Automotive Forging Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium & Heavy Commercial Vehicles, Agriculture Machinery, Construction Equipment, and Others), By Material (Steel and Aluminum), By Application (Gears, Crankshaft, Pistons, Axle, Bearings, Connecting Rods, and Others) By Technology (Closed Die, Open Die, and Others) By Supplier Type (Local and International), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

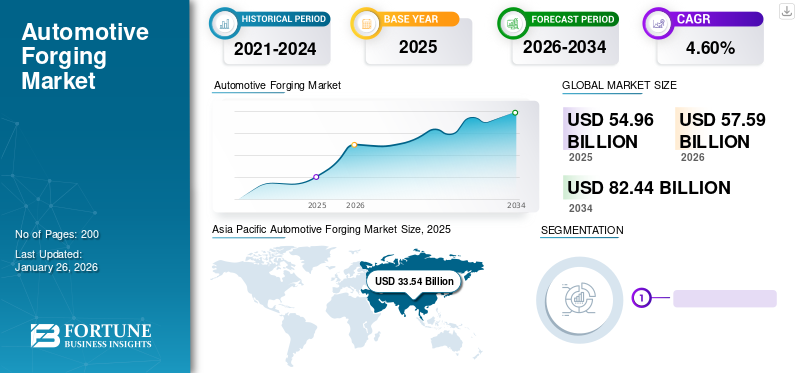

The global automotive forging market size was valued at USD 54.96 billion in 2025 and is projected to grow from USD 57.59 billion in 2026 to USD 82.44 billion by 2034, registering a CAGR of 4.60% over the forecast period. Asia Pacific dominated the automotive forging market with a market share of 61.02% in 2025.

Forging is a manufacturing process that utilizes compressive forces to shape metal. Automotive forging consists of engine parts, chassis, bearings, axles, and gears. Depending on the mechanical properties required, the process can be performed on the material. Metal forging produces some of the strongest manufactured parts with high mechanical properties compared to other manufacturing processes.

The demand for lightweight and fuel-efficient vehicles is expected to drive the automotive forging market growth. Forged components possess rigid and strong properties making them ideal for vehicle manufacturing. These properties are driving the global market.

The COVID-19 pandemic led to a decline in vehicle sales, causing a reduction in the demand for automotive components. For instance, the International Automobile Manufacturers Association (OICA) estimated that car sales in 2020 fell by 13.7% compared to 2019. In addition, the volatility in raw material prices during the pandemic due to supply chain disruptions and material unavailability also hit the global automotive forging industry. Rising raw material prices hampered market growth, especially in developing countries where inflation is very high. For instance, in India, in January 2021, hot-rolled steel coil prices in the wholesale market reached USD 710.32 per ton from USD 485.45 per ton in July 2020.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Automotive Forging Market Trends

Adoption of Smart Manufacturing Technology and Automation to Propel Market Growth

The acceptance of automation and intelligent manufacturing technologies is an ongoing trend in the market. Nearly all the leading players focus on automating their forging lineup to increase operational efficiency, overall productivity, and safety.

For instance, in September 2021, ThyssenKrupp AG started one of the most advanced forging lines in the world. The company established its advanced forging line in Homburg/Saarland. The company invested roughly USD 85 million in its new automotive forging facility for truck chassis components. The flagship of the new highly automated and digitized forging line in Homburg is a 16 thousand-ton forging press measuring nearly 15 meters in height and weighing 1,700 tons. The new line has the capacity to produce 360,000 forged components per year and will be able to make different large-scale products.

Furthermore, the increasing demand for lightweight or reduction in overall weight of a vehicle is also propelling the market growth. Therefore, the adoption of automation and smart manufacturing technologies to improve quality, precision, and productivity in the automotive forging line is anticipated to accelerate the market growth in the near term.

Automotive Forging Market Growth Factors

Rising Automotive Sales Drive Market Growth

As automotive sales rise, there’s a higher demand for forged components such as engine parts, transmission components, steering systems, and chassis parts, as they offer strength, durability, and precision, which are crucial for vehicle performance and safety. Forged components offer better efficiency and cost-effectiveness compared to components made through other manufacturing processes. They often require less machining, resulting in lower production costs and faster turnaround times, which is attractive to automakers looking to meet the growing demand for vehicles while maintaining profitability.

