Automotive Trailer Market Size, Share & Industry Analysis, By Trailer Type (Low Boy, Flat Bed, Dry Van, Refrigerated, and Tanker), By Number of axles (Single axle, and Multi axles), By Length (Upto 7 m, 7 to 13.6 m, and More than 13.6 m), By Tonnage (Upto 3.5 tons, 3.5 to 10 tons, and More than 10 tons), By Application (Construction, Industrial, Agriculture, Mining, and Port), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

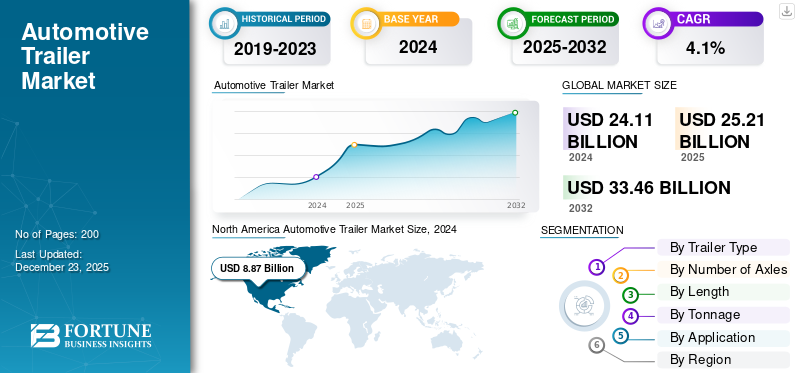

The global automotive trailer market size was valued at USD 25.21 billion in 2025 and is projected to grow from USD 26.30 billion in 2026 to USD 35.86 billion by 2034, exhibiting a CAGR of 3.95% during the forecast period.

Automotive trailers are non-motorized vehicles designed to be towed by motorized vehicles, primarily trucks or tractors, to transport goods, equipment, or even vehicles themselves. They play a vital role in logistics, construction, agriculture, mining, and industrial applications, enabling efficient movement of heavy and bulk loads over long distances. Trailers come in different forms, such as flatbeds, dry vans, refrigerated units, low boys, and tankers, each suited for specific cargo types. With varying capacities, lengths, and axle configurations, they significantly enhance freight transport flexibility, reduce logistics costs, and support global supply chain efficiency.

The global market trends have experienced consistent growth driven by rising freight demand, construction projects, and the expansion of agricultural and mining activities. Increasing international trade and infrastructure development, especially in Asia Pacific and North America, further strengthen trailer adoption. Innovations in lightweight materials, fuel efficiency, and safety regulations shape the market. Key global players include Great Dane, Utility Trailer, Wabash National, Hyundai Translead, Schmitz Cargobull, Krone, Kogel, CIMC Vehicles, Fliegl, Tirsan Treyler, Lecitrailer, Manac, Stoughton, and Faymonville. These manufacturers dominate dry van, flatbed, refrigerated, tanker, and low-boy segments, ensuring strong competition and technological advancement across regions.

The COVID-19 pandemic caused significant short-term disruptions in the market share, with supply chain breakdowns, factory shutdowns, and a decline in freight movement during 2020. Border restrictions and reduced industrial output slowed demand for construction, mining, and port trailers. However, the crisis also accelerated demand for refrigerated trailers to support the pharmaceutical and food cold chain sectors. Post-2021, as trade and industrial activity recovered, trailer demand rebounded strongly, particularly in e-commerce logistics, essential goods transportation, and infrastructure-driven sectors, positioning the market back on its long-term growth trajectory.

Download Free sample to learn more about this report.

Automotive Trailer Market Trends

Increasing Demand for Rapid Decarbonization of Refrigerated Trailers is a Market Trend

Shifting from diesel units to battery-electric, e-axle–assisted, and hybrid power, California now requires fleets to convert at least 15% of truck TRUs to zero-emission each year from December 31, 2023, ramping annually so that all TRUs operating in the state must be zero-emission by December 31, 2029. Manufacturers and fleets are responding at pace. Schmitz Cargobull has begun series rollouts of its all-electric S.KOe COOL, including deliveries to LC3 for Lidl in Italy and a formal UK & Ireland launch, pairing a battery with an e-axle generator to power the fridge independently of the tractor.

