Automotive Cross-Member and Side-Member Systems Market Size, Share & Industry Analysis, By Product Type (Side Members, Front Cross Members, Rear Cross Members, Underbody Cross Members & Subframe Assemblies), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs & HCVs), By Propulsion (ICE & Electric), By Material Type (High-Strength Steel (HSS), Advanced High-Strength Steel (AHSS), Aluminum & Aluminum Alloys, Magnesium Alloys & Multi-Material/Hybrid Structures), By Manufacturing Process (Stamping & Welding, Hydroforming, Roll Forming, Casting & Extrusion & Machining) and Regional Forecast, 2026-2034

Automotive Cross-Member and Side-Member Systems Market Size Overview

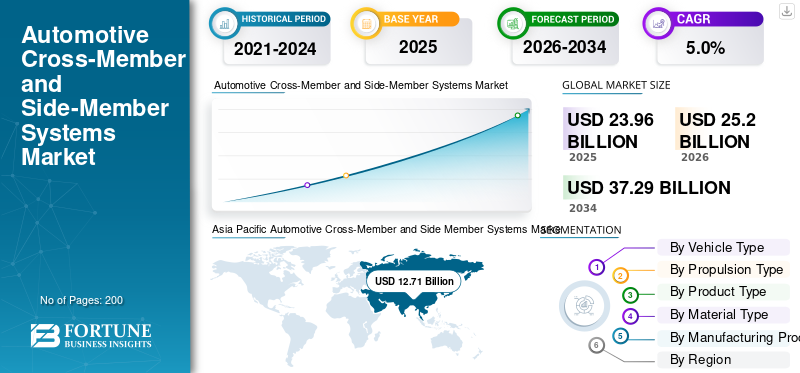

The global automotive cross-member and side-member systems market size was valued at USD 23.96 billion in 2025. The market is projected to grow from USD 25.20 billion in 2026 to USD 37.29 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the global market with a market share of 53.04% in 2025.

Automotive cross-member and side-member systems are structural chassis components forming the vehicle frame, providing load distribution, crash protection, mounting support and overall body rigidity for safe vehicle operation.

The market growth is driven by rising vehicle production, stricter safety regulations, lightweighting demand, electrification, improved crash performance requirements, and increased use of advanced materials in automotive structural components.

Major players in the market include Magna International, Benteler, Gestamp, Martinrea, and Aisin Seiki, competing through lightweight materials, advanced forming technologies, modular designs and enhanced crash management solutions.

Download Free sample to learn more about this report.

Automotive Cross-Member and Side-Member Systems Market Key Takeaways

- 2025 Market Size: USD 23.96 billion

- 2026 Market Size: USD 25.20 billion

- 2034 Forecast Market Size: USD 37.29 billion

- CAGR: 5.0% from 2026–2034

- Asia Pacific dominated the automotive cross-member and side-member systems market with a 53.04% share in 2025.

- Hatchback & sedans held the second-largest market share and are projected to grow at a CAGR of 3.9%.

- The electric vehicle segment is the fastest-growing segment, expanding at a CAGR of 8.2% during the forecast period.

Asia Pacific

Asia Pacific remains the largest and fastest-growing market, supported by strong vehicle production and rising EV demand.

Europe

Europe is the second-largest market, driven by stringent safety regulations and vehicle lightweighting initiatives.

North America

North America maintains steady growth due to strong demand for SUVs, pickups, and light commercial vehicles.

U.S.

The market is estimated at USD 3.09 billion in 2026, accounting for approximately 12.3% of global revenue.

Japan

The market is estimated at USD 1.98 billion in 2026, representing roughly 7.9% of global revenue.

