Automotive Seats Market Size, Share & Industry Analysis, By Position (Front and Rear), By Distribution Channel (OEM and Aftermarket), By Material (Fabric/Textile, Synthetic Leather, Genuine Leather, and Others), By Powertrain (ICE and Electric), By Type (Bucket, Bench, Folding, Suspension, and Others), By Technology (Manual, Power, Comfort, and Others), By Component (Structures & Mechanisms, Foam & Trims, Electronics & Comfort Modules, Safety Components, and Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), and Regional Forecast, 2026-2034

Automotive Seats Market Size & Share

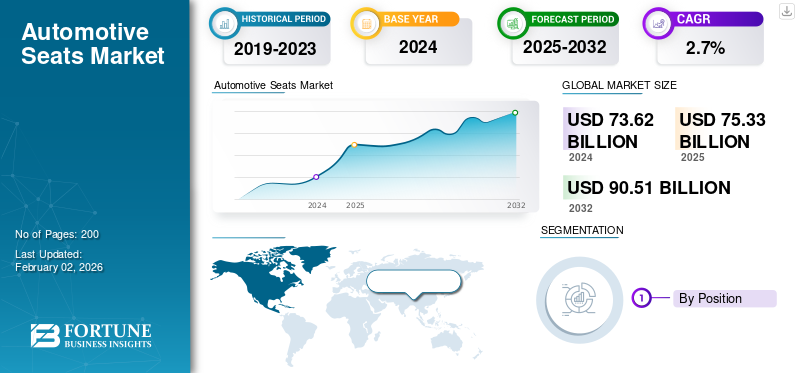

The global automotive seats market size was valued at USD 75.33 billion in 2025. The market is projected to grow from USD 77.35 billion in 2026 to USD 95.13 billion by 2034, exhibiting a CAGR of 2.62% during the forecast period. Asia Pacific dominated the global market with a share of 54.67% in 2025.

The automotive seats market represents the industry focused on designing, manufacturing, and supplying seating systems that enhance comfort, safety, and aesthetics in vehicles. Over the next few years, the market is expected to experience steady growth, driven by increasing vehicle production, growing consumer preference for advanced seat technologies, and rising demand for electric and luxury vehicles. Innovations such as lightweight materials, smart seating, and integrated climate control are shaping product development. Moreover, stringent safety regulations, ergonomic design trends, and the shift toward sustainable materials are encouraging manufacturers to develop more efficient, eco-friendly, and customizable seating solutions worldwide.

Key players in the market include Adient plc, Lear Corporation, FORVIA SE, Toyota Boshoku Corporation, Magna International Inc., and TS Tech Co. Ltd. These companies compete through innovations in lightweight materials, modular seat designs, and advanced comfort features. Strategic partnerships, mergers, and investments in smart seating technologies help strengthen their global presence. Many firms focus on sustainability by adopting recyclable materials and energy-efficient production methods. Additionally, moves such as footprint expansion in emerging markets and product portfolio alignment with electric and autonomous vehicle trends enable these players to enhance profitability and maintain a strong competitive edge in the evolving industry.

Download Free sample to learn more about this report.

Automotive Seats Market MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 75.33 billion

- 2026 Market Size: USD 77.35 billion

- 2034 Forecast Market Size: USD 95.13 billion

- CAGR: 2.62% from 2026–2034

- Asia Pacific dominated the global market with a share of 54.67% in 2025.

- The front seats segment held the largest market share of 56.56% in 2026.

- The OEM segment is expected to dominate the market with a share of 96.75% in 2026.

North American

North America contributed approximately USD 14.36 Billion to the global market in 2025, accounting for a 19.07% share, and is expected to reach USD 14.6 Billion in 2026.

Europe

In 2025, the Europe market stood at USD 16.28 Billion, representing 21.61% of global demand, and is projected to grow to USD 16.5 Billion in 2026.

Asia Pacific

The Asia Pacific region captured 54.67% of the global market in 2025, generating USD 41.18 billion in revenue, and is projected to reach USD 42.67 billion in 2026.

U.S.

The U.S. market is projected to reach USD 9.22 billion by 2026.