In North America, Thermo King is expanding fully electric trailer refrigeration solutions and partnering with technology players such as Range Energy to accelerate adoption across fleets. In the U.S., the USDA reports 3.70 billion cubic feet of refrigerated warehouse capacity as of October 1, 2023, evidence of a deepening cold chain that multiplies reefer-trailer duty cycles and emissions-reduction opportunities. Structural demand tailwinds reinforce this shift; the EU’s road freight share reached a decade high of 25.3% (1,807 billion tonne-km) in 2023, underscoring the scale of over-the-road cooling to decarbonize.

Technology is maturing quickly: e-axles that recuperate energy to the trailer battery, high-efficiency insulation, and intelligent power management are moving from pilots into mainstream specifications, while end users in grocery and parcel cold chains deploy at scale to meet corporate ESG targets and impending refrigerant restrictions. Together, regulation, OEM innovation, and freight fundamentals are locking in a multi-year electrification cycle for TRU-equipped trailers globally.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Surge In E-Commerce and Omnichannel Retail Drives Market Growth

A major demand driver is the surge in e-commerce and omnichannel retail, which is structurally lifting the need for dry-van and refrigerated trailers across regions. In the U.S., government data show e-commerce sales reached USD 1.1926 trillion in 2024, accounting for 16.1% of total retail, and continued to grow in 2025 with Q2 online sales at USD 304.2 billion volumes that translate directly into higher trailer turns, more drop-and-hook operations, and larger retailer private fleets.

EU road freight totaled 1,869 billion ton-kilometres in 2024, up 0.6% year-on-year, with food and beverages the largest goods categorysupporting persistent reefer-trailer utilization. Manufacturers and end users are investing to capture this flow. Utility Trailer opened a new facility in Eagle Pass, Texas, in June 2024 to support Cargobull North America TRU assembly, tightening the reefer technology supply chain near a key cross-border corridor.

CIMC Vehicles, one of the world’s largest trailer builders, reported USD 2.94 billion in 2024 revenue, underscoring the scale of OEM activity linked to logistics demand. Retailers are also pushing equipment innovation. Walmart piloted battery-electric TRU refrigerated trailers with Thermo King as part of its net-zero strategy, a signal that big fleets are expanding reefer capacity while decarbonizing high-growth e-grocery lanes. Together, these data points capture a reinforcing loop: rising online order density increases warehouse nodes and middle-mile shuttles; grocers’ cold-chain commitments expand reefer duty cycles; and OEMs respond with localized production and new tech. The result is a durable, multi-year pull for trailer capacity, specifications, and services aligned to retail logistics.

Market Restraints

Tightening of Regulatory Emission Standards and Associated Compliance Costs are Restraining Market Growth

The tightening of regulatory emissions standards and associated compliance costs increasingly challenge manufacturers and end users. Governments globally are adopting more stringent regulations to reduce greenhouse gas emissions, fuel consumption, and air pollutants from heavy-duty vehicles. In the European Union, the upcoming Euro VII standards will impose tighter limits on engine and exhaust emissions for trucks and tractors, which in turn elevate the technological and material requirements for tractor-trailer combinations, raising production costs. Similarly, in the U.S., the EPA’s proposed greenhouse gas (GHG) Phase 3 standards mandate lower CO₂ emissions beginning in 2027, forcing OEMs to accelerate powertrain enhancements. These elevated costs, whether for advanced aerodynamic trailer designs, lightweight composite materials, or integration of electric systems, are often passed to buyers, reducing demand in cost-sensitive segments such as agriculture and small-fleet operators.

