Battery-free Sensors Market Size, Share & Industry Analysis, By Sensor Type (Temperature Sensors, Pressure Sensors, Humidity Sensors, Motion Sensors, Gas Sensors, and Others (Lights, Sensors, etc.)), By Frequency (Low Frequency, High Frequency, and Ultra-High Frequency), By Industry (Industrial, Automotive, Industrial, Logistics & Transportation, Healthcare, and Others (Agriculture, Aerospace & Defense, etc.)), and Regional Forecast, 2026-2034

BATTERY-FREE SENSORS MARKET SIZE AND FUTURE OUTLOOK

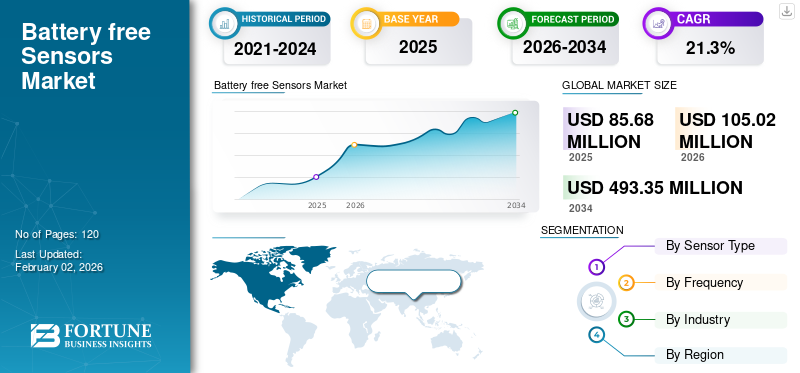

The global battery-free sensors market size was valued at USD 85.68 million in 2025 and is projected to grow from USD 105.02 million in 2026 to USD 493.35 million by 2034, exhibiting a CAGR of 21.3% during the forecast period. Asia Pacific dominated the battery-free sensors market with a market share of 46.7% in 2025.

Battery-free sensors use energy harvesting technologies to power themselves, drawing energy from their surrounding environment instead of a battery. This provides significant benefits, including lower maintenance, higher reliability, and reduced environmental impact from battery waste.

The market is experiencing significant growth, driven by the adoption of IoT devices, miniaturization, and advancements in energy harvesting technologies, which eliminate the need for batteries in applications such as automated condition monitoring, smart factories, and the automotive industry.

The main participants in the market include Infineon Technologies AG, STMicroelectronics N.V., Semiconductor Components Industries, LLC, Texas Instruments Inc., Powercast Corporation, Axzon, EnOcean GmbH, and Everactive, Advantech Co., Ltd.

Download Free sample to learn more about this report.

Impact of Gen AI

GenAI Speeds Up the Product Adoption by Generating Synthetic Training Data

Generative AI (GenAI) is speeding up the adoption of battery-free sensors via the generation of synthetic training data and small, event-driven AI models. This leads to more efficient data processing and transmission, and minimizes power consumption resulting in improved reliability and a stronger return on investment (ROI) for battery-free deployments. These advances speed up the adoption of battery-free sensors in crucial markets such as industrial automation, healthcare, and logistics, which require reliability along with lower maintenance costs to maximize ROI.

Impact of Reciprocal Tariff

Reciprocal Tariffs Raised the Cross-Border BoMs for Battery-Free Sensors, Stressing Pilot Projects Economics

Reciprocal tariffs have raised the cross-border bills of materials (BoMs) for battery-free sensors, which has contributed to higher Average Selling Prices (ASPs), putting strain on the economics of pilot projects. In response, Original Equipment Manufacturers (OEMs) are diversifying their supply chains and near-shoring or regionalizing manufacturing, while also increasing domestic innovation in order to mitigate the effects of the tariffs. These tariffs impose new costs on the key components, such as RF integrated circuits (ICs), antennas, and flexible substrates, many of them sourced from regions such as China.

MARKET DYNAMICS

Market Drivers

Advancements in Ultra-Low-Power Electronics & Harvesting Driving Market Growth

The battery-free sensors market growth is propelled by the advancements in ultra-low-power microelectronics and energy harvesting technologies by enabling devices to operate independently relying on ambient energy sources instead of replacing batteries. The advancements in low-power microelectronics, energy conversion efficiencies, miniaturized energy harvesting technology systems of self-maintaining sensors for smart buildings, industrial automation, healthcare, and wearables. Furthermore, the U.S. Department of Energy indicates that innovations in ultra-low-power circuits have reduced power consumption in sensor systems by nearly 60% in the last decade to encourage sustainable Internet of Things (IoT) deployments. This evolution has lowered maintenance costs and contributed to eco-efficient, long-range sensing ecosystems.

Market Restraints

Security Under Power Scarcity Limit Market Scalability

Integrating robust security features such as cryptography or Physical Unclonable Functions (PUFs) into battery-free sensors presents a major technical challenge due to their extremely limited micro-watt power budgets. These computationally intensive security functions often exceed the energy available from ambient energy harvesting, restricting the adoption of these sensors in regulated sectors such as healthcare and automotive that demand strong security.

