Automotive Over-The-Air Updates Market Size, Share & Industry Analysis, By Technology Type (Firmware OTA, Software OTA, & Full-System OTA), By Vehicle Architecture Layer (ECU-Level OTA, Domain Controller OTA, & Centralized/Zonal Architecture OTA), By Vehicle System (Powertrain & Energy Systems, ADAS & Autonomous Driving, Infotainment & Connectivity, Safety & Security Systems, & Telematics & Connectivity Modules), By Vehicle Type (Hatchback & Sedan, SUV, LCV, and HCV), By Connectivity Technology (Cellular, Wi-Fi OTA, Satellite OTA, & V2X/Edge-assisted OTA), and Regional Forecast, 2026–2034

Automotive Over-The-Air Updates Market Size and Future Outlook

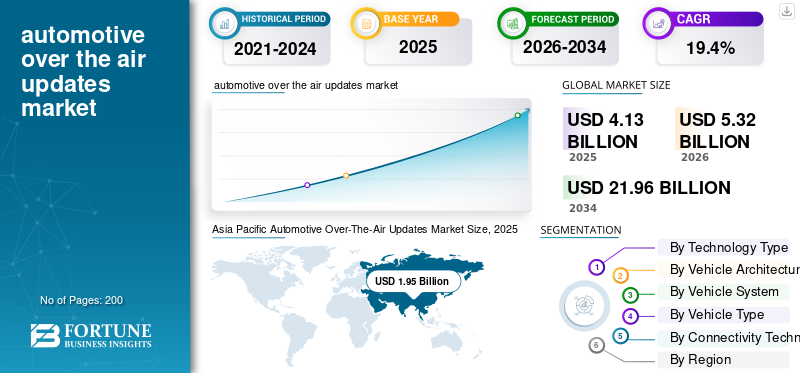

The global automotive over-the-air updates market size was valued at USD 4.13 billion in 2025. The market is projected to grow from USD 5.32 billion in 2026 to USD 21.96 billion by 2034, exhibiting a CAGR of 19.4% during the forecast period. Asia Pacific dominated the automotive over-the-air updates market with a market share of 47.21% in 2025.

The global automotive Over-The-Air (OTA) updates market refers to the ecosystem of technologies, platforms, and services enabling wireless software updates and upgrades in vehicles. It allows automakers to remotely deploy firmware over the air, applications, and system enhancements without physical intervention. This market covers passenger and commercial vehicles, supporting functions like infotainment, telematics, safety systems, and powertrain optimization, improving vehicle performance, security, compliance, and user experience throughout the vehicle lifecycle.

Key drivers of the market include increasing vehicle connectivity, rising demand for enhanced user experience, and the need for real time data software upgrades. Growing adoption of electric and autonomous vehicles, cybersecurity requirements, and cost reduction through remote diagnostics and maintenance further accelerate market growth, enabling continuous performance improvements and feature enhancements.

Major players in the market include Robert Bosch GmbH, Continental AG, Harman International, Aptiv PLC, Denso Corporation, and Qualcomm Technologies, Inc. Such players are competing through advanced software over the air platforms, secure connectivity solutions, cloud integration, and cybersecurity capabilities. Further, enabling seamless remote updates, enhanced vehicle performance, and continuous feature innovation across connected and software-defined vehicles.

Download Free sample to learn more about this report.

Automotive Over the Air Updates Market Key Takeaways

- 2025 Market Size: USD 4.13 billion

- 2026 Market Size: USD 5.32 billion

- 2034 Forecast Market Size: USD 21.96 billion

- CAGR: 19.4% from 2026–2034

- Asia Pacific dominated the automotive over-the-air updates market with a 47.21% share in 2025.

- The Domain Controller OTA segment accounted for the largest market share.

- The Centralized/Zonal Architecture OTA segment is projected to grow at a 19.2% CAGR during 2026–2034.

Asia Pacific

Connected vehicles, EV adoption, and 5G rollout continue to accelerate OTA deployment.

North America

Connected vehicle penetration and cloud platforms strengthen OTA implementation.

Europe

Cybersecurity regulations and software-defined vehicle adoption support strong market growth.

