Global Automotive Steer-by-Wire Actuator Market Size, Share & Industry Analysis, By Actuator Type (Steering Rack Actuators, Feedback / Road-Feel Actuators, and Redundant Backup Actuators), By Propulsion (ICE and Electric), By Automation Level (Semi-Autonomous Vehicles (Level 2 / Level 2+), Highly Automated Vehicles (Level 3), and Fully Autonomous Vehicles (Level 4 & Level 5)), By Actuation Technology (Electric Motor-Based Actuators, Electro-Hydraulic Actuators, and Purely Electromechanical Actuators), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

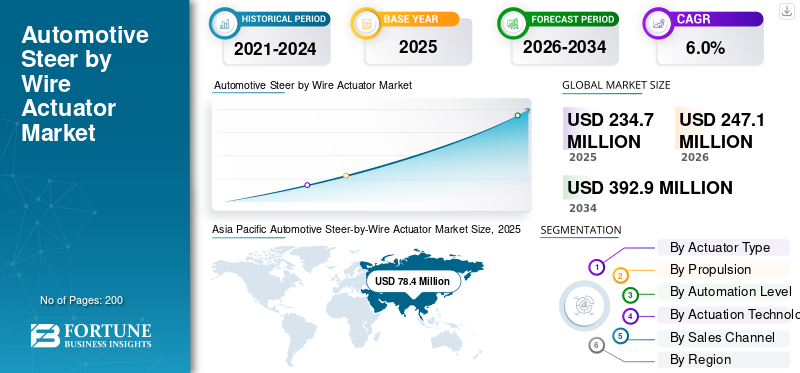

The global automotive steer-by-wire actuator market size was valued at USD 234.7 million in 2025. The market is projected to grow from USD 247.1 million in 2026 to USD 392.9 million by 2034, exhibiting a CAGR of 6.0% during the forecast period. Asia Pacific dominated the global automotive steer-by-wire actuator market with a market share of 33.4% in 2025.

The automotive steer-by-wire actuator market represents a rapidly evolving segment of the automotive industry, focusing on electronically controlled steering systems that eliminate the mechanical connection between the steering wheel and the wheels. In a steer by wire system, steering inputs are transmitted through electronic control units and actuators, allowing more precise and flexible steering response. This technology supports advanced vehicle architectures and plays a key role in efforts to improve vehicle handling, safety, and packaging efficiency.

Growth of the steer by wire actuator market is closely linked to the rising deployment of steer by wire technology in passenger cars, particularly in premium and luxury vehicles. Automakers are increasingly adopting electronic steering solutions to support modern cockpit layouts, reduce mechanical complexity, and enable software-based customization. In addition, rising production of autonomous and semi-autonomous vehicles has increased the importance of fully electronic steering systems that can interface seamlessly with braking and assistance system ADAS platforms.

Over the forecast period, the product adoption is expected to expand beyond high-end models as costs decline and regulatory frameworks mature. The global market will also benefit from growing safety requirements and increasing emphasis on redundancy and fail-safe steering architectures. Continuous innovation by key players such as ZF Friedrichshafen, Nexteer Automotive and Hyundai Mobis, including actuator miniaturization and integration with vehicle motion control software, will further accelerate adoption. As steering systems shift toward digital control, the automotive steer by wire ecosystem is expected to move steadily toward large-scale commercialization.

Download Free sample to learn more about this report.

AUTOMOTIVE STEER-BY-WIRE ACTUATOR MARKET TRENDS

Integration of Steer-by-Wire with ADAS and Centralized Vehicle Architectures Emerges as a Market Trend

A major trend is the integration of steer by wire technology with centralized vehicle computing and electronic control units. This enables tighter coordination between steering, braking, and ADAS functions. As software-defined vehicles become more common, steer-by-wire actuators gain importance as a core motion control interface.

