Automotive Wraps Films Market Size, Share & Industry Analysis, By Film Type (Cast Vinyl Films, Calendered Vinyl Films, and Others), By Application (Full Wraps, Partial Wraps, and Decals & Graphics), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), By End Use (Personal Styling and Advertising/Branding), and Regional Forecasts, 2026-2034

Automotive Wraps Films Market Overview

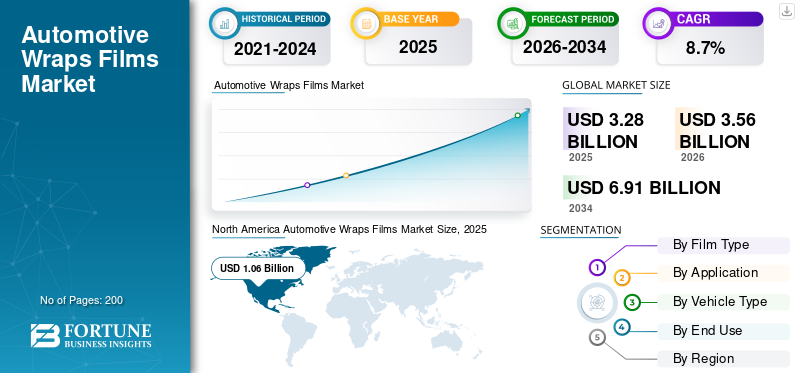

The global automotive wraps films market size was valued at USD 3.28 billion in 2025. The market is projected to grow from USD 3.56 billion in 2026 to USD 6.91 billion by 2034, exhibiting a CAGR of 8.7% during the forecast period. North America dominated the automotive wraps films market with a market share of 32.31% in 2025.

The global market represents a specialized segment within the automotive aftermarket, focused on vehicle wrapping solutions used for both aesthetic enhancement and surface protection. These films are thin, adhesive-backed materials applied over a vehicle’s original paint to change its appearance or provide protection against scratches, UV exposure, and environmental damage. Although closely tied to paint protection films, wrap films are primarily used for styling, branding, and advertising applications.

The market is witnessing steady market growth, driven by increasing demand for personalized vehicles and rising awareness about maintaining vehicle resale value. Consumers are increasingly opting for wraps as a cost-effective alternative to repainting, while businesses use vehicle wraps for mobile advertising, thereby accelerating market expansion. Additionally, technological advancements, including high-performance materials and innovations such as self-healing coatings, are enhancing product durability and expanding application areas.

The industry is also being influenced by evolving market dynamics, including the rise of ride-hailing services, logistics fleets, and e-commerce delivery vehicles that rely heavily on branding. These factors are contributing significantly to the growing demand for vehicle customization globally. Furthermore, improved installation techniques and the availability of diverse finishes such as matte, gloss, and textured films are strengthening adoption.

In the coming years, the market is expected to evolve with greater emphasis on sustainable materials and advanced film technologies. The presence of strong key players such as Fedrigoni and LG Chem and increasing investments in product innovation are expected to further shape the competitive landscape. Companies are focusing on expanding their market share through new product launches and regional growth strategies, supporting the steady growth of the market globally.

Download Free sample to learn more about this report.

Automotive Wraps Films MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.28 billion

- 2026 Market Size: USD 3.56 billion

- 2034 Forecast Market Size: USD 6.91 billion

- CAGR: 8.7% from 2026–2034

- North America dominated the automotive wraps films market with a market share of 32.31% in 2025.

- The full wraps segment is expected to grow at a CAGR of 10.7%.

- The light commercial vehicles segment is expected to grow at a CAGR of 11.2%.

North American

North America held the dominant share in 2025, valued at USD 1.06 billion, and also maintained its leading share in 2024, with USD 1.01 billion.

Europe

Europe is projected to record a growth rate of 6.9% during the forecast period and reach a valuation of USD 0.94 billion by 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 1.15 billion by 2026 and secure the position of the second-largest region in the market.

U.S.

The U.S. market stood at around USD 0.72 billion in 2025, representing roughly 22.0% of global sales.

Japan

Growth supported by high-quality automotive aesthetics demand and increasing adoption of protective wrap solutions.

