Automotive LED Lights Market Size, Share & Industry Analysis, By Technology Type (Basic LED, Adaptive LED, and OLED), By Product Type (Headlamps, Tail Lights, Daytime Running Lights (DRLs), Fog Lights, Interior Lighting, Turn Signal Indicators, and Others), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Wattage/Power Consumption (Low Power (<10W), Medium Power (10W–25W), and High Power (>25W)), and Regional Forecast, 2026–2034

automotive LED lights mark Overview

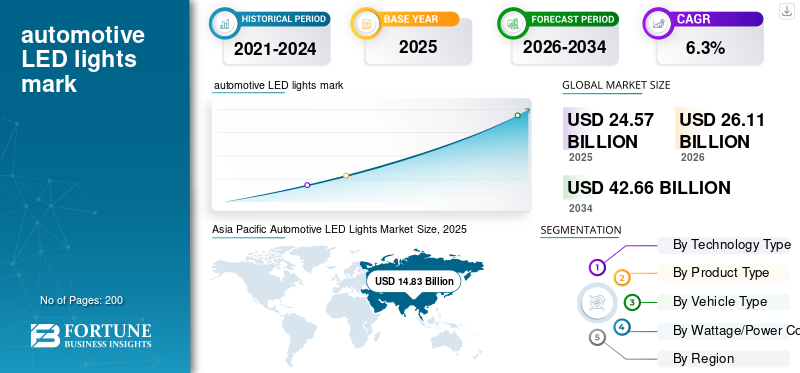

The global automotive LED lights market size was valued at USD 24.57 billion in 2025. The market is projected to grow from USD 26.11 billion in 2026 to USD 42.66 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. Asia Pacific dominated the automotive LED lights market with a market share of 60.35% in 2025.

Automotive LED lights are vehicle lighting systems that use Light-Emitting Diode (LED) technology for headlamps, taillights, DRLs, fog lights, indicators, and interior illumination. They offer higher energy efficiency, longer life, faster response time, better brightness control, and greater design flexibility than halogen and HID lighting systems. The global market is driven by rising vehicle production, stricter road safety standards, growing adoption of EVs, increasing SUV and premium vehicle sales, and demand for energy-efficient lighting. Automakers are also integrating adaptive LED, matrix lighting, DRLs, and ambient cabin lighting to improve visibility, styling, safety, and vehicle differentiation.

Major players include Koito, Stanley Electric, Valeo, FORVIA HELLA, Marelli, OSRAM, Lumileds, ZKW, Hyundai Mobis, and SL Corporation. These companies are focusing on adaptive LED, matrix headlamps, OLED rear lamps, energy-efficient modules, lightweight designs, and OEM partnerships to strengthen competitiveness in advanced automotive lighting.

Download Free sample to learn more about this report.

Automotive LED Lights Market KEY TAKEAWAYS

- 2025 Market Size: USD 24.57 billion

- 2026 Market Size: USD 26.11 billion

- 2034 Forecast Market Size: USD 42.66 billion

- CAGR: 6.3% from 2026–2034

- Asia Pacific dominated the automotive LED lights market with a 60.35% share in 2025.

- Basic LED segment dominated the market due to its widespread use in mass-market vehicles.

- Headlamps segment held the largest market share owing to their high value and essential safety function.

Asia Pacific

Asia Pacific is the largest and fastest-growing region, driven by strong vehicle production and EV adoption.

North America

North America is witnessing steady growth, supported by increasing demand for premium lighting systems.

Europe

Europe is expanding through strong adoption of adaptive LED and OLED technologies backed by strict safety regulations.

U.S.

U.S. The market reached USD 3.13 billion in 2026, supported by high demand for advanced automotive lighting.

Japan

Japan The market is projected to reach USD 2.14 billion in 2026, driven by its advanced automotive manufacturing industry.