Market Opportunities

Growing Adoption in Smart Buildings & Campuses Creates Opportunities for Innovation

The widespread adoption of smart buildings and campuses has created notable opportunities for market. Battery-free sensors provide more battery free options for powering these sensing devices by harnessing energy from their environment rather than utilizing batteries, resulting in more sustainable and cost effective option. For applications such as indoor air quality monitoring, and occupancy sensing, these sensors serve an important role. By preserving power and minimizing maintenance needs, battery free sensors support the transition to sustainable, energy-efficient building designs that are becoming essential across modern facilities.

BATTERY-FREE SENSORS MARKET TRENDS

Hybrid Energy Harvesting Becomes Mainstream as a Major Market Trend

Hybrid energy harvesting is becoming a major trend for battery-free sensors, with hybrid solar-RF systems improving duty cycles for indoor and outdoor use. In these systems, RF harvesting can supplement solar power during low-light conditions, while solar can supplement low-power RF harvesting. This technology is also enabling the development of flexible and wearable battery-free sensors for the Internet of Things (IoT), healthcare, and industrial automation.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Sensor Type

High-Volume Battery-Free Deployments Boosts Temperature Sensors Segment Growth

Based on the sensor type, the market is segmented into temperature sensors, pressure sensors, humidity sensors, motion sensors, gas sensors, and others (lights, sensors, etc.).

The temperature sensors segment held the largest revenue share of USD 17.9 million in the overall global market in the year 2024. The temperature sensors segment led the market accounting for 24.86% market share in 2026. The increase in revenue is driven by its ability to deliver the most universal condition metric at the lowest energy budget, enabling cheap, high-volume battery-free deployments across cold chain, HVAC, and industrial equipment health.

Of all the segments, gas sensors are expected to grow at a highest CAGR of 25.17% in the global market. Miniaturized low-power NDIR and MOX sensors plus tighter IAQ and emissions compliance make gas telemetry the highest-ROI upgrade, propelling battery-free adoption faster than other modalities.

By Frequency

Ultra-High Frequency Dominates Market Owing to Its Longer Read Range and Portal-Based Backscatter Infrastructure

Based on frequency, the market is divided into low frequency, high frequency, and ultra-high frequency.

The ultra-high frequency segment dominates with a battery-free sensors market share of USD 42.7 million. The ultra-high frequency segment dominated the market accounting for 61.67% market share in 2026. The segment continues to generate the major revenue due to its longer read range and portal-based backscatter infrastructure (RAIN RFID) enable high-throughput logistics and industrial deployments at the lowest cost per read, outscaling HF and NFC point reads. The segment also holds the highest CAGR of 24.06% in the global market. The growth is mainly due to expanding RAIN RFID portal infrastructure, long-range backscatter, and falling tag ASPs enable fleet-scale cold-chain and asset-tracking telemetry, making UHF the fastest-growing band.

By Industry

Dense IIoT Deployments On Hard-To-Reach Assets Augments the Industrial Segment Growth

Based on the industry, the market is divided into industrial, automotive, industrial, logistics & transportation, healthcare, and others (agriculture, aerospace & defense, etc.)).

The industrial segment for accounted for the largest market share at USD 20.7 million in 2024. The industrial segment is projected to dominate the market with a share of 0.22% in 2026. The segment continues to generate the highest revenues as dense IIoT and predictive-maintenance deployments on hard-to-reach assets (motors, conveyors, pipes) yield the highest TCO and uptime gains from battery-free sensing, driving earlier, larger-scale rollouts than other sectors.

Healthcare represent the largest CAGR at 25.76% in the global market. The segment is growing faster as battery-free implantables and disposable biosensing patches remove battery size/replacement risks and enable reimbursable remote monitoring, driving the fastest growth from a small base.

To know how our report can help streamline your business, Speak to Analyst

BATTERY-FREE SENSORS MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America Battery-free Sensors Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 21.83 million in 2025, capturing 25.50% of the global market share, and is expected to reach USD 25.99 million in 2026. The North America market is rapidly expanding owing to strong IoT adoption, advanced healthcare, and industrial automation. Other components driving growth in the region include government investment, a robust research and development ecosystem, and the rising demand for energy-efficient and sustainable monitoring solutions. The U.S. is at the forefront of the North American market, with expected revenue of USD 15.5 million in 2025. This growth is attributable to the country’s significant contributions in areas such as logistics, healthcare, and retail. The U.S. market is valued at USD 18.43 million by 2026.

Europe

In 2025, Europe represented USD 15.77 million, accounting for 18.40% of the worldwide market, and is expected to reach USD 18.91 million in 2026. This region’s growth is attributable to strict environmental regulations, the push for sustainability, and the expansion of Industry 4.0 and smart factory initiatives. Key sectors such as automotive, logistics, and healthcare are significant drivers, with Germany leading the adoption due to its strong industrial and automotive sectors. The U.K., Germany and France are some of the leading contributors to the growth in the market, with the required revenue stake of USD 3.6 million, USD 3.5 million in 2026 and USD 2.6 million respectively by 2025.