U.S.

U.S. Market Expected to reach USD 0.91 billion in 2026, accounting for 17.2% of global revenue.

Japan

Japan's Market is projected to reach USD 0.32 billion in 2026.

Read More

AUTOMOTIVE OVER-THE-AIR UPDATES MARKET TRENDS

Shift Toward Cloud-Based OTA Platforms and Edge Computing is a Prominent Trend

A prominent trend in the market is the increasing adoption of cloud-based platforms combined with edge computing capabilities. Automakers are leveraging cloud infrastructure to manage large-scale software deployments, monitor vehicle performance, and analyze real-time data. Edge computing further enhances this ecosystem by enabling localized data processing within the vehicle, reducing latency and improving update efficiency. This hybrid approach allows faster, more reliable OTA rollouts while minimizing network dependency. Additionally, it supports personalized updates and predictive maintenance by utilizing real-time analytics. As connected vehicle ecosystems expand, the integration of cloud and edge technologies is becoming a strategic priority, enabling scalable, secure, and efficient OTA update frameworks across diverse vehicle segments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Software-Defined Vehicles to Accelerate OTA Adoption

The transition toward Software-Defined Vehicles (SDVs) is a major driver of the automotive over-the-air updates market growth. Automakers are increasingly integrating advanced electronics, sensors, and centralized computing architectures that rely heavily on software for functionality and differentiation. OTA capabilities enable manufacturers to deploy feature upgrades, fix bugs, and enhance system performance remotely, reducing dependency on physical service visits. This approach not only lowers operational costs but also improves customer satisfaction through continuous innovation. As vehicles become more complex and software-driven, OEMs witness OTA updates as a critical enabler for lifecycle management, ensuring vehicles remain up-to-date with evolving standards, regulations, and consumer expectations.

MARKET RESTRAINTS

Data Privacy and Security Concerns to Limit Market Expansion

Concerns related to data privacy and cybersecurity present a significant restraint in the automotive OTA updates market. As OTA systems rely on wireless communication and cloud connectivity, they create potential entry points for cyberattacks, unauthorized access, and data breaches. Vehicles increasingly store and transmit sensitive user and operational data, raising regulatory and consumer scrutiny. Ensuring end-to-end encryption, secure authentication, and compliance with evolving data protection laws adds complexity and cost for automakers and OTA technology providers. Additionally, any high-profile security incident could damage consumer trust and slow adoption rates. These concerns compel companies to invest heavily in robust cybersecurity frameworks, which can delay deployment timelines and increase overall system integration costs.

MARKET OPPORTUNITIES

Integration with Electric and Autonomous Vehicles to Unlock New Growth Avenues

The rapid adoption of Electric Vehicles (EVs) and autonomous driving technologies presents a strong opportunity for the OTA updates market. These vehicles rely heavily on software to manage battery performance, energy efficiency, Advanced Driver Assistance Systems (ADAS), and autonomous functionalities. OTA updates enable real-time optimization, bug fixes, and feature enhancements without requiring dealership visits. This capability is particularly valuable for EVs, where battery management systems can be continuously improved. Additionally, autonomous vehicles require frequent software updates to refine algorithms and ensure safety compliance. As automakers scale production of EVs and self-driving vehicles, OTA solutions become essential, creating significant growth potential for technology providers offering advanced update platforms and services.

MARKET CHALLENGES

Complex Software Integration and Validation to Challenge Implementation

One of the key challenges in the automotive OTA updates market is the complexity associated with software integration and validation across diverse vehicle architectures. Modern vehicles consist of numerous electronic control units (ECUs) from multiple suppliers, each requiring seamless coordination during updates. Ensuring compatibility, stability, and safety across all systems during OTA deployment is a highly intricate process. Any failure or malfunction during an update can lead to system disruptions or safety risks. Additionally, rigorous testing and validation are required to meet regulatory standards and avoid recalls. This complexity increases development time and costs for OEMs, making it difficult to standardize OTA solutions across different models and platforms.