Read More

AUTOMOTIVE LED LIGHTS MARKET TRENDS

Rising Adoption of Adaptive and Smart Lighting Technologies Enhances Market Evolution

Automotive LED lighting is evolving beyond basic illumination toward intelligent systems such as matrix LED and pixel lighting. These technologies dynamically adjust beam patterns, improving visibility and safety while enabling distinctive vehicle styling. Integration with ADAS, sensors, and cameras is transforming lighting into an active safety component. Premium vehicles lead adoption, but costs are gradually declining, enabling penetration into mid-range vehicles. Interior ambient lighting is also becoming customizable and software-driven, aligning with software-defined vehicle trends. Automakers increasingly use lighting as a branding and differentiation tool, accelerating innovation across exterior and interior applications.

- In March 2023, Mercedes-Benz expanded its DIGITAL LIGHT system with projection technology across new models, enhancing adaptive beam precision and driver-assistance integration.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Vehicle Production and Electrification Accelerate LED Lighting Demand

Rising global vehicle production and strong growth in electric vehicles are major drivers of demand for automotive LED lights. LEDs are preferred in EVs due to their low energy consumption, which helps improve battery efficiency and vehicle range. Increasing SUV and premium vehicle sales further boost LED content per vehicle. Governments are also encouraging energy-efficient technologies, indirectly supporting LED adoption. Automakers are standardizing LED lighting across headlamps, DRLs, and tail lamps, even in mid-range vehicles. The combination of electrification, safety regulations, and design differentiation continues to accelerate LED penetration globally.

- In January 2024, Tesla continued integrating full LED lighting systems, including advanced headlamps and ambient lighting, across its Model 3 refresh to improve efficiency and design.

MARKET RESTRAINTS

High Initial Cost and Integration Complexity Limit Wider Adoption

The relatively high initial cost of LED lighting systems compared to halogen alternatives remains a key restraint, particularly in cost-sensitive markets. Advanced systems such as adaptive LED and OLED lighting involve complex electronics, sensors, and control units, increasing overall system cost. Integration challenges, including thermal management and compatibility with vehicle platforms, add to manufacturing complexity. As a result, entry-level vehicles often limit LED use to DRLs or tail lamps rather than full LED headlamp systems. This slows down widespread adoption in developing regions and commercial vehicle segments where affordability is critical.

- In June 2023, Ford highlighted cost and supply challenges in advanced lighting systems while balancing feature integration in mass-market vehicles such as the Ford Escape.

MARKET OPPORTUNITIES

Expansion of Premium and Electric Vehicle Segments Creates Growth Potential

The rapid expansion of premium vehicles and EVs creates significant opportunities for advanced automotive LED lights market growth. These segments demand high-performance lighting systems, including adaptive headlamps, signature DRLs, and ambient interior lighting. EV manufacturers prioritize futuristic design and energy efficiency, making LED lighting essential. Rising disposable incomes in emerging markets are also increasing demand for feature-rich vehicles. Additionally, OLED and smart lighting innovations provide new opportunities for differentiation and higher margins. As automakers focus on user experience and brand identity, lighting systems are becoming a key value-added component in modern vehicles.

- In September 2023, BMW introduced advanced LED and illuminated grille lighting in its i5 electric sedan, emphasizing design and premium appeal.

MARKET CHALLENGES

Rapid Technological Evolution and Standardization Challenges Impact Market Stability

The automotive LED lighting market faces challenges due to rapid technological advancements and inconsistent global standards. Continuous innovation in features such as adaptive lighting, OLEDs, and smart lighting requires frequent design and manufacturing upgrades, increasing R&D costs. Additionally, regional regulations on beam patterns, brightness, and safety compliance add complexity for global OEMs. Ensuring compatibility with evolving vehicle architectures, especially EVs and software-defined vehicles, further complicates development. These factors create operational challenges and cost pressures, particularly for smaller suppliers trying to keep pace with innovation and compliance requirements.

- In February 2022, the U.S. National Highway Traffic Safety Administration (NHTSA) updated regulations to allow Adaptive Driving Beam (ADB) headlights, highlighting the challenges of global regulatory evolution.