According to the Organisation Internationale des Constructeurs d'Automobiles, passenger car sales increased with a growth rate of around 2% in 2022, as compared to the previous year, 2021. The passenger car sales reached 57.5 million units in 2022, from 56.4 million units in 2021.

RESTRAINING FACTORS

Rising Electric Vehicle Penetration to Hinder Market Growth

Automotive manufacturing companies are one of the major buyers of forged metal products and components. Growing environmental concerns, rising government initiatives to promote green mobility, increasingly stringent emissions regulations, and escalating fuel prices drive electrification in the automotive industry. Almost all major automakers focus on developing electric vehicles as economical solutions for future mobility.

However, electric vehicles have lesser mobile and forged parts than conventional vehicles. Therefore, the increasing popularity and acceptance of electric vehicles and increasing electrification in the global automotive industry will likely hinder the market growth during the forecast period. For instance, according to the International Energy Agency, in 2022, around 10.2 million passenger cars were sold, whereas in 2021, around 6.5 million passenger cars were sold. This rise in the demand for electric vehicles drives the market growth over the forecast period. Additionally, various government initiatives offering tax breaks and subsidies for purchasing new electric vehicles are expected to boost EV adoption in emerging markets. EVs are expected to penetrate deeply across vehicle sales worldwide during the forecast period, further slowing the demand for automotive forging products.

Automotive Forging Market Segmentation Analysis

By Vehicle Type Analysis

Increasing Number of Forging Parts in Passenger Cars to Propel the Segment Growth

By vehicle type, the market is categorized as passenger cars, light commercial vehicles, medium & heavy commercial vehicles, agricultural machinery, construction equipment, and others.

The passenger cars segment is projected to reach 74.38% of the global market share in 2026 and is anticipated to continue its dominance throughout the forecast period. For instance, according to the Organisation Internationale des Constructeurs d'Automobiles, passenger cars production was increased by a growth rate of 7.9% in 2022, as compared to the previous year 2021. The production of passenger cars reached to 61.6 Million units in 2022, from 57 million units in 2021. The design of mechanical components in electric cars will be much simpler as designers can create significant impacts with simple geometries. Forged aluminum parts perform better than machined or cast parts, increasing reliability. These factors can positively impact the growth of the market.

The construction equipment segment is expected to grow at a significant CAGR from 2023 to 2030. Ferrous forgings are used heavily in heavy construction & off-highway equipment owing to the need for strength, machinability, and toughness. In addition to transmission and engine parts, forgings are utilized for axle beams, gears, wheel hubs, bearing holders, shafts, levers, links, yokes, rollers, and spindles. Therefore, the increasing demand for these automotive forged parts is anticipated to drive the segment growth.

Other segments such as light commercial vehicles and agricultural equipment also saw a positive growth rate during the forecast period. Medium & heavy commercial vehicles production volumes showed positive recovery in 2021. For instance, in key markets such as India, Brazil, the U.S., and Mexico, sales volumes increased by 75%, 101%, 20%, and 22%, respectively.

By Material Analysis

Steel Segment to Dominate Owing to High Production Efficiency and Impact Strength

By material, the market is categorized into aluminum and steel. The steel material segment is projected to reach a 64.66% share in 2026. Due to the high forge ability of carbon steel, in particular, along with its impact strength, production efficiency, and economic utilization, the demand for carbon steel is high in the automotive industry, possibly fueling the market growth during the forecast period. Vehicle weight reduction is one of the many factors that affect fuel economy and performance.

Aluminum in automotive forging is the fastest-growing segment throughout the forecast period as the aluminum usage in the automotive industry increased from 154 kg per vehicle in 2010 to 208 kg per vehicle in 2022, according to a study published in Current Trends in Automotive Lightweighting Strategies and Materials. For internal combustion engine (ICE) vehicles, with 10% less weight, fuel economy will improve by 6-8%. A lower-weight alternative to steel is aluminum, which is highly recovered and reused. The increasing demand for lightweight material is supporting aluminum in the automotive forging industry.

