"Market Intelligence that Adds Flavour to Your Success"

Blue Tea Market Size, Share & Industry Analysis, By Product Type (Loose Leaves, Tea Bags, and Others), By Packaging (Bulk Packaging and Retail Packaging), By Nature (Organic and Conventional), By Distribution Channel (Retail Shops [Supermarkets/Hypermarkets, Discount Stores, Specialty Stores, Online Retail Stores, and Others] and Food Service Providers), and Regional Forecast, 2026-2034

Last Updated: June 08, 2026

| Format: PDF

| Report ID:

FBI114281

Thank you for your interest in the

"United States Medical Devices Market!"

To receive a sample report, please provide the following details:

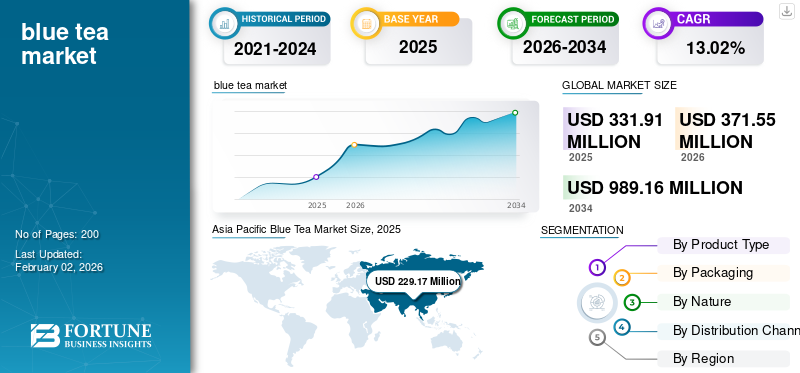

The global blue tea market size was valued at USD 331.91 million in 2025 and is projected to grow from USD 371.55 million in 2026 to USD 989.16 million by 2034, exhibiting a CAGR of 13.02% during the forecast period. Asia Pacific dominated the blue tea market with a market share of 69.05% in 2025.

Blue tea is an herbal-infused tea produced from the butterfly pea flower (Clitoria ternatea) and is gaining global traction owing to health attributes, pleasant appearance, and increased demand for functional drinks. It contains no caffeine, is versatile in blends, and is widely utilized in functional and wellness drinks in home and commercial applications. The product’s expansion via online and international e-commerce channels facilitate penetration into new countries and younger consumers. In January 2025, Blue Tea, India's Shark Tank-starred herbal tea company, marked its growth to reach approximately USD 12 million in annual revenues by the financial year (FY26) as the global wellness market sustains its healthy growth pace. This achievement reflects the brand's continued growth spurt driven by changing consumer trends, strategic collaborations, and phenomenal online performance.

The industry is dominated by key players, such as Blue Tea Co., Dilmah Ceylon Tea Company, Pukka Herbs, Yum Cha Tea Company, Butterfly Pea Co., and others. These players introduce new blends, flavors in terms of herbal, floral, and fruit, adaptogen variants, and functional ingredients to address changing consumer trends and add value to the product.

Asia Pacific dominated the blue tea market with a 69.05% share in 2025, supported by long-standing cultural consumption in Thailand, Malaysia, and Vietnam, along with the rising popularity of functional and natural beverages across the region. By product type, loose leaves held the largest share in 2024 at 53.68%, driven by demand for premium flavor, aroma, and customization preferred by health-conscious consumers and specialty tea enthusiasts.

Key Country Highlights:

United States: The U.S. market was valued at USD 27.29 million in 2024 and is projected to grow significantly, driven by rising demand for natural, functional beverages and expanding retail and online channels. Growth is further supported by strong social media influence, wellness trends, and product innovations introduced by U.S.-based tea brands.

Germany: Germany continues to experience steady adoption of blue tea, driven by health-oriented consumer behavior and expanding café culture that supports premium herbal and specialty tea offerings.

India: India remains a fast-growing market, supported by strong online penetration and the success of brands such as Blue Tea Co., which is expanding rapidly through functional blends, RTD innovations, and increasing presence in retail and cafés.

China: China’s growing interest in herbal and functional teas contributes to rising consumption, supported by a strong tea culture and increasing demand for visually attractive wellness beverages.

Brazil: Brazil’s market is expanding moderately due to growing consumer interest in natural beverages and the influence of global herbal tea trends reaching South American markets.

South Africa: South Africa is witnessing gradual market penetration led by niche consumer segments and increased availability of functional and specialty teas through online and modern retail channels.

Europe: Europe shows consistent growth driven by premiumization, clean-label preferences, and strong café culture across countries such as the U.K.,

Germany, France, Spain, and Italy.

Asia Pacific: Asia Pacific maintains market leadership, supported by centuries-old usage, rising disposable incomes, expanding foodservice sector, and strong demand for functional wellness drinks.

