Bicycle Bottom Bracket Market Size, Share & Industry Analysis, By Product Type (Threaded Bottom Brackets, Press-Fit Bottom Brackets, External Bearing Bottom Brackets, and Others), By Bearing Type (Steel Bearings and Ceramic Bearings), By Shell Width (Up to 80 mm and Above 120 mm), By Bicycle Type (Mountain, Road, Hybrid, Cargo, and Others), and Regional Forecast, 2026-2034

Bicycle Bottom Bracket Market Size and Future Outlook

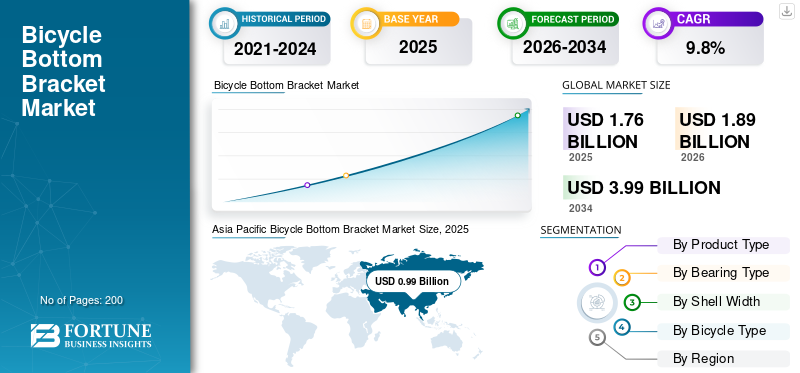

The global bicycle bottom bracket market size was valued at USD 1.76 billion in 2025. The market is projected to grow from USD 1.89 billion in 2026 to USD 3.99 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period. Asia Pacific dominated the bicycle bottom bracket market with a market share of 56.25% in 2025.

The bicycle bottom bracket market refers to the global industry involved in the design, manufacturing, and sale of bottom bracket systems, which connect the crankset to the bicycle frame and enable smooth rotation of the crank arms. The key market includes various types such as threaded, press-fit, and integrated bottom brackets, serving road, mountain, hybrid, and electric bicycles across OEM and aftermarket distribution channels worldwide.

Key market drivers include rising global bicycle adoption for commuting and fitness, growing popularity of e-bikes, increasing participation in cycling sports, advancements in lightweight and durable materials, expanding aftermarket upgrades, and supportive government initiatives promoting sustainable mobility and eco-friendly transportation infrastructure development worldwide.

Key players in the market include Shimano Inc., SRAM LLC, Campagnolo S.r.l., Full Speed Ahead (FSA), Chris King Precision Components, Hope Technology, and Token Products. These companies compete through advanced bearing technologies, lightweight materials such as carbon and ceramic, enhanced durability, improved sealing systems, broad frame compatibility, and seamless integration with high performance cranksets for road, mountain, and e-bikes.

Download Free sample to learn more about this report.

BICYCLE BOTTOM BRACKET MARKET TRENDS

Shift Toward Lightweight, Sealed, and Integrated Bottom Bracket Technologies to Drive the Market Growth

A prominent trend in the market is the transition toward lightweight, highly sealed, and integrated designs. Manufacturers are focusing on reducing overall drivetrain weight while improving stiffness and pedaling efficiency. Press-fit and integrated bottom bracket systems are gaining traction in performance bicycles due to improved frame compatibility and enhanced power transfer. Advanced sealing technologies are also being developed to increase resistance to water, mud, and dust, particularly for mountain and gravel bikes. Furthermore, integrating bottom brackets with specific crankset systems ensures optimized alignment and reduced mechanical friction. As bicycle frame materials evolve toward carbon fiber and advanced alloys, bottom bracket standards are also adapting to support modern frame geometries and performance demands across road, off-road, and e-bike categories.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Advancements in Drivetrain Efficiency and Power Transfer to Strengthen Component Replacement Demand

Continuous advancements in bicycle drivetrain technology are driving demand for high-precision bottom bracket systems that enhance power transfer and pedaling efficiency. Modern cyclists, particularly competitive riders and performance enthusiasts, prioritize components that minimize friction and energy loss. Manufacturers are responding with improved bearing designs, tighter tolerances, and optimized spindle interfaces that deliver smoother crank rotation and greater stiffness. As cranksets evolve with larger spindle diameters and lightweight materials, compatible bottom brackets must also advance to maintain structural integrity and durability. These technological improvements encourage both OEM adoption in mid- to high-end bicycles and aftermarket replacements among serious riders. The pursuit of marginal performance gains, especially in road racing, gravel, and mountain biking, continues to support demand for upgraded bottom bracket solutions globally.