Japan

The Japan market is projected to reach USD 7.32 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Comfort and Safety Features to Drive Market Expansion

Growing consumer expectations for enhanced in-vehicle comfort and safety is a major driver of the market. Modern buyers seek ergonomic designs, adjustable seating, and integrated technologies such as heating, ventilation, and massage functions. Automakers are increasingly incorporating advanced safety systems, including side-impact airbags and active head restraints, directly into seat structures. This trend is particularly pronounced in premium and electric vehicles, where differentiation largely depends on the interior experience. As a result, seat manufacturers are investing in smart materials, sensor integration, and lightweight construction to meet evolving regulatory standards and consumer preferences worldwide.

MARKET RESTRAINTS

High Production and Material Costs to Restrain Market Growth

One of the key restraints in the market is the high cost associated with advanced materials, design complexity, and integration of electronic components. Premium features such as climate control, sensors, and power adjustments increase overall production expenses. Additionally, the shift toward lightweight materials, such as composites and high-strength alloys, increases procurement and manufacturing costs. The fluctuating prices of raw materials, especially leather and foam, further challenge profit margins. These factors make it difficult for manufacturers to offer cost-effective solutions, particularly in price-sensitive markets, thereby limiting the widespread adoption of technologically advanced seating systems.

MARKET OPPORTUNITIES

Growing Adoption of Electric and Autonomous Vehicles Offer Lucrative Market Opportunities

The increasing production of electric and autonomous vehicles presents a significant opportunity for the market. These vehicles emphasize interior comfort, customization, and advanced connectivity, driving the demand for innovative automotive seating solutions. Autonomous driving enables flexible cabin layouts, offering opportunities for swivel, recline, and modular seat designs. Additionally, electric vehicles require lightweight seats to improve energy efficiency and range. Manufacturers can capitalize on this trend by developing smart, sustainable, and adaptable seating systems tailored to new mobility needs. This transformation is expected to significantly reshape product innovation and drive automotive seats market growth in the near future.

AUTOMOTIVE SEATS MARKET TRENDS

Integration of Smart and Connected Seating Technologies is one of the Significant Market Trends

A major trend shaping the market is the integration of smart and connected technologies. Modern vehicles are increasingly equipped with seats featuring embedded sensors, memory functions, and connectivity to monitor posture, temperature, as well as the health of occupants. These systems enable personalized comfort settings and enhance safety by detecting driver fatigue or improper seating positions. Connectivity with infotainment and vehicle control systems further elevates the in-cabin experience. As automakers focus on intelligent interiors and human-machine interaction, seat manufacturers are investing in digital innovation and ergonomic design. This transforms traditional seating into multifunctional, tech-enabled comfort systems for next-generation vehicles.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Complex Supply Chain and Manufacturing Constraints Challenges Market Deployment

A significant challenge in the market is managing complex supply chains and manufacturing processes. Seat production involves numerous components, including frames, foams, textiles, and electronic systems, which are often sourced from multiple suppliers across various regions. Disruptions caused by raw material shortages, logistics delays, or geopolitical tensions can impact production timelines and costs. Additionally, integrating advanced technologies while maintaining strict quality and safety standards adds to operational complexity. Manufacturers need to continuously balance customization demands with mass production efficiency. This requires strong supplier coordination and agile manufacturing strategies to remain competitive in an increasingly dynamic and resource-sensitive market environment.

Segmentation Analysis

By Position

Rising Demand for Advanced Comfort and Safety Features to Drives Front Seats Segment Growth

Based on position, the market is bifurcated into front and rear.

The front seats segment held the largest market share of 56.56% in 2026. The growth of this segment is driven by the rising demand for enhanced driver and passenger comfort, safety, and ergonomics. The increasing adoption of power-adjustable, ventilated, and heated front seats, particularly in premium and electric vehicles, supports market expansion. Additionally, technological advancements such as integrated airbags, memory functions, and smart sensors are encouraging automakers to upgrade front seat designs for improved performance and convenience.

The rear seats segment is expected to grow at the fastest CAGR of 3.0% over the forecast period. Rising consumer preference for comfort and convenience in passenger areas, particularly in premium and electric vehicles, will drive the growth of rear seats. Features such as recline functions, climate control, entertainment integration, and foldable configurations enhance the overall cabin experience. Automakers are also emphasizing spacious interiors and advanced materials, further boosting the demand for high-quality, ergonomic rear seating solutions.

By Distribution Channel

Rising Vehicle Production and Integration of Advanced Seating Systems to Drive OEM Segment Growth

In terms of distribution channel, the market is divided into OEM and aftermarket.

