Biologics Safety Testing Market Size, Share & Industry Analysis, By Products & Services (Kits & Reagents, Instruments, and Services), By Test Type (Sterility, Endotoxin/Pyrogen, Mycoplasma, Bioburden, Viral Safety/Adventitious Agents, Residual HCP/HCDNA, Cell Line Characterization, and Others), By Application (mAbs & Recombinant Proteins, Vaccines, Cell & Gene Therapies, Blood & Plasma Products, and Tissue/Stem Cell Products), By End User (Pharma & Biotech Companies, CROs/CDMOs, Academic & Research Institutes, and Government/Regulatory Labs), and Regional Forecast, 2026-2034

Biologics Safety Testing Market Size and Future Outlook

The global biologics safety testing market size was valued at USD 6.40 billion in 2025. The market is projected to grow from USD 7.00 billion in 2026 to USD 13.13 billion by 2034, exhibiting a CAGR of 8.18% during the forecast period. North America dominated the global biologics safety testing market with a market share of 37.34% in 2025.

The biologics safety testing market is projected to experience significant growth due to the exponential increase in the production of biologics and biosimilars, which aim to cater to the rising disease burden. This increasing production is anticipated to result in the growing adoption of biologics, safety testing consumables, and other services. The developing economies are emerging as a potential hub for outsourcing safety testing. Emphasizing the opportunities presented by these factors, many major players are focusing on expanding their biologics testing capabilities through facility launches worldwide.

- For instance, in November 2023, Merck KGaA completed the second phase of its new USD 39.4 million Biologics Testing Center in China, expanding the lab by 1,500 square meters, which was opened in 2024. The development enabled clients to access a broad range of testing services for cell line characterization and lot release from pre-clinical development to commercialization.

Additionally, the market is dominated by various key operating players, including Merck KGaA, SGS Société Générale de Surveillance SA, Thermo Fisher Scientific Inc., and Sartorius AG, which direct their resources toward strategic mergers and acquisitions to strengthen their market position.

Download Free sample to learn more about this report.

BIOLOGICS SAFETY TESTING MARKET KEY TAKEAWAYS

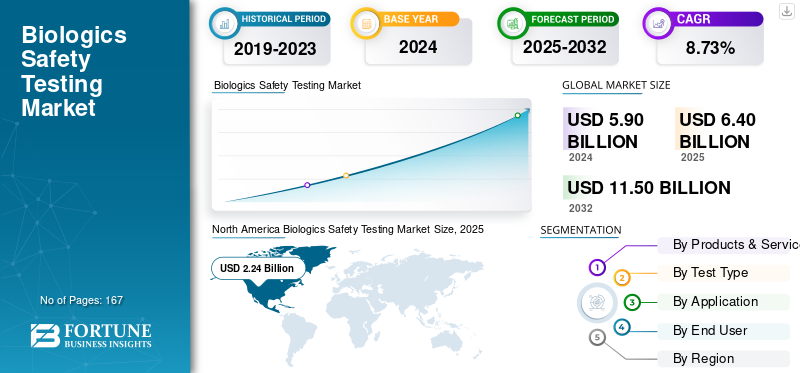

- 2024 Market Size: USD 5.90 billion

- 2025 Market Size: USD 6.40 billion

- 2032 Forecast Market Size: USD 11.50 billion

- CAGR: 8.73% from 2025–2032

- North America dominated the biologics safety testing market with a 37.97% share in 2024.

- The viral safety/adventitious agents segment is projected to hold a 27.8% share in 2025.

- The mAbs & recombinant proteins segment is projected to hold a 47.23% share in 2025.

North America

North America was USD 2.39B 2025, 37.34% share, driven by biologics safety testing demand, pharma concentration, and cell & gene therapy pipelines.

Europe

Europe was USD 1.84B 2025, 28.75% share and ~USD 2B+ 2026, driven by advanced therapies expansion and biosafety testing growth.