- For instance, in February 2025, ZF confirmed that its steer-by-wire system includes redundant steering actuators, reflecting an industry trend toward fail-operational electronic steering designs.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Autonomous and Digitally Controlled Steering Systems Accelerates Market Growth

The growing deployment of autonomous and semi-autonomous vehicles is a major driver for the automotive steer-by-wire actuator market growth. These vehicles require fully electronic steering architectures that can interface with assistance system ADAS and motion control software. As automation levels increase, steer-by-wire actuators become essential for enabling precise, software-defined vehicle control, supporting steady market expansion.

- For instance, in 2024, Euro NCAP highlighted that advanced driver assistance functions increasingly rely on electronically controlled steering systems, reinforcing the importance of steer-by-wire architectures.

MARKET RESTRAINTS

High System Cost and Safety Validation Complexity Limit Near-Term Adoption

The high cost of steer-by-wire actuators and extensive safety validation requirements restrain rapid adoption. Redundant actuators, backup power, and advanced software increase system cost, limiting penetration beyond premium segments. These challenges slow deployment in mass-market passenger cars, despite long-term potential in the global market.

- For instance, UNECE regulations emphasized strict functional safety and redundancy requirements for electronic steering systems, increasing development time and compliance costs for steer-by-wire solutions.

MARKET OPPORTUNITIES

Expansion of Steer-by-Wire Beyond Luxury Vehicles Creates New Growth Potential

As component costs decline, steer-by-wire adoption is expected to expand beyond luxury vehicles into mid-segment models. OEMs seeking flexible vehicle platforms and advanced safety integration consider steer-by-wire as a long-term solution. This creates strong growth opportunities in the market during the forecast period, particularly in high-volume vehicle segments.

- For instance, in January 2024, ZF stated that software-defined vehicle architectures require fully electronic steering systems, creating long-term opportunities for steer-by-wire actuators across future vehicle platforms.

MARKET CHALLENGES

Regulatory Acceptance and Consumer Trust Remain Key Market Challenges

Gaining regulatory approval and consumer trust remains challenging due to the removal of the mechanical steering column. Concerns around fail-safe performance and cybersecurity slow adoption. Overcoming these issues requires extensive testing and education, potentially delaying the large-scale deployment of automotive steer by wire systems.

- For instance, in 2024, the U.S. NHTSA noted that public confidence and regulatory validation remain critical challenges for advanced electronic steering systems without mechanical fallback.

Download Free sample to learn more about this report.

Segmentation Analysis

By Actuator Type

Steering Rack Actuators Dominate Due to Structural Importance in Vehicle Control

On the basis of actuator type, the market is divided into steering rack actuators, feedback / road-feel actuators and redundant backup actuators.

Steering rack actuators held the largest automotive steer-by-wire actuator market share, as they directly transmit driver input to wheel movement. Their role in handling, alignment, and stability across passenger cars and light commercial vehicles sustains consistent demand.

- For instance, in February 2025, ZF confirmed series steer-by-wire production for NIO ET9, supplying a redundant steering gear actuator at the rack plus software, showing rack actuators’ central role.

To know how our report can help streamline your business, Speak to Analyst

Redundant backup actuators segment is expected to grow at a CAGR of 8.2% over the forecast period.

By Propulsion

ICE Vehicles Dominate Due to Larger Installed Base

On the basis of propulsion, the market is segmented into ICE and electric.

ICE vehicles dominate as they represent the majority of vehicles on the road. Steer-by-wire integration is initially focused on premium ICE models.

- For instance, the IEA stated that electric cars exceeded 20% of global new-car sales in 2024, implying that newest vehicles remain ICE/hybrids, supporting near-term ICE-led volumes.

Electric segment is expected to grow at a CAGR of 7.4% over the forecast period.

By Automation Level

Integration of Electronic Steering with ADAS Features Drives Semi-Autonomous Vehicles Segment Growth

On the basis of automation level, the market is segmented into semi-autonomous vehicles (level 2 / level 2+), highly automated vehicles (level 3), and fully autonomous vehicles (level 4 & level 5).

Semi-autonomous vehicles dominate as they increasingly integrate electronic steering with ADAS features, supporting near-term steer-by-wire deployment.