Segmentation Analysis

By Technology Type

Rising Requirement for Continuous Software Enhancement to Drive SOTA Segment Dominance

Based on technology type segmentation, the market is categorized into Firmware OTA (FOTA), Software OTA (SOTA), and Full-System OTA (FSOTA).

The Software OTA (SOTA) segment dominates the market due to the increasing reliance on software-driven functionalities in modern vehicles. Automakers frequently deploy updates for infotainment, navigation, advanced driver Assistance Systems (ADAS) features, and user interfaces to enhance performance and customer experience. High demand for real-time feature upgrades, bug fixes, and personalization without dealership visits supports widespread SOTA adoption. Additionally, growing integration of connected services and subscription-based features further strengthens its dominance, as OEMs focus on delivering continuous value throughout the vehicle lifecycle.

The Full-System OTA (FSOTA) segment is projected to grow at a CAGR of 18.2% over the forecast period. Increasing adoption of centralized vehicle architectures and software-defined vehicles is enabling comprehensive vehicle-wide updates, driving demand for FSOTA solutions to manage complex system integrations efficiently.

By Vehicle Architecture Layer

Growing Shift Toward Domain-Based Architectures to Strengthen Domain Controller OTA Segment Leadership

Based on vehicle architecture layer segmentation, the market is categorized into ECU-level OTA, domain controller OTA, and centralized/zonal architecture OTA.

The domain controller OTA segment dominates the market as automakers increasingly adopt domain-based electronic architectures to manage complex vehicle functions efficiently. These systems enable coordinated updates across multiple ECUs within specific domains such as powertrain, ADAS, and infotainment. This improves update speed, reduces system fragmentation, and enhances reliability. OEMs prefer domain-level OTA as a transitional step toward full centralization, allowing scalable software management while maintaining compatibility with existing vehicle platforms, thereby driving widespread adoption.

The centralized/zonal architecture OTA segment is projected to grow at a CAGR of 19.2% over the forecast period. Increasing transition toward software-defined vehicles and high-performance computing platforms is accelerating demand for centralized OTA frameworks, enabling seamless, vehicle-wide updates with improved efficiency, scalability, and reduced hardware complexity.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle System

Rising Consumer Demand for Enhanced In-Car Experience to Drive Infotainment & Connectivity Segment Dominance

Based on vehicle system, the market is categorized into powertrain & energy systems, ADAS & autonomous driving, infotainment & connectivity, safety & security systems, and telematics & connectivity modules.

The infotainment & connectivity segment dominates the market due to its direct impact on user experience and high frequency of software updates. Features such as navigation, media, voice assistants, and connected services require continuous enhancements, bug fixes, and personalization. Automakers prioritize OTA updates for infotainment systems to improve customer satisfaction and enable subscription-based services. The rapid integration of smartphones, apps, and cloud-based platforms further accelerates update cycles, making this segment the most actively managed through OTA deployments across both mass-market and premium vehicles.

The powertrain & energy systems segment is projected to grow at a CAGR of 17.2% over the forecast period. Increasing adoption of electric vehicles and the need for continuous optimization of battery management and energy efficiency are driving OTA demand for powertrain-related software updates.

By Vehicle Type

Growing Consumer Preference for Versatility and Connected Features to Drive SUV Segment Dominance

Based on vehicle type, the market is categorized into hatchback & sedan, SUV, LCV, and HCV.

The SUV segment dominates the market due to its strong global demand and higher integration of advanced electronic and connected features. SUVs typically incorporate enhanced infotainment, ADAS, and connectivity systems, requiring frequent OTA updates for performance optimization and feature upgrades. Their rising adoption across both developed and emerging markets, coupled with premium positioning and higher software content per vehicle, encourages OEMs to prioritize OTA deployment in this segment, ensuring continuous improvements in user experience, safety functionalities, and digital services throughout the vehicle lifecycle.

The LCV segment is projected to grow at a CAGR of 16.2% over the forecast period. Expanding logistics, e-commerce, and fleet digitization are increasing demand for OTA-enabled updates in LCVs, supporting efficient fleet management, diagnostics, and performance optimization.