Asia Pacific

Asia Pacific reached USD 1.65B 2025 and USD 1.86B 2026, driven by rising biologics production and expanding biosafety testing demand.

U.S.

U.S. is projected at USD 2.39B 2026, driven by strong R&D investment and leadership in innovative therapies.

Japan

Japan is projected at USD 0.37B 2026, driven by expanding biologics development and testing adoption.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Exponential Growth of Biologics, Particularly Cell and Gene Therapies, to Drive Market Growth

With advancements in biologics, such as cell and gene therapy modalities, the need for rigorous, high-frequency safety testing is also increasing, directly driving the global biologics safety testing market growth. The manufacturing steps involved in these next-generation biologics are associated with high contamination risks and require stringent safety testing protocols at every stage of production.

The surge in clinical trials for cell and gene therapies is further pushing demand for validated safety profiling. Additionally, many key players are focusing on technological advancements to support the global demand for biologics safety testing and capitalize on their market position.

- For instance, in August 2025, ViruSure, a global leader in pathogen safety testing for biopharmaceuticals, and Oxford Nanopore Technologies, the company behind a new generation of molecular sensing technology based on nanopores, announced the launch of the industry’s first Good Laboratory Practice (GLP) validated Adventitious Viral Agent (AVA) detection test using nanopore-based sequencing technology. Such critical developments are expected to boost the market's growth.

MARKET RESTRAINTS:

Infrastructure and Talent Constraints to Impede the Market Growth

One of the prominent factors hampering the widespread adoption of these services includes the limited availability of high end infrastructure and specialized talent. These advanced services often require the presence of BSL-2/BSL-3 laboratories, technologically superior downstream processing equipment, robust data-integrity systems, and validated IT infrastructure, which often contributes to increased costs. Additionally, these services and products require upfront capital expenditure, trained professionals with specialized equipment, and strict compliance with regulatory and safety standards, increasing lead times and operational burden. Collectively, these factors increase the implementation costs and slow down adoption, hampering the market growth.

- For instance, in October 2025, Cytiva launched its third Global Biopharma Index and reported that approximately one-third of executives’ experience severe or critical shortages in key areas associated with advanced drug modalities, such as cell and gene therapies, mRNA, and Antibody Drug Conjugates (ADCs), sustainability, manufacturing, digital, and AI skills. These factors adversely impact the market growth.

MARKET OPPORTUNITIES:

Shift toward Rapid and Automated Microbiology Systems to Increase Efficiency and Offer Lucrative Growth Opportunities

One of the prominent opportunities for market growth is the increasing shift toward rapid and automated microbiology systems that offer efficiency in biologics safety testing. These automated systems offer various benefits over traditional methods, such as rapid sterility tests, real-time microbial detection sensors, and AI-enabled colony counters. These features significantly reduce QC timelines, enabling the rapid detection of contamination. These help reduce the turnaround time for biologics with shorter shelf lives, such as cell and gene therapies. Various key companies are partnering to utilize such automated platforms and increase their efficiency.

- For instance, in January 2024, Rapid Micro Biosystems, Inc. partnered with Samsung Biologics, utilizing its Growth Direct platform, for the automation of microbial quality control processes. This partnership aimed to deliver more robust data integrity, increased efficiency, and scalable quality control operations. Such strategic collaboration boosts the market growth.

BIOLOGICS SAFETY TESTING MARKET TRENDS

Shift toward Animal Free Testing is a Prominent Market Trend

One of the prominent trends observed in the market is a shift toward Rapid Microbiological Methods (RMM) and animal-free endotoxin testing assays, as manufacturers strive for more ethical quality testing. Traditional safety testing methods were highly relied on animal-derived components, which raised sustainability concerns. These factors encouraged companies to adopt automated microbial detection platforms and Recombinant Factor C (rFC) endotoxin assays, which reduce testing while simultaneously decreasing reliance on animal-derived components. Major players in the market have increased the adoption of these RMM and recombinant assays. As biologics pipelines expand, these technologies help shorten batch-release cycles, improve consistency, and cement them as a key industry trend.

