Autonomous Vehicle (AV) Support & Maintenance Services Market Size, Share & Industry Analysis, By Service Type (Software & OTA lifecycle services, Remote operations & fleet monitoring services, Sensor calibration & perception maintenance services, & Others), By Level of Autonomy (Level 2, Level 3, Level 4, and Level 5), By Vehicle Type (Passenger vehicles (L2+/L3), Robotaxis & autonomous shuttles (L4), Autonomous commercial vehicles & Others), By Service Delivery Mode (Remote/cloud-based services, Hybrid services, and & Others), By End User, and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

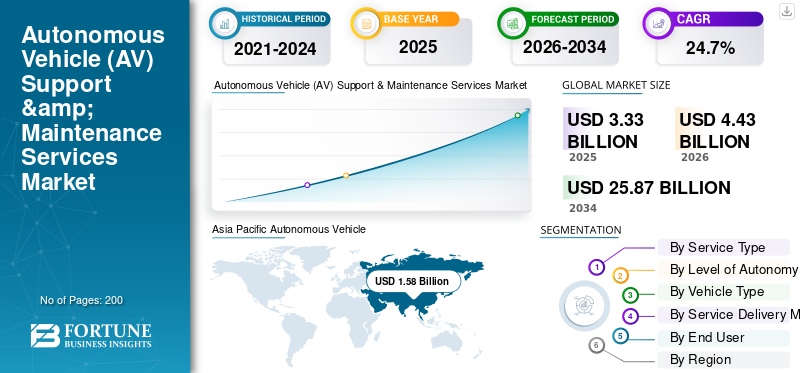

The global Autonomous Vehicle (AV) support & maintenance services market size was valued at USD 3.33 billion in 2025. The market is projected to grow from USD 4.43 billion in 2026 to USD 25.87 billion by 2034, exhibiting a CAGR of 24.7% during the forecast period. Asia Pacific dominated the global market with a market share of 47.44% in 2025.

The growth of the Autonomous Vehicle (AV) support & maintenance services market is steadily expanding as AV and advanced ADAS fleets require continuous software upkeep, safety validation, cybersecurity governance, and high-uptime operations. Growth is driven by rising deployment of connected vehicles and software-defined architectures, increasing reliance on OTA software lifecycle management, and the need for remote operations centers to supervise L4 services. Regulatory pressure around cybersecurity management and software update management systems is also increasing recurring compliance, testing, and re-validation needs.

Key players such as Bosch Mobility Solutions, Continental Automotive, and ZF Group are investing in cloud diagnostics, predictive maintenance, and automated calibration workflows to reduce downtime and improve fleet safety and reliability.

- For instance, in September 2025, Waymo partnered with Lyft to launch autonomous rides in Nashville (2026), with Lyft funding a dedicated fleet-management facility to handle vehicle maintenance and charging, directly strengthening AV operations support, depot maintenance capacity, and scalable fleet uptime management.

Download Free sample to learn more about this report.

Autonomous Vehicle (AV) Support & Maintenance Services Market Key Takeaways

- 2025 Market Size: USD 3.33 billion

- 2026 Market Size: USD 4.43 billion

- 2034 Forecast Market Size: USD 25.87 billion

- CAGR: 24.7% from 2026–2034

- Asia Pacific dominated the AV support & maintenance services market with a 47.44% share in 2025.

- Software & OTA lifecycle services led the market due to rising demand for software-driven vehicle updates.

- Level 2/2+ autonomy segment dominated due to widespread ADAS deployment and large installed base.

Asia Pacific

Asia Pacific led the market with USD 1.58 billion revenue in 2025, driven by connected vehicle adoption and autonomous deployments.

North America

North America showed strong growth due to robotaxi deployment, ADAS penetration, and advanced digital infrastructure.

Europe

Europe expanded steadily with strict safety regulations and growing demand for AV software services.

U.S.

The market is driven by robotaxi operations, ADAS adoption, and strong OTA service ecosystems.

Japan

The market is supported by advanced ADAS adoption, autonomous shuttles, and OEM-led maintenance services.

