Autonomous Driving Software Market Size, Share & Industry Analysis, By Component (Perception Software, Planning & Decision-Making Software, Mapping & Localization Software, Driver Monitoring Software, and Others), By Vehicle Type (Hatchback & Sedan, SUV, LCV, and HCV), By Propulsion Type (ICE, BEV, and HEV), By Level of Automation (Level 1, Level 2, Level 3, and Level 4 & 5), By Deployment Mode (On-Premises and Cloud-Based), and Regional Forecast, 2026-2034

Autonomous Driving Software Market Size and Future Outlook

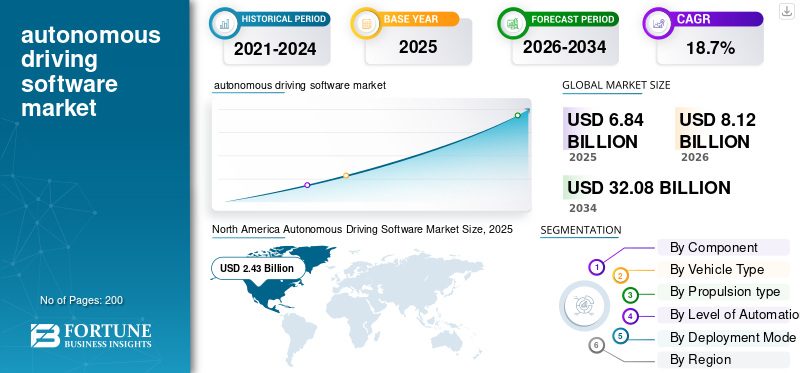

The global autonomous driving software market size was valued at USD 6.84 billion in 2025. The market is projected to grow from USD 8.12 billion in 2026 to USD 32.08 billion by 2034, exhibiting a CAGR of 18.7% during the forecast period. North America dominated the global market with a market share of 35.53% in 2025.

The market comprises software platforms, algorithms, and operating systems that enable vehicles to perform driving functions with minimal or no human intervention. These solutions integrate artificial intelligence, machine learning, sensor fusion, mapping, perception, and decision-making technologies to support advanced driver assistance systems (ADAS) and fully autonomous vehicles.

Key drivers of the market include rising demand for vehicle safety, growing adoption of ADAS technologies, increasing investments in AI and connected mobility, and supportive government regulations. Advancements in sensor fusion, machine learning, and high-definition mapping are accelerating autonomous vehicle development, while the expansion of electric vehicles further supports market growth globally.

Major players in the market include NVIDIA, Mobileye, Waymo, Tesla, Baidu Apollo, Qualcomm Technologies, Aptiv, Bosch, Continental AG, and Huawei, competing through AI-powered driving platforms, sensor fusion technologies, real-time data processing, cloud connectivity, and advanced autonomous navigation solutions.

Download Free sample to learn more about this report.

AUTONOMOUS DRIVING SOFTWARE MARKET TRENDS

Increasing Adoption of Software-Defined Vehicles to Transform Automotive Architecture

A key trend shaping the market is the growing adoption of software-defined vehicles (SDVs). Automotive manufacturers are shifting from hardware-centric vehicle designs toward centralized software-driven architectures that allow continuous feature upgrades and enhanced vehicle functionality. Autonomous driving software is becoming a core component of modern vehicles, enabling over-the-air updates, real-time diagnostics, predictive maintenance, and enhanced connectivity services. This trend is driving automakers to collaborate with software developers, semiconductor companies, and cloud service providers to create scalable digital ecosystems.

Consumers are also demanding personalized in-vehicle experiences and seamless integration with connected devices, further boosting software innovation. Additionally, the increasing use of centralized computing systems and high-performance processors is improving safety for vehicle intelligence and operational efficiency. The transition toward SDVs is expected to grow significantly redefine automotive value chains and future mobility solutions globally.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Integration of AI and ADAS Technologies to Accelerate Market Expansion

The growing integration of artificial intelligence (AI) and advanced driver-assistance systems (ADAS) is a major driver for the autonomous driving software market growth. Automakers are increasingly embedding features such as adaptive cruise control and lane-keeping assistance, automatic emergency braking, and driver monitoring systems into vehicles to enhance safety and driving efficiency. Autonomous driving software enables real-time data processing, sensor fusion, object recognition, and predictive decision-making, making vehicles smarter and more reliable. Rising consumer demand for safer mobility solutions and connected vehicles is further accelerating software adoption.