By Application Analysis

Axle Segment to Dominate Owing to its Vitality in Vehicle Drive Train

By application, the market is categorized into crankshaft, gears, piston, axle, bearings, connecting rods, and others.

An axle is a shaft that connects a pair of wheels in the automotive to propel wheels and retain their position to one another. The axle segment is projected to reach 33.19% of the global market share in 2026. The segment comprises applications for other automotive forged components such as input/output shafts, chassis, high-pressure valves, and others.

The growing use of special purpose vehicles and mining and defense purpose vehicles has resulted in the fast growth rate of the others segment over the forecast period. Forged engine and powertrain components include connecting rods, differential gears, clutch hubs, transmission shafts, crankshafts, drive shafts, and universal joint yokes. Forged gears, pinions, camshafts, and rocker's arms offer strength and ease of selective hardening. Axle beams and shafts, idler arms, linkages, steering arms, wheel spindles, and torsion bars for passenger cars, trucks, and buses characterize applications that require substantial toughness and strength. Hence, forging is a suitable manufacturing process for automotive components.

To know how our report can help streamline your business, Speak to Analyst

By Technology Analysis

Closed Die Segment to Dominate Owing to its Surface Finish and Superior Mechanical Properties

By technology, the market is divided into open die, closed die, and others. Closed die segment dominated the market with the highest market share 74.04% in 2026. It helps produce components with complex profiles. This type also offers an excellent surface finish and excellent mechanical properties. This factor further reduces processing requirements.

The open die segment is estimated to grow at a significant growth rate from 2023 to 2030. Its growth is driven by the increasing demand for simple geometry forged products such as shafts, axle beams, forks, and ball joints. In addition, part weight savings are achieved due to their inherent high strength-to-weight ratio. Therefore, more than 200 die forgings are used in vehicles and die forging machines are installed in almost all types of forging units to produce high-quality development products efficiently.

By Supplier Type Analysis

Local Segment is Dominant Due to Low Production Costs and Incentives for Manufacturers

By supplier type, the market is segmented into local and international (import). The local segment held the highest market share 2023. The major driving factor for its growth is the import of auto ancillaries and electric vehicle components from China and other Asian countries to Europe and North America.

The international segment is expected to showcase a positive growth rate in the forecast period. This growth is due to low production costs, economies of scale, government initiatives to tackle trade barriers, and manufacturing incentive schemes.

REGIONAL INSIGHTS

Increasing Budget and Spending on Military Requirements to Propel Market Growth in Asia Pacific

Regionally, the market is classified into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific Automotive Forging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 33.54 billion in 2025, accounting for 61.02% share, and is expected to reach USD 35.32 billion in 2026. The Asia Pacific market is expected to be the dominant and fastest-growing compared to other regions. China and India account for a huge share of forged components produced. The new investments by major regional players are focused on automation and high-level machinery with low energy consumption and higher efficiency. The presence of key players in these regions is projected to boost the growth of the forging market in the country. The companies such as Bharat Forge Limited, Ramkrishna Forgings LTD, and many other players are developing various opportunities in the country. The Japan market is projected to reach USD 3.82 billion by 2026, the China market is projected to reach USD 23.04 billion by 2026, and the India market is projected to reach USD 3.60 billion by 2026.

North America

North America contributed approximately USD 5.93 billion to the global market in 2025, accounting for 28.32% share, and is expected to reach USD 6.23 billion in 2026.

Europe

The Europe region captured 19.90% of the global market in 2025, generating USD 10.94 billion in revenue, and is projected to reach USD 11.36 billion in 2026. Europe is expected to grow significantly due to alternative production techniques in the forging industry. Government regulations support locally manufactured products, propelling the expansion of the Europe market. North America is expected to increase steadily in the global market owing to the increasing demand for forged automobile parts.

Light Commercial Vehicle (LCV) and heavy truck production both positively recovered. These segments also have a higher need for replacement. These factors positively impact the demand for forged parts in North America.

Brazil and Turkey are introducing auto sector policies that provide additional tax benefits to manufacturers who invest in technological developments. Such regulations have encouraged many automakers to adopt advanced manufacturing processes. These factors will positively impact the market growth in the rest of the world. The UK market is projected to reach USD 1.01 billion by 2026 and the Germany market is projected to reach USD 4.41 billion by 2026.

