Automotive Pumps Market Size, Share & Industry Analysis, By Type (Fuel Pump, Oil Pump, Water Pump, Vacuum Pump, and Others), By Vehicle Type (Two Wheeler, Passenger Cars, and Commercial Vehicles), By Technology (Mechanical and Electric), and Regional Forecast, 2026-2034

Automotive Pumps Market Size

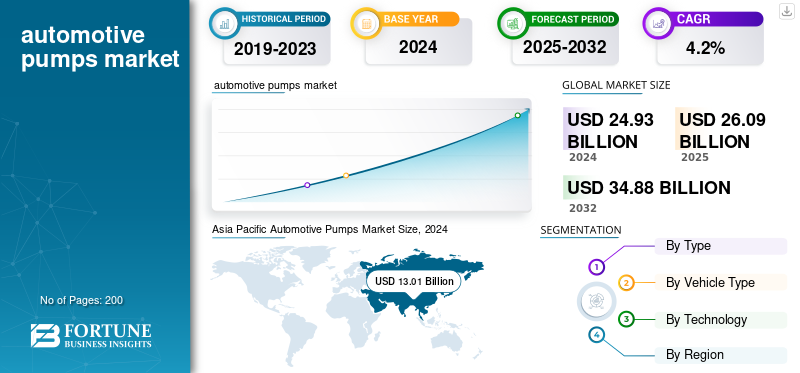

The global automotive pumps market size was valued at USD 26.09 billion in 2025 and is projected to grow from USD 27.31 billion in 2026 to USD 37.43 billion by 2034, exhibiting a CAGR of 4.02% during the forecast period. Asia Pacific dominated the global automotive pumps market with a market share of 51.85% in 2025.

Automotive pumps are mechanical or electronic devices used in vehicles to circulate essential fluids such as fuel, oil, coolant, and transmission fluids throughout the engine and other systems. These pumps maintain optimal lubrication, temperature control, and hydraulic pressure, ensuring efficient performance, reduced emissions, and extended engine life. Common types include fuel pumps, fuel injection pumps, oil pumps, water pumps, and vacuum pumps. With increasing electrification and emission regulations, modern vehicles increasingly employ electronically controlled and energy-efficient pump technologies to enhance reliability and fuel economy.

Growing vehicle production, emission norms, and demand for fuel-efficient technologies drive the demand for automotive pumps. Trends toward electrification and the shift toward hybrid and electric vehicles are further advancing the use of electric and variable-displacement pumps. Additionally, the integration of smart sensors and lightweight materials enhances performance and reduces energy loss. Major companies operating in this space include Robert Bosch GmbH, Continental AG, Denso Corporation, Aisin Seiki Co., Ltd., Delphi Technologies, Johnson Electric, ZF Friedrichshafen AG, and Magna International, all of which focus on efficiency, innovation, and cost optimization.

U.S. tariffs on imported automotive components, particularly from China and Europe, have impacted supply chains, pricing, and manufacturing strategies within the global automotive market. These tariffs increased production costs for OEMs and tier-1 suppliers, leading to localized manufacturing expansion in North America to reduce dependency on imports. Companies have also sought alternative sourcing regions in Mexico, India, and Southeast Asia. Although short-term disruptions in pricing and logistics occurred, the tariffs accelerated regionalization, prompting investment in advanced, cost-efficient, and compliant pump manufacturing technologies.

Download Free sample to learn more about this report.

AUTOMOTIVE PUMPS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 26.09 Billion

- 2026 Market Size: USD 27.31 Billion

- 2034 Forecast Market Size: USD 37.43 Billion

- CAGR: 4.02% from 2026–2034

- Asia Pacific dominated the automotive pumps market with a 51.85% share in 2025.

- The water pump segment is projected to account for 26.55% of the market in 2026.

- The passenger cars segment is expected to contribute 61.89% of the global market in 2026.

North America

The North America market was valued at USD 4.92 Billion in 2025, capturing 18.85% of global revenue, and is estimated to reach USD 5.17 Billion in 2026.

Europe

In 2025, Europe held 23.87% of the global market, reaching a valuation of USD 6.23 Billion, and is projected to grow to USD 6.56 Billion in 2026.

