Automotive Thermal Management System Market Size, Share & Industry Analysis, By Thermal System Type (Powertrain Thermal Management System, Battery Thermal Management System (BTMS), Cabin HVAC Thermal System, and Integrated/Centralized Thermal Management System), By Vehicle Type (Passenger Cars, LCVs, and HCVs), By Technology Type (Air-based Thermal Management, Liquid-based Coolant Systems, Refrigerant-based Cooling Systems, and Phase Change Material (PCM)-based Systems), By Component Type (Compressors, Heat Exchangers, Pumps, Valves & Manifolds, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

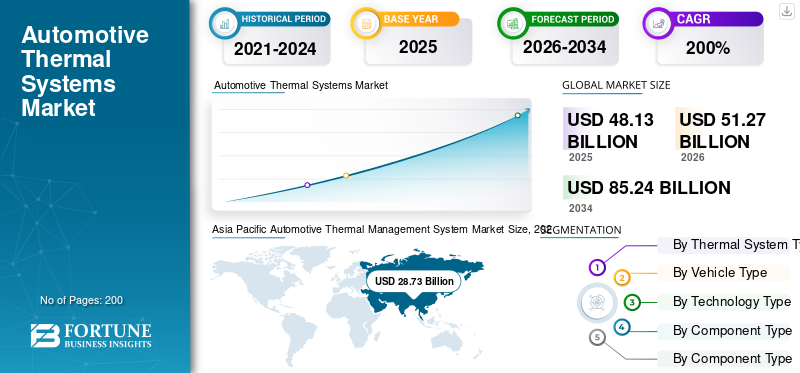

The global automotive thermal management system market size was valued at USD 48.13 billion in 2025. The market is projected to grow from USD 51.27 billion in 2026 to USD 85.24 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period. Asia Pacific dominated the automotive thermal management system market with a market share of 59.69% in 2025.

An Automotive Thermal Management System (ATMS) is an integrated set of components and controls that manages heat across a vehicle’s powertrain, battery, electronics, and cabin. It maintains optimal operating temperatures to improve efficiency, safety, performance, durability, charging capability, and passenger comfort under varying driving and climate conditions. The global market growth is driven by the rapid adoption of EVs and hybrids, which increases the demand for battery thermal management, liquid-cooling loops, and refrigerant-based chillers. Faster charging, higher-power-density electronics, and heat-pump HVAC also increase thermal complexity. Stricter efficiency and emissions rules, extreme climate exposure, and greater use of centralized, software-controlled architectures further accelerate system value per vehicle.

Major players include Bosch, Denso, Continental, Marelli, Aisin, Hitachi Astemo, and Delphi Technologies (BorgWarner). Trends include high-pressure GDI upgrades, improved injectors and pumps for greater efficiency and lower emissions, integration with engine management software, and a growing focus on hybrid-compatible fuel economy systems as pure-EV growth gradually limits long-term ICE volumes.

Download Free sample to learn more about this report.

Automotive Thermal Management System Market Key Takeaways

- 2025 Market Size: USD 48.13 billion

- 2026 Market Size: USD 51.27 billion

- 2034 Forecast Market Size: USD 85.24 billion

- CAGR: 6.6% from 2026–2034

- Asia Pacific dominated the automotive thermal management system market with a 59.69% share in 2025.

- The powertrain thermal management systems segment held the largest market share in 2025.

- The passenger cars segment accounted for the leading market share in 2025.

Asia Pacific

Asia Pacific led the global market with USD 28.73 billion in 2025, driven by strong vehicle production and rapid electrification.

North America

North America witnessed steady growth supported by rising EV adoption and demand for advanced HVAC and battery cooling systems.

Europe

Europe maintained a significant market presence due to stringent emissions regulations and growing deployment of heat-pump and battery cooling technologies.

U.S.

The market was valued at USD 6.82 billion in 2025, supported by strong EV and hybrid vehicle adoption.