During 2024, manufacturing executives reported that the introduction of new emission-related component testing and certification protocols increased R&D and production expenditures by upwards of 5–8%, squeezing profit margins. Additionally, regulatory uncertainty around the pace of heavy vehicle electrification makes many fleet owners hesitant to invest in additional new fleet assets when they are unsure about the useful life of those trailers. In markets such as Latin America and parts of Asia, where infrastructure and regulatory frameworks are still evolving, this hesitance is more pronounced. The compounded effect is that, while large fleets and OEMs may absorb these compliance costs, smaller operators and emerging markets face delayed adoption or outright hesitation in purchasing new automotive trailers, thereby restraining unit sales and slowing overall market momentum on a global scale.

Market Opportunities

Electrification of Trailer Subsystems is a Transformative Opportunity for Market

A very large near-term opportunity in the global automotive trailer market growth is the electrification of trailer subsystems, particularly refrigerated trailer units (TRUs) and auxiliary power via integrated e-axles, battery packs, and smart energy management, which unlocks new value for manufacturers, fleets, and cold-chain end users. Stricter zero-emission mandates are forcing fleet operators and retailers to replace diesel power with electric TRUs, creating immediate demand for electric-enabled trailers and retrofit systems. At the same time, supermarket and logistics operators pilot and adopt electric reefers and e-axle generator trailers in live routes, validating operational savings on fuel, lower maintenance, and predictable emissions reductions while supporting corporate net-zero commitments. OEM activity and partnerships are accelerating commercialization, leading trailer builders have launch all-electric reefer models.

OEMs and eTrailer system providers are working to deliver integrated offerings, while global manufacturers and trade groups are convening standards workshops to harmonize electric trailer requirements, all of which lowers market friction for fleet adoption. The sheer scale of the cold chain amplifies the opportunity, national statistics show refrigerated warehouse capacity measured in the billions of cubic feet, indicating high trailer duty cycles and a large addressable stock that will benefit from electrified solutions. Technological maturity, higher energy density batteries, regenerative-braking e-axles, and modular eTrailer systems are moving rapidly from pilots to revenue programs, enabling OEMs, Tier-1 suppliers, and energy-service providers to roll out complete electrified trailer ecosystems. Taken together, regulation, proven fleet pilots, large cold-chain infrastructure, and faster-maturing electrification technology create a multi-year, high-growth market opportunity for electric trailers, retrofit kits, and integrated service models globally.

Segmentation Analysis

By Trailer Type

Dry Vans Lead Market as They Serve General Merchandise, E-commerce, and Retail Supply Chains

By trailer type, the market is classified as low boy, flat bed, dry van, refrigerated, and tanker.

The Dry vans segment led the market accounting for 39.64% market share in 2026. Dry vans hold the largest automotive trailer market share as they serve general merchandise, e-commerce, and retail supply chains. The dry van is the backbone of long-haul logistics in North America, and equivalents dominate Europe and Asia Pacific corridors. Standardized sizes enable high containerization and terminal compatibility. Demand is propped by sustained e-commerce expansion and retail inventory models, which increase turn rates and replacement cycles. OEM investment centers on lightweight composite panels, aerodynamic skirts, and telematics integration, enhancing fuel economy and utilization factors that sustain dry-van dominance across mature and growth markets.

Tanker trailers transport liquids and gases, fuel, chemicals, and food-grade liquids, and are critical to energy and chemical supply chains. Their market is growing at the highest CAGR and is closely tied to crude/oil product flows, petrochemical plant throughput, and agricultural processing. Tankers require specialized tanks, liners, and safety certifications; that technical barrier places them in a moderate-growth bracket, sensitive to oil price cycles and regulatory safety standards. While electrification of powertrains affects truck tractors first, tankers’ adoption of sensors and IoT for custody transfer and preventive maintenance is increasing, improving asset uptime and bolstering the segment’s value proposition for fleet operators.