By Connectivity Technology

Expanding 5G Deployment and Always-On Connectivity to Drive Cellular Segment Dominance

Based on connectivity technology segmentation, the market is categorized into cellular (3G/4G/5G), Wi-Fi OTA, satellite OTA, and V2X/edge-assisted OTA.

The cellular (3G/4G/5G) segment dominates the market due to its widespread availability, reliability, and ability to support real-time, large-scale OTA updates. Automakers rely on cellular networks for seamless, remote software deployment across geographies without requiring user intervention. The rapid rollout of 5G further enhances data transfer speeds, enabling faster and more secure updates. Additionally, always-on connectivity supports continuous diagnostics, cloud integration, and connected services, making cellular technology the preferred choice for OEMs implementing scalable OTA solutions.

The V2X / edge-assisted OTA segment is projected to grow at a CAGR of 21.2% over the forecast period. Increasing adoption of edge computing and vehicle-to-everything communication is enabling faster, low-latency updates, improving efficiency and supporting next-generation connected and autonomous vehicle ecosystems.

Automotive Over-The-Air Updates Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Automotive Over-The-Air Updates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to strong vehicle production, rapid adoption of connected technologies, and increasing penetration of electric vehicles. Countries such as China, Japan, and South Korea are leading in software-defined vehicle development and 5G infrastructure deployment. Additionally, supportive government policies and growing consumer demand for smart mobility solutions further accelerate OTA adoption, making Asia Pacific the largest and most dynamic regional market.

China Automotive Over-The-Air Updates Market

The China market in 2026 is estimated at around USD 1.49 billion, accounting for roughly 28% of global market revenues. Rapid EV adoption, strong government support, and advanced digital ecosystem are accelerating large-scale OTA implementation.

Japan Automotive Over-The-Air Updates Market

The Japan market in 2026 is estimated at around USD 0.32 billion, accounting for roughly 5.1% of global market revenues. Increasing focus on vehicle connectivity, automation, and software upgrades continues to drive consistent market expansion.

Europe

Europe holds the second-largest market share and is projected to grow at a CAGR of 19.2% over the forecast period. The region’s strong focus on vehicle safety, cybersecurity regulations, and software compliance drives OTA adoption. Leading automakers are heavily investing in software-defined platforms and electrification, increasing reliance on OTA updates. Additionally, stringent emission norms and the push toward sustainable mobility require continuous software optimization. The presence of premium OEMs and technology providers further strengthens Europe’s position as a key market for advanced OTA deployment.

U.K. Automotive Over-The-Air Updates Market

The U.K. market in 2026 is estimated at around USD 0.15 billion, accounting for roughly 2.9% of global market revenues. Increasing EV adoption, regulatory focus on cybersecurity, and connected vehicle demand are accelerating OTA integration across vehicle segments.

Germany Automotive Over-The-Air Updates Market

The Germany market in 2026 is estimated at around USD 0.26 billion, accounting for roughly 4.8% of global market revenues. The presence of premium OEMs, strong R&D investments, and the transition toward software-defined vehicles are significantly driving OTA adoption.

North America

North America represents the third-largest market, driven by high penetration of connected vehicles and early adoption of OTA technologies. The presence of major automakers and technology companies fosters innovation in software platforms and cloud-based services. Consumers in the region demand advanced features, frequent updates, and seamless digital experiences, encouraging OEMs to expand OTA capabilities. Additionally, increasing investments in autonomous driving technologies and 5G infrastructure support market growth by enabling the efficient and large-scale deployment of OTA updates across diverse vehicle segments.

U.S. Automotive Over-The-Air Updates Market

The U.S. market in 2026 is estimated at around USD 0.91 billion, accounting for roughly 17.2% of global market revenues. High connected vehicle penetration, advanced 5G infrastructure, and the strong presence of tech-driven automakers support widespread OTA deployment.

Middle East & Africa

The Middle East & Africa market is witnessing gradual growth due to improving digital infrastructure and increasing adoption of connected vehicles. Rising investments in smart city initiatives and 5G deployment, particularly in countries such as the UAE and Saudi Arabia, are supporting OTA implementation. Although vehicle connectivity remains at a nascent stage compared to developed regions, growing demand for advanced automotive technologies is creating opportunities. OEMs are gradually introducing OTA-enabled features, especially in premium vehicles, contributing to steady market expansion across the region.