Japan

The market reached USD 3.96 billion in 2025, driven by demand for efficient powertrain cooling and thermal components.

Read More

AUTOMOTIVE THERMAL MANAGEMENT SYSTEM MARKET TRENDS

Integrated Heat-Pump Thermal Modules to Accelerate Platform-Level Consolidation

Automakers are moving from separate cooling and heating ventilation and air conditioning HVAC circuits toward integrated thermal supermodules that centrally manage battery, e-axle, and cabin heat flows. This trend is the strongest in EV platforms where reducing hose routing, components, and control complexity improves packaging and boosts cold-weather range. Centralized architectures also enable smarter heat sharing (e.g., using waste heat from power electronics) and faster calibration across vehicle variants, helping OEMs standardize thermal systems across multiple models. For suppliers, the shift favors higher-value assemblies that bundle compressors, heat exchangers, pumps, valves, sensors, and embedded controls into fewer modules, raising content per vehicle and increasing the importance of software in thermal optimization. In September 2025, MAHLE presented a compact thermal management module with an integrated heat pump to improve EV range in cold conditions.

MARKET DYNAMICS

MARKET DRIVERS

EV Range Preservation and Fast-Charging Needs to Push Thermal Content Higher

Vehicle electrification sharply increases thermal requirements as batteries, inverters, and motors must operate within narrow temperature bands to protect safety and performance. As fast charging becomes a mainstream expectation, heat rejection loads rise, accelerating the adoption of liquid engine cooling, refrigerant-based chillers, and more intelligent valve control, auguring well for automotive thermal management system market growth. At the same time, EV cabin heating can materially impact range, driving OEMs to adopt efficient HVAC concepts (heat pumps, zonal comfort strategies, and advanced air management) to reduce energy draw in winter. These shifts increase the average thermal bill of materials per vehicle and push suppliers to deliver integrated, energy-optimized systems rather than standalone components.

- In September 2025, Valeo announced new contracts to supply its Dual Layer HVAC system to a leading Chinese automaker, highlighting OEM demand for higher-efficiency cabin thermal solutions.

MARKET RESTRAINTS

Refrigerant Regulation Tightens Design Choices and Raises Compliance Burden

Thermal management systems increasingly rely on refrigerant circuits for heat pump operation and battery cooling. However, regulatory limits on fluorinated gases impose engineering and cost constraints. Compliance can require redesigning components, changing refrigerants, updating service procedures, and retraining technicians, especially challenging for global platforms sold across regions with different rules. Suppliers also face validation efforts for durability, leakage control, and performance under varied climates, while OEMs must manage transition timelines without disrupting production. This can slow the adoption of specific architectures, increase qualification costs, and create uncertainty about the refrigerant strategy for next-generation EV heat pumps.

- In October 2024, the European Contractors Association AREA published a practical guide explaining obligations and impacts of the EU F-Gas Regulation (EU) 2024/573 for refrigeration, air-conditioning, and heat-pump systems.

MARKET OPPORTUNITIES

Multi-Function Valves Create a Clear Path to Lower Cost and Higher Reliability

As EV thermal systems become more complex, a significant opportunity is to simplify architectures while maintaining high performance. Multi-function refrigerant valves and integrated manifolds can replace several discrete solenoids and check valves, cutting parts, wiring, leak points, and assembly time. Fewer components can improve reliability, reduce weight, and free up packaging space, benefits that matter as OEMs scale EVs into high-volume segments. This also supports faster platform rollouts as modular thermal blocks can be reused across models with software tuning rather than hardware redesign.

- In November 2025, Valeo announced that its compact 5-ways refrigerant valve for EV heat-pump systems was named a CES Innovation Awards 2026 honoree, underscoring the industry's focus on simplifying EV thermal architectures.