- For instance, in April 2025, Schrödinger, Inc. supported the U.S. FDA in reducing, refining, or potentially replacing current animal testing requirements with new approaches to improve drug safety and accelerate the evaluation process, while reducing animal experimentation.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Stringent Regulations and High Scrutiny by Regulatory Bodies Pose a Significant Challenge for Market Growth

One of the significant challenges the market faces is the increasing risk of microbial contamination, which results in scrutiny by regulatory bodies. It increases the operational and financial burden on manufacturers. These requirements become more rigorous as biologics and cell-based therapies grow in complexity, mandating more rigorous testing technologies and upgraded facilities. Failure to comply with these guidelines results in delays in approvals and extended timelines for product release.

Moreover, any minor contamination incident triggers immediate regulatory action, halting production, forcing batch destruction, and damaging timelines. These factors slow innovation and restrict the ability of emerging players to scale, thereby restraining the global market growth.

- For instance, in January 2025, the U.S. FDA inspected and issued a warning letter to Sanofi for its Genzyme Corporation drug manufacturing facility. The warning letter summarized deviations from Current Good Manufacturing Practice (CGMP) for Active Pharmaceutical Ingredients (APIs) and other quality failures, including particle characterization and microbial contamination.

Segmentation Analysis

By Products & Services

Services Segment Led the Market with the Escalating Adoption of Cell and Gene Therapy

Based on products & services, the market is segmented into kits & reagents, instruments, and services.

To know how our report can help streamline your business, Speak to Analyst

In 2025, the services segment is anticipated to dominate the global biologics safety testing market share. The growth of the segment is attributed to the increasing adoption of cell and gene therapy as well as the rising trend of outsourcing safety testing services for these innovative technologies. These therapies require complex biologics, advanced infrastructure, GMP-compliant facilities, and other specialized equipment to perform advanced safety testing, which mandates validated methods and regulatory documentation expertise. As regulatory agencies tighten standards, companies increasingly rely on these outsourcing services to perform various safety testing services. Such factors drive the market’s growth.

- For instance, in December 2024, Eurofins PHAST GmbH helped its clients detect and control impurities in pharmaceutical drugs earlier. Such timely delivery of these outsourcing services reduces turnaround time and supports segmental growth.

The kits & reagents segment is anticipated to hold a dominant market share of 39.99% in 2026. On the other hand, the kits & reagents segment is expected to grow at a CAGR of 9.03% during the forecast period.

By Test Type

Strong Demand for Viral Safety Tests to Drive Viral Safety/Adventitious Agents Segment’s Dominance

On the basis of test type, the market is classified into sterility, endotoxin/pyrogen, mycoplasma, bioburden, viral safety/adventitious agents, residual HCP/HCDNA, cell line characterization, and others.

The Virus Safety segment will account for 25.76% market share in 2026. Viral safety testing is the most critical component of biologics manufacturing and safety testing. Regulatory bodies mandate extensive viral safety testing for every stage of production. These viral safety assessments are complex, expensive, and method-intensive to ensure safety. With the rise of research and development in vaccine manufacturing, the semiconductor industry is expected to experience significant growth. These factors have encouraged many key players to invest in new product launches, research and development, and drive the growth of the segment.

- For instance, in September 2023, Charles River Laboratories International, Inc., in collaboration with PathoQuest SAS, published positive results of a seminal study in Vaccine. This study demonstrated that the company’s GMP-grade assay had a greater capability of detecting viral contaminants compared to in vivo assays.

The cell line characterization segment is expected to grow at a CAGR of 9.82% over the forecast period.

By Application

Considerable Demand for Monoclonal Antibodies to Drive Segmental Dominance

Based on application, the market is segmented into monoclonal antibodies (mAbs) & recombinant proteins, vaccines, cell & gene therapies, blood & plasma products, and tissue/stem cell products.

