Biofoam Packaging Market Size, Share & Industry Analysis, By Material (Polylactic Acid (PLA), Starch-based, Cellulose-based, Mycelium, and Others), By Packaging Type (Trays & Clamshells, Containers, Cups & Bowls, Inserts & Dividers, and Others), By End-use Industry (Food & Beverages, Consumer Goods, Healthcare, E-commerce & Logistics, and Others), and Regional Forecast, 2026-2034

Biofoam Packaging Market Size and Future Outlook

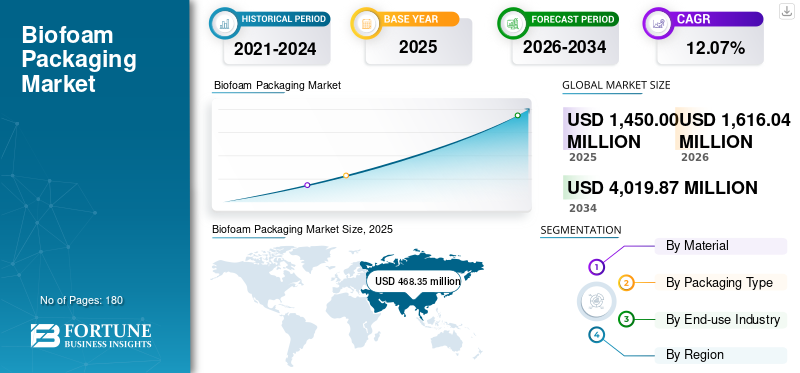

The global biofoam packaging market size was valued at USD 1,450.00 million in 2025. The market is projected to grow from USD 1,616.04 million in 2026 to USD 4,019.87 million by 2034, exhibiting a CAGR of 12.07% during the forecast period. Asia Pacific dominated the global biofoam packaging market with a market share of 32.3% in 2025.

The global biofoam packaging market refers to the sector dedicated to the manufacturing and distribution of foam-based packaging materials derived from renewable, biodegradable, or compostable bio-based polymers, as opposed to conventional petroleum-based plastics such as EPS or EPE. The expansion of this market is propelled by the growing sustainability regulations, the implementation of plastic bans, and the increasing consumer inclination toward environmentally friendly packaging alternatives.

Furthermore, the market is dominated by several major players, including Sealed Air, Stora Enso, and Ecovative LLC, at the forefront. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

BIOFOAM PACKAGING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.45 Billion

- 2026 Market Size: USD 1.62 Billion

- 2034 Forecast Market Size: USD 4.02 Billion

- CAGR: 12.07% from 2026–2034

- Asia Pacific dominated the biofoam packaging market with a 32.3% share in 2025.

- The starch-based material segment is projected to grow at a CAGR of 12.26% during the forecast period.

- The containers packaging type segment is expected to expand at a CAGR of 12.11% over the forecast period.

North America

North America was valued at USD 420.07 million in 2025 and is projected to grow at a CAGR of 12.14%, supported by expanding e-commerce, cold-chain logistics, and direct-to-consumer delivery services.

Europe

Europe accounted for USD 269.99 million in 2025, benefiting from strict sustainability regulations, circular economy initiatives, and advanced recycling infrastructure.

Asia Pacific

Asia Pacific reached USD 468.35 million in 2025 and remained the leading regional market, driven by rapid industrialization, food delivery growth, and supportive regulations for bio-based materials.

U.S.

The market was valued at USD 350.29 million in 2025, driven by rising demand for sustainable packaging, stringent plastic regulations, and innovation in plant- and fungi-based materials.

Japan

The market is witnessing steady growth due to government support for sustainable packaging, increasing adoption of bio-based materials, and efforts to reduce plastic waste across industries.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Surging Demand for Sustainable & Circular Packaging Drives Market Growth

Rising environmental concerns and heightened regulatory pressure to minimize plastic waste are significantly propelling the adoption of biofoam packaging. Companies in foodservice, e-commerce, consumer goods, and protective packaging sectors are swiftly transitioning to biodegradable, compostable, and bio-based materials to fulfill corporate sustainability objectives and comply with national plastic-reduction regulations. This transition directly enhances the demand for biofoam alternatives derived from starch, PLA, PHA, seaweed, and various other renewable resources. Henceforth, the growing demand for sustainable and circular packaging drives the global biofoam packaging market growth.