Read More

AUTONOMOUS VEHICLE (AV) SUPPORT & MAINTENANCE SERVICES MARKET TRENDS

Outsourced Fleet Operations and Depot Partnerships to Reshape Market Development

Autonomous vehicle support is increasingly shifting from in-house OEM programs to specialized, contract-based service ecosystems that combine remote diagnostics, depot operations, charging, and scheduled sensor upkeep. This trend is strongest where robotaxi and shuttle deployments require high uptime, rapid turnaround repairs, and standardized operating playbooks across cities. As fleets expand, operators prefer partners that can run integrated maintenance, parts planning, and operational tooling under service-level commitments, rather than building those capabilities from scratch. This pushes growth in fleet-as-a-service maintenance models, including dedicated depots and embedded maintenance teams tied to real-world utilization and safety performance metrics.

For instance, in September 2025, Lyft and Waymo announced a partnership in Nashville, where Lyft’s Flexdrive provides end-to-end fleet management, including vehicle maintenance, infrastructure, and depot operations.

MARKET DYNAMICS

MARKET DRIVERS

Lifecycle Cybersecurity and Software Update Governance to Accelerate Product Demand

Modern AV and advanced ADAS systems increasingly rely on continuous software releases, safety case updates, and cybersecurity controls throughout the vehicle lifecycle. This creates durable demand for OTA campaign management, version control, validation, incident response, and compliance evidence generation services that persist long after vehicle sales or fleet launches have occurred. As software content increases, even minor changes can necessitate regression testing, sensor/perception revalidation, and documentation to maintain safety performance in real-world environments. This dynamic also increases the value of managed services that standardize update pipelines, telemetry monitoring, and cybersecurity management across global fleets, reducing operational risk and downtime.

For instane, in January 2021, UN Regulation No. 155 (Cybersecurity Management System) and UN Regulation No. 156 (Software Update and SUMS) entered into force, reinforcing ongoing cybersecurity and software update management needs.

MARKET RESTRAINTS

Safety Incidents and Permit Actions Can Constrain Deployment

Even when AV technology improves, market expansion can be constrained by sudden operational pauses, permit suspensions, or stricter oversight following safety events that limit driverless testing or deployment. Such disruption shrinks or suspends fleet operations, immediately reducing demand for high-value services such as remote operations staffing, depot maintenance, and on-road calibration cycles. Service providers also face revenue volatility as contracts may be delayed, renegotiated, or narrowed until operators regain approval to expand their services. This uncertainty can slow investment in specialized depots, tooling, and technician training, especially in new cities. For instance, in October 2023, the California DMV announced the immediate suspension of Cruise’s driverless deployment and testing permits, citing public safety concerns.

MARKET OPPORTUNITIES

Rising Need for Industrialized Validation Services to Support Market Growth

An expanding opportunity is emerging around continuous assurance platforms that unify simulation, scenario-based testing, software verification, and safety documentation for AV stacks. As fleets scale, operators need repeatable methods to validate updates, prove safe behavior in edge cases, and demonstrate compliance readiness without slowing release velocity. This is driving technology demand for industrialized validation services, which combine cloud computing, AI-driven test generation, and integrated reporting, often delivered as subscriptions or managed programs. The result is a growing market for third-party toolchains that reduce the cost and time required for safety validation, while improving auditability, particularly for L4 geo-fenced operations. In March 2025, NVIDIA announced NVIDIA Halos, a full-stack safety system aimed at supporting AV safety, validation, and compliance workflows.

MARKET CHALLENGE

Software Complexity to Hinder Market Growth

A core challenge for AV support and maintenance is that software-defined driving functions can fail in rare, real-world situations that are difficult to reproduce in test environments. When issues arise, providers must rapidly triage telemetry, identify root causes, validate fixes, deploy updates safely, and confirm performance across diverse operating domains, often while vehicles remain in active service. These cycles increase the burden on monitoring, incident management, and continuous calibration, and they can create reputational risk if fixes are delayed or introduce regressions. The operational challenge grows with fleet size and geographic spread, making robust maintenance engineering and disciplined release governance essential. For instance, in December 2025, U.S. regulators issued a recall for 3,067 Waymo vehicles related to an ADS software issue, which was addressed through a software update.

Download Free sample to learn more about this report.

Segmentation Analysis

By Service Type

Software & OTA Lifecycle Services Lead due to its Ability to Enhance Perception Accuracy

Based on service type, the market is segmented into software & OTA lifecycle services, remote operations & fleet monitoring services, sensor calibration & perception maintenance services, cybersecurity & compliance services, and AV hardware & electronics maintenance services.