MARKET RESTRAINTS

Price Sensitivity in Entry-Level Bicycle Segments to Limit Premium Adoption

While innovation in bottom bracket technology is advancing rapidly, strong price sensitivity in entry-level and mass-market bicycle segments acts as a restraint. A significant portion of global bicycle sales comes from affordable commuter and utility bicycles, particularly in emerging markets. In these segments, manufacturers prioritize cost efficiency over advanced features such as ceramic bearings, carbon components, or high-end sealing systems. As a result, premium bottom bracket solutions face limited penetration outside high-performance and enthusiast categories. OEMs often opt for standardized, low-cost threaded or cartridge bottom brackets to maintain competitive pricing. This cost-focused approach can restrict margins for premium component manufacturers and slow the adoption of technologically advanced systems, particularly in price-driven markets across Asia, Africa, and Latin America.

MARKET OPPORTUNITIES

Growth of Aftermarket Upgrades and Performance Customization to Create New Revenue Streams

The expanding culture of bicycle customization and performance upgrades presents a strong opportunity in the bottom bracket market. Cycling enthusiasts increasingly seek enhanced stiffness, reduced weight, smoother rotation, and improved durability through aftermarket component replacements. High-performance road cyclists, mountain bikers, and gravel riders frequently upgrade factory-installed bottom brackets to ceramic-bearing or precision-engineered alternatives. The rise of direct-to-consumer sales channels and online specialty retailers has further simplified access to premium upgrade components globally. Additionally, social media communities and cycling influencers actively promote performance optimization, encouraging riders to invest in drivetrain improvements. This shift toward personalization and premiumization enables manufacturers to diversify their product portfolios, introduce specialized bottom bracket standards, and capture higher margins in enthusiast-driven market segments worldwide.

MARKET CHALLENGES

Fragmented Standards and Compatibility Issues to Challenge Market Stability

The proliferation of multiple bottom bracket standards presents a significant challenge to market stability and consumer confidence. Over the years, manufacturers have introduced numerous threading types, shell widths, spindle diameters, and press-fit variations, creating compatibility complexities for consumers and retailers. This fragmentation often leads to confusion during replacement or upgrade purchases, increasing the risk of improper installation and product returns. Bicycle retailers must maintain extensive inventories to support different standards, raising operational costs. Additionally, incompatibility between frames, cranksets, and bottom brackets can deter consumers from upgrading components. The absence of universal standardization complicates supply chain efficiency and limits interchangeability, creating long-term structural challenges for manufacturers striving to balance innovation with broad compatibility across global bicycle platforms.

Segmentation Analysis

By Product Type

Established Frame Compatibility and Cost Efficiency to Sustain Threaded Bottom Brackets Segment Growth

Based on product type, the market is classified into threaded bottom brackets, press-fit bottom brackets, external bearing bottom brackets, and others.

The threaded bottom brackets segment dominates the market due to its long-standing industry standardization, broad frame compatibility, and cost-effectiveness. These are widely used on entry-level, mid-range, and commuter bicycles and are preferred for their durability, ease of installation, and reduced creaking issues. Their service-friendly design supports frequent replacements in urban and utility bicycles, ensuring consistent OEM adoption and steady aftermarket demand across global cycling markets.

The external bearing bottom brackets segment is projected to grow at a CAGR of 11.0% during the forecast period. Increasing demand for improved stiffness, better power transfer, and lightweight crank systems in road, gravel, and mountain bikes is accelerating adoption. Performance-oriented cyclists increasingly prefer external bearing systems for enhanced durability and drivetrain efficiency.

To know how our report can help streamline your business, Speak to Analyst

By Bearing Type

Cost-Effectiveness and Wide OEM Adoption to Maintain Steel Bearing Segment Leadership

In terms of bearing type, the market is categorized into steel bearings and ceramic bearings.

The steel bearings segment dominates the market due to its affordability, durability, and widespread OEM integration across entry-level and mid-range bicycles. Steel bearings offer reliable performance under diverse riding conditions, including commuting and recreational cycling. Their lower production cost makes them ideal for mass-market bicycles, particularly in emerging economies. Additionally, ease of replacement and broad compatibility across threaded and press-fit systems support sustained aftermarket demand, reinforcing their dominant bicycle bottom bracket market share.