Read More

AUTOMOTIVE CROSS-MEMBER AND SIDE-MEMBER SYSTEMS MARKET TRENDS

Light weighting through Advanced Materials and Forming Technologies are Key Trends

One of the key market trends is the light weighting of cross members and side members through advanced materials and forming technologies. Automakers are increasingly adopting high-strength steel, aluminum and mixed-material and carbon fiber solutions to reduce vehicle weight without compromising safety. Automotive cross-member and side-member systems are being optimized using hydroforming, hot stamping and tailored blanks. This trend supports enhancing fuel efficiency and EV range improvement targets. Continuous material innovation and advanced manufacturing are reshaping structural component design strategies globally.

MARKET DYNAMICS

MARKET DRIVERS

Stricter Safety and Crashworthiness Regulations to Drive Market Growth

Rising global safety regulations, leading to increased need for robust automotive structures droves global automotive cross-member and side-member systems market growth. Automotive cross-member and side-member systems play a critical role in crash energy absorption and occupant protection. Regulatory bodies in North America, Europe and Asia Pacific are mandating improved crash performance, pushing OEMs to adopt advanced structural designs. This consistently drives demand for high-strength, precision-engineered cross-member and side-member systems across passenger and commercial vehicles. Thus stricter safety and crashworthiness regulations drive the market expansion.

- In August 2025, India’s Automotive Research Association (ARAI) published updated Automotive Industry Standards (AIS) covering vehicle safety and construction requirements, reinforcing stricter structural and safety norms before vehicles and components can be certified for the Indian market.

MARKET RESTRAINTS

High Development and Tooling Costs to Limit New Entrants

Automotive cross-member and side-member systems require heavy capital investment in tooling, stamping, hydroforming and welding technologies. Developing lightweight vehicles yet crash-compliant structures involves extensive testing and validation. These high upfront production costs can restrain smaller manufacturers and slow capacity expansion. As a result, market participation remains concentrated among established Tier-1 suppliers with strong financial and engineering capabilities.

MARKET OPPORTUNITIES

Electrification and EV Platform Redesigns Creates New Design Opportunities

The shift toward electric vehicles (EVs) is opening opportunities for redesigned structural architectures. Battery packs require new load paths, underbody protection, integration of advanced driver assistance systems (ADAS) and reinforced side-members. These are increasingly integrated to support battery enclosures and improve torsional rigidity. This transition allows suppliers to co-develop modular, EV-specific structural systems with OEMs, creating fresh revenue streams beyond conventional internal combustion platforms.

- In December 2025, China’s electric vehicle maker Leapmotor announced plans to boost annual sales to more than 4 million units within the next decade, aiming for 1 million sales by 2026 and expanding globally with a Stellantis partnership and new premium models.

MARKET CHALLENGES

Managing Structural Complexity Across Multiple Vehicle Platforms as a Challenge

OEMs are pursuing platform consolidation while demanding high customization across regions and vehicle types. This creates challenges in designing automotive cross-member and side-member systems that balance standardization with localized performance requirements. Suppliers must manage complexity in design, tooling and supply chains while maintaining cost effective solutions. Coordinating multiple platforms without compromising structural integrity remains a critical industry challenge.

Download Free sample to learn more about this report.

Automotive Cross-Member and Side-Member Systems Market Segmentation Analysis

By Vehicle Type

Rising SUV Production and Structural Reinforcement Needs Propels SUVs Segmental Requirement

Based on vehicle type, the market is segmented into hatchbacks & sedans, SUVs, LCVs, and HCVs.

The SUVs segment holds the largest automotive cross-member and side-member systems market share, due to high global SUV production and increasing structural complexity. SUVs require stronger cross-members and reinforced side-members to support higher vehicle weight, elevated ride height and improved vehicle crash protection. Growing consumer preference for SUVs, coupled with stringent safety norms and electrified SUV platform launches, sustains strong OEM demand for advanced structural systems across major automotive sectors.

- In July 2025, Nissan confirmed specifications for the 2025 Ariya ahead of its Australian launch, highlighting its flat battery pack with integrated cross-member structure for rigidity and a spacious flat-floor EV architecture, alongside Australian availability from September with multiple battery options.