Software & OTA lifecycle services capture the key Autonomous Vehicle (AV) support & maintenance services market share as autonomous and ADAS-equipped vehicles increasingly rely on frequent software updates to enhance perception accuracy, safety logic, and system reliability. OEMs and fleet operators prioritize OTA-enabled maintenance to reduce recalls, minimize downtime, and support continuous feature upgrades. Regulatory mandates for software traceability and update governance further reinforce demand. These services generate recurring revenue across the vehicle lifecycle, unlike one-time hardware repairs. The remote operations & fleet monitoring services segment is projected to grow at the fastest CAGR of 26.4% over the forecast period.

By Level of Autonomy

Widespread ADAS Deployment Sustains Level 2/2+ Autonomy Segment Leadership

Based on level of autonomy, the market is segmented into Level 2/2+, Level 3, Level 4, and Level 5 autonomy.

Level 2 and Level 2+ vehicles dominate AV support and maintenance demand due to their large global installed base and reliance on camera, radar, and software-driven driver assistance systems. These vehicles require regular diagnostics, OTA updates, calibration, and cybersecurity monitoring, creating consistent service revenue. While autonomy remains partial, the scale of deployment across mass-market passenger vehicles ensures sustained dominance.

The Level 4 autonomy segment is projected to grow at the fastest CAGR of 34.2% over the forecast period, driven by the deployment of commercial robotaxis and shuttles in controlled urban environments.

- In June 2023, Mercedes-Benz received approval for Level 3 DRIVE PILOT in California and Nevada, expanding conditional automation support requirements.

By Vehicle Type

Passenger Vehicle Dominated due to Rapid Integration of ADAS Features

Based on vehicle type, the market is segmented into passenger vehicles, robotaxis & autonomous shuttles, autonomous commercial vehicles, and off-highway & industrial autonomous vehicles.

Passenger vehicles dominated the autonomous vehicle (AV) support and maintenance services market due to their high share in global vehicle production and rapid integration of ADAS features. Automakers increasingly embed software-defined functions, connected diagnostics, and OTA update capabilities into consumer vehicles, driving recurring service needs through OEM and dealer networks. The sheer scale of the passenger vehicle parc outweighs higher per-vehicle service intensity witnessed elsewhere, even in electric vehicles.

The off-highway & industrial autonomous vehicles segment is projected to grow at the fastest CAGR of 28.1%, supported by use cases in mining, agriculture, and port automation.

- For instance, in 2022, Caterpillar reported expanding autonomous haulage systems across mining sites globally, increasing demand for specialized support services.

To know how our report can help streamline your business, Speak to Analyst

By Service Delivery Mode

On-Site/Depot-Based Maintenance Services Segment Lead due to Safety Inspections

Based on service delivery mode, the Autonomous Vehicle (AV) support & maintenance services market is segmented into remote/cloud-based services, hybrid services, and on-site/depot-based maintenance services.

On-site and depot-based maintenance services dominate as many AV support tasks, such as sensor calibration, hardware replacement, and safety inspections, require physical access to vehicles. Despite advances in remote diagnostics, safety-critical repairs still necessitate controlled service environments and trained technicians. Large fleets also rely on centralized depots to manage uptime and parts logistics efficiently.

The remote/cloud-based services segment is projected to grow at the fastest CAGR of 27.4% over the forecast period, driven by expanding connected-vehicle penetration and OTA capabilities.

- For instance, in December 2024, Waymo expanded its Phoenix and San Francisco depot infrastructure to support fleet maintenance and calibration operations in public transport vehicles.

By End User

OEMs & Authorized Dealer Networks Dominated due to Proprietary Diagnostics

Based on end user, the market is segmented into OEMs & authorized dealer networks, autonomous mobility operators, logistics & trucking fleets, and industrial operators.

OEMs & authorized dealer networks dominate the AV support and maintenance services market due to their control over vehicle software, proprietary diagnostics, and warranty-linked service workflows. As vehicles become increasingly software-defined, OEM-led ecosystems manage OTA updates, cybersecurity compliance, and system validation at scale. This centralized control ensures consistent service quality and adherence to regulations.

The autonomous mobility operators segment is projected to grow at the fastest CAGR of 27.5%, as robotaxi and shuttle fleets expand and outsource high-uptime maintenance services.

- For instance, in April 2024, Tesla reaffirmed that all Full Self-Driving updates are delivered exclusively via OTA, reinforcing OEM-led service control.