The ceramic bearings segment is projected to grow at a CAGR of 13.1% over the forecast period. Increasing demand for low-friction, lightweight, and high-efficiency drivetrain components among competitive and performance cyclists is accelerating adoption. Premium road, gravel, and mountain bike segments are driving stronger uptake of ceramic bottom bracket solutions.

By Shell Width

High Compatibility with Standard Frame Designs to Drive Up to 80 mm Segment Dominance

Based on shell width, the market is segmented into Up to 80 mm and Above 120 mm.

The up to 80 mm segment dominates the market due to its extensive compatibility with standard road, hybrid, and cross-country mountain bike frames. Most traditional threaded and press-fit bottom bracket shells fall within this range, making it the preferred specification for mass-produced bicycles. Its widespread OEM adoption across entry-level and mid-range models ensures high production volumes. Additionally, a strong presence in commuter and recreational bicycles sustains consistent aftermarket replacement demand, reinforcing the segment’s leading position globally.

The above 120 mm segment is projected to grow at a CAGR of 13.8% during the forecast period. Growth is driven by expanding fat bike and e-bike categories, which require wider shells to accommodate larger tires and higher torque systems. Increasing adoption of specialized off-road and electric bicycles is accelerating demand.

By Bicycle Type

Versatile Urban Utility and Mass Adoption to Strengthen Hybrid Bicycle Segment Leadership

Based on bicycle type, the market is segmented into mountain, road, hybrid, cargo and others.

The hybrid bicycle segment dominates the market due to its wide consumer base and versatility across commuting, fitness, and leisure applications. Hybrid bicycles combine features of road and mountain bikes, making them popular among urban riders seeking comfort and practicality. Strong demand across Europe, North America, and Asia for affordable, multi-purpose bicycles supports high OEM production volumes. Additionally, hybrids are widely used for daily commuting and short-distance travel, resulting in steady wear-and-tear and consistent aftermarket bottom bracket replacement demand, reinforcing the segment’s dominant position.

The cargo bicycle segment is projected to grow at a CAGR of 11.7% over the forecast period. Rising adoption for last-mile delivery, urban logistics, and family transport is increasing demand for durable, high-load bottom bracket systems capable of handling heavier payloads and electric assist configurations.

Bicycle Bottom Bracket Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific dominates the market due to its strong bicycle manufacturing base in China, Taiwan, and Japan, as well as high domestic consumption in China and India. The region benefits from large-scale OEM production, cost-efficient supply chains, and expanding e-bike adoption. Growing urbanization, supportive government cycling initiatives, and rising fitness awareness further support demand. Additionally, rapid growth in electric and performance bicycles positions the Asia Pacific as the fastest-growing region over the forecast period.

Asia Pacific Bicycle Bottom Bracket Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Bicycle Bottom Bracket Market

The China’s market in 2026 is estimated at around USD 0.38 billion, accounting for a significant share of global market revenues. Strong domestic bicycle manufacturing, expanding e-bike production, and export-oriented component supply chains continue to drive steady bicycle bottom bracket market growth.

India Bicycle Bottom Bracket Market

The Indian market in 2026 is estimated at around USD 0.29 billion, accounting for a modest share of global market revenues. Rising bicycle adoption, government cycling initiatives, and growing fitness awareness position India as the fastest-growing market in the region.

Europe

Europe holds the second-largest market share, supported by strong cycling culture, established infrastructure, and high e-bike penetration in countries such as Germany, the Netherlands, and France. Consumers prioritize premium and performance bicycles, driving demand for advanced bottom bracket technologies, including ceramic and external bearing systems. Government policies promoting sustainable mobility and low-emission transport further stimulate bicycle adoption. The region is projected to grow at a CAGR of 9.5% over the forecast period.

Germany Bicycle Bottom Bracket Market

Germany’s market in 2026 is estimated at around USD 0.05 billion, accounting for a notable share of global market revenues. Strong e-bike penetration, established cycling infrastructure, and demand for premium drivetrain components support consistent market expansion.

Italy Bicycle Bottom Bracket Market

The Italian market in 2026 is estimated at around USD 0.08 billion, accounting for a considerable share of global market revenues. The presence of leading component brands and a strong road cycling culture sustains OEM integration and aftermarket upgrade demand.