Low boy trailers serve heavy, oversized cargo and are indispensable for moving construction machinery, wind-turbine components, and industrial plant equipment. Globally, they represent a niche but essential value segment with durable demand tied to infrastructure and energy projects. Adoption is concentrated where heavy-haul permits and escorts are available; their high unit value means revenue share outpaces unit share. Growth is cyclical, peaking with infrastructure investment booms, and is limited by permitting complexity and transport restrictions. OEMs and specialized hauliers have invested in modular multi-axle low-boy systems to improve payload-to-weight ratios and reduce transport costs, supporting steady market value even amid broader trailer market fluctuations.

Flat beds remain a cornerstone for construction, steel, and project cargo movement owing to their versatility and simplicity. They dominate in markets where large, irregular loads steel coils, pipe, and precast concrete, are common; flatbeds’ relatively low capital cost and straightforward loading drive strong unit demand. Increasingly, fleets favor higher-strength, lighter alloys to raise payload and lower fuel consumption. In emerging markets, flatbeds capture near-term share as industrialization expands, while in developed markets, innovation focuses on modularity and payload optimization. Due to their broad application across sectors, flatbeds are among the largest trailer-type revenue contributors globally.

Refrigerated trailers are a significantly growing trailer subsegment due to expanding cold-chain needs for food, pharmaceuticals, and e-grocery. Growth is driven by supermarket expansion, rising per-capita cold-chain consumption, and regulatory pushes for vaccine and pharma logistics. Fleets and retailers are rapidly piloting and adopting electric TRU solutions and battery-assisted reefers to reduce emissions and meet zero-emission mandates in regions such as California; manufacturers are commercializing e-reefer platforms and partnerships to meet demand. The combination of high duty cycles, increasing refrigerated warehouse capacity, and regulatory momentum makes reefers a high-value, high-growth area within trailers.

To know how our report can help streamline your business, Speak to Analyst

By Number of Axles

Multi-Axle Trailers Dominated Market Due to Higher Allowable Gross Weights and Distributed Load Capacity

By number of axles, the market is classified as single axle and multi axles.

The multi-axles segment dominated the market accounting for 80.00% market share in 2026. The multi-axles segment accounted for the highest market share and faster growth rate in the market in long-haul and heavy-haul operations due to additional axles increasing allowable gross weights and distributing loads to meet bridge/road rules. Their dominance in revenue share is reinforced by demand for higher payload efficiency, containerized freight, and heavy equipment transport. Multi-axle units also enable larger trailer lengths and modular low-boy configurations. Regulatory environments that permit higher axle counts or weight exemptions accelerate multi-axle uptake. As freight grows and fleets seek lower cost per ton-mile, multi-axle combinations are the fastest-growing axle configuration in commercial fleets globally.

Single-axle trailers are used, especially in utility, regional, and consumer applications. They are common where lower gross vehicle weight and maneuverability matter last-mile delivery, small businesses, and recreational towing. Single-axle units are lower cost to buy and operate, making them attractive for owner-operators and small fleets. However, regulatory limits on axle loads and fleets’ desire for higher payload per trip are shifting demand toward multi-axle units for medium and heavy segments. Consequently, single-axle share is stable in light applications but declines slowly in aggregate market share as heavier multi-axle combinations grow.

By Length

Lower Unit Cost with High Density and Container Transport by More than 13.6 m Segment Dominates Market

By length, the market is classified as upto 7 m, 7 to 13.6 m, and more than 13.6 m.

The more than 13.6 m segment is projected to dominate the market with a share of 44.48% in 2026, and higher growth rate also. The 53-ft dry van standard in North America underpins high volume, high-utilization fleets and drives significant revenue share. Longer trailers are favored for containerized cargo, palletized freight, and high-density lanes, providing lower unit transport cost. Growth in this segment is tied to long-haul freight expansion, low cost per ton-mile economics, and regulatory allowances. It remains the dominant revenue segment in mature long-haul markets.