Asia Pacific

The market in Asia Pacific reached USD 13.53 Billion in 2025, representing 51.85% of total market revenue, and is projected to reach USD 14.06 Billion in 2026.

U.S.

The U.S. automotive pumps market is estimated to reach USD 3.35 billion by 2026, supported by robust vehicle production, replacement demand, and increasing focus on pump reliability and safety.

Japan

Japan’s automotive pumps market is estimated to reach USD 1.90 billion by 2026, driven by strong automotive manufacturing capabilities and rising adoption of advanced vehicle technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rapid Electrification of Vehicle Powertrains Drives Market Growth

The driving factor for the global market is the rapid electrification of vehicle powertrains, along with the associated thermal management requirements. As more hybrid and battery electric vehicles enter production, traditional mechanical pumps alone cannot meet the growing demand for precise fluid control, thermally efficient cooling, and integrated fluid circuits. Manufacturers such as Bosch Mobility Solutions are introducing pumps such as the PDE electric coolant pump, tailored for battery and dual-axle cooling. This highlights that pump systems are evolving from simple engine cooling to high-power thermal loops that span batteries, inverters, and e-axles. As BEVs and hybrids replace engine-driven pump shafts with electronically controlled fluid loops, the market is compelled to expand its product portfolios with electric pumps. These new pump systems deliver more efficient flow matching, lower parasitic losses, and better integration with vehicle control systems, factors that support both performance and emissions compliance.

MARKET RESTRAINTS

Instability in the Supply Chain of Critical Components and Raw Materials Hinders Market Growth

This hampers production and increases costs across pump manufacturers and vehicle makers. The pump industry relies on components such as precision alloys, bearing assemblies, electronic control units, and even semiconductors for the increasingly electrified pump modules. As pump suppliers often have long lead times and tight integration with vehicle assembly lines, any delay or cost escalation in key components forces tier-1 pump vendors to either absorb higher costs or pass them upstream, which reduces profitability or delays product launches. Moreover, aftermarket replacement demand also suffers when parts are back-ordered, reducing the strength of that sales channel. In summary, the complex and globalized nature of the automotive pumps value chain means that supply chain fragility, rising input costs, scarcity of specialized components, and logistics bottlenecks are acting as a brake on faster growth and efficient scaling in the market.

MARKET OPPORTUNITIES

Fast Deployment of Advanced Thermal Management Systems for Electric and Hybrid Vehicles Generates Beneficial Opportunities

As electrification deepens, both OEMs and tier-1 pump suppliers are witnessing significant orders and product launches. As vehicles go electric or hybrid, the conventional engine-driven fluid pumps diminish in their role, but they are replaced by electric pumps, including coolant, vacuum, and transmission/oil pumps, which require new design, motors, electronics, diagnostics, and production capacity. Suppliers who invest in these electrified pump systems gain new business streams. In addition, growing regulatory pressure for emissions and energy efficiency means that thermal systems must become more efficient, reducing energy loss and enabling smaller, lighter pump modules to be integrated into electric vehicle architectures. Thus, this transition from electrification to thermal management constitutes a high-leverage opportunity for the market.

AUTOMOTIVE PUMPS MARKET TRENDS

Shift from Purely Mechanical Pump Systems to Electronically Controlled and Electric-Drive Pump Modules

One major trend in the global market is the widespread shift from purely mechanical pump systems to electronically controlled and electric-drive pump modules, especially driven by vehicle electrification and advanced thermal management. This trend supports the market by opening up entirely new product categories such as electric water/coolant pumps, high-voltage vacuum/auxiliary pumps, and smart pump modules with speed control and diagnostics. For example, the adoption of electric water pumps in hybrid and EV architectures allows manufacturers to eliminate mechanical drive-belt losses, reduce parasitic energy consumption, and optimize thermal loops for battery, inverter, and motor cooling.