MARKET CHALLENGES

Margin Pressure and Capital Intensity to Challenge Suppliers during EV Transition

Even as content per vehicle rises, suppliers face a tough challenge. Thermal systems are becoming more electronics and software heavy while OEMs continue to demand aggressive cost reductions. Scaling new EV thermal products often requires capital for new lines, tooling, unobstructed supply chains, and validation. At the same time, legacy ICE volumes can be volatile, creating a problematic mix of investment needs and pricing pressure. In addition, warranty risk grows as integrated systems become more complex, raising the cost of quality and field support. This combination can strain balance sheets and force the prioritization of programs with more substantial margins or long-term platform commitments.

- In September 2025, Hanon Systems announced that its board had approved a rights offering totaling approximately KRW 900 billion to strengthen financial stability and support long-term growth funding.

Download Free sample to learn more about this report.

Segmentation Analysis

By Thermal System Type

Powertrain Segment Leads with Extensive Presence across Electric, ICE, and Hybrid Vehicles

Based on thermal system type, the market is segmented into powertrain thermal management systems, Battery Thermal Management Systems (BTMS), cabin HVAC thermal systems, and integrated/centralized thermal management systems.

The powertrain thermal management systems segment dominates the global market due to their universal presence across ICE, electric, and hybrid vehicles. Engines, transmissions, electric motors, and inverters require continuous and reliable temperature control to ensure efficiency, durability, and regulatory compliance. Even as electrification rises, power electronics cooling and e-axle thermal control sustain high increased demand.

- In March 2025, Bosch announced the expanded production of advanced power electronics cooling solutions for electric drivetrains in China, reinforcing continued powertrain thermal demand.

The Battery Thermal Management System (BTMS) segment is projected to grow at a CAGR of 9.9% over the forecast period, driven by EV safety and fast-charging requirements.

By Vehicle Type

High Passenger Vehicle Volumes to Foster Passenger Cars Segmental Dominance

Based on vehicle type, the market is segmented into passenger cars, LCVs, and HCVs.

The passenger cars segment dominates the automotive thermal management system market share due to their significantly higher global production volumes and growing thermal complexity. Rising EV penetration, enhanced cabin comfort features, expectations, and stricter efficiency norms increase thermal content per passenger vehicle.

However, light commercial vehicles are witnessing the rapid adoption of electrified powertrains for last-mile delivery, boosting the demand for advanced battery and power electronics cooling. The LCV segment is projected to grow at a CAGR of 7.6% over the forecast period, outpacing other vehicle categories.

- In June 2024, Ford confirmed the expansion of electric van production capacity in Europe to meet commercial fleet demand, increasing thermal system integration needs.

To know how our report can help streamline your business, Speak to Analyst

By Technology Type

Liquid-based Coolant Systems Segment Dominates with Superior Heat Transfer Efficiency

Based on technology type, the market is segmented into air-based thermal management, liquid-based coolant systems, refrigerant-based cooling systems, and Phase Change Material (PCM)-based systems.

The liquid-based coolant systems segment dominates the market due to their superior heat transfer efficiency, scalability, and suitability for both ICE and electrified vehicles. They are essential for engines, batteries, motors, and inverters, particularly under high-load and fast-charging conditions.

Refrigerant-based cooling systems are rapidly gaining adoption in EVs, enabling efficient battery chilling and heat-pump HVAC integration. The refrigerant-based cooling systems segment is projected to grow at a CAGR of 8.3% over the forecast period.

- In September 2024, Toyota announced the wider deployment of refrigerant-based battery cooling in next-generation EV platforms to support higher charging rates.

By Component Type

Heat Exchangers Lead with Mounting Adoption across Multiple Thermal Loops

Based on component type, the market is segmented into compressors, heat exchangers, pumps, valves & manifolds, and thermal modules & control units.

The heat exchangers segment dominates the global market as they are used across multiple thermal loops, including radiators, condensers, evaporators, chillers, and heater cores. Their universal applicability across vehicle types and propulsion systems propels high-volume demand.

