Automotive E-Compressor Market Size, Share & Industry Analysis, By Compressor Output Type (Fixed-Speed and Variable-Speed), By Vehicle Type (Hatchback/Sedan, SUVs, Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs)), By Voltage Class (High-Voltage and Low-Voltage), By Powertrain (BEV and Hybrid), By Application (Cabin A/C, Heat Pump System, Battery Thermal Management, Power Electronics/Motor Thermal Management, and Integrated Thermal Management), and Regional Forecast, 2026-2034

Automotive E-Compressor Market Size and Future Outlook

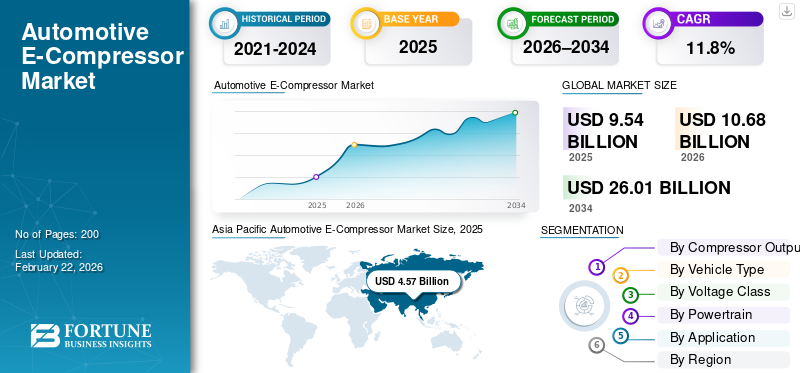

The global automotive e-compressor market size was valued at USD 9.54 billion in 2025. The market is projected to grow from USD 10.68 billion in 2026 to USD 26.01 billion by 2034, exhibiting a CAGR of 11.8% during the forecast period. Asia Pacific dominated the global automotive e-compressor market with a market share of 47.90% in 2025.

The global automotive e-compressor industry covers electrically driven compressors used to circulate refrigerant within vehicle HVAC systems. Unlike belt-driven units, these compressors operate independently of the engine, making them essential for electric vehicles (EVs) and increasingly crucial in hybrids that must maintain comfort during engine-off operation. As vehicle electrification expands, the market is gaining strategic importance as thermal loads are rising across cabins, batteries, and electronics. Modern automotive e-compressors support air conditioning systems and, in many new platforms, act as a core actuator within broader thermal management systems that balance cabin comfort, battery temperature, and power electronics efficiency.

Over the forecast period, market growth is expected to be driven by three major forces. First, rising electric-car production increases the installed base where e-compressors are mandatory. Second, the market is being reshaped by heat pumps and multi-loop architectures that require tighter control of refrigerant flow to stabilize range and charging performance across climates. Third, OEMs are focusing on energy efficiency and packaging, which favors compact, inverter-integrated, variable-speed compressor designs. In addition to passenger platforms, electrified fleets and light commercial vehicles are adopting more advanced climate control systems to protect cargo, electronics, and driver comfort.

Key players such as DENSO, Bosch, and Valeo are scaling capacity, broadening high-voltage portfolios, and improving system integration, as illustrated by Hanon Systems reaching a major production milestone with CO₂ (R744) electric compressors for EV heat pump systems.

Download Free sample to learn more about this report.

AUTOMOTIVE E-COMPRESSOR MARKET TRENDS

Integrated Thermal Modules Increase Compressor Value Per Vehicle

OEMs are moving from separate cooling subsystems toward integrated, multi-loop thermal management systems that coordinate cabin, battery, and power electronics within a single architecture. This trend increases demand for variable-speed compressors and integrated inverters that enable precise control and compact packaging. As these integrated climate control systems become mainstream, suppliers that offer modular platforms and software-ready controls will capture more content per vehicle.

- For instance, MAHLE describes new thermal management modules that combine multiple functions to reduce complexity and boost EV efficiency, supporting higher-value thermal content.

MARKET DYNAMICS

MARKET DRIVERS

Rising Electrification Makes E-Compressors a Must-Have Component

As electric vehicles scale, e-compressors become unavoidable as cabin cooling/heating and refrigerant circulation cannot depend on engine power. OEMs also add heat pumps and integrated loops to improve range and winter performance, increasing compressor content and value per vehicle. This structural shift steadily lifts demand for automotive e-compressors across passenger cars and commercial fleets, reinforcing long-term volume growth.