MARKET RESTRAINTS

Higher Production Costs and Limited Economies of Scale Hamper Market Growth

Biofoam packaging is currently experiencing elevated production costs, primarily due to the high expense of raw materials such as starch, PLA, PHA, algae-based polymers, and mycelium, which are considerably costlier than petroleum-based polymers such as EPS or EPE. These biopolymers necessitate specialized processing, controlled environments, and frequently imported additives, all of which contribute to the overall expense. Additionally, the limited availability of automated machinery, the requirement for custom molds, supply chain disruptions, and dependence on emerging technologies further increase operational costs. Consequently, many price-sensitive industries, particularly in developing markets, are reluctant to adopt biofoam packaging on a large scale, hindering its penetration into the mass market despite the rising demand for sustainability.

MARKET OPPORTUNITIES

Expansion in E-commerce & Cold-Chain Logistics Provides Potential Opportunities

The swift growth of global e-commerce and cold-chain logistics is generating significant demand for biofoam packaging, as these industries necessitate protective, lightweight, and thermally insulated solutions for high-volume shipping. As consumers increasingly purchase fresh groceries, meal kits, beverages, pharmaceuticals, vaccines, and temperature-sensitive items online, businesses are looking for packaging that not only protects products but also adheres to sustainability goals.

With the global increase in online retail penetration and the expansion of cold-chain networks into pharmaceuticals, food exports, and specialty goods, the demand for sustainable packaging solutions is anticipated to surge, presenting a substantial growth opportunity for biofoam manufacturers.

BIOFOAM PACKAGING MARKET TRENDS

Increased Adoption in Foodservice, Meal Kits & Ready-to-Eat Foods Emerges as a Market Trend

The rapid expansion of the global foodservice sector, coupled with the growing demand for meal kits and ready-to-eat (RTE) food items, is significantly propelling the adoption of biofoam packaging. As consumers increasingly depend on takeaway meals, cloud kitchens, quick-service restaurants (QSRs), and subscription-based meal kit services, the amount of disposable packaging has dramatically increased, creating substantial pressure on brands to transition toward sustainable options. Meal kit companies, in particular, necessitate packaging that ensures perishable ingredients remain cool and secure during last-mile delivery, rendering biofoam insulated inserts, trays, and coolers particularly appealing. Likewise, manufacturers of ready-to-eat food products gain from biofoam’s capacity to sustain temperature stability, avert leakage, and convey an environmentally friendly brand image.

MARKET CHALLENGES

Limited Global Composting & Recycling Infrastructure is a Key Challenge to Market

One of the primary obstacles to the adoption of biofoam packaging is the insufficient composting and recycling infrastructure present in numerous regions. While biofoam materials such as starch-based, PHA, PLA, or mycelium foams are engineered to be biodegradable or suitable for industrial composting, the majority of countries lack extensive facilities that can process them effectively. Industrial composting facilities are predominantly located in certain areas of Europe and North America, resulting in significant markets in Asia, Latin America, and Africa relying on rudimentary landfill and informal waste management systems.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Polylactic Acid (PLA) Segment Led Market Due to Its Excellent Combination of Performance

In terms of material, the market is categorized as polylactic acid (PLA), starch-based, cellulose-based, mycelium, and others.

The polylactic acid (PLA) segment captured the largest share of the market in 2025. In 2025, the segment dominated with a 41.01% share. Polylactic acid (PLA) is the leading material in the biofoam packaging sector due to its excellent combination of performance, cost effectiveness, and sustainability when compared to other biopolymers. PLA is produced from plentiful and low-cost agricultural resources such as corn starch, sugarcane, and cassava, which guarantees a steady supply and reduced raw material expenses.

Its straightforward processing, compatible with current foam manufacturing machinery, simplifies production and speeds up the path to market. PLA-based biofoam exhibits favorable characteristics such as a lightweight design, cushioning properties, thermal insulation, and robust mechanical strength, making it ideal for applications in foodservice, e-commerce, protective packaging, and consumer products.

The starch-based material segment is expected to grow at a CAGR of 12.26% over the forecast period.

By Packaging Type

Trays and Clamshells Led Market Due to High Foodservice Demand and Versatile Protective Performance

In terms of packaging type, the market is categorized into trays & clamshells, containers, cups & bowls, inserts & dividers, and others.

