Automotive Engine Encapsulation Market Size, Share & Industry Analysis, By Type (Engine Mounted, Body Mounted, and Both), By Fuel (Gasoline and Diesel), By Vehicle Type (Luxury and Non-luxury), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

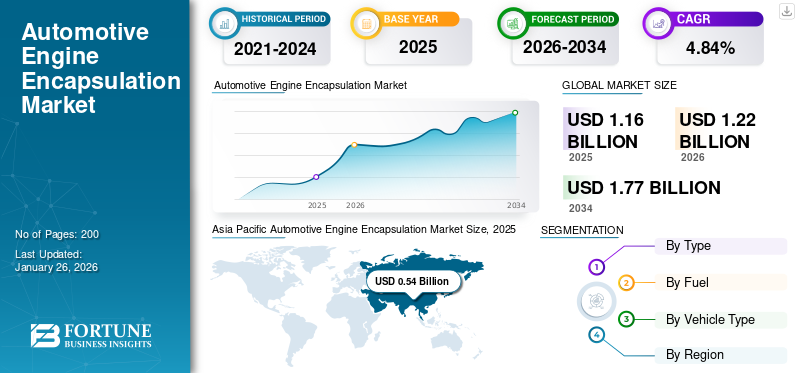

The global automotive engine encapsulation market size was valued at USD 1.16 billion in 2025. The market is projected to grow from USD 1.22 billion in 2026 to USD 1.77 billion by 2034, exhibiting a CAGR of 4.84% during the forecast period. Asia Pacific dominated the global market with a share of 46.54% in 2025.

Engine encapsulation is practice of isolating the engine from the vehicle's body using insulating materials and methods. The primary goal of this technique is to minimize the amount of heat, noise, and vibrations generated by the engine from reaching other parts of the vehicle, such as the passenger compartment. In doing so, engine encapsulation enhances the overall driving experience by improving comfort, reducing noise levels, and increasing fuel efficiency.

Key players in the market include Autoneum, Elringklinger AG, Rochling SE & Co. KG, Woco Group, Auria Solutions, and Pimsa Automotive, which compete in developing new products and pricing.

Engine bay is a harsh environment, exposed to dust, dirt, water, road salt, and temperature extremes. Engine encapsulation acts as a protective shield, safeguarding sensitive electronic components, wiring harnesses, sensors, and ancillary systems from these elements. Creating a cleaner, more stable environment helps prevent corrosion, extend the lifespan of critical parts, and reduce the likelihood of costly repairs. This added layer of protection contributes directly to vehicle reliability and perceived quality.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Focus on Noise, Vibration, and Harshness (NVH) Reduction to Augment the Market Growth

Perhaps the most immediately perceptible benefit of engine encapsulation is its profound impact on Noise, Vibration, and Harshness (NVH). Modern consumers, especially in the premium and luxury segments, demand increasingly quiet and refined cabin experiences. Engine noise, traditionally a significant contributor to cabin NVH, can be effectively muffled by encapsulation. These systems transform the driving environment by absorbing and dampening sound waves generated by the combustion process, ancillary systems, and mechanical vibrations.

This acoustic experience enhances quality and comfort, allows for clearer in-car communication, better enjoyment of audio systems, and reduces driver fatigue. Regulatory pressures, particularly in Europe, also play a role, with stricter limits on external vehicle noise levels pushing manufacturers toward comprehensive acoustic management solutions.

Market Restraint

High Production Cost May Hamper the Market Growth Over the Forecast Period

Encapsulation systems, particularly those utilizing advanced materials and complex designs, can substantially burden the overall vehicle manufacturing price. The cost of the necessary materials, such as high-temperature resistant polymers, specialized foams, and robust sealing components, contributes significantly to the automotive engine encapsulation market growth.

Furthermore, the development and tooling expenses associated with designing and manufacturing an encapsulation system tailored to a specific engine model can be prohibitive, especially for smaller production runs or budget-conscious vehicle segments. This cost sensitivity is particularly acute in price-sensitive markets and entry-level vehicle models, where manufacturers constantly seek ways to minimize expenses.

