Autonomous Drone Systems Market Size, Share & Industry Analysis, By Range (Short-Range Drones, Medium-Range Drones, & Long-Range Drones), By Platform Type (Multirotor, Fixed-Wing, & Hybrid VTOL), By Level of Autonomy (Remote Piloted Drones, Semi-Autonomous Drones, Fully Autonomous Drones, & Swarm-Enabled Autonomous Drones), By Payload Type (Electro-Optical/Infrared (EO/IR) Cameras, Light Detection & Ranging (LiDAR) Sensors, Radar & Synthetic Aperture Radar Systems, Sensors, & Others), By Application (Inspection & Monitoring, Surveying & Mapping, & Others), and Regional Forecast, 2026-2034

Autonomous Drone Systems Market Size and Future Outlook

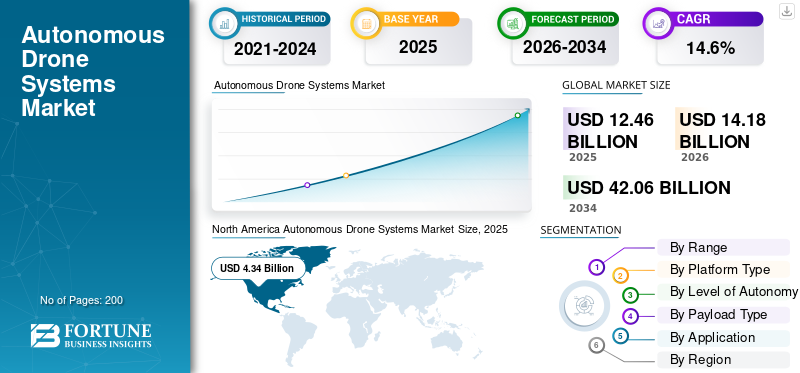

The global autonomous drone systems market size was valued at USD 12.46 billion in 2025. The market is projected to grow from USD 14.18 billion in 2026 to USD 42.06 billion by 2034, exhibiting a CAGR of 14.6% during the forecast period. North America dominated the autonomous drone systems market with a market share of 34.83% in 2025.

Autonomous drone systems encompass unmanned aerial vehicles (UAVs) with self-navigating capabilities via AI, machine learning, and advanced sensors for missions such as reconnaissance, delivery, and inspection. Evolving from remote-piloted models, they feature obstacle avoidance, real-time data processing, and swarm coordination, transforming industries with reduced operational risks and costs. Key advancements include hybrid propulsion, edge AI for low-latency decisions, and modular payloads for versatility. Defense remains a core adopter for ISR tasks, while commercial uses expand in logistics and monitoring, driven by miniaturization and battery innovations that enhance endurance and autonomy.

Key players in the market include DJI, Skydio, AeroVironment, Anduril Industries, Quantum Systems, Parrot, Delair, ideaForge, ACSL, and Autel Robotics. These companies compete through stronger autonomy software, better payload integration, longer endurance, and mission-focused platforms for defense, inspection, mapping, surveillance, and industrial monitoring applications worldwide across regions.

Download Free sample to learn more about this report.

AUTONOMOUS DRONE SYSTEMS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 12.46 billion

- 2026 Market Size: USD 14.18 billion

- 2034 Forecast Market Size: USD 42.06 billion

- CAGR: 14.6% from 2026–2034

- North America dominated the autonomous drone systems market with a 34.83% share in 2025.

- The short-range drones segment accounted for the largest market share in 2025.

- The multirotor segment held the dominant market share in 2025.

North America

North America reached USD 4.34 billion in 2025, driven by utility inspection, public safety adoption, and BVLOS operations.

Europe

Europe is projected to reach USD 3.62 billion in 2026, supported by EASA regulations and expanding commercial drone applications.

Asia Pacific

Asia Pacific is expected to reach USD 4.49 billion in 2026 and grow at a CAGR of 15.3%, driven by China, India, and Japan.

U.S.

The market is estimated at USD 4.35 billion in 2026, accounting for approximately 13.9% of global sales.

Japan

The market is projected to reach USD 0.56 billion in 2026 and grow at a CAGR of 14.1% during the forecast period.