The mAbs & recombinant proteins segment is anticipated to hold a dominant market share of 50.01% in 2026. Viral safety testing is the most critical component of biologics manufacturing and safety testing. Regulatory bodies mandate extensive viral safety testing for every stage of production. These viral safety assessments are complex, expensive, and method-intensive to ensure safety. With the increasing focus on research and development for vaccine manufacturing, the segment is expected to experience significant growth. These factors have encouraged many key players to invest in new product launches, driving the growth of the segment.

- For instance, in August 2024, Cygnus Technologies collaborated with TriLink BioTechnologies to launch Cygnus’ AccuRes Host Cell DNA Quantification Kits. The technology is used to develop an assay that helps produce safer, more stable biotherapeutics, including vaccines.

The vaccines segment is expected to grow at a CAGR of 8.82% over the forecast period.

By End User

Increasing Bioprocessing Activities to Drive the Pharmaceutical & Biotechnology Companies Segmental Growth

Based on end-user, the market is categorized into pharma & biotech companies, CROs/CDMOs, academic & research institutes, and government/regulatory labs.

The pharma and biotech companies segment is poised to dominate the market with a 51.2% share in 2025. The government/regulatory labs segment is expected to lead the market, contributing 53.65% globally in 2026. These companies are primary developers, manufacturers, and commercializers of these biologics and require intensive safety profiling of their candidates. They conduct intensive quality checks in these facilities, in compliance with the guidelines of various regulatory bodies, throughout the development and production process. They operate large manufacturing capacities, conduct various clinical trials, and engage in research and development, thus facilitating the adoption of these safety testing consumables and driving demand. Such factors encourage key companies to expand their biosafety testing centers and acquire GMP certification, which further amplifies their testing volume, strengthening their market dominance.

- For instance, in August 2024, WuXi Biologics inaugurated four manufacturing facilities and the Suzhou Biosafety Testing Center in China, and received Good Manufacturing Practice (GMP) certificates from the European Medicines Agency (EMA).

The CROs/CDMOs segment is expected to grow at a CAGR of 7.46% over the forecast period.

Biologics Safety Testing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Biologics Safety Testing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 2.39 Billion in 2025, representing 37.34% of the global industry, and is expected to reach USD 2.57 Billion in 2026. The region dominated the market with a significant CAGR, due to the presence of a large number of pharmaceutical companies and an expanding pipeline of biologics and cell and gene therapies. These factors drive the demand for biologics safety testing in the market. The U.S. market is projected to reach USD 2.39 billion by 2026. Furthermore, the U.S. is the epicenter of innovative therapies and experiences, with increasing research and development investment intensifying market demand.

- For instance, in October 2024, Abzena expanded its Quality Control (QC) testing capabilities at its cGMP manufacturing site. The new laboratory space enhanced the company’s analytical toolkit for antibodies, offering rapid microbiology release testing and improved scalability through advanced materials separation. Such developments boost the market growth.

Europe

Europe recorded a market size of USD 1.84 Billion in 2025, capturing 28.75% of the global market share, and is projected to reach USD 2. Billion in 2026. This growth is primarily driven by the rise of advanced therapies across Europe and the expansion of biosafety testing capabilities by key players in the region. Backed by these factors, the UK market is projected to reach USD 0.43 billion by 2026, and the Germany market is projected to reach USD 0.48 billion by 2026 and France USD 0.26 billion in 2025.

Asia Pacific

In 2025, Asia Pacific represented USD 1.65 Billion, accounting for 25.78% of the worldwide market, and is projected to grow to USD 1.86 Billion in 2026 and secured the position of the third-largest region in the market. In the region, Japan market is projected to reach USD 0.37 billion by 2026, the China market is projected to reach USD 0.75 billion by 2026, and the India market is projected to reach USD 0.21 billion by 2026.

Latin America

The Latin America market was valued at USD 0.32 Billion in 2025, capturing 5.00% of global revenue, and is estimated to reach USD 0.35 Billion in 2026. Increasing biologics production in the region is expected to drive growth. In the Middle East & Africa, the GCC is anticipated to reach a valuation of USD 0.09 billion in 2025.