Market Opportunities

Surging Advancements in Material Science to Support the Market Growth

Advancements in materials science have led to the development of lightweight, durable, and heat-resistant materials, such as advanced plastics, composites, and specialized insulation materials. These materials offer superior thermal performance without adding significant vehicle weight, a crucial consideration for fuel efficiency. Furthermore, sophisticated design and manufacturing techniques, including 3D printing and advanced molding processes, allow for creating complex encapsulation geometries tailored to specific engine designs, optimizing thermal performance, and minimizing space requirements.

Market Challenges

Technical and Engineering Complexities May Affect the Market Growth

The engine bay is an extremely challenging environment: high temperatures, vibrations, fluid exposure, and tight packaging constraints. Designing an encapsulation system that effectively insulates against noise and heat while simultaneously allowing for adequate cooling of critical components is a delicate balancing act. Trapping heat too efficiently can lead to overheating of sensors, electronic control units (ECUs), and other heat-sensitive components, potentially compromising reliability and longevity.

Moreover, the added bulk of encapsulation materials competes for valuable space under the hood, making integration difficult without extensive redesigns of surrounding components or the vehicle's front structure. Material selection is critical here, requiring innovations in lightweight, durable, highly efficient acoustic, and thermal insulators that can withstand the harsh automotive climate.

Automotive Engine Encapsulation Market Trends

Increasing Focus on Sustainability to Positively Influence Market Growth in the Future

Vehicle manufacturers are increasingly committed to reducing their carbon footprint and adhering to sustainability targets. Engine encapsulation materials are evolving to incorporate recycled and bio-based materials that lessen the environmental impact. This trend toward using sustainable materials is becoming a focal point for manufacturers considering to improve their reputation and meet consumer demands for eco-friendly products.

Impact of COVID-19

The immediate impact of the COVID-19 pandemic on the automotive engine encapsulation market was significant disruptions in the supply chain. Lockdowns instituted by governments globally resulted in the temporary closure of manufacturing facilities and the halting of logistics operations. Suppliers faced challenges in obtaining raw materials, which delayed production timelines for encapsulation systems and complete vehicles.

For instance, suppliers of key materials such as plastics and composites faced shortages due to factory closures and logistical bottlenecks. As manufacturers struggled to meet production schedules, many automakers had to halt or reduce vehicle production, further cascading supply chain issues. Consequently, there was a marked decline in demand for engine encapsulation solutions, leading to reduced revenues for manufacturers in this segment.

Segmentation Analysis

By Type

Superior NVH Reduction Characteristics to Drive the Demand for Both Segment

Based on type, the market has been divided into engine mounted, body mounted, and both.

Both segments are expected to be the leading segment and capture a significant market share of 72.37% in 2026. The presence of engine-mounted and body-mounted encapsulation in a vehicle represents a sophisticated, multi-pronged strategy rather than a simple redundancy. By tackling noise at its source and blocking its path, this dual-layer system delivers the refined and quiet cabin experience, meeting the consumers’ expectation. Simultaneously, it optimizes the vehicle's thermal and aerodynamic efficiency, contributing to better fuel economy and lower emissions. This elegant engineering solution is a clear testament to the fact that in the quest for performance and refinement, the most effective defense is often layered.

The engine mounted segment is expected to grow at a considerable CAGR during the forecast period. Thermal management is yet another driving factor for implementing engine mounted encapsulation. Engines generate substantial heat during operation, which can negatively impact their efficiency and longevity, if not properly managed. Encapsulation can help regulate the thermal environment around the engine, maintaining optimal operating temperatures. The encapsulated design insulates the engine, reducing heat transfer to surrounding components and improving the performance of nearby systems such as electrical wiring and fluids. Moreover, maintaining lower engine temperatures can enhance fuel efficiency, as engines operate more effectively under optimal thermal conditions. This focus on energy efficiency aligns with increasing consumer awareness of environmental issues and the demand for fuel-efficient vehicles.

By Fuel

Technology Advancement and Stringent Regulatory Environment to Augment the Gasoline Segment’s Market Growth

Based on the fuel, the market is segmented into gasoline and diesel.