Read More

AUTOMOTIVE WRAPS FILMS MARKET TRENDS

Integration of Advanced Materials to Amplify Product Adoption

A key trend shaping the global market is the integration of advanced materials featuring innovations such as self-healing properties and improved durability. These technologies enhance film lifespan and help maintain vehicle appearance, attracting consumers seeking long-term solutions. Such advancements contribute to evolving market dynamics and support sustained automotive wraps films market growth.

- For instance, in November 2025, Avery Dennison showcased new PrismaPro color PPF, Supreme Defense, and Neo paint protection films at SEMA, highlighting advancements in style-led and self-healing vehicle protection.

Market Dynamics

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Personalized Vehicles Drives Market Growth

The increasing demand for personalized vehicles is a major driver of the global automotive wrap films market. Consumers are increasingly preferring vehicle wrapping solutions to enhance aesthetics without altering the original paint, supporting long-term value retention. Additionally, businesses utilize wraps for branding, further accelerating market growth. This trend is reinforced by changing consumer preferences and growing awareness of cost-effective customization options.

- For instance, in September 2025, Avery Dennison launched the Supercar Blondie Collection featuring four new Supreme Wrapping Film colors, directly supporting demand for vehicle personalization and premium color-change wraps.

MARKET RESTRAINTS

High Installation Costs to Limit Market Expansion

Despite strong market growth, the high installation and material costs associated with premium wrap films restrict adoption, particularly in developing regions. Skilled labor requirements and ongoing maintenance concerns further impact demand. These factors slow market expansion, especially among cost-conscious consumers who may prefer traditional repainting over advanced vehicle wrapping solutions.

- For instance, in October 2025, Kelley Blue Book stated that full vehicle wraps generally cost around USD 2,000 to USD 10,000 or more, depending on vehicle size, finish, and installation complexity.

MARKET OPPORTUNITIES

Expansion of Logistics and Ride-Hailing Services to Create New Growth Opportunities

The rapid expansion of logistics and ride-hailing services presents significant opportunities for the global market. Commercial fleets are increasingly adopting vehicle wrapping for advertising, improving visibility and brand recognition. This trend supports sustained market expansion and enhances demand across emerging economies where fleet-based branding is growing rapidly.

- For instance, in February 2025, Wrapify partnered with a rideshare ad platform to expand measurable wrapped-vehicle advertising, turning rideshare cars into data-enabled out-of-home media channels.

MARKET CHALLENGES

Limited Awareness and Skill Gaps to Challenge Market Development

Limited awareness about the benefits of vehicle wrapping and a shortage of skilled installers pose challenges to market growth. Improper installation can damage the original paint surface, discouraging adoption among consumers. Additionally, inconsistent quality standards across regions affect customer confidence, slowing overall market expansion.

- For instance, in July 2025, SEMA announced expanded free training sessions for aftermarket professionals, including shop challenges, talent management, and partnered technical programs, reflecting the industry’s increasing need for skilled labor.

Segmentation Analysis

By Film Type

Cast Vinyl Films Segment Dominates Due to Their Superior Performance and Durability

On the basis of film type, the market is segmented into cast vinyl films, calendered vinyl films, and others.

Cast vinyl films secure the dominant automotive wraps films market share due to their superior flexibility, durability, and ability to conform to complex surfaces. These high-performance films are widely used in premium applications, ensuring long-term protection of the original paint. Their extended lifespan and advanced features support strong adoption across developed markets.

- For instance, in May 2025, ORAFOL introduced new ORACAL 970RA Premium Wrapping Cast colors at FESPA 2025, expanding its cast wrap line to over 130 colors.

The others segment is expected to grow at a CAGR of 12.3% over the forecast period.

By Application

Partial Wraps Segment Dominates Due to Their Affordability

On the basis of application, the market is segmented into full wraps, partial wraps, and decals & graphics.

The partial wraps segment dominates due to their affordability and flexibility, making them ideal for both personal styling and branding. They offer effective vehicle wrapping solutions at lower costs compared to full wraps, supporting widespread adoption and contributing significantly to segment growth.