AUTONOMOUS VEHICLE (AV) SUPPORT & MAINTENANCE SERVICES MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Autonomous Vehicle (AV) Support & Maintenance Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America exhibits strong growth, driven by the early commercialization of autonomous driving technologies, high penetration of connected vehicles, and the active deployment of Level 4 robotaxi and pilot trucking fleets. The region benefits from advanced digital infrastructure, strong OEM technology partnerships, and mature cloud and OTA ecosystems, thereby supporting Autonomous Vehicle (AV) support & maintenance services market growth. Recurring needs for software updates, remote fleet supervision, cybersecurity management, and depot-based maintenance reinforce demand. Regulatory scrutiny and safety oversight further increase demand for continuous validation, monitoring, and compliance-focused AV support services.

U.S.

The U.S. leads the region due to large-scale robotaxi deployments, advanced ADAS penetration in passenger vehicles, and strong OEM control over OTA and diagnostics. High fleet utilization rates and software-driven recall management accelerate demand for remote operations, depot maintenance, and lifecycle software services.

Europe

Europe’s AV support and maintenance services market is growing steadily, supported by stringent regulatory frameworks, a strong focus on vehicle safety, and mandated cybersecurity and software update governance. High adoption of ADAS in passenger vehicles creates recurring demand for calibration, validation, and OTA services. While large-scale robotaxi deployment remains limited, Europe’s emphasis on compliance, homologation, and structured service networks sustains long-term service revenue growth across OEM-led ecosystems and commercial fleets.

U.K.

U.K. benefits from active autonomous testing programs, smart mobility initiatives, and strong software engineering capabilities. Growth is driven by ADAS-heavy passenger fleets and increasing use of autonomous shuttles in controlled environments, supporting demand for validation and remote diagnostics services.

Germany

Germany’s Autonomous Vehicle (AV) support & maintenance services market is anchored by premium OEMs integrating advanced ADAS and conditional autonomy. Strong emphasis on functional safety, cybersecurity compliance, and software lifecycle management drives high demand for OTA governance, system validation, and authorized service network support.

Asia Pacific

Asia Pacific is the dominating and fastest-growing region due to its massive vehicle production base, rapid adoption of connected technologies, and expanding autonomous deployments, particularly in China. The region benefits from rising ADAS penetration in passenger vehicles, government-backed smart mobility initiatives, and an increasing number of use cases for commercial and industrial autonomy. High vehicle volumes combined with growing regulatory attention to software updates and cybersecurity create strong, recurring demand for AV support, maintenance, and remote service solutions.

China

China dominates the Asia Pacific region due to its large-scale robotaxi operations, high connected-vehicle penetration, and strong government support for autonomous mobility. Intensive fleet operations significantly boost demand for remote monitoring, frequent calibration, and software lifecycle management services.

Japan

The adoption of advanced ADAS, aging demographics, and the controlled deployment of autonomous shuttles drive Japan’s growth. OEM-led OTA updates, safety validation, and precision calibration services underpin steady demand for Autonomous Vehicle (AV) support & maintenance services.

India

India is experiencing emerging growth, driven by the increasing adoption of ADAS-equipped passenger vehicles and the growing use of autonomy in commercial and industrial applications. Software diagnostics, fleet monitoring, and gradual adoption of autonomous vehicles AVs in logistics and mining environments drive expansion.

Rest of the World

The Rest of the World region grows steadily as connected vehicle adoption increases across Latin America, the Middle East, and parts of Africa. While autonomous deployment remains limited, the rising penetration of ADAS, improving digital infrastructure, and growing commercial fleet automation drive demand for diagnostics, calibration, and on-site maintenance services. Expansion of logistics, mining, and port automation supports incremental growth in specialized AV support and maintenance solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Software-Defined Vehicle Platforms, Remote Fleet Operations, and Compliance Expertise Shape AV Services' Competitiveness

The global Autonomous Vehicle (AV) support & maintenance services market is shaped by the transition toward software-defined vehicles, increasing complexity of autonomy, and the need for continuous assurance of safety and compliance. Leading players, including Bosch, Continental, ZF, Aptiv, Mobileye, NVIDIA, Accenture, Capgemini, and AWS, compete through advanced OTA lifecycle management, remote fleet operations, cybersecurity services, and automated validation frameworks. Companies enhance their competitiveness by expanding cloud-based diagnostics platforms, investing in AI-driven predictive maintenance, establishing dedicated AV depots, and forming strategic alliances with OEMs, cloud providers, and autonomous mobility operators. Modular service architectures, global delivery capabilities, and regulatory expertise across cybersecurity and software update governance are key differentiators.

