace metals at scale. Adjacent growth paths include mobility platforms, autonomous vehicle structures, and lightweight commercial vehicles.

List of Top Automotive Composites Companies:

- Teijin Ltd.

- Mitsubishi Chemical Corporation

- Toray Industries, Inc.

- SGL Carbon

- RTP Company

- Plasan Carbon Composites

- Owens Corning

- Solvay S.A.

- UFP Technologies, Inc.

- BASF SE

- Other Players

KEY INDUSTRY DEVELOPMENTS:

- February 2021 – Teijin Ltd. announced the installation of a glass fiber sheet molding compound line at the company’s automotive composites business named ‘Benet Automotive s.r.o’. The investment was made to meet growing demand for Teijin’s composite parts from European automotive manufacturers.

- January 2021 – SGL Carbon announced an investment of USD 4.5 million at its Arkansas site to expand the production of carbon composites for electric vehicles. The company is engaged in the manufacturing of carbon and glass fiber reinforced products for automotive applications. The new capacity addition will be used to meet growing demand for composite battery enclosures of modern e-car chassis.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The automotive composites market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, resin, fiber, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Kilo Tons) |

|

Segmentation |

By Fibre

|

|

By Resin

|

|

|

By Application Area

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global automotive composites market was valued at USD 11.22 billion in 2025 and is projected to reach USD 41.55 billion by 2034, growing at a CAGR of 15.66% during the forecast period.

Automotive composites are used in manufacturing vehicle body panels, chassis components, interior trims, bumpers, dashboards, and structural parts. They reduce vehicle weight, improve fuel efficiency, and enhance design flexibility and durability.

The most common materials include glass fiber composites, carbon fiber composites, and natural fiber composites, often combined with thermoset or thermoplastic resins for enhanced performance and lightweight design.

Electric vehicles (EVs) and high-performance sports cars are major drivers due to the need for lightweight structures that enhance battery efficiency and speed performance while reducing carbon emissions.

Benefits include weight reduction, fuel efficiency, corrosion resistance, design versatility, and improved crash performance. These factors are crucial for automakers aiming to meet environmental regulations and customer demands.

Asia Pacific dominates the market due to large-scale automotive production in China, India, and Japan. Europe and North America follow, supported by stringent emission norms and increasing EV adoption.

Top companies include Toray Industries, SGL Carbon, Teijin Limited, Mitsubishi Chemical Holdings, Hexcel Corporation, Gurit Holding AG, and Owens Corning, known for innovations in carbon and glass fiber technologies.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us