- For instance, DENSO highlights that thermal management systems are indispensable for EVs and use heat pump technology to efficiently control batteries, inverters, motors, and cabin comfort.

MARKET RESTRAINTS

High Integration and Safety Requirements Raise Cost and Complexity

The global automotive e-compressor supply chain faces higher costs due to high-voltage safety design, electronics integration, and stringent validation for wide temperature ranges. OEM qualification cycles can be long, and redesigns are costly as compressors interact with multiple vehicle domains. In addition, shifting to lower-GWP refrigerants can require new materials and designs, increasing engineering burden and compliance effort. This is expected to hinder the automotive e-compressor market growth in the coming years.

- For instance, the EU’s revised F-gas Regulation accelerates the transition toward lower-GWP refrigerants, increasing redesign pressure across refrigerant-based systems and related components.

MARKET OPPORTUNITIES

Natural Refrigerants and CO₂ Systems Unlock Premium Growth

A strong opportunity comes from next-generation refrigerants and heat pump designs that reduce environmental impact while improving cold-weather performance. CO₂ (R744) systems in particular can support efficient heating with lower climate impact, driving adoption of specialized compressors and enabling suppliers to secure multi-year platform awards. As EV makers standardize these architectures, value per vehicle can rise, strengthening market share for advanced compressor suppliers.

- For instance, Hanon Systems states that its R744 electric compressor supports EV heat pump systems and helps mitigate driving-range decline in cold weather.

MARKET CHALLENGES

Efficiency Trade-Offs Under Extreme Climates Remain Difficult

Even with advanced designs, EV heat pump and compressor systems face performance challenges in very hot or very cold conditions, where energy use can rise, and control becomes more complex. Maintaining stable cabin comfort while protecting battery health demands careful calibration, and any inefficiency can reduce range or charging performance. This pushes suppliers to invest heavily in testing, controls, and refrigerant-cycle optimization.

- For instance, Academic reviews note EV heat pump air-conditioning can consume significant power in hot/cold weather, highlighting ongoing technical challenges for vapor-compression systems.

Download Free sample to learn more about this report.

Segmentation Analysis

By Compressor Output Type

Variable-speed Segment Dominates as EV Thermal Loads Constantly Fluctuate

On the basis of compressor output type, the market is divided into fixed-speed and variable-speed. The variable-speed segment leads the automotive e-compressor market share as these units match compressor output to real-time cooling/heating demand, improving efficiency and comfort. They also support heat pumps and multi-loop thermal management systems, where precise control protects batteries and electronics while reducing energy draw. As EV adoption expands, OEMs prefer variable-speed solutions that help maintain range in diverse climates and enable advanced HVAC systems architectures.

- For instance, MAHLE notes e-compressors are the heart of thermal management in EVs and highlights strong order volumes in this product area.

The variable-speed segment is expected to grow at a CAGR of 12.6% over the forecast period.

By Vehicle Type

Hatchback/Sedan Segment Dominates as They Form Passenger Car Production Basis

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs).

The hatchback/sedan segment dominates the global market, as these body styles form the core of passenger car production, especially in Asia Pacific and Europe, where compact and mid-sized vehicles lead EV and hybrid adoption. Their consistent demand for reliable air conditioning systems and the growing integration of heat pumps sustain a high aggregate market share, despite lower per-unit ASPs than SUVs.

- For instance, Toyota Motor Corporation highlighted that compact and mid-sized electric sedans such as the Corolla Hybrid and bZ series remain central to its global electrification strategy due to their high volumes and mass-market affordability, reinforcing sustained demand for efficient HVAC and e-compressor systems.

The SUVs segment is expected to grow at a CAGR of 13.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Voltage Class

High-Voltage Segment Leads Market as It Supports Advanced Heat Pump Functions

On the basis of voltage class, the market is segmented into high-voltage and low-voltage.

The high-voltage segment dominates the market, as most battery-electric SUVs use high-voltage electrical architectures to power compressor operation and enable integrated inverter designs. This supports higher capacity, improved efficiency, and advanced heat pump functions, aligning with the evolving needs of climate control systems. As OEMs expand high-voltage platforms to mainstream SUV lines, demand for HV compressors remains structurally strong.

- For instance, Valeo expanded its high-voltage thermal offerings for EVs, reinforcing the shift toward high-voltage compressor portfolios that support modern electrified platforms.