MARKET DYNAMICS

Market Drivers

Popularity of Functional Beverages and Nutrition Provided by Blue Tea Drives its Demand

The demand for blue tea is driven by the increasing consumer preference of functional drinks. Functional drinks such as herbal teas provide health benefits over and above basic nutrition, which fit perfectly with the consumer trend of wellness and health. Blue tea is packed with antioxidants in the form of anthocyanins, providing stress relief, anti-inflammatory properties, and skin care. As health awareness increases among consumers, there is demand for natural, plant-based drinks such as blue tea, which offers general well-being, relaxation of mind, and a distinct visual attraction from its volatile blue color that alters with acidity.

According to the Agriculture and Agri-Food Canada organization, sales of natural fruit/herbal tea in the U.S. increased from USD 584.0 million in 2021 to USD 630.3 million in 2022. The rise in herbal tea sales boosts consumer openness to trying innovative blends such as blue tea, often marketed as premium, functional, and artisanal products.

Market Restraints

Limited Awareness and Raw Material Availability Deter Market Growth

The product awareness and its benefits are still limited beyond Southeast Asia and some Western markets. A lack of exposure to blue tea influences consumers to be reluctant to try it, unlike more established herbal teas such as green tea or matcha. The premium cost of the product, compared to conventional teas further deters price-conscious consumers. Limited knowledge hinders trust, particularly when there are inconsistencies in quality and adulteration because of unregulated supply chains. Additionally, production is constrained in terms of restricted large-scale farming and unstable raw material availability. Recent supply chain disruptions and trade tariffs have also raised procurement expenses and resulted in stock shortages, leading manufacturers to seek alternative sourcing areas.

Market Opportunities

Manufacturers Shift Toward Developing Ready-To-Drink (RTD) Formats Unlock New Opportunities

The market is witnessing a strategic shift as key players are moving toward production of ready to drink (RTD) formats to unlock new growth opportunities. RTD blue tea offerings are gaining popularity since they provide the health benefits of blue tea in an easily consumable form, which appeals to the younger population, consumers who follow an active lifestyle and health-conscious individuals. Major players are capitalizing on these aspects by introducing RTD blue tea offerings to target convenience-driven consumers and tap into increased health awareness.

For instance, in May 2025, Blue Tea, an Indian herbal tea brand, outlined plans to increase its presence in 2026 with the launch of a ready-to-drink (RTD) blue tea and its foray into offline retail outlets and cafés. The initiative would broaden the company's current direct-to-consumer (D2C) business, which has grown significantly since its debut on the reality show Shark Tank India.

Blue Tea Market Trends

Social Media Popularity Coupled with Premium and Clean-Label Positioning Shapes the Industry

Social media sites, particularly Instagram and wellness influencer collaborations, have greatly increased exposure and demand for blue tea by showcasing its health advantages and attractive indigo color, which is specifically of interest to young consumers and health-aware consumers. The high-end positioning of blue tea brands is supported by direct procurement from farmers, fair trade, and organic certifications, which are good reasons for a premium price and enhances consumer confidence. Clean label trends require the demand for pure and natural ingredients without additives, matching consumers' need for transparency and healthier product options in functional drinks such as blue tea.

Richer Flavor and Aroma Created by Loose Leaves Amplifies its Demand

On the basis of product type, the market is sub-segmented into loose leaves, tea bags, and others.

The loose leaves segment is expected to lead the market, contributing 2026 with a 53.63% Share. Loose leaves offer a purer, more authentic tea-drinking experience that appeals to health conscious consumers. Blue tea made with loose leaves retain more natural flavor and vibrant color compared to processed forms such as tea bags, allowing consumers to customize brewing strength and enjoy the unique sensory qualities of butterfly pea flowers.

The tea bags segment is expected to grow significantly in the forecast period with a CAGR of 12.34%.

By Packaging

Growing Foodservice and Hospitality Industries to Lead Bulk Packaging Segment Growth

On the basis of packaging, the market is split into bulk packaging and retail packaging.

The bulk packaging segment is anticipated to hold a dominant market share of 67.88% in 2026. The segment dominates the market due to its cost-effectiveness, maintaining the freshness and quality, and its appeal among tea connoisseurs and premium consumers. Cafes, restaurants, and hotels increasingly provide specialty drinks such as blue tea to cater to increased customer demand for differentiated and functional beverages. Such outlets often buy ingredients in bulk to optimize costs and operations.

The retail packaging segment is expected to grow significantly at a CAGR of 12.38% during the forecast period.

By Nature

Price and Accessibility Fuels Conventional Segment’s Market Leadership

On the basis of nature, the market is segmented into organic and conventional.

The conventional segment is anticipated to hold a dominant market 73.59% share in 2026, primarily because conventional blue tea products are more readily available and competitively priced than organic ones, making them accessible to a wider consumer base. Conventional farming methods yield larger quantities of butterfly pea tea, ensuring a consistent supply and stable pricing. Additionally, established distribution networks and greater consumer familiarity with conventional products help maintain their market stronghold.