For pump suppliers, this trend means investing in new motor-control electronics, integrated sensors, software diagnostics, and higher-voltage architectures (e.g., 48 V or 400 V/800 V systems). It also drives aftermarket and OEM replacement cycles differently: electric modules have different failure modes, diagnostic needs, and service flows compared to mechanical units. The trend lowers barriers for legacy mechanical-pump suppliers to lose share if they do not adapt to electric pump platforms. Yet, it also presents an opportunity to capture the premium electric module segment. Automotive OEMs, under global emissions/efficiency mandates, view electric-pump architectures as one of the enablers of improving system efficiency. Pump suppliers who align with platform electrification are better positioned for next-generation vehicle programs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Oil Pumps Dominate Due to the Existing Vast Global Fleet of ICE and HEV Powertrains

By type, the market is sub-segmented into fuel pump, oil pump, water pump, vacuum pump, and others.

The Water Pump segment is projecteed to dominate the market with a share of 26.55% in 2026. the oil pump segment held the leading position by capturing the largest share of the market. Oil pumps remain the backbone of lubrication and thermal control in the vast global fleet of internal-combustion and hybrid powertrains. As electrification accelerates, high-efficiency variable and electric oil pumps are proliferating in hybrids and e-axles, extending the category’s leadership. The sustained demand for engine/transmission lubrication, combined with a large installed base, requires replacement over time. Bosch portfolio adds electronically controlled coolant/oil solutions that integrate speed control and diagnostics, reinforcing the migration to intelligent pumps. Modernization from mechanical to electric/variable oil pumps keeps this sub-segment essential across ICE, hybrid, and e-axle lubrication, supporting both OEM fitment and long-term service demand.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Passenger Cars Hold Leading Position Due to Their Highest Numbers Globally

By vehicle type, the market is categorized into two-wheeler, passenger cars, and commercial vehicles.

The Passenger Cars segment is expected to lead the market, contributing 61.89% globally in 2026. Passenger cars command the highest volumes worldwide, driving demand for pumps across fuel, oil, coolant, and auxiliary circuits. In 2024, Europe registered around 10.6 million new cars with BEVs, accounting for a 13.6% share, while ICE/hybrids collectively represented the remainder, requiring substantial pump content. Europe’s recent registration data also show hybrid and PHEV momentum, which inherently uses electric coolant and vacuum pumps, reinforcing content per passenger car.

By Technology

Mechanical Type Dominates Because of Its Global Installation on Road Stock

By technology, the market is split into mechanical and electric.

The Mechanical segment is projecteed to dominate the market with a share of 56.36% in 2026. Despite the rapid electrification of the global ICE fleet, mechanical pumps still equip the majority of the fleet and a large share of current production, especially in oil and fuel delivery. Mechanical pumps sustain huge baseline volumes and aftermarket pull. Yet, the transition path is clear; electronically driven pumps are scaling with EV/hybrid platforms. For the forecast window, mechanical technology remains prevalent due to the enormous legacy parc and ongoing ICE/hybrid production in many regions; simultaneously, OEMs are back-specifying efficiency gains into mechanical designs to meet emissions and durability targets. The coexistence of a dominant mechanical base with rapidly growing electric modules sustains total pump demand while enabling suppliers to diversify their portfolios and reinvest in next-generation electrified solutions, supporting overall market growth.

AUTOMOTIVE PUMPS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

Asia Pacific Automotive Pumps Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 4.92 Billion in 2025, capturing 18.85% of global revenue, and is estimated to reach USD 5.17 Billion in 2026. North America’s automotive pumps market growth is driven by a large ICE vehicle parc needing fuel, oil, and transmission pumps, alongside growing demand for electric coolant and auxiliary pumps in hybrids and EVs. Strong aftermarket networks and stringent safety expectations keep replacement volumes high and push suppliers to improve reliability. In October 2024, American Honda announced a recall of 720,000 U.S. vehicles to inspect and replace defective high-pressure fuel pumps, highlighting continuing focus on pump quality and safety. The U.S. market is estimated to reach USD 3.35 billion by 2026.

The U.S. leads North America with high pump demand from SUVs and pickups, plus rapid expansion of EV thermal-management solutions. Recalls around fuel-pump reliability and rising adoption of electric coolant pumps in new EV platforms together sustain strong OEM and aftermarket pump volumes.