Additionally, governments and regulatory authorities globally are promoting vehicle safety standards and encouraging the deployment of semi-autonomous technologies. Continuous advancements in machine learning, cloud computing, and edge processing are also improving software performance, scalability, and responsiveness, supporting the widespread commercialization of autonomous mobility solutions globally.

MARKET RESTRAINTS

High Development and Validation Costs to Limit Commercial Adoption

The market faces significant restraints due to the high costs associated with software development, testing, and validation. Developing reliable autonomous systems requires extensive investments in artificial intelligence models, simulation platforms, sensor integration, cybersecurity frameworks, and high-performance computing infrastructure. Companies must also conduct millions of miles of real-world and virtual testing to ensure system accuracy and passenger safety under diverse road conditions. In addition, frequent software updates, regulatory compliance requirements, and complex certification procedures further increase operational expenses.

Smaller automotive technology firms often struggle to compete with established companies due to limited financial resources. The long commercialization timeline and uncertainty regarding return on investment also discourage rapid deployment. These financial and technical barriers are slowing the widespread adoption of fully autonomous driving technologies, particularly in cost-sensitive and emerging automotive markets globally.

MARKET OPPORTUNITIES

Expansion of Robotaxi and Mobility-as-a-Service Platforms to Create New Revenue Streams

The rapid emergence of robotaxi services and Mobility-as-a-Service (MaaS) platforms is creating substantial growth opportunities for the market. Transportation companies and automotive manufacturers are increasingly investing in self-driving fleets to reduce operational costs, improve transportation efficiency, and address urban mobility challenges. Autonomous driving software plays a critical role in enabling navigation, route optimization, real-time traffic analysis, and passenger safety management in shared mobility services.

Rising urbanization and growing demand for convenient on-demand transportation solutions are encouraging the deployment of autonomous ride-hailing and delivery vehicles. Additionally, advancements in 5G connectivity, cloud-based fleet management, and smart city infrastructure are supporting the scalability of autonomous mobility ecosystems. Emerging partnerships between automakers, technology providers, and mobility operators are expected to accelerate commercialization and generate long-term recurring software revenue opportunities across global markets.

MARKET CHALLENGES

Complex Regulatory and Safety Validation Frameworks to Challenge Market Growth

One of the major challenges in the market is the lack of standardized global regulations and complex safety validation requirements. Autonomous vehicles operate in highly dynamic environments, making it difficult for software systems to consistently ensure safe decision-making across all road and weather conditions. Governments and regulatory agencies globally are still developing frameworks related to liability, cybersecurity, functional safety, and autonomous driving approvals. Differences in regional regulations create additional complexity for manufacturers seeking large-scale deployment across multiple countries.

Moreover, any software malfunction or cybersecurity breach can result in serious safety concerns, negatively impacting consumer trust and brand reputation. The need for extensive validation, continuous software monitoring, and compliance with evolving legal requirements significantly increases development timelines. These regulatory and operational uncertainties continue to challenge the commercialization and scalability of fully autonomous driving technologies globally.

Segmentation Analysis

By Component

Advanced Sensor Fusion and Real-Time Object Detection to Propel Perception Software’s Dominance

Based on component, the market is categorized into perception software, planning & decision-making software, mapping & localization software, driver monitoring software, and others.

The perception software segment dominates the market due to its critical role in enabling vehicles to interpret surrounding environments accurately and safely. Perception systems process data from cameras, LiDAR, radar, and ultrasonic sensors to detect objects, pedestrians, traffic signs, and road conditions in real time. Increasing adoption of ADAS features and autonomous driving technologies across passenger and commercial vehicles is significantly driving demand for advanced perception capabilities. Automakers are heavily investing in AI-powered computer vision and deep learning technologies to improve driving accuracy and safety performance. Growing regulatory emphasis on vehicle safety systems and collision avoidance technologies is further accelerating the deployment of perception software solutions globally.

The planning & decision-making software segment is projected to expand at a CAGR of 20.1% over the forecast period. Rising advancements in AI-driven path planning, predictive analytics, and autonomous navigation technologies are increasing demand for intelligent decision-making systems capable of enabling safer and more efficient self-driving operations across diverse traffic environments.

By Vehicle Type

SUVs Dominate Due to Increasing Global Consumer Preference for Premium, Spacious, and Technologically Advanced Vehicles

Based on vehicle type, the market is categorized into hatchback & sedan, SUV, LCV, and HCV.