Meanwhile, increasing system integration and multi-loop architectures are driving the rapid adoption of intelligent valves and manifolds. The valves & manifolds segment is projected to grow at a CAGR of 7.9% over the forecast period.

- In November 2025, Continental unveiled an innovative multi-way coolant valve designed to optimize EV thermal efficiency and reduce system complexity.

AUTOMOTIVE THERMAL MANAGEMENT SYSTEM MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Thermal Management System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest and fastest-growing region, driven by massive vehicle production volumes and rapid electrification. China’s EV dominance, rising adoption of electric two- and four-wheelers, and expanding commercial vehicle electrification significantly boost the demand for BTMS, liquid cooling, and integrated thermal systems. Cost optimization, localized manufacturing, and scaling thermal management technologies further strengthen the regional growth momentum.

China Automotive Thermal Management System Market

China dominated with a 60.4% share within Asia Pacific in 2025, driven by the world’s largest EV market and aggressive fast-charging deployment. The high adoption of liquid and refrigerant-based battery cooling, centralized thermal systems, and advanced HVAC drives strong growth in thermal system value per vehicle.

Japan Automotive Thermal Management System Market

The Japan market growth is steady, supported by hybrid and electrified powertrains and high engineering standards. The demand remains strong for efficient powertrain cooling, compact heat exchangers, and high-reliability thermal components. The Japan market was valued at USD 3.96 billion in 2025.

India Automotive Thermal Management System Market

India is a high-growth market with a CAGR of 8.2% over the forecast period, as vehicle production expands and electrification accelerates across passenger cars, buses, and LCVs. Rising climate-control needs and EV adoption increase the demand for scalable, cost-efficient thermal systems.

North America

North America represents a mature yet steadily growing market, supported by rising electrification, larger vehicle sizes, and strong demand for advanced HVAC and power-electronics cooling. EV adoption in passenger cars and commercial fleets is increasing thermal content per vehicle, particularly for battery cooling and heat-pump systems. Stringent fuel-efficiency regulations and extreme climate conditions further drive the demand for robust, high-performance thermal architectures, sustaining consistent market expansion across the region.

U.S. Automotive Thermal Management System Market

The U.S. drives regional market growth through high vehicle production, rapid adoption of EVs and hybrids, and intense penetration of large SUVs and pickup trucks. These vehicles require higher-capacity cooling, advanced HVAC, and increasingly battery thermal systems. The expansion of electric passenger cars and delivery vans continues to raise the average thermal system value per vehicle. The U.S. market was valued at USD 6.82 billion in 2025.

Europe

Strict emissions regulations, high EV penetration, and a strong focus on energy efficiency are shaping Europe’s market growth. Automakers increasingly adopt heat pumps, integrated thermal modules, and refrigerant-based battery cooling to optimize range and reduce emissions. Although vehicle production growth is moderate, rising thermal complexity per vehicle, especially in the electric and premium segments, supports steady market expansion across Western and Central Europe.

U.K. Automotive Thermal Management System Market

The U.K. market benefits from strong EV adoption and policy support for electrification. The growing production of electric passenger cars and vans increases the demand for BTMS, heat-pump HVAC, and compact integrated thermal solutions, particularly for urban mobility and fleet vehicles. The U.K. market was valued at USD 1.08 billion in 2025.

Germany Automotive Thermal Management System Market

Germany remains a key contributor, with a 29.1% share within Europe in 2025, due to its strong OEM base and high concentration of premium and performance vehicles. Advanced powertrain cooling, battery thermal systems, and integrated thermal architectures are widely deployed, supporting higher-than-average thermal content per vehicle.