Europe

In 2025, Europe held 23.87% of the global market, reaching a valuation of USD 6.23 Billion, and is projected to grow to USD 6.56 Billion in 2026. Europe is the fastest-growing region as aggressive CO₂ targets and rapid electrification raise demand for efficient electric water, oil, and vacuum pumps. EV and plug-in hybrid platforms require multi-circuit thermal management, boosting electric coolant and auxiliary pump content per vehicle. Strong Tier-1 presence of Bosch, Continental, Valeo, Gates, and NTN underpins technology upgrades and extensive aftermarket coverage. In October 2023, Continental introduced 17 types of adjustable auxiliary water pumps specifically for hybrid and electric vehicles, underscoring this electrification-driven pump market expansion. The UK market is estimated to reach USD 0.78 billion by 2026, and the Germany market is estimated to reach USD 2.08 billion by 2026.

Asia Pacific

The market in Asia Pacific reached USD 13.53 Billion in 2025, representing 51.85% of total market revenue, and is projected to reach USD 14.06 Billion in 2026. Asia Pacific dominates the global automotive pumps market, supported by its position as the world’s largest vehicle production hub and rapidly expanding NEV fleet. China, Japan, and India collectively produce the majority of global vehicles, driving huge baseline demand for fuel, oil, water, and transmission pumps in ICE and hybrid models, while EV growth accelerates the adoption of electric coolant and oil pumps. Local and global suppliers compete aggressively on cost and efficiency, and high production volumes across passenger cars and two-wheelers cement Asia Pacific’s leading share in pump consumption. The Japan market is estimated to reach USD 1.9 billion by 2026, the China market is estimated to reach USD 6.62 billion by 2026, and the India market is estimated to reach USD 2.55 billion by 2026.

Rest of the World

The rest of the world observes steady growth in automotive pumps, driven by an expanding vehicle parc, infrastructure development, and hot-climate operating conditions that stress cooling systems. Mechanical fuel and water pumps still dominate, but electrification initiatives and hybrid imports gradually introduce electric auxiliary and coolant pumps. Global suppliers leverage regional distributors to expand coverage and support demanding duty cycles in commercial fleets and off-road applications. Over time, tightening emissions standards and gradual EV adoption are expected to lift demand for higher-efficiency, electronically controlled pump solutions in these markets. In 2025, Rest of the World generated USD 1.42 Billion, contributing 5.43% to global market revenue, and is projected to grow to USD 1.52 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

High System Integration and Diversified Supply Chains Anchor Market Competition

The global automotive pumps market is led by tier-1 suppliers such as Bosch, Continental AG, Valeo, and Denso Corporation, which provide a diversified portfolio of fuel, water, oil, transmission, and steering pumps to global OEMs. Their broad manufacturing footprint, long-standing OEM relationships, and capability to deliver both mechanical and electric pump technologies ensure reliable supply and global aftermarket coverage. Mid-size and specialty players also compete on pump type, efficiency, and EV-ready solutions, increasing overall supply-chain resilience and lowering entry barriers for OEMs seeking multi-vendor sourcing. The shift toward electrification and thermal-management needs is accelerating demand for electric coolant and water-pump systems, giving room to newer, agile suppliers to innovate and supply next-generation pump solutions for hybrid and EV platforms.

LIST OF KEY AUTOMOTIVE PUMPS COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- Aisin Seiki Co., Ltd. (Japan)

- Continental AG (Germany)

- Delphi Technologies (U.K.)

- Rheinmetall AG (Germany)

- SHW AG (Germany)

- Hitachi Astemo (Japan)

- Mikuni Corporation (Japan)

- Valeo S.A. (France)

- Hella GmbH & Co. KGaA (Germany)

- Mahle GmbH (Germany)

- Magna International (Canada)

- Cummins Inc. (U.S.)