Trailers up to 7 m serve light commercial, recreational, and local delivery needs; they are prominent where city access, parking, and narrow roads constrain operations. This segment is dominated by utility trailers, small box trailers, and single-axle platforms for tradespeople and small logistics players. While they are large in number, their revenue share is proportionally smaller than long-haul trailers. Growth is steady but modest, driven by urban logistics growth and light-goods delivery, yet constrained by medium- and long-haul replacement cycles that contribute more to overall market revenue.

A 7 to 13.6 m bracket, including Europe’s 13.6 m standard, is crucial for regional and intercity distribution. It balances payload, maneuverability, and regulatory fit in many jurisdictions, making it a large, stable market segment. Curtain-siders, medium flatbeds, and refrigerated variants populate this band, and manufacturers optimize for quick regional turnarounds. This segment benefits from urban consolidation centers and intermodal feeder services, remaining a large revenue contributor globally, especially across Europe and Asia Pacific, where infrastructure favors this length class.

By Tonnage

More than 10 Tons Segment Dominates Due to High Unit Cost and Principal Use in Long-Haul, Container Transport, Construction, and Mining

By tonnage, the market is classified as upto 3.5 tons, 3.5 to 10 tons, and more than 10 tons.

More than 10 tons of trailers represent the heavy commercial fleet semi-trailers and modular multi-axle heavy-haulers. They dominate global market revenue due to high unit cost and principal use in long-haul, container transport, construction, and mining. As trade volumes, containerization, and infrastructure investment expand, demand for >10 t trailers remains robust. This tonnage bucket is the market’s largest by value. It is also the focal point for innovations in lightweight materials, aerodynamics, and electrified auxiliaries to reduce the total cost of ownership and emissions.

The 3.5 to 10 tons segment is a bridge between light and heavy commercial use, faster growth rate in regional distribution, municipal services, and specialist trades. Trailers here serve medium trucks and rigid combinations, offering flexibility for urban deliveries with a larger payload than light units. This segment is expanding in emerging markets as fleets migrate from small vans to more efficient medium combinations, and in developed markets as last-mile consolidation ramps. It is a significant contributor to market volume and shows moderate growth as urban logistics becomes denser.

Trailers rated up to 3.5 tons GVW are primarily light-duty utility and consumer segments, common in Europe’s small-goods delivery and owner-operator markets. They require less stringent driver licensing in many regions and are used for local services, small commerce, and recreation. Numerically abundant, these trailers represent a small fraction of the overall market value compared to heavier categories. Growth ties closely to small business activity and last-mile delivery expansion; however, revenue impact is limited due to lower unit price and payload capacity.

By Application

Durability, Low Lifecycle Cost, and Consistent Requirement from Manufacturer and Service Networks Make Industrial Segment Dominate Market

By application, the market is classified as construction, industrial, agriculture, mining, and port.

The Industrial segment will account for 41.99% market share in 2026. Industrial applications, plant equipment, component transport, and inter-plant logistics constitute the single largest trailer application by consistent revenue share, making it dominate the market. Industrial freight demands both specialized heavy-haul and standard dry-van movement; manufacturers tailor trailers for secure machinery moves and optimized payloads. Steady manufacturing output, factory relocations, and supply-chain reshoring increase industrial trailer demand globally. Industrial users value durability, low lifecycle cost, and manufacturer service networks, making this application dominant in the trailer market value.

Agriculture relies on platform and tanker trailers for crop, livestock, and input transport; demand ties to seasonality and commodity cycles. In emerging markets, rising mechanization and cold-chain development increase trailer uptake for produce and inputs. Agricultural trailers are lower-speed, short-haul oriented, but often numerous, giving notable unit shares though lower revenue per unit. Innovations in corrosion resistance and ease of cleaning for food transport are raising coffers on next-generation agricultural trailers, while rural road improvements support broader adoption, making it the fastest-growing segment.