Asia Pacific

The Asia Pacific market generated USD 40.02 million in 2025, representing 46.70% of the global market landscape, and is expected to reach USD 50.31 million in 2026. The region holds the majority share, which it attributable to its dense electronics manufacturing base and supply chains in China, Japan, South Korea, Taiwan, and ASEAN, rapid IIoT and logistics deployments, and large-scale smart-infrastructure programs that favor low-cost, battery-free rollouts.

At the same time, the region is also expected to have the highest CAGR of 26.03%, further solidifying the market as the fastest growing. This growth is owing to government-backed smart-city programs, and a vast manufacturing base rapidly scale battery-free sensing atop expanding RAIN/NFC reader infrastructure.

The Japan market is valued at USD 9.81 million by 2026, the China market is valued at USD 10.2 million by 2026, and the India market is valued at USD 7.17 million by 2026.

To know how our report can help streamline your business, Speak to Analyst

South America and Middle East & Africa

The markets of South America and Middle East & Africa accounted for USD 4.45 million in 2025, representing 5.20% of the global market share, and is projected to reach USD 5.45 million in 2026. The region’s growth is attributable to increased adoption of IoT systems and the push for more efficient, low-maintenance technology. GCC countries are predicted to have a market share of USD 1.4 million by 2025.

Latin America

In 2025, Latin America held 4.20% of the global market, reaching a valuation of USD 3.6 million, and is projected to grow to USD 4.36 million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Focusing On Developing New Solutions to Lead the Industry

The key players in the industry include Infineon Technologies AG, STMicroelectronics N.V., Semiconductor Components Industries, LLC, Texas Instruments Inc., Powercast Corporation, Axzon, EnOcean GmbH, Everactive, Advantech Co., Ltd. These leading firms develop and provide a range of battery-free sensor solutions that use energy harvesting technologies to eliminate the need for batteries. They are also leveraging the ultra-low-power sensors, wireless connectivity enhancement, and AI-integrated monitoring systems for competitive advantage.

LIST OF KEY BATTERY-FREE SENSORS COMPANIES PROFILED:

- Infineon Technologies AG (Germany)

- STMicroelectronics N.V. (Switzerland)

- Semiconductor Components Industries, LLC (U.S.)

- Texas Instruments Inc. (U.S.)

- Powercast Corporation (U.S.)

- EnOcean GmbH (Germany)

- Everactive (U.S.)

- Advantech Co., Ltd. (Taiwan)

- Farsens (Spain)

- OniO (Norway)

- Atmosic Technologies (U.S.)

- Identiv (U.S.)

- Avery Dennison Smartrac (Netherlands)

- Wiliot (Israel)

KEY INDUSTRY DEVELOPMENTS:

- October 2025- Dracula Technologies, a pioneer in enabling battery-free IoT through energy harvesting from ambient indoor light, announced the completion of its Series A extension round, bringing the total Series A funding to USD 34.87 million. This marks a key milestone in the company’s mission to eliminate batteries from billions of connected devices worldwide.

- June 2025- Energous Corporation d/b/a Energous Wireless Power Solutions (NASDAQ: WATT), a leader in over-the-air (OTA) wireless power networks, today announced the launch of the e-Sense tag, a battery-free, maintenance-free wireless sensor for location and temperature monitoring in retail, supply chain, and logistics environments.

- May 2025- Powercast Corporation, the go-to source for both off-the-shelf and customized wireless charging solutions, has collaborated with Asset Vue to customize Powercast's RFID-powered, wire-and-battery-free sensor condition monitoring system to meet the needs of data centers.

- June 2023- Identiv, a global leader in digital security and identification in the Internet of Things (IoT), in collaboration with Asygn, launched the first battery-free Sensory Tag on Metal (TOM®) label designed to measure temperature and strain in proximity to metallic structures.

- December 2022- Powercast Corporation, the leader in radio-frequency (RF)-based over-the-air wireless power technology, and KYOCERA AVX, a leading global manufacturer of advanced electronic components, are teaming to create sustainable, battery-free solutions capable of harvesting power from industry-standard RFID readers to power ESLs (electronic shelf labels), RFID Sensor Tags and other battery-free IoT devices.

- October 2022- Everactive, the maker of category-defining batteryless Internet of Things (IoT) systems, released its first battery-free development kit to allow third-party developers to build their own IoT products. The development kit includes two of Everactive’s patented batteryless IoT devices, each with a comprehensive sensor suite that simultaneously measures temperature, humidity, pressure, and triaxial acceleration.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the battery-free sensors market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAIL |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 21.3% from 2026-2034 |

| Historical Period | 2019-2023 |

| Unit | Value (USD Million) |

| Segmentation | By Sensor Type, Frequency, Industry, and Region |

| By Sensor Type |

|

| By Frequency |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 85.68 million in 2025 and is projected to reach USD 493.35 million by 2034.

The market is expected to exhibit steady growth at a CAGR of 21.3% during the forecast period.

Advancements in ultra-low-power electronics & harvesting is speeding up the market growth.

Infineon Technologies AG, STMicroelectronics N.V., Semiconductor Components Industries, LLC, Texas Instruments Inc., Powercast Corporation, Axzon, EnOcean GmbH, Everactive, Advantech Co., Ltd. are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 40.02 million in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us