Read More

AUTONOMOUS DRONE SYSTEMS MARKET TRENDS

AI, 5G Connectivity, and Advanced Sensors to Shape the Evolution of the Market

The market is moving toward fully unmanned, AI‑guided platforms capable of complex missions with minimal human intervention. The growing adoption spans defense, logistics, agriculture, infrastructure inspection, and emergency‑response use cases, where drones perform repetitive or hazardous tasks more efficiently than traditional methods. The integration of advanced sensors, 5G‑enabled connectivity, and cloud‑based data analytics is enabling longer‑range, higher‑precision operations, while hybrid vertical‑takeoff‑and‑landing (VTOL) designs are becoming the preferred architecture for multi‑role autonomous systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Product Demand to Accelerate as Organizations Need Safer, Faster, and More Cost-Effective Operations

Key drivers for autonomous drone systems market growth include the rising demand for safer, faster, and more cost‑effective operations across defense and commercial sectors. Advancements in artificial intelligence, computer vision, and navigation technologies are enabling drones to perform complex tasks such as obstacle avoidance, autonomous routing, and real‑time decision‑making. The government push for digitalization and infrastructure modernization, coupled with expanding use cases in surveillance, logistics, energy, and environmental monitoring, is accelerating investments in autonomous UAV platforms and supporting software ecosystems.

MARKET RESTRAINTS

Fragmented Regulations, Safety Concerns, and High Upfront Costs to Limit Large-Scale Deployment

Strict and fragmented aviation regulations, particularly around beyond‑visual‑line‑of‑sight (BVLOS) operations and urban airspace usage, constrain large‑scale deployment of autonomous drone systems. Safety, security, and privacy concerns, including the risks of collisions, unauthorized surveillance, and data breaches, also limit acceptance in densely populated areas. In addition, high upfront costs for advanced sensor suites, secure communication links, and specialized training create entry barriers for smaller operators and public‑sector agencies, slowing the pace of adoption.

MARKET OPPORTUNITIES

New Growth Opportunities to Emerge as Industries Seek Automation, Real-Time Monitoring, and Operational Efficiency

The market offers substantial opportunity in sectors seeking automation, real‑time data, and enhanced operational efficiency. The expanding demand in precision agriculture, smart cities, industrial inspection, and last‑mile logistics enables vendors to deploy scalable fleets and software platforms for continuous monitoring and analytics. Defense and homeland‑security forces are also investing in autonomous UAVs for persistent surveillance, border control, and force‑protection missions, creating long‑term contracts and system‑integration opportunities for aerospace and technology providers.

MARKET CHALLENGES

Battery Limits, Cybersecurity Risks, Weather Exposure, and Operational Complexity are Key Challenges for Large-Scale Adoption

The market faces technical and operational challenges such as limited battery endurance, vulnerability to adverse weather, and dependence on stable communication and positioning systems. Cybersecurity threats, including the risk of spoofing, jamming, or hijacking autonomous platforms, require robust encryption and anti‑tampering measures that increase complexity and cost. Regulatory uncertainty, lack of standardized protocols, and public hesitancy around unmanned systems in populated zones further complicate commercial rollouts and large‑scale fleet operations, demanding close coordination among regulators, industry, and end users.

Segmentation Analysis

By Range

Demand for Short-Range Drones to Rise with Lower-Risk Operating Rules

Based on range, the market is segmented into short-range drones, medium-range drones, and long-range drones.

The short-range drones segment is anticipated to account for the largest autonomous drone systems market share. Short-range drones are seeing strong demand as they fit the bulk of today’s legal, repeatable missions, including site inspection, police response, utility checks, and facility monitoring. They are cheaper, easier to deploy, and better aligned with VLOS and lower-risk operating rules. Hence, organizations can scale usage faster without waiting for complex BVLOS approvals.

The long-range drones segment is anticipated to rise with a CAGR of 15.6% over the forecast period.

By Platform Type

Multirotor Drones Segment Led the Market due to Rising Demand with Fast Setup and Vertical Take-off

Based on platform type, the market is segmented into multirotor, fixed-wing, and hybrid VTOL.

In 2025, the multirotor segment dominated the global market. Multirotor demand is rising as most commercial and public-sector drone work still depends on vertical take-off, stable hovering, close-proximity imaging, and fast setup. Those strengths make multirotors the practical choice for inspection, emergency response, mapping of confined sites, and urban missions where operational flexibility matters more than very long endurance.