Mining requires specialized heavy low-boy and modular multi-axle trailers to move mining equipment, overburden, and processed ores. It’s a capital-intensive application with high per-unit revenue as trailers must endure extreme loads and harsh conditions. Demand closely follows commodity cycles: booms in metals and minerals trigger heavy equipment shipments and new trailer purchases. Mining’s trailer share is smaller overall but yields a high-margin, specialized business for manufacturers experienced in modular heavy-haul solutions.

Construction is a leading end-use for heavy flatbeds, low-boys, and tipper trailers, underpinning demand when infrastructure and real-estate investment are high. Trailers transport equipment, steel, concrete beams, and modular components; the project's pace directly affects fleet replacement and rental needs. During global infrastructure pushes and stimulus programs, construction trailer demand spikes. However, the segment is cyclical and sensitive to commodity prices and permitting delays.

Port and terminal operations rely on a mix of container chassis, flatbeds, and specialized ro-ro trailers for import/export flows; port activity correlates tightly with container throughput and trade volumes. Growing containerization and hinterland container haulage needs have made port-linked trailers a critical operational segment; investments in port automation and on-terminal electric handling change trailer duty cycles and specs, encouraging chassis modernization. The ports’ strategic importance to global trade makes this application a stable and strategically important contributor to trailer market demand.

AUTOMOTIVE TRAILER MARKET REGIONAL OUTLOOK

Regionally, the market segmentation is into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Automotive Trailer Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America maintained a strong presence in the global market, reaching USD 9.18 billion in 2025, accounting for 36.42% share, and is expected to reach USD 9.49 billion in 2026, driven by a highway-centric freight system, high long-haul utilization, and a deep trailer aftermarket. The U.S. vehicle registration and highway statistics show very large trailer and combination fleets supporting interstate commerce, underpinning steady replacement and upgrade cycles. OEM and supplier moves such as Utility Trailer’s 2024 Eagle Pass TRU assembly facility to support refrigerated-trailer demand demonstrate manufacturers localizing supply chains and expanding cold-chain capacity. These structural features keep North America dominant in value, with incremental growth focused on reefers, telematics, and lightweight materials.

The U.S. automotive trailer market has experienced steady growth, driven by robust economic activity, expanding logistics and freight transport, and increasing consumer demand for diverse trailer types. According to official U.S. Department of Transportation data, North American truck freight valued at around USD 77.7 billion in early 2023 marked a 12.7% year-over-year increase, reflecting stronger demand for trailers. Innovations such as connected smart trailers with real-time telematics and electric refrigerated units cater to stringent environmental regulations and e-commerce logistics needs. These factors combined enhance operational efficiency and sustainability. The U.S. market’s growth, supported by infrastructure investment and expanding e-commerce, significantly propels the overall North American automotive trailer market, encouraging technology adoption and fleet expansion.

Asia Pacific

The Asia Pacific market accounted for USD 7.39 billion in 2025, representing 29.30% of the global industry, and is expected to reach USD 7.86 billion in 2026. The Asia Pacific market is the fastest-growing due to rapid industrialization, expanding domestic logistics networks, and large OEM scale in China. CIMC Vehicles reported strong 2024 revenues and reinforced its leading domestic semi-trailer share, reflecting massive manufacturing volumes and rising export activity. Growth is concentrated in China and India. Long-haul adoption, containerization, and cold-chain investments are expanding reefers and multi-axle heavy trailers. OEMs are scaling production and local standards development to serve large internal demand and export markets, making Asia Pacific the principal growth engine for the global trailer industry.

Europe

In 2025, Europe generated USD 6.57 billion, contributing 26.05% to global market revenue, and is projected to grow to USD 6.77 billion in 2026. Europe is a high-value market characterized by dense regional flows, strict emissions/weights rules, and strong OEM concentration in Germany and nearby countries. Standardization around the 13.6 m semi-trailer and investments in axle and automation capacity reinforce Europe’s efficiency focus; for example, Schmitz Cargobull’s continued production milestones and innovation awards indicate strong OEM R&D and manufacturing scale. Electrification and electric TRU showcases at IAA 2024 highlight a push toward low-emission reefers and energy-efficient trailers. Europe’s market is stable, innovation-led, and focused on regulatory compliance and advanced telematics.