For instance, in March 2025, NVIDIA introduced the Halos safety system, supporting AV validation, monitoring, and compliance workflows, reinforcing integrated support service ecosystems for autonomous and highly automated vehicle deployments.

LIST OF KEY AUTONOMOUS VEHICLE (AV) SUPPORT & MAINTENANCE SERVICES COMPANIES PROFILED

- Bosch Mobility Solutions (Germany)

- Continental Automotive (Germany)

- ZF Group (Germany)

- Aptiv (Ireland)

- Mobileye (Israel)

- NVIDIA Automotive (U.S.)

- Harman International (U.S.)

- Siemens Digital Industries Software (Germany)

- Tata Elxsi (India)

- Luxoft, a DXC Technology company (Switzerland)

- Capgemini Engineering (France)

- Accenture Industry X (Ireland)

- Cognizant Mobility (U.S.)

- Waymo (U.S.)

- Baidu Apollo (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025- Uber and Lyft confirmed plans to test robotaxis in London using Baidu’s Apollo Go technology, pending regulatory approvals, with pilots expected to begin in the first half of 2026. New-city launches typically require rapid build-out of local depots, fleet monitoring, calibration capability, and operational maintenance partnerships.

- October 2025- Stellantis and Pony.ai signed an agreement to jointly develop and test the Level 4 autonomous vehicle market in Europe, starting with testing in Luxembourg and targeting broader rollout from 2026. As L4 programs move toward deployment, the need intensifies for validation services, compliance support, sensor/perception upkeep, and structured maintenance regimes.

- Reuters

- September 2025- Einride initiated public-facing progress toward Level 4 autonomous electric truck operations, emphasizing remote monitoring and control tower concepts for fleet supervision. As autonomous freight expands, recurring needs rise for remote diagnostics, preventive maintenance scheduling, sensor health checks, and structured depot servicing to sustain high utilization and safety performance in logistics corridors.

- December 2024- Waymo outsourced key robotaxi fleet operations to Moove, shifting responsibilities such as day-to-day fleet management (including charging and depot execution) to a specialist operator as Waymo scales beyond its core markets. The move reinforces outsourced AV support models built around dedicated facilities, dispatch, and maintenance processes focused on uptime.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 24.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, By Level of Autonomy, By Vehicle Type, By Service Delivery Mode, By End User, and By Region. |

|

By Service Type |

· Software & OTA lifecycle services · Remote operations & fleet monitoring services · Sensor calibration & perception maintenance services · Cybersecurity, compliance & validation services · AV hardware & electronics maintenance services |

|

By Vehicle Type |

· Passenger vehicles (L2+/L3) · Robotaxis & autonomous shuttles (L4) · Autonomous commercial vehicles (LCV & trucks) · Off-highway & industrial autonomous vehicles |

|

By Level of Autonomy |

· Level 2 / Level 2+ (advanced ADAS vehicles) · Level 3 (conditional autonomy) · Level 4 (highly automated, geo-fenced operations) · Level 5 (fully autonomous, limited deployment) |

|

By Service Delivery Mode |

· Remote / cloud-based services · Hybrid services (remote diagnostics + on-site intervention) · On-site / depot-based maintenance services |

|

By End User |

· OEMs & authorized dealer networks · Autonomous mobility operators (robotaxi/shuttle fleets) · Logistics & trucking fleet operators · Industrial & infrastructure operators (ports, mining, campuses) |

|

By Geography |

· North America (By Service Type, By Level of Autonomy, By Vehicle Type, By Service Delivery Mode, By End User, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Service Type, By Level of Autonomy, By Vehicle Type, By Service Delivery Mode, By End User, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Service Type, By Level of Autonomy, By Vehicle Type, By Service Delivery Mode, By End User, and By Country ) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World ( By Service Type, By Level of Autonomy, By Vehicle Type, By Service Delivery Mode, By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.33 billion in 2025 and is projected to reach USD 25.87 billion by 2034.

In 2025, the market value stood at USD 1.58 billion.

The market is expected to grow at a CAGR of 24.7% during the forecast period from 2026 to 2034.

The Level 2 segment led the market in terms of the level of autonomy.

Lifecycle cybersecurity and software update governance are the key factors driving market growth.

Key market players include Bosch Mobility Solutions, Continental Automotive, ZF Group, Aptiv, and Nvidia.

Asia Pacific accounts for the largest share of the market.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us