The OEM segment is expected to dominate the market with a share of 96.75% in 2026, driven by increasing global vehicle production and the integration of advanced seating technologies during the manufacturing process. Automakers are collaborating with seat suppliers to develop lightweight, ergonomic, and feature-rich designs that meet safety and comfort standards. The growing demand for electric and luxury vehicles further supports OEMs' adoption of innovative, customized seating solutions to enhance the overall driving experience and brand value.

The aftermarket segment is expected to exhibit a high CAGR of 3.4% during the forecast period, with its growth characterized by rising consumer interest in vehicle customization, comfort enhancements, and aesthetic upgrades. Increasing replacement of worn-out or damaged seats in aging vehicles also fuels demand. Additionally, the growing popularity of performance and racing seats among enthusiasts, combined with the expansion of e-commerce channels for automotive accessories, is encouraging manufacturers to offer a diverse range of high-quality aftermarket seating options.

By Material

Rising Preference for Durable and Cost-Effective Upholstery Materials Reinforce Synthetic Leather Segment Growth

By material, the market is divided into fabric/textile, synthetic leather, genuine leather, and others.

The synthetic leather segment dominates the market with a share of 53.91% in 2026 & owing to its durability, affordability, and ease of maintenance compared to genuine leather. Increasing consumer focus on premium aesthetics and eco-friendly materials supports its adoption. Automakers favor synthetic leather for its lightweight properties, resistance to wear, and design flexibility, making it a popular choice for mass-market and luxury vehicles across global automotive production lines.

The others segment is expected to grow at the highest CAGR of 2.9% during the forecast period. The growth of composites and recycled materials is driven by rising environmental awareness and regulatory pressure to reduce vehicle emissions. Automakers are adopting lightweight, eco-friendly materials to improve fuel efficiency and meet sustainability goals. Composites and recycled fabrics offer strength, comfort, and design flexibility, enabling manufacturers to develop durable, high-performance seating solutions while supporting circular economy initiatives within the automotive industry.

To know how our report can help streamline your business, Speak to Analyst

By Powertrain

Sustained Vehicle Production and Demand in Developing Regions to Drive the Growth of ICE Segment

On the basis of powertrain, the market is segmented into ICE and electric.

The ICE segment is expected to dominate the market in 2026 with a share of 64.63%. Steady production and strong consumer demand for conventional vehicles, especially in emerging economies, will bolster the segment’s growth. Lower fuel prices, well-established infrastructure, and affordability continue to support the sales of ICE vehicles. Automakers are enhancing seat comfort, safety, and design in these models to attract buyers, ensuring consistent demand for seating systems within the traditional automotive segment.

The electric segment will grow at a rapid CAGR of 11.0% during the forecast period. Rising electric vehicle production and consumer preference for advanced, comfortable interiors will augment the segment’s growth. EV manufacturers emphasize lightweight, energy-efficient seating to enhance vehicle range and sustainability. The integration of smart features, such as climate control, adjustable support, and eco-friendly materials, further boosts demand. This makes innovative seat designs a key differentiator in the evolving electric mobility landscape.

By Type

Rising Demand for Sporty Design and Enhanced Driver Support Fortify Bucket Seats Segment Growth

Based on type, the market is categorized into bucket, bench, folding, suspension, and others.

The bucket seat type segment dominates the market due to increasing demand for sporty aesthetics, superior comfort, and better lateral support. These seats are widely adopted in performance, luxury, and electric vehicles to enhance driving dynamics and passenger safety. Advancements in ergonomic design, lightweight materials, and customization options further boost their popularity among consumers seeking a premium and performance-oriented driving experience.

The others segment will grow at a rapid CAGR of 5.7% during the forecast period. The increasing adoption of seats in luxury vans, SUVs, and long-haul vehicles enhances passenger relaxation and convenience. Features such as reclining mechanisms, extended legroom, massage functions, and high-quality materials are encouraging automakers to integrate these advanced seating options across upscale and long-distance vehicle segments.

By Technology

High Demand for Affordable and Reliable Seating Solutions Drive Manual Segment Growth

Based on technology, the market is categorized into manual, power, comfort, and others.

The manual segment captured the majority of market share in 2024. Strong demand in entry-level and mid-range vehicles, where cost efficiency and durability are key priorities, will drive the segment’s growth. Manual seats are easier to manufacture, lightweight, and require minimal maintenance compared to powered alternatives. Their affordability and widespread use in compact and commercial vehicles make them a preferred choice in price-sensitive markets and developing automotive regions.