The hatchback & sedans segment holds the second-largest share and is projected to grow at a CAGR of 3.9%. Stable passenger car production, continued urban demand and incremental structural upgrades to meet safety and demand for lightweight structures support steady, moderate growth across mature and emerging markets.

By Propulsion Type

Large Installed ICE Vehicle Base and Mature Platform Designs Leads to ICE Segment Dominance

Based on propulsion type, the market is segmented into ICE and electric.

The ICE segment dominates the market due to its vast global vehicle production base and long-established platform architectures. ICE vehicles rely on well-defined structural layouts to support engines, transmissions and exhaust systems, driving consistent demand for cross-members and side-members. Ongoing production of passenger and commercial ICE vehicles, especially in emerging markets, leads to high-volume OEM demand despite gradual electrification.

The electric segment is the fastest-growing, expanding at a CAGR of 8.2%, over the forecast period. Rapid EV adoption is driving redesigned structural systems to support battery packs, underbody protection and improved crash load paths, accelerating demand for advanced cross-member and side-member solutions.

- According to the IEA, global electric car sales exceeded 17 million in 2024, growing over 25%, with the additional 3.5 million vehicles sold in 2024 alone surpassing total global electric car sales recorded in 2020.

By Product Type

Primary Load-Bearing Role and Structural Integration Augments Side Members Segment Growth

By product type, the market is divided into side members, front cross members, rear cross members, underbody cross members and subframe assemblies.

Side members dominate the market as they form a backbone of the vehicle structure. They carry longitudinal loads, support major powertrain and suspension components, and play a critical role in frontal and side-impact crash management. Their essential function across all vehicle types and propulsion platforms ensures consistent demand, reinforced by stricter safety regulations and increasing vehicle size and weight.

The underbody cross members segment market is expected to propel at a CAGR of 6.8%. This growth is driven by EV platform architectures requiring battery protection, improved torsional rigidity and optimized load distribution, increasing the adoption of advanced underbody structural solutions.

To know how our report can help streamline your business, Speak to Analyst

By Material Type

Cost Efficiency, Strength and Safety Compliance Advances High-Strength Steel Segment Growth

By Material Type, the market is categorized into High-Strength Steel (HSS), Advanced High-Strength Steel (AHSS), aluminum & aluminum alloys, magnesium alloys, and multi-material/hybrid structures.

High-Strength Steel (HSS) dominates the market of automotive cross-member and side-member systems due to its optimal balance of strength, formability, and cost. HSS enables effective crash energy absorption while meeting stringent safety regulations across vehicle segments. Its compatibility with existing stamping and welding infrastructure further supports large-scale adoption by OEMs, ensuring sustained demand across ICE and electric vehicle platforms globally.

The aluminum & aluminum alloys segment is the fastest-growing, expanding at a CAGR of 6.3%. Light weighting requirements, EV range optimization and improved aluminum forming technologies are driving increased use of aluminum structural members in next-generation vehicle architectures.

- In August 2024, Brazil’s Mover program emphasized aluminum adoption in automotive structures, promoting lightweight cross members and side members to support green mobility, EV adoption, and lower vehicle emissions through structural mass reduction.

By Manufacturing Process

High Production Scalability and Proven Structural Performance Boosts Stamping & Welding Segment Growth

By manufacturing process, the market is categorized into stamping & welding, hydroforming, roll forming, casting, and extrusion & machining.

Stamping and welding segment dominate the market due to their cost efficiency, high production scalability and proven structural reliability. These processes are well-suited for high-strength steel components, enabling precise load-path control and consistent crash performance. Established manufacturing infrastructure and widespread OEM acceptance further reinforce their dominance across mass-market passenger and commercial vehicle platforms.

Casting is the fastest-growing segment among all the manufacturing processes, registering a CAGR of 6.9%. Growing adoption of lightweight and integrated structural components in EVs and premium vehicles is accelerating demand for advanced aluminum and magnesium casting technologies.

Automotive Cross-Member and Side-Member Systems Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific and the rest of the world.