The trays and clamshells segment captured the largest biofoam packaging market share in 2025. In 2025, the segment dominated with a 45.01% share. The market is primarily led by the trays and clamshells segment, as these formats are extensively utilized in foodservice, fresh produce, meal kits, bakery, and ready-to-eat (RTE) applications, where there is a swift rise in the demand for sustainable, insulated, and disposable packaging. Biofoam trays and clamshells provide outstanding cushioning, thermal retention, grease resistance, and rigidity, rendering them an excellent alternative to traditional polystyrene food containers that have been prohibited in numerous areas. Their lightweight design, ability to be stacked, and compatibility with both hot and cold food improve operational efficiency for restaurants, cloud kitchens, grocery retailers, and food delivery services.

The containers packaging type segment is expected to grow at a CAGR of 12.11% over the forecast period.

By End-use Industry

Food & Beverages Led Market Due to High Consumption of Single-Use Packaging and Strong Shift Toward Sustainable Foodservice Solutions

Based on end-use industry, the market is segmented into food & beverages, consumer goods, healthcare, e-commerce & logistics, and others.

In 2024, the global market was dominated by food & beverages in terms of end-use industry. Furthermore, the segment held a 53.69% share in 2025. The food and beverage sector leads the biofoam packaging industry, as it accounts for the largest share of single-use packaging globally, thereby driving significant demand for environmentally friendly substitutes for plastic and polystyrene foams. Restaurants, cafés, quick-service restaurant (QSR) chains, cloud kitchens, bakeries, and grocery stores depend extensively on trays, clamshells, cups, bowls, produce trays, and insulated containers formats where biofoam performs exceptionally well due to its lightweight nature, thermal insulation properties, cushioning ability, and resistance to grease and moisture. The rapid increase in takeaway meals, online food delivery services, ready-to-eat (RTE) products, and meal kits has further intensified the demand for packaging that is both sustainable and functional.

Additionally, the end-use industry of consumer goods is projected to grow at a CAGR of 11.81% during the study period.

To know how our report can help streamline your business, Speak to Analyst

Biofoam Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Biofoam Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valued at USD 417.87 million, and maintained its leading position in 2025, with a value of USD 468.35 million. The market in the Asia Pacific region is propelled by swift industrial growth, a surge in food delivery services, and significant advancements in electronics manufacturing that necessitate protective packaging. Nations such as China, India, Japan, and Indonesia are implementing bans on plastic and promoting the use of bio-based materials through policy changes and financial incentives.

In the region, China and India are valued at USD 161.86 million and USD 130.67 million, respectively, in 2025.

North America

During the forecast period, the North America region is projected to record a growth rate of 12.14%, which is the second highest among all regions, and is valued at USD 420.07 million in 2025. The demand for biofoam packaging in North America is mainly driven by significant growth in e-commerce, cold-chain logistics, and direct-to-consumer delivery systems, particularly for meal kits, fresh produce, and pharmaceuticals.

In 2025, the U.S. market is valued at USD 350.29 million. The biofoam packaging market in the U.S. is experiencing significant growth, propelled by the demand for sustainability, stringent regulations on plastics, and the expansion of e-commerce. Notable trends encompass advancements in materials derived from plants and fungi, improved performance facilitated by technology such as artificial intelligence and nanotechnology, an increasing application in sectors like electronics, food, and medicine, as well as a movement towards the development of high-performance, intelligent biofoams.

Europe

The European market is valued at USD 269.99 million in 2025 and has secured the position of the third-largest region in the market. Europe is at the forefront of the global market, driven by its stringent sustainability regulations, such as the EU Single-Use Plastics Directive (SUPD), the Green Deal, and the circular economy framework. Additionally, Europe's well-established recycling and waste management systems facilitate quicker commercialization and scaling efforts.

Backed by these factors, countries including Germany are valued at USD 60.75 million, the U.K. USD 45.90 million, and France USD 39.01 million in 2025.

Latin America

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space. The Latin America market in 2025 is valued at USD 160.81 million. Latin America is witnessing a rapid increase in the use of biofoam packaging, as nations such as Brazil, Chile, Colombia, and Mexico implement regulations on single-use plastics. Moreover, investment in research and development and rising consumer preferences for PLA packaging bolster market growth.