The others segment will grow at the highest CAGR of 4.3% over the forecast period. Smart & connected seats integrate sensors, memory functions, and connectivity to monitor posture, temperature, and occupant health. The rising demand for premium vehicles, along with a growing focus on safety and driver well-being, encourages automakers to incorporate intelligent seating systems that enhance the user experience and overall vehicle functionality.

By Component

Increasing Focus on Seat Safety, Durability, and Lightweight Design Boosts Structures & Mechanisms Segment Growth

Based on component, the market is divided into structures & mechanisms, foam & trim, electronics & comfort modules, safety components, and others.

The structures & mechanisms segment dominated the market in 2024. Rising demand for stronger, safer, and lighter seat frames will drive the demand for structural and mechanical components. Automakers are adopting advanced materials, such as high-strength steel and aluminum, to enhance crash performance and improve fuel efficiency. Continuous innovation in recliner mechanisms, height adjusters, and folding systems further supports the development of durable, ergonomic, and space-efficient seating structures across vehicle categories.

The electronics & comfort modules segment is expected to grow rapidly at a CAGR of 4.8% over the forecast period. Modern vehicles incorporate electronic systems for heating, ventilation, massage, and memory functions to enhance passenger comfort and convenience. Additionally, the growing emphasis on driver assistance and occupant safety supports the adoption of sensor-based control modules, making electronic integration a key factor in seat innovation and performance.

By Vehicle Type

Rising Demand for Comfort, Safety, and Advanced Seating Features in Passenger Cars Fuels Segmental Growth

Based on vehicle type, the market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles.

The passenger cars segment dominated the market in 2024 and is expected to grow at the highest CAGR of 2.8% during the forecast period. The segment growth is driven by increasing consumer preference for comfort, safety, and enhanced driving experiences. Automakers are incorporating advanced features, such as power adjustments, ventilation, lumbar support, and smart sensors, to enhance occupant well-being and comfort. Rising production of electric and luxurious vehicles further accelerates innovation in seat design, emphasizing lightweight materials and ergonomic configurations. Additionally, stringent safety standards and growing awareness of interior quality among buyers are pushing manufacturers to invest in premium, customizable seating solutions that enhance both comfort and aesthetic appeal.

Automotive Seats Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Seats Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 54.67% of the global market in 2025, generating USD 41.18 billion in revenue, and is projected to reach USD 42.67 billion in 2026. The growth of the region is driven by rapid vehicle production, increasing disposable income, and rising demand for enhanced in-vehicle comfort. Countries such as China, India, Japan, and South Korea are major automotive hubs, supporting large-scale vehicle manufacturing and exports. The growing adoption of electric and luxury cars, along with urbanization and technological advancements, is driving the integration of advanced seating features. Additionally, supportive government policies, expanding aftermarket sales, and cost-efficient production capabilities strengthen the region’s position as a leading center for innovation and development in automotive seats.

The Japan market is projected to reach USD 7.32 billion by 2026, the China market is projected to reach USD 23.75 billion by 2026, and the India market is projected to reach USD 4.18 billion by 2026.

North America

North America contributed approximately USD 14.36 Billion to the global market in 2025, accounting for a 19.07% share, and is expected to reach USD 14.6 Billion in 2026. North America holds the third-largest automotive seats market share, driven by the rising demand for luxury and high-performance vehicles equipped with advanced comfort and safety features. Consumers are increasingly preferring seats with heating, ventilation, and massage functions, prompting automakers to integrate innovative technologies. Strong presence of major OEMs, high vehicle ownership rates, and rapid adoption of electric vehicles further boost market expansion. Additionally, emphasis on lightweight materials, ergonomic design, and sustainability supports continuous innovation, positioning North America as a key hub for next-generation automotive seating solutions.

The U.S. market is projected to reach USD 9.22 billion by 2026. The U.S. dominates the North American market due to strong consumer demand for advanced comfort, safety, and customization features in vehicles. Automakers are increasingly integrating smart technologies such as climate control, massage functions, and memory settings. The rapid expansion of electric and luxury vehicle production further fuels innovation in automotive seats design. Additionally, the emphasis on lightweight materials and sustainable manufacturing practices supports continued growth and competitiveness in the U.S. market.