- For instance, in May 2023, the U.S. Bureau of Transportation Statistics published “New Car and Light Truck Sales by Levels of Driving Automation,” showing that Level 0–2 driver-assist systems dominate recorded sales.

Fully autonomous vehicles (Level 4 & Level 5) segment is expected to grow at a CAGR of 8.5% over the forecast period.

By Actuation Technology

Electromechanical Actuators Dominate Due to Simplicity and Efficiency

On the basis of actuation technology, the market is segmented into electric motor-based actuators, electro-hydraulic actuators and purely electromechanical actuators.

Electromechanical actuators segment dominates the market due to their lower complexity and easier integration with vehicle electronics compared to hybrid systems.

- February 2025: ZF’s NIO ET9 steer-by-wire supply includes a steering wheel actuator and a redundant steering gear actuator with software, an explicitly actuator-driven, electromechanical steering approach.

Purely electromechanical actuators segment is expected to grow at a CAGR of 7.2% over the forecast period.

By Sales Channel

OEM Channel Dominates Through Platform-Level Integration

On the basis of sales channel, the market is segmented into OEM and Aftermarket.

OEMs dominate the market, as steer-by-wire must be integrated during the vehicle design stage to meet safety and regulatory requirements.

- For instance, in October 2025, Nexteer announced its Direct Drive Hand Wheel Actuator for steer-by-wire, positioning it for automakers’ next-generation platforms, showing SbW actuators are primarily integrated through OEM vehicle programs.

Aftermarket segment is expected to grow at a CAGR of 7.5% over the forecast period.

Automotive Steer-by-Wire Actuator Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Steer-by-Wire Actuator Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the automotive steer-by-wire actuator market, due to high vehicle production, increasing adoption of technology, and strong presence of steering system suppliers. Countries such as China, Japan, and South Korea are actively investing in steer by wire technology to support autonomous and semi-autonomous vehicles and advanced safety functions. Growing demand for intelligent steering solutions in passenger cars, along with expanding electronics manufacturing capabilities, continues to strengthen the region’s position in the global market.

- For instance, Japanese and Chinese automakers are actively developing electronic steering systems to support next-generation vehicle platforms.

North America

North America is expected to witness steady growth driven by early adoption of advanced vehicle technologies and strong ADAS penetration. The U.S. plays a key role due to active testing of autonomous vehicles and close collaboration between OEMs and technology suppliers. Increasing focus on electronically controlled steering systems supports gradual expansion of the automotive steer-by-wire actuator market.

Europe

Europe’s market growth is supported by premium vehicle manufacturing and strict vehicle safety regulations. Automakers emphasize advanced steering solutions to improve driving dynamics and integrate automation features. Strong engineering capabilities and supplier presence further reinforce adoption of automotive steer by wire systems.

Rest of the World

The rest of the world displays gradual growth as steer-by-wire adoption remains limited to high-end imports and pilot automation programs. As regulatory frameworks evolve and costs decline, long-term opportunities are expected to emerge across selected markets.

COMPETITIVE LANDSCAPE

Key Industry Players

System Integration, OEM Collaboration, and Safety Validation Define Competition

The competitive landscape of the global automotive steer-by-wire actuator market is currently shaped by a small group of technologically advanced suppliers with strong system integration capabilities. These companies operate at the intersection of steering hardware, software, and electronic control units, making high R&D investment a core competitive requirement. Leading suppliers focus on delivering complete steer by wire system solutions rather than standalone components.

Major players such as ZF Friedrichshafen AG and Nexteer Automotive leverage long-term relationships with global OEMs to co-develop steering platforms for next-generation vehicles. Competitive advantage is built through early involvement in vehicle development programs, allowing suppliers to tailor actuators and control logic to specific platform needs. This approach strengthens entry barriers and reinforces supplier positions across the global automotive steer ecosystem.