Middle East & Africa

In the Middle East & Africa, South Africa is valued at USD 36.63 million in 2025. In the Middle East & Africa, the expansion of biofoam packaging is propelled by national sustainability objectives, including Saudi Arabia's Vision 2030 and the UAE's Waste-to-Resource initiatives, both of which promote the use of environmentally friendly packaging.

COMPETITIVE LANDSCAPE

Key Industry Players

Top Companies Focus onProduct Innovation and Strategic Partnerships to Maintain Their Leading Positions

The global biofoam packaging market exhibits a semi-concentrated structure, with numerous small to mid-size companies actively operating worldwide. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Sealed Air, Stora Enso, and Ecovative LLC are among the leading players in the market. A comprehensive range of Biofoam Packaging products, a global presence through a strong distribution network, and collaborations with research and academic institutions are a few characteristics that support the dominance of these players.

Apart from this, other prominent players in the market include BASF SE, Woamy OY, BEWI, and others. These companies are undertaking various strategic initiatives, including investments in research and development (R&D) and partnerships with pharmaceutical companies, to enhance their market presence.

LIST OF KEY BIOFOAM PACKAGING COMPANIES PROFILED:

- Sealed Air (U.S.)

- Stora Enso (Finland)

- Ecovative LLC (U.S.)

- BASF SE (Germany)

- Woamy OY (Finland)

- BEWI (Sweden)

- Good Biopak (Australia)

- Lisopack b.v. (Netherlands)

- Semepack (China)

- ROHA (India)

- Magical Mushroom Company (U.K.)

- PolyLINK Solutions (Canada)

- Storopack (Germany)

- Woodbridge (Canada)

- Zotefoams (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: Storopack introduced an innovative bio-based foam packaging solution. The FOAMplus 7008-BIO, a new packaging foam from Storopack, emphasizes sustainability as its primary focus. This polyurethane foam contains over 83% genuine bio-based carbon content in the B-Component, indicating that it is derived from renewable sources and has a significantly lower carbon footprint compared to similar products made from fossil origins.

- May 2025: The Czech firm, Myco, introduced its biodegradable alternative to polystyrene packaging, which is claimed to be ‘100% plastic-free’ and is composed of mushroom mycelium and organic waste. Evidently, this material is a composite that includes mycelium, a network of fungal fibers, along with organic waste materials such as sawdust, hemp shavings, and paper. The mycelium proliferates through the loose components, thereby strengthening the structure.

- January 2024: SEE introduced a compostable protein packaging tray at the IPPE 2024 event. The new CRYOVAC brand compostable overwrap tray from SEE is constructed from biobased, food-contact-grade resin, which has received USDA certification for containing 54% biobased content chemically sourced from renewable wood cellulose.

- June2023: Ecovative Design LLC, recognized as the foremost company in mycelium technology globally, declared the initial closing of a Series E funding round exceeding USD 30 million. Of this amount, USD 15 million is being reinvested into its subsidiary, MyForest Foods Co., which was established in 2020. This funding will enable Ecovative to further develop its Forager business into a premier supplier of sustainable textile and foam products, while the investment in MyForest Foods will support its retail expansion as it expands its presence along the Eastern Seaboard.

- November 2021: Naya introduced innovative mushroom packaging to promote sustainability. This packaging is developed using Mycelium Technology. Mycelium, which is the subterranean root system of mushrooms, serves as a bio-contributing material that provides a safe, sustainable, and entirely home-compostable option. Crafted from mushrooms, the kit is fully biodegradable, recyclable, and compostable, establishing it as Naya's most sustainable gift set to date.

REPORT COVERAGE

The global biofoam packaging market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, market sizing, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.07% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Material, Packaging Type, End-use Industry, and Region |

|

By Material |

|

|

By Packaging Type |

|

|

By End-use Industry |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1,450.00 million in 2025 and is projected to reach USD 4,019.87 million by 2034.

In 2025, the market value stood at USD 468.35 million.

The market is expected to exhibit a CAGR of 12.07% during the forecast period of 2026-2034.

The trays and clamshells segment led the market by packaging type.

The key factor driving the market growth is the surging demand for sustainable & circular packaging.

Sealed Air, Stora Enso, Ecovative LLC, BASF SE, Woamy OY, and BEWI are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

The growing demand for bio-based packaging from several end-use industries is one of the factors expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us