The organic segment is anticipated to grow at a CAGR of 14.74% during the forecast period as health-conscious consumer demand represents a smaller share because it is often more expensive and less widely distributed due to farming and certification constraints.

By Distribution Channel

Rapid Disease Control and Cost-Effectiveness Fuels Foliar Application Market Leadership

On the basis of distribution channel, the market is categorized into retail shops and food service providers.

To know how our report can help streamline your business, Speak to Analyst

The retail shops segment is anticipated to hold a dominant market share of 67.85% share in 2026 and is expected to maintain this majority share through the coming years. The segment is further divided into supermarkets/hypermarkets, discount stores, specialty stores, online retail stores, and others. These stores provide convenient product availability for customers who like to shop personally, where products are visually examined before being selected. The channel is suitable for the majority of consumers as it provides immediate buying with the option of comparing the products immediately.

The food service providers segment is anticipated to grow at a CAGR of 12.07% during the forecast period.

Blue Tea Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Blue Tea Market Size, 2025 (USD Million)

In 2025, the Asia Pacific market stood at USD 229.17 million, representing 69.05% of global demand, and is projected to grow to USD 256.13 million in 2026. The blue tea market is currently dominated by Asia Pacific, which accounted for 69.05% of the market share in 2025. Its leadership is fueled by the centuries-old consumption of butterfly pea flower tea in Thailand, Malaysia, and Vietnam, as well as growing consumer awareness of its inclusion of antioxidants and cognitive benefits. Growing disposable incomes, natural and functional drinks trend, and the increasing availability on online platforms also contribute to the blue tea market growth. The Japan market is projected to reach USD 20.82 billion by 2026, the China market is projected to reach USD 68.43 billion by 2026, and the India market is projected to reach USD 36.72 billion by 2026.

North America

North America, though smaller in size, is the leader in growth rate with a CAGR of approximately 14.04% during 2025-2032. The market in North America reached USD 30.9 million in 2025, representing 9.31% of total market revenue, and is projected to reach USD 35.04 million in 2026. Drivers for growth are growing health awareness, demand for natural and functional beverages, and growing retail and online channels. The U.S. market is projected to reach USD 28.67 billion by 2026. The UK market is projected to reach USD 13.11 billion by 2026, and the Germany market is projected to reach USD 15.4 billion by 2026.

Europe

Europe demonstrates consistent growth driven by the trends in health and cafe culture, while South America growing moderately, driven by interest in natural beverages. The Middle East & Africa have greater challenges and relatively slower growth, with gradual market penetration driven by niche consumer segments. Europe contributed approximately USD 55.38 million to the global market in 2025, accounting for 16.69% share, and is expected to reach USD 62.15 million in 2026.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 3.49 million in 2025, accounting for 1.05% share, and is expected to reach USD 3.84 million in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Focus on New Product Launches to Support Market Growth of Key Players

The global blue tea market share is highly fragmented, with a combination of small regional brands and large international players addressing health-aware consumers. Blue Tea Co., Dilmah Ceylon Tea Company, Pukka Herbs, Yum Cha Tea Company, and Butterfly Pea Co. are some prominent companies. The major players are concentrated on product innovation, sourcing high-quality ingredients, and establishing strong brand names.

In August 2025, Bigelow Tea, an American manufacturer of dried teas, expanded its Butterfly Pea Flower Tea line nationwide in the U.S. The new range is designed with high-quality butterfly pea flowers from small, woman-owned farms in Thailand.

October 2024: Octavius, a premium quality Indian tea company, launched Butterfly Blue Pea Flower Tea. The new product is rich in antioxidants, which help reduce stress and anxiety, making it the perfect addition to a daily routine.

October 2024: Bigelow Tea introduced two new caffeine-free herbal teas featuring butterfly pea flower: Butterfly Pea Flower Sapphire Bay and Butterfly Pea Flower Vanilla Midnight. Both highlight the mesmerizing color-changing properties of butterfly pea flowers and are sourced from small, women-owned farms in Thailand.

March 2023: Rishi's Sparkling Botanicals launched a new product, Blue Tea Jasmine. The new range features a vibrant purple color derived from the butterfly pea flower of Thailand. Its natural blue infusion transforms to purple when lemon is added.

December 2020: Purecise launched a new Blue Pea Green Tea. This tea blend combines butterfly blue pea flower with organic Indian green tea. It is noted for its antioxidant properties and is marketed as helping to improve the immune system and detoxify the body.

REPORT COVERAGE

The global blue tea market report analyzes the market in depth and highlights crucial aspects such as market trends, secondary research market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the market analysis and highlights significant industry developments.

The global blue tea market size is projected to grow from $371.55 million in 2026 to $989.16 million by 2034, at a CAGR of 13.02% during the forecast period