The gasoline segment is expected to capture a majority of the automotive engine encapsulation market share of 69.91% in 2026. With the increased focus on improving NVH levels in gasoline vehicles, manufacturers are investing in advanced materials and innovative design solutions for engine encapsulation. This includes lightweight materials, such as composites and engineered plastics, contributing to weight reduction and improved fuel efficiency. Stricter environmental regulations globally are pressuring manufacturers to reduce emissions and improve fuel efficiency. Engine encapsulation helps manufacturers meet these regulatory demands by enhancing thermal management, minimizing heat loss, improving engine performance, and reducing emissions.

The diesel segment is expected to grow steadily during the forecast period. Materials science and engineering innovations enable the development of lighter and more efficient encapsulation systems. These advancements help diesel vehicle manufacturers design components that perform better and add minimal weight to the vehicle, thus preserving fuel efficiency.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Increasing Need for Comfortable Environment to Drive the Demand for Luxury Vehicles

Based on the vehicle type, the market is divided into luxury and non-luxury.

The luxury segment is expected to account for the largest share of 50.17% in 2026. Luxury vehicle owners expect a quiet and comfortable driving experience. Engine noise, particularly from high-performance engines in performance-oriented models, can be intrusive and detract from the overall experience. Engine encapsulation mitigates this issue by reducing engine noise infiltration into the cabin. As more consumers prioritize comfort in their driving experience, manufacturers increasingly turn to encapsulation solutions to meet these expectations.

The non-luxury segment is expected to capture a considerable market share during the forecast period. The evolution of materials science and manufacturing processes has made engine encapsulation more accessible and cost-effective. Advancements have led to lighter, more efficient materials that offer excellent sound absorption and thermal insulation. This shift enables non-luxury vehicle manufacturers to adopt engine encapsulation without substantial increase in production costs. The weight reduction also contributes to improved fuel efficiency, further incentivizing the adoption of these technologies.

Automotive Engine Encapsulation Market Regional Outlook

North America

Asia Pacific Automotive Engine Encapsulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 0.1 billion in 2025, representing 8.98% of the global market landscape, and is expected to reach USD 0.11 billion in 2026. The increased demand for automotive engine encapsulation in North America reflects a broader trend of innovation and sustainability within the automotive industry. With pressures stemming from regulatory bodies, consumer expectations, and the rise of electric vehicles, encapsulation technology is becoming a key component of modern automotive design. As manufacturers continue to navigate the challenges and opportunities presented by this trend, the evolution of engine encapsulation will play a significant role in shaping the future of transportation. In this rapidly changing landscape, understanding and adapting to these demands will be essential for companies seeking to thrive in the competitive automotive marketplace. The U.S. market is expected to reach USD 0.09 billion by 2026.

The increasing demand for automotive engine encapsulation in the U.S. reflects a broader industry shift toward enhanced vehicle performance, compliance with environmental regulations, and improved user experience. As the automotive landscape evolves, encapsulation technology will undoubtedly play a crucial role in shaping the future of vehicle design, pushing the envelope for noise reduction, thermal efficiency, and overall quality. With a stronger commitment to sustainability and technological integration, the market is poised for continued growth and innovation in the years to come.

Europe

Europe contributed 43.14% to the global market in 2025, with a valuation of USD 0.5 billion, and is projected to reach USD 0.52 billion in 2026. As the automotive industry in Europe embraces the shift toward sustainability and efficiency, the demand for automotive engine encapsulation is poised to grow. This innovative solution enhances vehicle performance and consumer experience and aligns with regulatory expectations and consumer preferences for greener, quieter, and more efficient vehicles. Manufacturers and stakeholders who adapt and implement these technologies will comply with regulatory measures and set themselves apart in a competitive market. The U.K. market is expected to reach USD 0.04 billion by 2026, while the Germany market is expected to reach USD 0.20 billion by 2026.