The high-voltage segment is expected to grow at a CAGR of 12.3% over the forecast period.

By Powertrain

BEVs Dominate as Electric Compressors are Functionally Mandatory

On the basis of powertrain, the market is segmented into BEV and hybrid.

BEVs lead the market as refrigerant compression must be electric, and thermal needs extend beyond the cabin to batteries and electronics. Heat pumps and integrated loops further increase compressor duty cycle and value. As BEV production rises globally, suppliers secure multi-year contracts and scale manufacturing, strengthening BEV-led revenue growth across the forecast period.

- For instance, DENSO describes EV thermal management as indispensable, using heat pumps to maintain cabin comfort and support key electric components, thereby supporting BEV dominance.

The BEV segment is expected to grow at a CAGR of 12.8% over the forecast period.

By Application

Cabin A/C Dominates Due to Universal Requirement Across Vehicle Types

On the basis of application, the market is segmented into cabin A/C, heat pump system, battery thermal management, power electronics/motor thermal management, and integrated thermal management.

The cabin A/C remains the largest application as every electrified platform still requires reliable cabin cooling and defogging, regardless of whether it uses a heat pump. While battery and electronics loops are growing faster, cabin cooling remains the broadest installed base across passenger cars, SUVs, and light commercial vehicles. This keeps Cabin A/C the biggest value pool even as integrated architectures expand.

- For instance, DENSO explains that heat pump systems deliver cooling/dehumidification/heating functions to achieve cabin comfort, underscoring why cabin conditioning remains central.

The integrated thermal management segment is expected to grow at a CAGR of 15.4% over the forecast period.

Automotive E-Compressor Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive E-Compressor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 4.57 billion, and also maintained the leading share in 2024, with USD 4.05 billion. Asia Pacific dominates the market due to China-led EV scale, rapid platform launches, and dense local supply chains for HVAC systems components. High EV production volumes, growing heat pump penetration, and strong vertical integration support both unit demand and value growth. Regional OEMs also accelerate the adoption of advanced thermal management systems to protect batteries in varied climates, sustaining long-term leadership.

- For instance, Hanon Systems’ milestone in R744 electric compressor production reflects the scale-up of advanced compressor technologies used in EV heat pump systems.

China Automotive E-Compressor Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 3.13 billion, representing roughly 32.8% of the global market.

India Automotive E-Compressor Market

The India market in 2025 was valued at USD 0.21 billion, accounting for roughly 2.2% of global Automotive E-Compressor revenues.

North America

North America is projected to record a growth rate of 14.2% in the coming years, the highest among all regions, and to reach a valuation of USD 2.06 billion by 2026. North America is expected to grow steadily as EV and hybrid manufacturing expand, and OEMs localize critical supply chains. SUV-heavy electrification raises compressor capacity needs and increases value per vehicle, supporting higher ASPs through the forecast period. The U.S. remains the center of regional growth, driven by new EV platform launches and the broader adoption of integrated climate control systems for comfort and efficiency.

U.S. Automotive E-Compressor Market

Given North America’s strong contribution and the U.S. dominance within the region, the U.S. market valued at USD 1.49 billion in 2025, representing roughly 15.6% of the global market.

Europe

Europe is estimated to reach USD 2.59 billion in 2026 and secure the position of the second-largest region in the market. Europe grows on the back of stricter climate policy, higher efficiency expectations, and strong heat pump adoption in EV platforms. The region’s push toward lower-GWP refrigerants and integrated thermal management systems supports continued demand for advanced compressors and inverter-integrated designs, especially in premium vehicles.

Germany Automotive E-Compressor Market

The German market in 2025 was valued at USD 0.63 billion, accounting for roughly 6.6% of global automotive e-compressor revenues.

U.K. Automotive E-Compressor Market

The U.K. market in 2025 was valued at USD 0.47 billion, accounting for roughly 4.9% of global automotive e-compressor revenues.

Rest of the World

The rest of the world expands from a smaller base as electrified production and imports increase and charging ecosystems mature. Growth is strongest where fleets electrify first, and OEMs introduce localized assembly, gradually increasing demand for air conditioning systems and EV-ready HVAC systems components across emerging markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategies Intensify as Electrification Raises Thermal Stakes

Platform wins, technology differentiation, and global manufacturing reach shape competition in the automotive e-compressor market. Leading suppliers compete on efficiency, noise–vibration performance, durability, and compact packaging, as OEMs evaluate compressors not only as parts of heating, ventilation, and air conditioning architectures but also as enablers of total vehicle energy efficiency. A major battleground is variable-speed control and inverter integration, which can simplify wiring, reduce losses, and help OEMs optimize refrigerant cycles in demanding climates.