The hybrid VTOL (vertical takeoff) segment is projected to grow at a CAGR of 15.4% over the forecast period.

By Level of Autonomy

Remote Piloted Drones Segment to Lead Owing to Regulations Focused on Direct Operator Responsibility

Based on the level of autonomy, the market is segmented into remote piloted drones, semi-autonomous drones, fully autonomous drones, and swarm-enabled autonomous drones.

The remote piloted drones segment is anticipated to witness a dominating market share over the forecast period. These drones continue to see strong demand as most current regulations still center on direct operator responsibility, procedural control, and staged integration of autonomy. Buyers want proven systems they can field now, along with future-ready platforms. Hence, remotely piloted models remain the default for utilities, public safety, and many defense applications.

The swarm-enabled autonomous drones segment is projected to grow at a high CAGR of 16.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Payload Type

Electro-Optical/Infrared (EO/IR) Cameras Segment Led the Market Due to Extensive Mission Coverage

Based on payload type, the market is segmented into electro-optical/infrared (EO/IR) cameras, light detection and ranging (LiDAR) sensors, radar and synthetic aperture radar (SAR) systems, sensors, and others.

The electro-optical/infrared (EO/IR) cameras segment dominated the global market share in 2025. EO/IR supports day-night inspection, perimeter monitoring, firefighting support, search and rescue, and asset assessment, giving operators the broadest mission coverage at practical cost.

In addition, the radar and synthetic aperture radar (SAR) systems segment is projected to grow at a CAGR of 16.6% during the analysis period.

By Application

Inspection and Monitoring Segment Led the Market as Enterprises Need Faster and Safer Asset Checks

Based on application, the market is segmented into inspection and monitoring, surveying and mapping, precision agriculture, surveillance and reconnaissance, and others.

The inspection and monitoring segment dominated the global market share in 2025. The inspection and monitoring demand is rising as drone programs now solve clear cost, safety, and speed problems for infrastructure owners. Utilities, transport operators, and industrial sites use drones to reduce manual exposure, shorten shutdowns, and improve documentation quality, making inspection one of the most repeatable and scalable commercial use cases.

In addition, the precision agriculture segment is projected to grow at a CAGR of 15.0% during the study period.

Autonomous Drone Systems Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Autonomous Drone Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 3.73 billion, and also maintained the leading share in 2025, with USD 4.34 billion. The product demand in North America is rising on the back of utility inspection, public safety adoption, and a clearer pathway toward scalable BVLOS operations. The U.S. drives volume, while Canada is accelerating through new medium-drone and BVLOS-friendly rules.

U.S. Autonomous Drone Systems Market

Based on North America’s strong contribution and U.S.’s dominance within the region, the U.S. market can be analytically approximated at around USD 4.35 billion in 2026, accounting for roughly 13.9% of global sales. The U.S. demand is rising as the market already has scale, a large remote-pilot base, growing public-safety adoption, and a clearer FAA path toward routine drone integration. Inspection, emergency response, and enterprise monitoring remain the main demand anchors.

Europe

The Europe market is estimated to reach USD 3.62 billion in 2026 and secure the position of the third largest region in the market. The product demand in Europe is rising as EASA’s risk-based framework and the EU drone strategy are steadily widening legal commercial use cases. Inspection, mapping, emergency response, and secure drone initiatives are pushing demand beyond pilots and trials.

U.K. Autonomous Drone Systems Market

The U.K. market is estimated to touch around USD 0.63 billion in 2026, exhibiting a CAGR of 14.8% over the forecast period. The product demand in the country is rising as the CAA (Civil Aviation Authority) is actively building a roadmap toward routine BVLOS operations, while registration and compliance structures keep the market formalized. Public safety, infrastructure monitoring, and professional services are the main growth drivers.

Germany Autonomous Drone Systems Market

The Germany market is projected to reach approximately USD 0.81 billion in 2026. Germany’s demand is rising as industrial inspection, infrastructure management, and security-related monitoring fit well within Europe’s structured drone framework. A mature airspace-management environment and enterprise use cases keep demand practical, recurring, and commercially relevant.