Rest of the World

Rest of the World accounted for USD 2.07 billion in 2025, representing 8.23% of the global market share, and is projected to reach USD 2.18 billion in 2026. The Rest of the World (Latin America, Middle East & Africa) market is smaller in share but important for niche and specialty trailers tied to mining, agriculture, and regional trade. Trade and customs data show rising exports of trailers from emerging producers, and countries with large infrastructure programs spur demand for low-boys, flatbeds, and tankers. Adoption is uneven, constrained by regulatory harmonization and financing, but increasing port throughput and commodity cycles create episodic surges. Manufacturers and fleets often prioritize rugged, cost-efficient designs for these markets rather than the highest-spec innovations.

COMPETITIVE LANDSCAPE

Key Industry Players

Pioneering Innovation, Strong Customer Base Make Utility Trailer Manufacturing Company a Leading Player

Utility Trailer Manufacturing Company is recognized as the world’s largest privately owned producer of refrigerated trailers and one of the most influential leaders in the automotive trailer industry. Established in 1914, the company has grown to dominate global markets primarily due to its relentless innovation in cold-chain transport solutions, coupled with strong customer loyalty from logistics providers, food distributors, and large retail chains. Its leadership stems from its specialization in refrigerated trailers, which form the backbone of perishable goods transportation, a segment witnessing steady global growth. The company has continuously invested in research and development to design lighter, more fuel-efficient trailers using advanced composite materials, thereby reducing operating costs for fleets and ensuring compliance with tightening environmental standards. In addition, Utility’s extensive dealer and service network across North America and its export markets ensures rapid after-sales support, a critical factor in customer retention. Product-wise, Utility manufactures a wide portfolio that includes the 3000R refrigerated van, the 4000D-X Composite dry van, and 4000S/4000AE flatbeds, all of which are benchmark products for durability, payload capacity, and operational efficiency. Its commitment to sustainability, product performance, and strong brand reputation has established Utility as the number one leader in the global market.

Wabash National Corporation is also among-largest players in the global market, distinguished by its extensive innovation in both dry and refrigerated van trailers, and specialty tank trailers. Founded in 1985, Wabash has rapidly risen to prominence by pioneering advanced composite technology, lightweight materials, and aerodynamic solutions that directly address fleet operators’ needs for efficiency and reduced total cost of ownership. Its consistent focus on integrating sustainability with product design has aligned it with fleet operators adapting to strict emissions targets, giving it an edge in regulatory compliance markets. Wabash’s trailer portfolio includes the DuraPlate dry van trailer, the ArcticLite refrigerated van, and a variety of tank and flatbed trailers, all of which are widely adopted by logistics giants in North America and beyond. The company’s strength also lies in its ability to diversify across multiple trailer categories, offering fleets end-to-end solutions rather than being confined to one niche. Additionally, Wabash has invested heavily in digitalization, predictive maintenance solutions, and telematics integration, ensuring that its trailers not only meet but also exceed modern fleet expectations. This innovation-driven approach, coupled with a strong manufacturing footprint and strategic acquisitions, has established Wabash as the second leading force in the global automotive trailer industry.

LIST OF KEY AUTOMOTIVE BUSHING COMPANIES PROFILED

- Great Dane LLC (U.S.)

- Utility Trailer Manufacturing Company (U.S.)

- Wabash National Corporation (U.S.)

- Hyundai Translead (South Korea / U.S.)

- Schmitz Cargobull AG (Germany)

- Krone (Fahrzeugwerk Bernard Krone GmbH) (Germany)

- Kogel Trailer GmbH (Germany)

- Fliegl Fahrzeugbau GmbH (Germany)

- CIMC Vehicles Group Co., Ltd. (China)

- China International Marine Containers (CIMC) (China)

- Tirsan Treyler (Turkey)

- Lecitrailer S.A. (Spain)

- Faymonville Group (Belgium/Luxembourg)

- Stoughton Trailers LLC (U.S.)