Segmentation Analysis

By Technology Type

Cost-Effective Standardization Across Mass-Market Vehicles Supports Basic LED Segment Dominance

Based on technology type, the market is segmented into basic LED, adaptive LED, and OLED.

Basic LED dominates as it is widely used in mass-market headlamps, tail lights, DRLs, indicators, and cabin lights owing to its lower cost, durability, and energy efficiency. It is especially strong in hatchbacks, sedans, LCVs, and mid-range SUVs. However, premium styling and advanced rear-light designs are pushing OLED faster from a small base.

The OLED segment is projected to grow at a 10.5% CAGR over the forecast period.

- In October 2024, OLEDWorks announced that the upgraded Audi Q7 SUV used its digital OLED rear-light panels.

By Product Type

High-Value Front Illumination Requirements Augment Headlamps Segment Demand

Based on product type, the market is segmented into headlamps, tail lights, Daytime Running Lights (DRLs), fog lights, interior lighting, turn signal indicators, and others.

Headlamps segment dominates the automotive LED lights market share as they carry the highest value per vehicle and are essential for night visibility, safety compliance, and premium vehicle styling. LED headlamps are increasingly standard across SUVs and passenger vehicles, while adaptive versions further enhance value.

- In February 2022, NHTSA allowed adaptive driving beam headlights on new vehicles in the U.S.

The interior lighting segment is projected to grow at a 7.5% CAGR over the forecast period.

By Vehicle Type

Rising Production and Premium Feature Adoption Fuel SUV Segment Growth

Based on vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs, and HCVs.

SUVs dominate as they usually carry higher-value LED packages, including projector headlamps, DRLs, fog lamps, tail-light signatures, and ambient lighting. Their higher average selling price allows OEMs to install more advanced lighting features than in entry-level hatchbacks and sedans. The SUV segment is projected to grow at a CAGR of 8.4% over the forecast period.

- In 2024, Toyota stated that the RAV4 used standard LED projector-beam headlights and integrated fog lights.

The HCV is the second-fastest-growing segment at a rate of 6.6% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Wattage/Power Consumption

Balanced Brightness and Cost Efficiency Strengthens Medium Power LED Adoption

Based on wattage/power consumption, the market is segmented into low power, medium power, and high power.

Medium power LEDs dominate as they suit many mainstream applications such as DRLs, fog lights, indicators, and selected exterior lighting systems, offering a balance between brightness, heat control, and cost. They are widely used across passenger and commercial vehicles. High Power LEDs are expanding faster as adaptive headlamps and premium front-lighting systems require stronger illumination.

The high power segment is projected to grow at an 8.6% CAGR over the forecast period.

- In December 2024, the Federal Register confirmed rules enabling ADB headlighting certification.

AUTOMOTIVE LED LIGHTS MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Automotive LED Lights Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the fastest-growing and largest region, driven by massive vehicle production in China, India, Japan, and South Korea. China alone contributes significantly, given its dominant automotive manufacturing base and rapid adoption of LED lighting across both mass-market and premium vehicles. Increasing disposable income, urbanization, and rising SUV demand further accelerate growth. The region also benefits from expanding EV production and the strong presence of automotive OEMs and component manufacturers, making it the key growth engine of the global market.

China Automotive LED Lights Market

China dominates the Asia Pacific market with a 60.3% share, supported by its massive vehicle production and rapid LED adoption across both mass-market and premium vehicles. Strong EV growth, government support, and increasing demand for advanced lighting technologies further reinforce its leading position in the global market.

Japan Automotive LED Lights Market

Japan’s market size is expected to reach USD 2.14 billion in 2026, driven by a strong OEM presence and the adoption of advanced technologies. The country’s focus on innovation, including adaptive LED and high-efficiency lighting systems, along with premium vehicle manufacturing, drives consistent demand for automotive LED solutions.

India Automotive LED Lights Market

India is the fastest-growing market with a CAGR of 8.6%, driven by rising vehicle production, increasing SUV demand, and growing adoption of LED lighting in mid-range vehicles. The government's focus on energy efficiency and the expansion of the EV ecosystem is further accelerating LED penetration across passenger and commercial vehicle segments.