Asia Pacific

Asia Pacific Automotive Cross-Member and Side Member Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and remains the fastest-growing market, driven by high vehicle production volumes in China, India, Japan and Southeast Asia. Rapid urbanization, rising disposable incomes, and strong demand for SUVs and electric vehicles support structural component demand. The region also benefits from expanding local OEM manufacturing, cost-competitive supplier bases, and increasing enforcement of vehicle safety norms, accelerating the adoption of advanced structural designs.

- In 2024, China maintained its global EV leadership, with electric cars accounting for nearly half of total vehicle sales. Over 11 million EVs were sold, surpassing global sales from two years earlier, resulting in one in ten cars on Chinese roads being electric.

China Automotive Cross-member and Side-member Systems Market

The China market in 2026 is estimated at around USD 7.68 billion, accounting for roughly 30.5% of global revenues. China dominates Asia Pacific region, driven by high vehicle production, light weighting, and EV platform scaling.

Japan Automotive Cross-member and Side-member Systems Market

The Japan market in 2026 is estimated at around USD 1.98 billion, accounting for roughly 7.9% of global revenues. The market growth in Japan is supported by hybrid production, advanced materials adoption and structural safety optimization.

India Automotive Cross-member and Side-member Systems Market

The India market in 2026 is estimated at around USD 1.51 billion, accounting for roughly 6.0% of global revenues. Rapid growth stems from rising vehicle volumes, localization, and cost-efficient modular chassis designs.

Europe

Europe holds the second-largest market share and is projected to grow at a CAGR of 4.2%. Stringent crash safety regulations, aggressive vehicle light weighting targets and strong EV penetration drive demand for advanced automotive cross-member and side-member systems. OEMs focus on aluminum, mixed-material architectures and modular vehicle platforms further supports structural innovation. Stable passenger vehicle production and premium vehicle concentration sustain consistent OEM-level demand across major European automotive hubs.

- In August 2025, KIRCHHOFF Automotive highlighted advanced body-in-white solutions, including optimized cross members and side members, showcasing lightweight steel and aluminum structural components designed to improve crash performance and modular vehicle platform compatibility.

Germany Automotive Cross-member and Side-member Systems Market

The Germany market in 2026 is estimated at around USD 1.34 billion, accounting for roughly 5.3% of global revenues. Germany’s growth in the market is fueled by premium vehicle demand, EV architectures, and lightweight aluminum-intensive structures.

U.K. Automotive Cross-member and Side-member Systems Market

The U.K. market in 2026 is estimated at around USD 0.30 billion, accounting for roughly 1.2% of global revenues. Growth in U.K. market is supported by EV assembly, platform consolidation, and supplier-led structural innovations.

North America

North America represents a mature yet significant market, supported by strong demand for SUVs, pickups, and light commercial vehicles. These vehicle types require reinforced side-members and robust cross-member systems to meet performance and safety expectations. Platform consolidation strategies by OEMs encourage standardized yet high-value structural components. Additionally, rising EV investments in the U.S. and Canada are gradually reshaping structural designs, supporting steady long term market expansion.

- In February 2023, Ford introduced the next-generation Ranger Raptor, featuring a strengthened ladder frame with reinforced side members and redesigned cross members to enhance off-road durability and high-speed stability.

U.S. Automotive Cross-member and Side-member Systems Market

The U.S. market in 2026 is estimated at around USD 3.09 billion, accounting for roughly 12.3% of global revenues. The U.S. leads North America market due to high SUV and pickup production, strong OEM concentration, strict safety regulations, and rising EV investments, driving sustained demand for robust cross-member and side-member structural systems.

Rest of the World

The Rest of the World market is driven by gradual motorization, expanding vehicle ownership, and increasing local assembly activities in regions such as Latin America and Middle East & Africa. Improving safety awareness and regulatory alignment with global standards is encouraging the adoption of stronger structural components. While volumes remain lower than in developed regions, long-term growth is supported by infrastructure development, rising SUV penetration, and the entry of global OEM manufacturing operations.