- For instance, ORAFOL’s car wrapping portfolio specifically covers full and partial wraps, with ORACAL 970RA positioned for long-term car wrapping and surface protection.

The full wraps segment is expected to grow at a CAGR of 10.7% over the forecast period.

By Vehicle Type

Passenger Vehicles Segment Dominates Due to a Large Global Vehicle Base

On the basis of vehicle type, the market is segmented into passenger vehicles, light commercial vehicles, and heavy commercial vehicles.

Passenger vehicles dominate the global market due to their large global presence and rising demand for vehicle customization. Consumers increasingly adopt wraps to enhance aesthetics while preserving the original paint, supporting sustained market growth.

- For instance, in July 2023, the U.S. Department of Agriculture confirmed that corn remains the primary feedstock for ethanol production, supporting large-scale biofuel output in North America.

To know how our report can help streamline your business, Speak to Analyst

The light commercial vehicles segment is expected to grow at a CAGR of 11.2% over the forecast period.

By End Use

Advertising/Branding Dominate Due to Their Growing Usage in Mobile Promotions

On the basis of end use, the market is segmented into personal styling and advertising/branding.

The advertising/branding segment dominates as businesses increasingly use vehicle wrapping for mobile promotions. Fleet operators leverage wraps for visibility, driving market expansion and strengthening demand across logistics and ride-hailing sectors.

- For instance, in 2025, 3M promoted fleet vehicle graphics as a cost-effective advertising format, supporting commercial branding demand through durable graphic wraps for vehicles.

The personal styling segment is expected to grow at a CAGR of 10.4% over the forecast period.

Automotive Wraps Films Market Regional Outlook

By geography, the global market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Automotive Wraps Films Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 1.06 billion, and also maintained its leading share in 2024, with USD 1.01 billion. Market growth is supported by a strong customization culture, high disposable income, and advanced aftermarket infrastructure. The region benefits from widespread adoption of vehicle wrapping for both personal and commercial purposes. The presence of major key players and continuous product innovation supports market growth. The U.S. remains the largest contributor, driven by strong demand for fleet branding and premium wraps, reinforcing its leading position in the region.

- For instance, in 2025, 3M expanded its U.S. authorized graphics installer network, improving access to certified vehicle wrap installation services and supporting strong regional adoption of wrap films.

U.S. Automotive Wraps Films Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 0.72 billion in 2025, representing roughly 22.0% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.15 billion by 2026 and secure the position of the second-largest region in the market. The region is expected to witness significant market growth due to rapid urbanization, expanding automotive fleets, and rising demand for vehicle customization. Countries such as China and India are driving market expansion with increasing adoption of cost-effective wrap solutions and growing commercial fleet branding activities.

China Automotive Wraps Films Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 0.39 billion, representing roughly 12.0% of global revenues.

India Automotive Wraps Films Market

The Indian market in 2025 stood at around USD 0.17 billion, accounting for roughly 5.2% of global revenues.

Europe

Europe is projected to record a growth rate of 6.9% during the forecast period and reach a valuation of USD 0.94 billion by 2026. Europe’s market growth is driven by strong automotive culture, premium vehicle ownership, and rising adoption of advanced vehicle wrapping technologies. Increasing focus on aesthetics and sustainability supports demand, while established aftermarket networks contribute to steady market expansion.

Germany Automotive Wraps Films Market

Germany market in 2025 stood at around USD 0.24 billion, accounting for roughly 7.2% of global revenues.

U.K. Automotive Wraps Films Market

The U.K.’s market in 2025 stood at around USD 0.19 billion, accounting for roughly 5.9% of global revenues.

Latin America

Latin America is experiencing gradual growth in the market due to the increasing use of vehicle wraps for advertising and branding. Cost-sensitive consumers prefer partial wraps and decals, supporting adoption. Expanding logistics and ride-hailing services contribute to rising demand across the region.