North America

North America demonstrates steady progress in the market growth, driven by strong SUV and pickup truck demand, which typically incorporates high-value lighting systems such as adaptive headlamps and premium interior lighting. The U.S. dominates the region, supported by high consumer preference for advanced safety features and premium vehicle trims. Mexico contributes significantly through vehicle manufacturing and exports. Increasing adoption of EVs and regulatory support for advanced lighting technologies further boost demand. However, growth is moderate compared to the Asia Pacific due to relatively stable vehicle production volumes.

U.S. Automotive LED Lights Market

The U.S. dominates the North American market, accounting for USD 3.13 billion in 2026, driven by strong SUV and pickup demand and high adoption of advanced lighting technologies. Premium vehicle penetration, EV expansion, and regulatory support for adaptive lighting systems continue to enhance LED integration across headlamps, DRLs, and interior lighting applications.

Europe

Europe shows stable yet value-driven growth, supported by strong adoption of advanced lighting technologies such as adaptive LED and OLED systems. Countries such as Germany, France, and the U.K. lead due to premium vehicle manufacturing and strict safety regulations. European automakers emphasize innovation, design differentiation, and energy efficiency, increasing LED penetration across vehicle segments. Although overall vehicle production growth is moderate, higher vehicle content drives market value. Regulatory support for advanced headlamp technologies and increasing EV adoption further sustain growth in the region.

U.K. Automotive LED Lights Market

The U.K. market value is projected to reach USD 0.61 billion in 2026, supported by rising EV adoption and increasing demand for premium lighting features. The strong presence of advanced automotive technologies and the growing consumer preference for safety and design differentiation are accelerating LED adoption across passenger vehicles and SUVs in the country.

Germany Automotive LED Lights Market

Germany holds a significant 28.2% share in the European market, driven by its strong automotive manufacturing base and leadership in premium vehicle production. High integration of adaptive LED and OLED lighting systems, along with stringent safety regulations, continues to strengthen demand across luxury and high-performance vehicles.

South America

South America experiences moderate growth, led primarily by Brazil and Argentina. The market is driven by a gradual recovery in automotive production and by the increasing adoption of LED lighting in passenger vehicles and SUVs. Cost sensitivity limits the adoption of advanced lighting technologies, with basic LED systems dominating the region. However, improving economic conditions and rising demand for modern vehicle features are supporting gradual market expansion. OEM production and regional manufacturing hubs play a crucial role in sustaining growth.

Brazil Automotive LED Lights Market

Brazil dominates the South American market with a 64.8% share, driven by its large automotive production base and growing SUV demand. The increasing adoption of LED lighting in passenger vehicles and improving economic conditions are supporting market growth, though cost sensitivity continues to favor basic LED systems.

Middle East & Africa

The Middle East & Africa region is experiencing emerging growth, supported by rising vehicle demand, particularly in Gulf countries and South Africa. Rising SUV sales, premium vehicle imports, and gradual adoption of LED lighting technologies drive the market. Infrastructure development and fleet modernization also drive demand for commercial vehicles. However, limited local vehicle production and economic variability constrain rapid expansion. Despite this, the region is expected to grow steadily as consumer demand for advanced vehicle features and improved safety standards increases.

UAE Automotive LED Lights Market

The UAE market is projected to grow at a CAGR of 8.7% during the forecast period, driven by high demand for premium and luxury vehicles. Strong SUV sales, increasing adoption of advanced lighting technologies, and rising consumer preference for aesthetics and safety features are accelerating LED integration across vehicle segments in the country.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation, OEM Partnerships, and Advanced Lighting Systems Define Competitive Landscape

The market trends are moderately consolidated, with a mix of global Tier-1 suppliers and regional manufacturers competing on technology, cost, and OEM partnerships. Key players such as Koito Manufacturing, Valeo, FORVIA HELLA, Stanley Electric, Marelli, OSRAM, Lumileds, ZKW Group, Hyundai Mobis, and SL Corporation compete through advanced lighting technologies, including adaptive LED, matrix headlamps, and OLED rear lighting. To gain a competitive edge, companies are focusing on software-integrated lighting, energy-efficient modules, and design-centric solutions that enhance vehicle aesthetics and safety. Strategic collaborations with automakers, expansion of production facilities, and localization strategies are widely adopted to strengthen global presence. Continuous investment in R&D and innovation in smart lighting systems remains a key differentiator.