- Manac Inc. (Canada)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, Gormley, Ontario-based Premier Bulk Systems, a subsidiary of the Heniff family of companies, acquired Longhorn Transportation, based in Berry Mills. Premier Bulk Systems operates approximately 120 tractors and 250 trailers with expertise in chemical transport, food-grade transport, rail transloading, ISO depot operations, equipment maintenance, tank cleaning services, and logistics.

- In December 2024, the bike passenger car and commercial vehicle parts distributor, Alliance Automotive, added 16 new Don-Bur box van lifting deck trailers to its fleet. The 13.6m long units are liveried with ‘NAPA Auto Parts’ branding as Alliance Automotive is the American company’s official UK distributor.

- In March 2024, Italian transport firm LC3 started sustainable refrigerated transport in Italy with all-electric reefer semi-trailers from Schmitz Cargobull. With this, the company maintains its goal of offering customers high-quality transport and logistics services characterised by safety, punctuality, and an environmentally-conscious approach.

- In September 2023, ZF presented the trailer electrification concept at the NUFAM commercial vehicles trade show in Karlsruhe (Germany). The ZF electrified trailer solution made possible by integrating ZF’s AxTrax 2 electric axle with a modular battery system box for recuperation and traction support. The AxTrax 2 electrified axle system enables recuperation and traction support to deliver up to 210 kW continuous power and 26,000 N·m of peak output of seamless torque.

- In July 2023, Hendrickson launched its air and mechanical suspensions and axles for trailer applications in India. The single axle is designed for Indian and global markets, and it can be coupled with any air and tandem or tridem mechanical suspension system, providing a reliable solution for various applications. The TA 14 heavy-duty air suspension is designed for Indian applications, considering the local road conditions and the changing face of infrastructure in the country. This suspension comes in Top and Low Mount variants, offering numerous options to the customers based on their application requirements.

REPORT COVERAGE

The global automotive trailer market analysis provides detailed market analysis and focuses on key aspects such as leading companies, trailer types, number of axles, length, tonnage, and application. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.95% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

Trailer Type · Low Boy · Flat Bed · Dry Van · Refrigerated · Tanker Number of Axles · Single Axle · Multi Axles Length · Upto 7 m · 7 to 13.6 m · More than 13.6 m Tonnage · Upto 3.5 tons · 3.5 to 10 tons · More than 10 tons Application · Construction · Industrial · Agriculture · Mining · Port By Region · North America (By Trailer Type, By Number of Axles, By Length, By Tonnage, By Application, and By Country) o U.S. (By Trailer Type) o Canada ( By Trailer Type ) o Mexico ( By Trailer Type ) · Europe (By Trailer Type, By Number of Axles, By Length, By Tonnage, By Application, and By Country ) o Germany ( By Trailer Type ) o France ( By Trailer Type ) o U.K. ( By Trailer Type ) o Rest of Europe ( By Trailer Type ) · Asia Pacific ( By Trailer Type, By Number of Axles, By Length, By Tonnage, By Application, and By Country ) o China ( By Trailer Type) o India ( By Trailer Type) o Japan ( By Trailer Type ) o South Korea ( By Trailer Type ) o Rest of Asia Pacific ( By Trailer Type ) o Rest of the World (By Trailer Type, By Number of Axles, By Length, By Tonnage,and By Application) |

Frequently Asked Questions

Fortune Business Insights says the market will reach USD 35.86 billion by 2034.

The market is expected to grow at a CAGR of 3.95% during the forecast period.

Surge in e-commerce and omnichannel retail fuel market growth.

North America led the market in 2025.

North America's market size share was USD 9.18 billion in 2025.

Great Dane LLC, Utility Trailer Manufacturing Company, Wabash National Corporation, Hyundai Translead, and Schmitz Cargobull AG are a few of the major key players operating in the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us