The SUV segment dominates the market due to increasing global consumer preference for premium, spacious, and technologically advanced vehicles. Automakers are extensively integrating advanced driver-assistance systems (ADAS), AI-powered navigation, and autonomous driving features into SUVs to enhance safety, comfort, and driving performance. The higher adoption of electric and connected SUVs across developed and emerging economies is further accelerating autonomous software deployment. Additionally, luxury SUVs often serve as early platforms for advanced Level 2 and Level 3 autonomous technologies, supporting higher software integration rates. Rising disposable incomes, expanding urban mobility needs, and growing demand for intelligent mobility solutions continue to strengthen the dominance of SUVs in the market globally.

The hatchback & sedan segment is projected to expand at a CAGR of 20.0% over the forecast period. Increasing adoption of affordable ADAS technologies, rising connected vehicle penetration, and growing demand for fuel-efficient smart passenger vehicles are accelerating autonomous driving software integration across compact and mid-sized car categories globally.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion type

ICE Propulsion’s Higher Preference is Led by Widespread Integration of ADAS Technologies in Conventional Automobiles

Based on propulsion type, the market is categorized into ICE, BEV, and HEV.

The ICE segment dominates the market due to the massive global fleet of internal combustion engine vehicles and the widespread integration of ADAS technologies in conventional automobiles. Automakers are increasingly equipping ICE-powered passenger and commercial vehicles with autonomous functionalities such as collision avoidance, lane assistance, and adaptive cruise control to comply with evolving safety regulations. The affordability and established infrastructure supporting ICE vehicles continue to sustain high production volumes globally. Additionally, many automotive manufacturers are deploying semi-autonomous software solutions in existing ICE platforms before transitioning fully toward electrified mobility. Strong consumer demand for connected driving experiences and ongoing advancements in automotive electronics are further supporting the continued dominance of ICE vehicles in autonomous software adoption.

The BEV segment is projected to expand at a CAGR of 19.2% over the forecast period. Rising electric vehicle adoption, growing investments in autonomous EV platforms, and increasing integration of AI-driven software architectures are accelerating demand for autonomous driving solutions across battery-electric passenger and commercial vehicles globally.

By Level of Automation

Increasing Deployment of Driver Assistance Features to Propel Level 2 Segmental Dominance

Based on level of automation, the market is categorized into Level 1, Level 2, Level 3, and Level 4 & 5.

The Level 2 segment dominates the market due to the widespread adoption of partial driving automation features in modern vehicles. Level 2 systems combine steering assistance with acceleration and braking support, offering enhanced driving convenience and safety while still requiring driver supervision. Automakers are increasingly integrating adaptive cruise control, lane centering, and traffic jam assist functions into passenger vehicles to meet rising consumer demand for advanced safety technologies. Regulatory support for ADAS implementation and growing awareness regarding road safety are further accelerating Level 2 software adoption globally. Additionally, Level 2 technologies are comparatively cost-effective and commercially viable, enabling rapid deployment across mid-range and premium vehicle categories in both developed and emerging automotive markets.

The Level 4 & 5 segment is projected to expand at a CAGR of 20.5% over the forecast period. Increasing investments in fully autonomous mobility solutions, robotaxi platforms, AI-based navigation systems, and smart transportation infrastructure are driving demand for advanced self-driving software with minimal or no human intervention capabilities.

By Deployment Mode

On-Premises Deployment is Highest Due to Greater Data Security and Real-Time Processing Control

Based on deployment mode, the market is categorized into on-premises and cloud-based.

The on-premises segment dominates the market due to the growing need for secure, low-latency, and real-time processing capabilities in autonomous vehicle operations. Automotive manufacturers and mobility companies prefer on-premises deployment for handling sensitive driving data, sensor analytics, and safety-critical applications with enhanced control and cybersecurity protection. These solutions support faster decision-making without relying heavily on external network connectivity, which is essential for autonomous navigation and vehicle safety functions. Additionally, large automotive OEMs are investing in dedicated in-house computing infrastructure to optimize software integration, performance validation, and compliance with regulatory standards. The increasing deployment of advanced AI processors and edge computing technologies is further strengthening the adoption of on-premises autonomous driving software solutions globally.

The cloud-based segment is expected to witness substantial growth of 21.9% over the forecast period. The growth is attributed due to rising adoption of connected vehicle ecosystems, over-the-air software updates, and scalable data management platforms. Growing advancements in cloud computing, 5G connectivity, and fleet analytics are accelerating demand for cloud-enabled autonomous driving solutions globally.