- In July 2023, Valeo launched its third-generation Smart Safety 360 lighting systems, integrating advanced LED technology with ADAS to enhance vehicle safety and visibility.

LIST OF KEY AUTOMOTIVE LED LIGHTS COMPANIES PROFILED

- Koito Manufacturing Co., Ltd. (Japan)

- Stanley Electric Co., Ltd. (Japan)

- Marelli Holdings Co., Ltd. (Japan)

- Valeo S.A. (France)

- Hella GmbH & Co. KGaA (Germany)

- OSRAM GmbH (Germany)

- Signify N.V. (Netherlands)

- Lumileds Holding B.V. (Netherlands)

- Samsung Electronics Co., Ltd. (South Korea)

- LG Innotek Co., Ltd. (South Korea)

- Hyundai Mobis Co., Ltd. (South Korea)

- Ichikoh Industries, Ltd. (Japan)

- Varroc Engineering Limited (India)

- ZKW Group GmbH (Austria)

- SL Corporation (South Korea)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Marelli showcased next-generation automotive lighting technologies at Auto China 2026, with a focus on software-defined vehicle integration. The company highlighted advanced digital lighting systems, including smart RGB LED solutions and adaptive lighting platforms that enhance personalization, safety, and communication between vehicles and surroundings.

- March 2026: Marelli announced the expansion of its India footprint with a new manufacturing plant in Sanand, Gujarat. The facility will support the production of advanced automotive lighting systems and electronic components, strengthening local supply capabilities, improving cost efficiency, and catering to growing demand from OEMs in India’s expanding automotive and EV market.

- January 2026: Toyoda Gosei unveiled its innovative moving light technology, designed to project light patterns onto roads to communicate vehicle intentions to pedestrians and surrounding traffic. This advanced LED-based system enhances safety and interaction, especially for autonomous and electric vehicles, by improving visibility and signaling capabilities.

- January 2026: ZKW equipped the new Audi Q3 with digital Matrix LED headlights developed in collaboration with Audi, featuring high-resolution micro-LED technology. Each spotlight contains 25,600 individually controllable pixels, enabling precise light control, improved glare-free high beam, and projection functions for compact SUV applications.

- January 2026: Neolite ZKW inaugurated a new automotive lighting manufacturing facility in Pune, India, to supply OEM lighting solutions for passenger vehicles, commercial vehicles, two-wheelers, three-wheelers, EVs, and ICE vehicles, including advanced LED modules, dynamic DRLs, adaptive front lighting systems, and signature aesthetic lamps.

REPORT COVERAGE

The global automotive LED lights market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on rapid technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market shares, emerging opportunities, and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.3% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology Type, By Product Type, By Vehicle Type, By Wattage/Power Consumption, and By Region |

| By Technology Type |

|

| By Product Type |

|

| By Vehicle Type |

|

| By Wattage/Power Consumption |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 24.57 billion in 2025 and is projected to reach USD 42.66 billion by 2034.

In 2025, the market value stood at USD 14.83 billion.

The market demand is expected to grow at a CAGR of 6.3% from 2026 to 2034.

The basic LED segment led the market share by technology type.

Rising vehicle production, stricter road-safety standards, growing adoption of EVs, increasing SUV and premium vehicle sales, and demand for energy-efficient lighting are driving market momentum.

Key market players include Koito, Stanley Electric, Valeo, FORVIA HELLA, Marelli, OSRAM, Lumileds, and ZKW.

The Asia Pacific region accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, South America, and the Middle East & Africa regions are considered in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us