Asia Pacific

Asia Pacific dominated the market with a valuation of USD 0.54 billion in 2025 and USD 0.57 billion in 2026. Asia Pacific captured the largest market share and is expected to grow at the highest CAGR over the forecast period. The region is a global hub for automotive manufacturing, accounting for a substantial share of the world's vehicle production. As manufacturers ramp up production to meet the demands of a growing middle class and rapid urbanization, implementing engine encapsulation can help improve the efficiency and competitiveness of new vehicles. Modern consumers increasingly prioritize comfort, performance, and sustainability when purchasing vehicles. With the rising awareness of environmental issues, consumers are looking for quieter, cleaner, and more efficient vehicles. Engine encapsulation addresses these expectations by providing a quieter engine operation and reducing the vehicle's carbon footprint. The Japan market is expected to reach USD 0.12 billion by 2026, the China market is expected to reach USD 0.35 billion by 2026, and the India market is expected to reach USD 0.02 billion by 2026.

Rest of the World

The rest of the world is expected to grow steadily during the forecast period. Latin America and the Middle East & Africa are experiencing robust growth in their automotive markets. With the increasing production and sale of vehicles, demand for enhanced performance and compliance with safety and environmental standards has driven manufacturers to invest in advanced engine encapsulation technologies. Countries including Brazil and Mexico are seeing a rising number of automotive suppliers and manufacturers, prompting a competitive landscape that encourages innovation.

Competitive Landscape

Key Market Players

Key Market Players Emphasis on Collaboration to Seek Edge in the Market

The market will grow substantially as the industry navigates through evolving consumer demands and regulatory landscapes. With a competitive landscape populated by multiple key players pushing for innovation, sustainability, and advanced designs, the future looks promising for engine encapsulation technologies. Emphasizing collaboration and R&D will be crucial for companies seeking an edge in this vibrant and rapidly changing market. As automakers continue to innovate and respond to environmental pressures, effective engine encapsulation solutions will undoubtedly become more critical in the quest for quieter, more efficient vehicles.

List of Key Automotive Engine Encapsulation Companies Profiled in The Report

- Autoneum (Switzerland)

- Rochling SE & Co. KG (Germany)

- Elringklinger AG (Germany)

- Woco Group (Germany)

- Auria Solutions (UK)

- Pimsa Automotive (Turkey)

- Pritex Limited (U.K)

- BASF SE (Germany)

- Adler Pelzer Group (Germany)

- Trocellen (Germany)

Key Industry Developments

- May 2025 – Autoneum acquired Chinese automotive supplier Chengdu FAW-Sihuan Automobile Interior Parts Co., Ltd.

- November 2024 – Autoneum expanded global research and development capacities with a new Research & Technology (R&T) Center in Shanghai, China.

- November 2024 – Autoneum signed an agreement to acquire 70 percent of the shares of Jiangsu Huanyu Group.

- August 2024 – Autoneum opened a new production facility in Pune to improve its strategic focus on future profitable growth with a particular emphasis on Asian growth markets.

- April 2022 – Auria Solutions and Feltex Automotive formed a joint venture to serve certain automotive OEMs (Original Equipment Manufacturers) in the region.

Investment Analysis and Opportunities

Technological Advancements and Material Innovation to Generate Opportunities for Market Growth

Innovations in materials science have led to the development of lightweight and efficient encapsulation materials. The introduction of advanced composites and polymers enhances the performance and durability of engine encapsulation systems, making them more appealing to manufacturers. Investing in companies focused on developing next-generation materials tailored for engine encapsulation can yield significant returns. Innovative materials that offer better insulation and noise dampening without adding substantial weight are in high demand.

Report Coverage

The global automotive engine encapsulation market report analyzes the market deeply and highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, and technology adoption. Besides this, the market research report provides insights into the automotive engine encapsulation market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.84% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Fuel

By Vehicle Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market size was USD 1.16 billion in 2025 and is anticipated to reach USD 1.77 billion by 2034.

The market will exhibit a CAGR of 4.84% over the forecast period (2026-2034).

By type, both segment will dominate the market during the forecast period.

Increasing focus on Noise, Vibration, And Harshness (NVH) reduction to augment the market growth.

Leading companies include Autoneum, Elringklinger AG, Rochling SE & Co. KG, Woco Group, Auria Solutions, and Pimsa Automotive.

Asia Pacific held the largest share in the global market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us