Europe

In 2025, the Europe market stood at USD 16.28 Billion, representing 21.61% of global demand, and is projected to grow to USD 16.5 Billion in 2026. Europe is experiencing steady growth, driven by the region’s strong focus on innovation, sustainability, and the production of premium vehicles. Leading automakers are adopting eco-friendly materials, lightweight designs, and advanced ergonomics to meet stringent emission and safety standards. The increasing demand for electric and luxury vehicles is driving the integration of smart seating systems, which feature amenities such as massage, heating, and posture adjustment. Furthermore, the growing consumer awareness of interior comfort and rising investments in research and development are fostering continuous advancements in automotive seats technology across Europe.

The U.K. market is projected to reach USD 1.09 billion by 2026, while the Germany market is projected to reach USD 3.87 billion by 2026.

Rest of the World

In 2025, Rest of the World represented USD 3.51 Billion, accounting for 4.66% of the worldwide market, and is projected to grow to USD 3.57 Billion in 2026. The market growth in the rest of the world, including Latin America and the Middle East & Africa, is driven by increasing vehicle production, urbanization, and rising disposable incomes. Expanding demand for passenger vehicles and light commercial vehicles supports the adoption of comfortable and durable seating systems. Automakers are investing in localized manufacturing and affordable seat designs to cater to cost-sensitive consumers. Additionally, improvements in infrastructure, growing interest in electric vehicles, and a gradual shift toward modern interior designs are contributing to steady market development across these emerging regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Advancements in Materials and Technologies to Drive the Leadership of Key Players

The presence of major players, including Adient plc, Lear Corporation, FORVIA SE, Magna International Inc., and Toyota Boshoku Corporation, characterizes the competitive landscape. These companies focus on innovation, strategic partnerships, and product differentiation to strengthen their market position. Advancements in lightweight materials, modular designs, and smart seating technologies are key strategies driving market competition. Additionally, firms are expanding their global footprint, investing in sustainability, and enhancing manufacturing efficiency to meet evolving consumer preferences and regulatory requirements. They ensure long-term growth and profitability in a rapidly transforming automotive industry.

LIST OF KEY AUTOMOTIVE SEATS COMPANIES PROFILED

- Adient plc (U.S.)

- Lear Corporation (U.S.)

- Forvia SE (France)

- Toyota Boshoku Corporation (Japan)

- Magna International Inc. (Canada)

- TS Tech Co., Ltd. (Japan)

- NHK Spring Co., Ltd. (Japan)

- Recaro Automotive (Germany)

- Tachi-S Co., Ltd. (Japan)

- Brose Fahrzeugteile SE & Co. KG (Germany)

KEY INDUSTRY DEVELOPMENTS

- In February 2025, Lear Corporation announced its ComfortMax Seat engineering integration with General Motors beginning in Q2 2025, which incorporates new thermal comfort technology to better manage heating and ventilation in seat trim covers.

- In December 2024, Adient plc, Jaguar Land Rover (JLR) and Dow collaborated to develop a first-of-its-kind closed-loop recycled polyurethane seat-foam for premium vehicles, aiming to reduce CO₂ and support circular economy initiatives.

- In July 2024, FORVIA and BYD opened a new seat-assembly plant in Rayong, Thailand, with capacity to produce 180,000 complete seating sets annually for electric and hybrid models.

- In October 2023, Daechang Seat Corp. of South Korea announced a USD 72.5 million investment to build a new seat-frame plant in Georgia, U.S., creating more than 500 jobs and supporting Hyundai Motor Group’s nearby EV assembly facility.

- In September 2023, FORVIA unveiled the world’s first fossil-free steel seat structure via its partnership with SSAB. It reduces CO₂ footprint by nearly 90% compared with conventional steel structures and targeting full-scale production by 2026.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 2.62% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Position, By Distribution Channel, By Material, By Powertrain, By Type, By Technology, By Component, By Vehicle Type, and By Region |

| By Position |

|

| By Distribution Channel |

|

| By Material |

|

| By Powertrain |

|

| By Type |

|

| By Technology |

|

| By Component |

|

| By Vehicle Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 77.35 billion in 2026 and is projected to reach USD 95.13 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 41.18 billion.

The market is expected to exhibit a CAGR of 2.62% during the forecast period of 2026-2034.

The synthetic leather segment dominates the market by material.

Technological advancements associated with smart and connected seats are the key factors driving the market.

Key players in the market include Adient plc, Lear Corporation, FORVIA SE, Magna International Inc., and Toyota Boshoku Corporation.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us