- TRW Automotive (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Rheinmetall AG received a significant contract from a major North American truck manufacturer. The deal covers the supply of CWA 2000 high-voltage electric coolant pumps for battery-electric medium- and heavy-duty trucks, with deliveries scheduled from 2028 to 2035. These 800-V-ready pumps enable thermal control of traction batteries, motors, and power electronics in high-load commercial applications. Rheinmetall stated that this long-term agreement strengthens its North American footprint and underlines how heavy-duty OEMs are now electrifying drivetrains at scale, driving demand for fuel-efficient vehicles, with advanced, low-noise, and maintenance-free coolant pump technologies.

- September 2024: Robert Bosch GmbH introduced its next-generation PDE electric coolant pump, a power-dense unit engineered for electric and hybrid vehicles. Delivering up to 1,200 liters per hour at 1.7 bar, the pump offers an expected service life exceeding 41,000 operating hours. It supports active cooling for batteries, inverters, and dual e-axles, critical for fast-charging capability and long component life. Bosch emphasized its compact packaging, high efficiency, and precise variable-speed control, noting that the PDE design reduces energy consumption compared to belt-driven mechanical pumps and forms a key element of its integrated thermal management platform for e-mobility.

- August 2024: Rheinmetall AG released an update on its mechanical and variable coolant-pump portfolio, confirming production of both direct-drive and solenoid-controlled variable-flow designs. The latter enables on-demand coolant delivery, reducing parasitic losses and improving fuel efficiency in combustion engines. Rheinmetall’s statement emphasized continued R&D investment to bridge the gap between traditional mechanical solutions and fully electric pumps for hybrid applications. The company showcased prototypes capable of integrating electronic control valves and real-time diagnostics, underscoring its strategy to combine the reliability of mechanical units with the adaptability of electronically modulated systems in modern powertrains.

- June 2024: Rheinmetall AG announced that it had secured a major order for electric coolant pumps from a leading international automobile manufacturer. The order involves production running through 2030 and a service contract extending to 2045. The pumps are designed for use in next-generation hybrid vehicles, offering high efficiency, precise electronic control, and durability under demanding thermal-management conditions. Rheinmetall emphasized that the contract reinforces its growing leadership in electrified mobility solutions and highlights the industry’s shift from mechanical to electric fluid-handling systems for cooling batteries, inverters, and e-axles.

- October 2022: Bosch expanded its aftermarket electric coolant-pump portfolio across Europe. The new range now includes more than 50 part numbers, 14 of which cover hybrid and electric applications, representing approximately 60 percent of passenger cars and light vans in the region equipped with electric pumps. The company highlighted that the extension ensures independent workshops can service modern cooling systems in EVs and hybrids with OE-level components. Bosch also introduced updated cataloging and diagnostic support for multi-pump architectures, aiming to enhance the aftermarket’s readiness for increasingly electrified thermal management systems in both new and legacy vehicle platforms.

- May 2022: DENSO Corporation and Aisan Industry Co., Ltd. announced an agreement to transfer DENSO’s fuel-pump module business to Aisan. The strategic move consolidates expertise in fuel-supply systems and enhances manufacturing efficiency. Both companies stated that the collaboration allows a sharper focus on electrification while optimizing cost and quality in ICE and hybrid fuel-delivery systems. The transfer highlights ongoing restructuring among Tier-1 suppliers, who are specializing in next-generation propulsion components.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.02% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Vehicle Type, Technology, and Region |

|

By Type |

· Fuel Pump · Oil Pump · Water Pump · Vacuum Pump · Others |

|

By Vehicle Type |

· Two Wheeler · Passenger Cars · Commercial Vehicles |

|

By Technology |

· Mechanical · Electric |

|

By Geography |

· North America (By Type, Vehicle Type, Technology, and Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Type, Vehicle Type, Technology, and Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Type, Vehicle Type, Technology, and Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Type, Vehicle Type, Technology, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 26.09 billion in 2025 and is projected to reach USD 37.43 billion by 2034.

In 2025, the market value stood at USD 13.53 billion.

The market growth is expected to expand at a CAGR of 4.02% during the forecast period.

The mechanical segment leads by holding the maximum share.

Rising technical shift to high-pressure fuel delivery systems drives market growth.

Top players in include Robert Bosch GmbH, Continental AG, Denso Corporation, Aisin Seiki Co., Ltd., and Delphi Technologies.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us