Rest of the World

The rest of the world shows moderate but improving growth, supported by a gradual increase in vehicle production, expanding electrification, and rising demand for cabin comfort in warm climates. ICE vehicles still dominate, keeping powertrain cooling and HVAC demand strong, while EV adoption slowly lifts BTMS and integrated system uptake over the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Introduce Advanced Products to Stay Ahead of Competitors

The global automotive thermal management system market depicts rapid electrification, rising system integration, and increasing demand for energy-efficient cooling and heating solutions. Leading players such as Denso, Valeo, Hanon Systems, MAHLE, Bosch, Continental, Marelli, Modine, and BorgWarner compete through advanced battery thermal management systems, heat-pump HVAC, integrated thermal modules, and smart valves and control software. Suppliers focus on centralized architectures that combine powertrain, battery, and cabin thermal functions to reduce weight, cost, and energy losses. Competitive strength is enhanced through platform-level collaborations with OEMs, investments in EV-focused R&D, expansion of localized manufacturing, and partnerships with refrigerant, semiconductor, and software specialists. Companies are also leveraging digital simulation, predictive thermal control, and software-defined strategies to optimize performance across climates and driving conditions.

- In October 2025, MAHLE announced new integrated thermal management solutions for electric vehicle platforms aimed at improving fast-charging capability and cold-weather range, reinforcing the shift toward high-value, system-level competition.

LIST OF KEY AUTOMOTIVE THERMAL MANAGEMENT SYSTEM COMPANIES PROFILED

- Denso Corporation (Japan)

- Valeo SA (France)

- Hanon Systems (South Korea)

- MAHLE GmbH (Germany)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Modine Manufacturing Company (U.S.)

- BorgWarner Inc. (U.S.)

- Dana Incorporated (U.S.)

- Sanden Holdings Corporation (Japan)

- Marelli Holdings Co., Ltd. (Japan)

- Zhejiang Yinlun Machinery Co., Ltd. (China)

- Webasto SE (Germany)

- Vitesco Technologies (Germany)

- Gentherm Incorporated (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Gentherm and Modine announced a definitive agreement to combine Modine’s Performance Technologies business with Gentherm, creating a scaled thermal-management leader. The transaction strengthens Gentherm’s position as a scaled leader across thermal solutions and accelerates platform-level integration capabilities relevant to EV and ICE applications.

- January 2026: Valeo highlighted at CES 2026 how it is democratizing electrification through optimized architectures and innovative thermal-management systems, emphasizing affordability alongside range and efficiency. The focus reflects OEM demand for compact, integrated thermal solutions that reduce energy losses and improve real-world usability across climates.

- December 2025: Marelli unveiled its Intelligent Energy Management solution at CTI Europe 2025, using proprietary software, to coordinate thermal, propulsion, and electronics energy domains. The modular approach is designed to integrate with vehicle and zonal controllers, enabling more efficient thermal flows and improved vehicle-level energy optimization for hybrids and EVs.

- October 2025: DENSO announced newly developed electrification products adopted for Toyota’s updated bZ4X, targeting improved energy efficiency, performance, and reduced charging time. Such upgrades reinforce the growing interdependence of battery management, power electronics, and thermal-control strategies needed to sustain fast charging and stable operating temperatures.

- September 2025: BorgWarner showcased next-generation thermal modules alongside heating and thermal management technologies at IAA Mobility 2025, positioning them to improve energy efficiency in hybrid and battery-electric architectures. The exhibit underscored the supplier's emphasis on integrated subsystems that reduce losses, maintain stable component battery temperatures and enhance cabin comfort across diverse duty cycles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.6% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Thermal System Type, By Vehicle Type, By Technology Type, By Component Type, and By Region |

| By Thermal System Type |

|

| By Vehicle Type |

|

| By Technology Type |

|

| By Component Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 48.13 billion in 2025 and is projected to reach USD 85.24 billion by 2034.

In 2025, the market value stood at USD 28.73 billion.

The market is expected to grow at a CAGR of 6.6% during the forecast period from 2026 to 2034.

The passenger cars segment leads the market by vehicle type.

EV range preservation and fast-charging needs are key factors driving the market.

Key market players include Bosch, Denso, Continental, Marelli, Aisin, Hitachi Astemo, and Delphi Technologies.

Asia Pacific accounts for the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us