COMPETITIVE LANDSCAPE

Key Industry Players

OEM-Centric Design Collaboration and Lightweight Structural Innovation to Shape Competitive Dynamics

The automotive cross-member and side-member systems market is characterized by strong Tier-1 supplier dominance and close OEM collaboration. Key players such as Magna International, Benteler, Gestamp, Martinrea, and Aisin Seiki compete through lightweight material innovation, advanced forming technologies and modular structural designs. Companies focus on co-developing crash-optimized architectures for ICE and electric platforms. To strengthen competitiveness, manufacturers invest in research and development, suppliers invest in aluminum and mixed-material capabilities, regional manufacturing expansion and platform-based solutions. Strategic partnerships, long-term OEM contracts and localized production help manage costs, ensure supply continuity and support global vehicle programs.

LIST OF KEY AUTOMOTIVE CROSS-MEMBER AND SIDE-MEMBER SYSTEMS COMPANIES PROFILED

- Magna International (Canada)

- Benteler Group (Germany)

- Gestamp Automoción (Spain)

- Martinrea International (Canada)

- Aisin Corporation (Japan)

- Hyundai Mobis (South Korea)

- CIE Automotive (Spain)

- Tower International (U.S.)

- Dana Incorporated (U.S.)

- Thyssenkrupp Automotive Body Solutions (Germany)

- Kirchhoff Automotive (Germany)

- Schaeffler AG (Germany)

- Kautex Textron (U.S.)

- Nemak (Mexico)

- Constellium Automotive Structures (France)

KEY INDUSTRY DEVELOPMENTS

- In January 2025, Italdesign unveiled the Quintessenza concept at CES 2025, showcasing innovative modular architecture with integrated cross members and side members supporting electrification, performance, and advanced vehicle packaging.

- In October 2024, Lexus introduced updates to its global model lineup, highlighting reinforced side members and optimized cross-member structures to improve body rigidity, crash safety, and ride comfort across premium vehicle platforms.

- In July 2024, Malben Engineering detailed its data-centric welding automation approach, enhancing quality control and consistency in welded automotive structures such as side members and cross members used in safety-critical vehicle frames.

- In June 2024, BMW recalled select i4 electric vehicles in Europe due to potential defects in rear side members, which could affect structural integrity and crash safety performance under specific driving conditions.

- In February 2024, Nifco announced new plastic structural components supporting vehicle underbody applications, complementing metal cross members and side members by improving NVH performance and under-floor protection efficiency.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Propulsion Type, By Product Type, By Material Type, By Manufacturing Process, and By Region |

|

By Vehicle Type |

· Hatchbacks & Sedans · SUVs · LCVs · HCVs |

|

By Propulsion Type |

· ICE · Electric |

|

By Product Type |

· Side Members · Front Cross Members · Rear Cross Members · Underbody Cross Members · Subframe Assemblies |

|

By Material Type |

· High-Strength Steel (HSS) · Advanced High-Strength Steel (AHSS) · Aluminum & Aluminum Alloys · Magnesium Alloys · Multi-Material/Hybrid Structures |

|

By Manufacturing Process |

· Stamping & Welding · Hydroforming · Roll Forming · Casting · Extrusion & Machining |

|

By Geography |

· North America (By Vehicle Type, By Propulsion Type, By Product Type, By Material Type, By Manufacturing Process, and By Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, By Propulsion Type, By Product Type, By Material Type, By Manufacturing Process, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, By Propulsion Type, By Product Type, By Material Type, By Manufacturing Process, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, By Propulsion Type, By Product Type, By Material Type, By Manufacturing Process) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 23.96 billion in 2025 and is projected to reach USD 37.29 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 12.71 billion.

The market is expected to exhibit a CAGR of 5.0% during the forecast period of 2026-2034.

The SUVs segment leads the market in terms of vehicle type.

Stricter safety and crashworthiness regulations to drive structural demand

Key players in the market include Magna International, Benteler, Gestamp, Martinrea, and Aisin Seiki, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us