North America

North America is the third-largest market, driven by recreational cycling, mountain biking, and the growing popularity of gravel bikes in the U.S. and Canada. Strong demand for performance-oriented bicycles supports the adoption of high-quality drivetrain components and aftermarket upgrades. The growing e-bike segment, particularly in urban areas, further contributes to bottom bracket demand. Additionally, the presence of premium bicycle brands and specialty retailers supports consistent OEM and replacement sales across the region.

U.S. Bicycle Bottom Bracket Market

The U.S. market in 2026 is estimated at around USD 0.21 billion, accounting for a significant share of global market revenues. Growth is supported by rising gravel biking, e-bike adoption, and strong aftermarket component replacement trends.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, presents emerging growth opportunities in the market. Rising urban congestion, increasing fuel prices, and improving awareness of affordable mobility solutions are driving bicycle adoption. Expanding middle-class populations and growing interest in recreational cycling further support market expansion. While price sensitivity remains high, gradual infrastructure development and rising imports of mid-range bicycles are expected to steadily boost demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation-Driven Competition and Strategic OEM Partnerships Shape Market Landscape

The bicycle bottom bracket market is characterized by intense competition among established global component manufacturers and specialized premium brands. Leading players such as Shimano Inc., SRAM LLC, Campagnolo S.r.l., and Full Speed Ahead (FSA) leverage strong OEM partnerships, broad product portfolios, and global distribution networks to maintain market leadership. These companies focus on precision engineering, compatibility across multiple frame standards, and continuous drivetrain innovation. Their scale advantages enable cost optimization, consistent quality control, and the ability to serve both mass-market and performance bicycle segments effectively.

In addition to large multinational players, niche manufacturers such as Chris King, CeramicSpeed, Hope Technology, and Token Products compete through product differentiation and high-performance offerings. These companies emphasize ceramic bearing technology, lightweight materials, enhanced sealing systems, and premium craftsmanship to attract enthusiasts and professional cyclists. Strategic product launches, sponsorship of professional cycling teams, and expansion into direct-to-consumer channels are common competitive strategies. Increasing focus on durability, reduced friction, and compatibility solutions further shapes the evolving competitive landscape.

LIST OF KEY BICYCLE BOTTOM BRACKET COMPANIES PROFILED

- Shimano Inc (Japan)

- SRAM LLC (U.S.)

- Campagnolo S.r.l. (Italy)

- Full Speed Ahead (FSA) (Taiwan)

- CeramicSpeed A/S (Denmark)

- Chris King Precision Components (U.S.)

- Hope Technology Ltd. (U.K.)

- Token Products (Taiwan)

- Rotor Bike Components (Spain)

- Tange Seiki Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Shimano Inc. announced expansion of its high-end drivetrain component production capacity in Japan to support growing global demand for performance road and gravel bicycle components, including advanced bottom bracket systems.

- December 2025: Bikone introduced new lightweight, aero bottom bracket for Tadej Pogacar and UAE Team Emirates-XRG. This new unit is the lightest the brand has ever produced at 77 grams, 15 grams lighter than the previous unit, and for comparison, about 3 grams lighter than the CeramicSpeed BB Alpha.

- November 2025: Campagnolo S.r.l. launched a next-generation Super Record groupset featuring redesigned bottom bracket compatibility to enhance stiffness and power transfer efficiency.

- October 2025: Ceramic Speed launched a brand new bottom bracket range today, named the BB Alpha, which will replace all existing CeramicSpeed bottom brackets and become the brand's new standard. The BB Alpha units represent a complete overhaul of the current CeramicSpeed bottom bracket offering.

- September 2025: CeramicSpeed unveiled a new coated ceramic bottom bracket series designed to reduce friction and extend service life for professional cycling teams.

- July 2025: Full Speed Ahead (FSA) expanded its MegaExo bottom bracket range with lightweight alloy cups targeting the growing gravel bike segment.

- May 2025: Hope Technology introduced a precision-machined threaded bottom bracket line manufactured in the U.K. to strengthen its premium aftermarket portfolio.

REPORT COVERAGE

The global bicycle bottom bracket market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, By Bearing Type, By Shell Width, By Bicycle Type, and By Region |

| By Product Type |

|

| By Bearing Type |

|

| By Shell Width |

|

| By Bicycle Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.76 billion in 2025 and is projected to reach USD 3.99 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 0.99 billion.

The market is expected to exhibit a CAGR of 9.8% during the forecast period.

The hybrid segment is leading the market by bicycle type.

Advancements in drivetrain efficiency and power transfer are the key factors driving the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us