To gain an advantage, suppliers pursue several strategies. First, they invest in product roadmaps aligned with EV voltage migration and higher-capacity needs, building families of automotive e-compressors that scale from passenger cars to commercial platforms. Second, they embed the compressor into broader thermal management systems and heat pump modules, positioning themselves as system partners rather than component vendors. Third, they expand localized production and engineering to win regional programs and reduce supply risk. Fourth, suppliers strengthen aftermarket coverage for electrified thermal components, supporting lifecycle availability and serviceability as EV fleets expand.

Leading suppliers compete by upgrading compressor technology to improve efficiency, noise performance, and durability, while aligning designs with high-voltage electric platforms and next-generation thermal management requirements.

- For instance, in May 2024, Sanden announced a new production line in France for next-generation electric compressors, strengthening its European supply for accelerating vehicle electrification.

LIST OF KEY AUTOMOTIVE E-COMPRESSOR COMPANIES PROFILED

- DENSO Corporation (Japan)

- Hanon Systems (South Korea)

- Valeo (France)

- MAHLE (Germany)

- Toyota Industries Corporation (Japan)

- Marelli (Japan)

- Panasonic Automotive Systems (Japan)

- Mitsubishi Heavy Industries Thermal Systems (Japan)

- Bosch (Germany)

- Aisin Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Valeo unveiled its EDC-120 high-capacity electric compressor for electric buses at Busworld Europe. The product is designed for high thermal loads and integrates advanced power electronics, enabling efficient cabin climate control and battery thermal management in heavy-duty electric mobility applications.

- September 2025: Hanon Systems announced it had surpassed the cumulative production of one million CO₂ (R744) electric compressors. This milestone reflects strong OEM adoption of natural refrigerant heat pump systems in electric vehicles, supporting improved cold-climate performance and compliance with tightening global environmental regulations.

- May 2024: Sanden announced a new production line in France for next-generation electric compressors, strengthening its European manufacturing base to meet accelerating demand for electrification.

- May 2024: Hankook & Company Group announced actions to secure management rights in Hanon Systems through an additional stake-acquisition plan, reinforcing its strategic focus on thermal solutions.

- April 2024: Vitesco Technologies and Sanden announced a collaboration to develop an integrated thermal management system for BEVs, linking powertrain control expertise with compressor/thermal know-how.

- April 2024: Valeo announced the creation of its Valeo Power division as part of its electrification strategy, supporting tighter alignment of electrified power and thermal product roadmaps.

- March 2024: DENSO emphasized EV thermal management as central to improving range and energy utilization, supporting continued investment in heat pump and integrated control capabilities.

REPORT COVERAGE

The global automotive e-compressor market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.8% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Compressor Output Type, Vehicle Type, Voltage Class, Powertrain, Application, and Region |

|

By Compressor Output Type |

· Fixed-Speed · Variable-Speed |

|

By Vehicle Type |

· Hatchback/Sedan · SUVs · Light Commercial Vehicles (LCVs) · Heavy Commercial Vehicles (HCVs) |

|

By Voltage Class |

· High-Voltage · Low-Voltage |

|

By Powertrain |

· BEV · Hybrid |

|

By Application |

· Cabin A/C · Heat Pump System · Battery Thermal Management · Power Electronics/Motor Thermal Management · Integrated Thermal Management |

|

By Region |

· North America (By Compressor Output Type, Vehicle Type, Voltage Class, Powertrain, Application, and Country) o U.S. o Canada o Mexico · Europe (By Compressor Output Type, Vehicle Type, Voltage Class, Powertrain, Application, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Compressor Output Type, Vehicle Type, Voltage Class, Powertrain, Application, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Compressor Output Type, Vehicle Type, Voltage Class, Powertrain, Application, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.54 billion in 2025 and is projected to reach USD 26.01 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 4.57 billion.

The market is expected to exhibit a CAGR of 11.8% during the forecast period of 2026-2034.

The hatchback/sedan segment leads the market by vehicle type.

Rising electrification is driving the global market.

Denso, Valeo, Bosch, and Hanon are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us