Autonomous Driving Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Autonomous Driving Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the market due to the strong presence of leading technology companies, autonomous vehicle developers, and automotive manufacturers across the U.S. and Canada. The region is witnessing substantial investments in AI, machine learning, and autonomous mobility platforms, particularly for robotaxi and autonomous trucking applications. Favorable regulatory support for autonomous vehicle testing and increasing deployment of connected vehicle infrastructure are accelerating software adoption. Additionally, rising consumer demand for advanced driver-assistance systems, software-defined vehicles, and smart mobility services is further strengthening market growth throughout the region.

U.S. Autonomous Driving Software Market

The U.S. market is estimated at around USD 2.54 billion in 2026, fueled by advanced AI innovation, autonomous vehicle testing programs, strong technology company presence, and increasing commercialization of robotaxi and autonomous trucking services.

Asia Pacific

Asia Pacific holds the second largest autonomous driving software market share and is projected to expand at a CAGR of 19.8% over the forecast period. Rapid electric vehicle adoption, strong automotive manufacturing capabilities, and increasing investments in smart mobility infrastructure are driving market expansion across China, Japan, and South Korea. Governments are actively supporting autonomous vehicle development through funding initiatives and favorable policies. Additionally, rising urbanization, increasing demand for connected vehicles, and growing deployment of AI-powered transportation technologies are accelerating autonomous driving software integration across passenger and commercial vehicles throughout the region.

China Autonomous Driving Software Market

The Chinese market is estimated at around USD 1.19 billion in 2026, supported by rapid electric vehicle adoption, expanding robotaxi deployments, and strong government investments in AI-powered smart mobility infrastructure and autonomous transportation ecosystems nationwide.

Japan Autonomous Driving Software Market

The Japanese market is estimated at around USD 0.24 billion in 2026, driven by strong investments in robotics, connected mobility, and intelligent transportation systems. Growing deployment of ADAS technologies and government-backed autonomous vehicle initiatives support market expansion.

Europe

Europe represents the third-largest market for autonomous driving software due to the strong presence of premium automotive manufacturers and increasing focus on vehicle safety regulations. Germany, the U.K., and France are investing heavily in autonomous vehicle research, connected mobility ecosystems, and intelligent transportation infrastructure. Rising deployment of software-defined vehicles and growing adoption of ADAS technologies are supporting software demand across the region. Additionally, stringent emission regulations and increasing electric vehicle penetration are encouraging automotive companies to integrate advanced autonomous driving software solutions into next-generation mobility platforms.

U.K. Autonomous Driving Software Market

The U.K. market is estimated at around USD 0.37 billion in 2026, driven by rising smart mobility investments, favorable autonomous vehicle regulations, and increasing collaborations between automotive manufacturers, software developers, and connected infrastructure providers.

Germany Autonomous Driving Software Market

The German market is estimated at around USD 0.62 billion in 2026, supported by strong automotive manufacturing capabilities, increasing software-defined vehicle adoption, and significant investments in autonomous driving research and intelligent mobility technologies.

Middle East & Africa

The Middle East & Africa market is gradually expanding due to rising investments in smart city projects, intelligent transportation systems, and connected mobility infrastructure. The UAE and Saudi Arabia are increasingly focusing on advanced automotive technologies as part of their digital transformation initiatives. Growing adoption of luxury vehicles equipped with ADAS features and increasing awareness regarding vehicle safety are supporting software demand. Additionally, government-led investments in AI technologies, 5G connectivity, and smart mobility ecosystems are creating opportunities for autonomous vehicle deployment.

UAE Autonomous Driving Software Market

The UAE market is estimated at around USD 0.10 billion in 2026, driven by smart city initiatives, advanced transportation infrastructure investments, and growing adoption of connected and autonomous mobility technologies across urban transportation networks.

Latin America

Latin America is witnessing steady growth in the market due to increasing adoption of connected vehicles and growing awareness regarding advanced vehicle safety technologies. Brazil and Mexico are experiencing rising automotive production and gradual integration of ADAS functionalities in passenger vehicles. Expanding urban mobility challenges and increasing investments in smart transportation infrastructure are supporting demand for autonomous driving solutions. Additionally, the presence of global automotive manufacturers and improving digital connectivity are contributing to market development.