Middle East & Africa

The Middle East & Africa market is growing steadily, supported by rising luxury vehicle ownership and increasing interest in vehicle customization. Demand is particularly strong in the UAE, where premium wraps and high-performance films are widely adopted, contributing to regional market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Innovation and Expansion to Boost Their Market Share

The competitive landscape of the market is characterized by the presence of established key players focusing on innovation, geographic expansion, and product differentiation to strengthen their market share. Leading companies are investing heavily in research and development to introduce high-performance films with enhanced durability, flexibility, and ease of installation. These advancements are aimed at addressing evolving customer requirements and supporting long-term market growth.

Strategic partnerships and collaborations with automotive OEMs, detailing studios, and distributors are increasingly common. Companies are also expanding their distribution networks to capture untapped opportunities across emerging markets, contributing to overall market expansion. The competitive environment is further shaped by regional manufacturers such as Guangzhou Carbins Film Co., Ltd., China, which are offering cost-effective alternatives, intensifying price competition.

Another key strategy includes the introduction of advanced film technologies featuring innovations such as self-healing properties, improved UV resistance, and better adhesion capabilities. These developments enhance product lifespan and customer satisfaction, thereby strengthening brand positioning. Additionally, companies are focusing on digital marketing and installer training programs to boost product adoption and reinforce their presence across global markets.

- For instance, in April 2026, Fedrigoni Graphics showcased its vehicle wrapping film portfolio at the ISA International Sign Expo in partnership with The Wrap Institute. The partnership highlighted product innovation, installer training, and strategic positioning in the global automotive wrap films market.

LIST OF KEY AUTOMOTIVE WRAPS FILMS COMPANIES PROFILED

- 3M Company (U.S.)

- Avery Dennison Corporation (U.S.)

- Orafol Group (Germany)

- Hexis S.A. (France)

- Arlon Graphics LLC (U.S.)

- XPEL Inc. (U.S.)

- Eastman Chemical Company (U.S.)

- Fedrigoni S.p.A. (Italy)

- LG Chem (South Korea)

- TeckWrap International (China)

- KPMF (U.K.)

- Hexis Graphics (France)

- Grafityp Self Adhesive Products (Belgium)

- Kay Premium Marking Films (U.K.)

- Vvivid Vinyl (Canada)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Fedrigoni introduced the F-Wrap Ultimate 1000 Digital Colour Card, a comprehensive tool for vehicle wrapping applications featuring its cast film range with 3D conformability and Slide & Tack adhesive technology. The solution supports installers in selecting colors and enhances precision in full and partial vehicle wrap projects.

- March 2026: Fedrigoni launched F-Wrap Ultimate Wrapping Films, a 90 µm dual-layer cast film range for full and partial wraps on cars, motorcycles, vans, and trucks, offering up to 12 years’ durability.

- December 2025: HEXIS announced HEXSO, a new production facility in China, aimed at improving proximity to Asian markets, faster deliveries, and competitiveness in entry-level product ranges.

- November 2025: Avery Dennison showcased the Supreme Wrapping Film Supercar Blondie collection at SEMA 2025, along with MPI 1105 digitally printable wrapping film and automotive protection films.

- September 2025: XPEL introduced COLOR Paint Protection Film, combining color styling with paint protection across 16 colors and a stated durability of more than 10 years.

- September 2025: Avery Dennison partnered with Supercar Blondie to launch four exclusive Supreme Wrapping Film colors, targeting premium vehicle customization. The collaboration focuses on high-end aesthetics, color innovation, and global consumer appeal, strengthening Avery Dennison’s position in the premium automotive wrap films segment.

- September 2025: KPMF added new vehicle wrap colors, including Matte Dune Metallic, Matte Palladian Blue, and Gloss Viola Noir, expanding options in premium vinyl wrap finishes.

REPORT COVERAGE

The global automotive wraps films market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Film Type, Application, Vehicle Type, End Use, and Region |

| By Film Type |

|

| By Application |

|

| By Vehicle Type |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.28 billion in 2025 and is projected to reach USD 6.91 billion by 2034.

In 2025, the market value stood at USD 1.06 billion.

The market is expected to exhibit a CAGR of 8.7% during the forecast period.

The passenger vehicles segment led the market by vehicle type.

Rising demand for vehicle customization is the key factor driving the market.

3M, Avery Dennison, Orafol Group, and LG Chem are some of the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us