Rest of the World

The Rest of the World market generated USD 4.11 billion in 2025, representing 7.49% of the global market landscape, and is expected to reach USD 4.32 billion in 2026.

List of Key Companies in Automotive Forging Market

Early Adoption of Smart Manufacturing Technology to Drive the Competition Among Market Players

ThyssenKrupp Group is an international group of companies comprising largely independent industrial technology businesses. The company has presence across 56 countries. Six segments handle its business activities - industrial components, material services, steel Europe, multi-tracks, marine systems, and automotive technology. Adopting automation and smart/intelligent manufacturing technologies is an ongoing trend in the market. The company’s nearly 3,600 employees work in the R&D department across 78 locations worldwide.

R&D is mainly a company's team that works primarily in the industry's energy transition, climate protection, future mobility, and digital transition. ThyssenKrupp Group has a portfolio of nearly 18,100 patents and utility models. Most leading players focus on turning their forging lineup automated to increase operational efficiency, overall productivity, and safety.

LIST OF KEY COMPANIES PROFILED:

- ThyssenKrupp AG (Germany)

- CIE Automotive (Spain)

- NTN Corporation (Japan)

- American Axle and Manufacturing Inc. (U.S.)

- Bharat Forge Limited (India)

- Ramkrishna Forgings (India)

- Dana Limited (U.S.)

- Meritor Inc. (U.S.)

- ZF Friedrichshafen AG (Germany)

KEY INDUSTRY DEVELOPMENTS:

- November 2023 - Forge Nano, Inc. unveiled the establishment of a lithium-ion battery business and developed a product called Forged Battery. The company would produce batteries for defence, aerospace and specialty electric vehicle markets at the gigafactory in Raleigh, North Carolina.

- July 2023 - Talbros Automotive Components was awarded a multi-year business contract worth INR 400 Crore (USD 48.4 million). Under the contract term for 5-7 years, Talbros would provide gasket, heat shield, forging, and chassis product lines.

- March 2023 - Ramkrishna Forgings incorporated its subsidiary RKFL Engineering Industry Private Limited. The company is in business for forging, pressing, rolling of metal sheets, and stamping processes. The subsidiary has been incorporated to implement a resolution plan under the Corporate Insolvency Resolution Process (CIRP) for JMT Auto, a unit of Amtek Auto group.

- February 2023 - Jiangsu Pacific Precision Forging invested around USD 64.9 million to build a new energy vehicle parts plant in Thailand. The new plant will be located at Pinthong Industrial Park in Rayong province and will be fully operational in five years. The Taizhou-based company said it would be involved in vehicle gears, forging parts, and assembly products without specifying product capacities.

- July 2022 - Siderforgerossi Group S.p.A. acquired Grupo Euskal Forging, S.L. and its subsidiaries. This acquisition will make the company reach a leading position in the forgings market across offshore and onshore applications.

- May 2022 - Ramkrishna Forgings Limited received a multi-year contract valued at USD 13.5 million annually for major chassis-related systems and components primarily for trailers, trucks, and buses in the U.S.

- March 2022 - American Axle & Manufacturing announced that it secured multiple next-generation full-sized truck rear and front axle programs with global OEM customers. The contracts and a previously announced award in early 2021 are anticipated to generate more than USD 10 billion of lifetime revenue from mid-decade to beyond 2030.

REPORT COVERAGE

The global automotive forging market research report provides detailed market analysis and focuses on key aspects such as leading companies, product types, end-users, design, and technology. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market growth in recent years.

An Infographic Representation of Automotive Forging Market

View Full Infographic

View Full InfographicTo get information on various segments, share your queries with us

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.60% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

By Material

By Application

By Technology

By Supplier Type

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 54.96 billion in 2025 and is projected to grow from USD 57.59 billion in 2026 to USD 82.44 billion by 2034.

The market is expected to register a CAGR of 4.60% during the forecast period (2026-2034).

The increasing demand for lightweight fuel-efficient vehicles is expected to propel the market growth.

The Asia Pacific region led the global market in 2023.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us