Brazil Autonomous Driving Software Market

The Brazilian market is estimated at around USD 0.19 billion in 2026, supported by rising automotive digitalization, increasing awareness regarding vehicle safety technologies, and gradual adoption of advanced driver-assistance and connected vehicle solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Investments in R&D and Advanced Computing Architectures by Key Players to Strengthen Market Competition

The autonomous driving software market is highly competitive, with global automotive manufacturers, semiconductor companies, and technology firms focusing on strengthening their autonomous mobility capabilities through innovation and strategic collaborations. Leading companies are heavily investing in artificial intelligence, machine learning, sensor fusion, and cloud-based vehicle platforms to improve autonomous driving accuracy and safety. Market participants are also emphasizing partnerships with automotive OEMs, mobility providers, and smart infrastructure developers to accelerate commercialization. Continuous investments in research and development, software validation, and advanced computing architectures are enabling companies to enhance their technological differentiation and expand their global market presence.

Competition in the market is further intensifying due to the rapid evolution of software-defined vehicles and increasing demand for connected mobility solutions. Companies are prioritizing over-the-air software updates, cybersecurity enhancements, and scalable autonomous platforms to gain a competitive advantage. Major players are also expanding autonomous testing programs and pilot deployments across passenger cars, robotaxis, and commercial fleets. Additionally, mergers, acquisitions, and collaborations between automotive and technology companies are supporting product portfolio expansion and faster innovation cycles. The growing focus on regulatory compliance, data security, and real-time processing capabilities continues to shape competitive strategies within the global industry.

LIST OF KEY AUTONOMOUS DRIVING SOFTWARE COMPANIES PROFILED IN REPORT

- Waymo (U.S.)

- NVIDIA Corporation (U.S.)

- Tesla, Inc. (U.S.)

- Mobileye Global Inc. (Israel)

- Baidu Apollo (China)

- Aptiv PLC (Ireland)

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Aurora Innovation, Inc. (U.S.)

- ai, Inc. (U.S.)

- AutoX Inc. (China)

- Huawei Technologies Co., Ltd. (China)

- Qualcomm Technologies, Inc. (U.S.)

- Toyota Woven by Toyota, Inc. (Japan)

- ZF Friedrichshafen AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2026: Tesla announced the arrival of its Full Self-Driving software, known as FSD Supervised, in China. The American automaker confirmed the expansion on the social media platform X and noted that the software is also available in other global markets: South Korea, Australia, Canada, the Netherlands, and the U.S.

- May 2026: Stellantis and Qualcomm Technologies expanded their multi-year collaboration to integrate Snapdragon Digital Chassis solutions and Snapdragon Ride Pilot ADAS platforms across next-generation vehicle architectures, enhancing AI-driven cockpit systems, connectivity, and scalable Level 2+ autonomous driving capabilities globally.

- February 2026: Elektrobit and Mobileye announced the integration of EB corbos Linux for Safety Applications into Mobileye Drive, a scalable end-to-end Level 4 self-driving system. As the foundation for global OEM offerings and robotaxi vendors, the Mobileye platform will utilize Elektrobit’s safety-compliant solution, delivering automotive grade features and field updates. This collaboration reflects Mobileye’s interest in EB corbos Linux for Safety Applications.

- August 2025: Baidu Apollo expanded autonomous mobility testing in China by deploying advanced autonomous driving software for robotaxis and intelligent transportation systems, supporting the country’s rapidly growing smart mobility infrastructure initiatives.

- June 2025: Bosch launched upgraded autonomous driving software solutions focused on AI-enabled perception and predictive driving functions, enabling enhanced Level 2 and Level 3 automation capabilities for global automotive manufacturers.

- February 2025: Aptiv announced the commercialization of next-generation autonomous driving software architectures designed to improve vehicle safety, sensor integration, and high-performance computing for advanced driver-assistance and autonomous vehicle applications.

- December 2024: Huawei expanded its intelligent automotive software portfolio by introducing advanced autonomous navigation and driver monitoring systems for electric vehicles, strengthening its position in China’s smart mobility and autonomous driving market.

REPORT COVERAGE

The global autonomous driving software market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 18.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Vehicle Type, By Level of Automation, By Propulsion Type, By Deployment Mode, and By Region |

| By Component |

|

| By Vehicle Type |

|

| By Propulsion type |

|

| By Level of Automation |

|

| By Deployment Mode |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.84 billion in 2025 and is projected to reach USD 32.08 billion by 2034.

In 2025, the North America’s market value stood at USD 2.43 billion.

The market is expected to exhibit a CAGR of 18.7% during the forecast period of 2026-2034

The SUV segment is the leading segment in the market by vehicle type.

Rising integration of AI and ADAS technologies to accelerate market expansion.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us