Asia Pacific

The Asia Pacific market is projected to record a growth rate of 15.3% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 4.49 billion by 2026. Asia Pacific is the strongest growth engine as China brings scale, India brings policy-led expansion, and Japan brings advanced operational frameworks such as Level 4 flights. That mix supports inspection, logistics, agriculture, and security demand.

China Autonomous Drone Systems Market

The China market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated to touch around USD 2.06 billion. The China demand is rising as the country already operates at huge scale, with strong manufacturing depth, heavy flight activity, and broad civil-drone deployment. That installed base supports continued expansion in inspection, agriculture, security, and logistics applications.

Japan Autonomous Drone Systems Market

The Japan market is estimated to reach around USD 0.56 billion in 2026, accounting for roughly a CAGR of 14.1% during the forecast period. The product demand in Japan is rising as the country has already enabled Level 4 operations, giving the market a stronger framework for higher-value drone use. Infrastructure inspection, logistics experiments, and industrial monitoring are the main demand drivers.

India Autonomous Drone Systems Market

The India market is estimated to touch around USD 0.83 billion in 2026. The product demand in the country is rising as the “Drone Rules” sharply simplified the regulatory structure and improved the operating environment for commercial adoption. Agriculture, infrastructure inspection, surveying, and homeland-security missions are expanding from a relatively smaller base.

Rest of the World

The rest of the world includes the Middle East and Africa and Latin America. These regions are expected to witness moderate growth during the forecast period. The Middle East & Africa and Latin America markets are set to reach USD 0.67 billion and USD 0.47 billion respectively in 2026. The demand in the rest of the world is smaller but rising steadily, led by border surveillance, energy infrastructure monitoring, mining, and agriculture. The security side is reinforced by stronger defense spending, especially in the Middle East.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players to Expand AI-Enabled Autonomy and Dock-Based Operations to Strengthen their Market Share

Key players are shaping the autonomous drone systems market through a mix of AI-enabled flight autonomy, dock-based remote operations, tactical ISR platforms, and industrial inspection solutions. DJI and Skydio are pushing unattended and remotely managed deployments, while AeroVironment and Anduril are strengthening the defense side with mission-ready autonomous air systems. Quantum Systems, Parrot, Delair, ideaForge, ACSL, and Autel Robotics are widening adoption across mapping, infrastructure inspection, security, logistics, and geospatial workflows. This broader product depth and mission coverage is helping lift market demand across both commercial and defense users.

LIST OF KEY AUTONOMOUS DRONE SYSTEMS COMPANIES PROFILED

- DJI (China)

- Skydio (U.S.)

- AeroVironment (U.S.)

- Anduril Industries (U.S.)

- Quantum Systems (Germany)

- Parrot (France)

- Delair (France)

- ideaForge (India)

- ACSL (Japan)

- Autel Robotics (China)

KEY INDUSTRY DEVELOPMENTS

- March 2026: The U.S. Army planned to field the Red Dragon autonomous drone, capable of 400 km strikes without GPS.

- March 2026: XTEND completed an USD 8.8 million contract with the U.S. government to deliver prototype autonomous operational systems.

- March 2026: ParaZero Technologies entered a USD 4 million direct offering agreement to boost financial flexibility for its drone interception systems.

- January 2026: Spain signed a USD 39.5 million contract with Indra Sistemas for Lanza LTR-25 mobile 3D radar systems to detect low-flying drones.

- January 2025: Foresight Autonomous Holdings signed a deal with an Indian defense supplier (5-year contract) with USD 2.5 million potential by 2026 and USD 16 million by 2029.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Range, By Platform Type, By Level of Autonomy, By Payload Type, By Application, and Region |

| By Range |

|

| By Platform Type |

|

| By Level of Autonomy |

|

| By Payload Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 12.46 billion in 2025 and is projected to reach USD 42.06 billion by 2034.

In 2025, the North America market value stood at USD 4.34 billion.

The market is expected to exhibit a CAGR of 14.6% during the forecast period of 2026-2034.

By range, the short-range drones segment is expected to dominate the market.

The rising organizational need for safer, faster, and more cost-effective operations is a key factor driving market growth.

DJI (China), Skydio (U.S.), AeroVironment (U.S.), Anduril Industries (U.S.), Quantum Systems (Germany), and Parrot (France) are major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us