Middle East & Africa

Middle East & Africa contributed 3.13% to the global market in 2025, with a valuation of USD 0.2 Billion, and is projected to reach USD 0.22 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Collaborations of Key Players Supported their Leading Positions

The market for biologics safety testing exhibits a concentrated structure, with a few companies actively operating worldwide. These players are actively involved in capacity expansion, new product launches, strategic partnerships, mergers and acquisitions, and geographic expansion. They actively invest in technology advancement and offer a wide array of product offerings for innovative computer vision systems.

Merck KGaA, SGS Société Générale de Surveillance SA, Thermo Fisher Scientific Inc., Waters Corporation, and Lonza are some of the significant players in the market. A comprehensive range of various biological safety testing products and services for the testing of various types of biologics is to contribute extensively to the market share of these companies.

- For instance, in July 2025, Waters Corporation collaborated with BD to combine BD's Biosciences & Diagnostic Solutions business with Waters to combine, creating a life science and diagnostics leader focused on regulated, high-volume testing.

Apart from this, other prominent players in the market include Charles River Laboratories, BD, and others. These companies are undertaking various strategic initiatives, such as investments in R&D to enhance their market presence.

LIST OF KEY BIOLOGICS SAFETY TESTING COMPANIES PROFILED:

- Merck KGaA (Germany)

- SGS Société Générale de Surveillance SA (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- BD (U.S.)

- Sartorius AG (Germany)

- Charles River Laboratories (U.S.)

- Eurofins Scientific (Luxembourg)

- Lonza (Switzerland)

- Waters Corporation (U.S.)

- Reading Scientific Services Ltd (U.S.)

- Abzena (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Charles River Laboratories International, Inc. collaborated with Toxys. The collaboration provided the company with access to ReproTracker, a human stem cell-based in vitro assay that rapidly and reliably identifies developmental toxicity hazards associated with new drugs and chemicals.

- September 2025: Bionique Testing Laboratories LLC (Bionique), a subsidiary of Asahi Kasei, expanded its facility to support drug development further and meet the demand for rapid biosafety testing solutions.

- July 2025: Creative Diagnostics launched its Mammalian HCP ELISA Kits. These advanced assay kits provided sensitive and reliable detection of Host Cell Proteins (HCPs) in biopharmaceutical development and manufacturing processes. They are used to detect and quantify residual host cell proteins that may contaminate biological products during the production process.

- May 2025: Creative Diagnostics launched a highly sensitive T7 RNA polymerase ELISA kit for the detection of biopharmaceutical impurities.

- October 2024: Merck KGaA inaugurated a new biosafety testing facility in Rockville, Maryland, U.S.

- August 2024: Cygnus Technologies collaborated with TriLink BioTechnologies to launch Cygnus’ AccuRes Host Cell DNA Quantification Kits. The technology is used to develop an assay to help produce safer, more stable biotherapeutics, including vaccines.

REPORT COVERAGE

The market analysis provides a comprehensive study of the market size and forecast for all the market segments included in the report. It encompasses details on the market dynamics and trends expected to drive the market during the forecast period. It also provides overviews of technological advancements, product development, key industry developments, mergers and acquisitions, and strategic insights into market growth. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.18% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Products & Services

By Test Type

By Application

By End User

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.00 billion in 2026 and is projected to reach USD 13.13 billion by 2034.

In 2025, the North America market value stood at USD 2.39 billion.

The market is expected to exhibit a CAGR of 8.18% during the forecast period of 2026-2034.

The services segment is expected to lead the market byproducts & services in 2026.

The increasing production of biologics and cell and gene therapy are the key factors driving the market.

Merck KGaA, SGS Société Générale de Surveillance SA, Thermo Fisher Scientific Inc., BD, and Sartorius AG are among the prominent players in the market.

North America dominated the global biologics safety testing market with a market share of 37.34% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us