Latin America

Latin America is experiencing steady growth in the automotive OTA updates market, supported by gradual modernization of the automotive sector and increasing connectivity adoption. Countries such as Brazil and Mexico are witnessing rising demand for connected vehicles and digital services. While infrastructure limitations and cost sensitivity pose challenges, OEMs are progressively integrating OTA capabilities in new models. Additionally, expanding urbanization and improving telecom networks are enabling better connectivity, supporting long-term adoption of OTA solutions across passenger and light commercial vehicle segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Emphasis on Secure and Scalable OTA Platforms Intensifying Market Competition

The automotive OTA updates market is characterized by intense competition among global automotive suppliers, semiconductor companies, and software platform providers. Key players such as Bosch, Continental, Denso, Aptiv, and Qualcomm focus on developing secure, scalable, and cloud-integrated OTA solutions. Companies are investing heavily in cybersecurity frameworks, edge computing, and 5G-enabled connectivity to strengthen their offerings. Strategic partnerships with OEMs and cloud service providers are becoming increasingly common, enabling seamless software deployment, faster update cycles, and enhanced vehicle performance across diverse automotive platforms.

In addition to established players, emerging technology firms and software specialists are entering the market, intensifying innovation and competition. Companies are differentiating through advanced data analytics, AI-driven diagnostics, and subscription-based service models. Mergers, acquisitions, and collaborations are key strategies to expand technological capabilities and geographic presence. Furthermore, the shift toward software-defined vehicles is encouraging OEMs to develop in-house OTA capabilities, creating a dynamic competitive environment where continuous innovation, reliability, and security remain critical success factors.

LIST OF KEY AUTOMOTIVE OVER-THE-AIR UPDATES COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Aptiv PLC (Switzerland)

- Qualcomm Technologies, Inc. (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- Harman International (U.S.)

- Denso Corporation (Japan)

- NVIDIA Corporation (U.S.)

- Airbiquity Inc. (U.S.)

- BlackBerry QNX (Canada)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Bosch and Qualcomm expanded their partnership to include ADAS and centralized vehicle computing platforms, enabling scalable software-defined vehicle architectures supporting OTA-driven feature upgrades.

- January 2026: NVIDIA and Qualcomm unveiled next-generation automotive technologies at CES, focusing on AI-driven platforms and connected vehicle intelligence. NVIDIA announced deployment of its Drive AI software in Mercedes vehicles, while Qualcomm introduced Snapdragon Elite platforms supporting advanced OTA-enabled updates and connectivity.

- January 2026: Qualcomm expanded collaboration with Google to integrate Snapdragon Digital Chassis with automotive software, accelerating OTA-enabled AI features and real-time vehicle software upgrades.

- December 2025: Bosch introduced AI-enabled cockpit upgrade platforms allowing OTA-based enhancements without hardware replacement, supporting long-term vehicle software lifecycle management.

- November 2025: Aptiv PLC expanded its software-defined vehicle architecture strategy, strengthening OTA update capabilities for scalable and secure vehicle-wide software deployment.

- August 2025: NXP Semiconductors launched advanced automotive processors supporting secure OTA updates, targeting domain and zonal architectures in next-generation vehicles.

- July 2025: BlackBerry QNX enhanced its OTA platform with fail-safe update mechanisms, ensuring reliability and minimizing risks associated with incomplete or interrupted updates.

REPORT COVERAGE

The global automotive over-the-air updates market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology Type, By Vehicle Architecture Layer, By Vehicle System, By Vehicle Type, By Connectivity Technology, and By Region |

| By Technology Type |

|

| By Vehicle Architecture Layer |

|

| By Vehicle System |

|

| By Vehicle Type |

|

| By Connectivity Technology |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.13 billion in 2025 and is projected to reach USD 21.96 billion by 2034.

In 2025, the market value stood at USD 1.95 billion.

The market is expected to exhibit a CAGR of 19.4% during the forecast period.

The SUV segment led the market by vehicle type.

The rising software-defined vehicles to accelerate OTA adoption.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us