Another key strategy is investment in redundancy and safety validation. Since steer-by-wire removes mechanical fallback, suppliers prioritize dual-motor actuators, backup power supply integration, and software fail-safe mechanisms. These features are crucial for securing regulatory approvals and gaining OEM trust, particularly for autonomous and semi-autonomous vehicles. Companies are also aligning their product roadmaps with ADAS and automated driving timelines to remain relevant as vehicle automation advances.

Geographic expansion also plays a key role, with suppliers strengthening engineering and testing capabilities in Asia, Europe, and North America to support global OEM programs. As adoption grows beyond luxury vehicles, scale, reliability, and cost optimization will increasingly define competitive success in the steer by wire market.

- For instance, in June 2024, ZF strengthened its steering components portfolio by expanding chassis system production to support OEM demand for durable ball joints and steering linkages.

LIST OF KEY AUTOMOTIVE STEER-BY-WIRE ACTUATOR COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Nexteer Automotive (U.S.)

- Robert Bosch GmbH (Germany)

- JTEKT Corporation (Japan)

- NSK Ltd. (Japan)

- Hitachi Astemo (Japan)

- Denso Corporation (Japan)

- Hyundai Mobis (South Korea)

- Continental AG (Germany)

- Schaeffler AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Nexteer introduced its Direct Drive Hand Wheel Actuator (DD-HWA) for steer-by-wire. The company positioned it to improve steering feel, packaging flexibility, and integration for software-defined vehicles across assisted and automated driving levels.

- October 2025: JTEKT announced its steer-by-wire system and Libuddy backup power supply were installed in the Lexus RZ. The high-heat-resistant energy device supports steering availability as a safety-critical fallback power source.

- September 2025: Schaeffler stated that it is advancing steer-by-wire by using a Hand Wheel Actuator with integrated force feedback. It presented the technology as part of its broader software-defined vehicle integration platform at the IAA Mobility event.

- March 2025: Lexus revealed the new 2025 RZ, featuring its first application of a steer-by-wire system. Lexus linked the update to improvements in driving engagement alongside broader BEV system upgrades and performance enhancements.

- February 2025: ZF announced the start of series production for steer-by-wire with NIO’s ET9. ZF supplies the steering wheel actuator, a redundant steering gear actuator, and related software removing the mechanical link between steering input and wheels.

REPORT COVERAGE

The global automotive steer-by-wire actuator market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.0% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Actuator Type, Propulsion, Automation Level, Actuation Technology, Sales Channel and Region |

|

By Actuator Type |

· Steering Rack Actuators · Feedback / Road-Feel Actuators · Redundant Backup Actuators |

|

By Propulsion |

· ICE o Hatchback/Sedan o SUVs o Light Commercial Vehicles (LCVs) o Heavy Commercial Vehicles (HCVs) · Electric o Hatchback/Sedan o SUVs o Light Commercial Vehicles (LCVs) o Heavy Commercial Vehicles (HCVs) |

|

By Automation Level |

· Semi-Autonomous Vehicles (Level 2 / Level 2+) · Highly Automated Vehicles (Level 3) · Fully Autonomous Vehicles (Level 4 & Level 5) |

|

By Actuation Technology |

· Electric Motor-Based Actuators · Electro-Hydraulic Actuators · Purely Electromechanical Actuators |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Geography |

· North America (By Actuator Type, Propulsion, Automation Level, Actuation Technology, Sales Channel and Country) o U.S. o Canada o Mexico · Europe (By Actuator Type, Propulsion, Automation Level, Actuation Technology, Sales Channel and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Actuator Type, Propulsion, Automation Level, Actuation Technology, Sales Channel and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Actuator Type, Propulsion, Automation Level, Actuation Technology, Sales Channel and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 234.7 million in 2025 and is projected to reach USD 392.9 million by 2034.

In 2025, the Asia Pacific market value stood at USD 78.4 Million.

The market is expected to exhibit a CAGR of 6.0% during the forecast period of 2026-2034.

Steering rack actuators segment is leading the market by actuator type.

Rising demand for autonomous and digitally controlled steering systems are the key factors driving the market.

Bosch, ZF Friedrichshafen, Schaeffler and Nexteer are some of the top players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us