Blood Screening Market Size, Share & Industry Analysis, By Product Type (Instruments, and Reagents & Kits), By Technology (Molecular Tests, and Serology Tests), By End User (Independent Clinical Laboratories, Hospital-based Laboratories, and Others), and Regional Forecast, 2026-2034

Blood Screening Market Size and Industry Overview

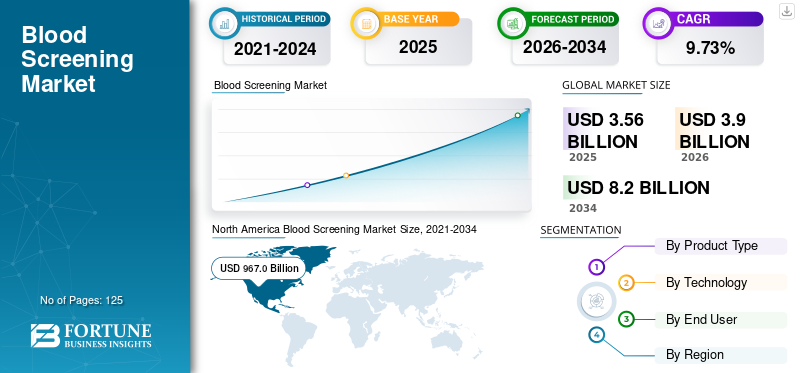

The global blood screening market size was valued at USD 3.56 billion in 2025. The market is projected to grow from USD 3.90 billion in 2026 to USD 8.20 billion by 2034, exhibiting a CAGR of 9.73% during the forecast period. North America dominated the global market with a share of 41.86% in 2025.

Introduction of automated molecular platforms for blood screening has been a growing strategy among leading market players and is subsequently boosting the market growth. Blood screening tests are specifically designed to assure the safety of donated blood units, and to detect any marker of transfusion transmissible infection (TTIs) in the blood.

Increasing number of blood donations and blood donors, increasing awareness regarding safety of donated blood, rising prevalence of infectious diseases combined with several government initiatives are some of the major factors augmenting the growth of the blood screening market.

Download Free sample to learn more about this report.

Blood Screening Market Overview & Key Metrics

Market Size & Forecast:

- 2025 Market Size: USD 3.56 billion

- 2026 Market Size: USD 3.9 billion

- 2034 Forecast Market Size: USD 8.2 billion

- CAGR: 9.73% during the forecast period

Market Share:

- North America dominated the global blood screening market with a 41.86% share in 2025, driven by high awareness of blood safety, strong blood donor participation, advanced healthcare infrastructure, and rapid adoption of molecular screening technologies.

- By product type, Reagents & Kits held the largest share in 2018 and are expected to account for 83.5% of the market by 2025, supported by high test accuracy, cost-effectiveness, and large-volume consumption for blood donation screening.

Key Country Highlights:

- Japan: Market expected to reach USD 208.2 million by 2025, supported by rising patient affordability and increased adoption of molecular testing technologies in blood banks.

- United States: High annual donor participation (around 6.8 million people) and early adoption of automated molecular platforms for transfusion safety underpin market leadership.

- China: Forecast to grow at a strong CAGR of 11.30% during the forecast period due to rising healthcare investment, growing donor pool, and increasing prevalence of infectious diseases necessitating blood safety.

- Europe: Anticipated CAGR of 7.3% with growth driven by adoption of advanced blood screening systems such as Roche’s cobas Zika test for donor blood safety, supported by favorable regulatory approvals.

BLOOD SCREENING MARKET TRENDS

Introduction of Automated Molecular Platforms for Blood Screening to Fuel Growth

Shift from manual to automated screening platforms has been pivotal in rapid detection of transfusion transmissible infections (TTIs) in the blood samples. Increasing automation is expected to eliminate human error during the transfusion screening process. Generally, these screening tests influence a majority of medical decisions made in blood banks and hospitals. For instance, in December 2019, F. Hoffmann-La Roche Ltd announced the CE-IVD launch of ‘cobas’, which detects Zika virus in human plasma and is intended to be used in screening blood donations. Hence, introduction of such automated molecular platforms by key players has subsequently resulted in its increasing adoption in blood donation centers. This is projected to further propel the blood screening market growth during the forecast period.

Download Free sample to learn more about this report.

MARKET DRIVERS

Increasing Number of Blood Donations to Fuel the Demand for Blood Screening

According to the World Health Organization (WHO), an approximate 117.4 million blood donations were collected globally in 2018. This was a result of various initiatives taken by governments and non-profit organizations about blood donation which has led to a tremendous increase in the number of voluntary blood donors and donation campaigns in the past decade. For instance, the Australian Red Cross in 2016 had implemented two initiatives to increase blood donation in the country, first was a SMS alert and second was a toolkit which was used to reduce the anxiety of first time donors, and consequently increased voluntary blood donations in the country.

Along with this, growing awareness concerning blood safety from infectious diseases through several programs is leading to a high demand for blood screening tests worldwide. Increasing cases of accidents and prevalence of chronic disease like cancer is creating a huge demand for blood for treatment of the patient population. It was also validated by various studies that a single victim of a car accident can require up to 100 units of blood and also, while receiving a chemotherapy treatment some of the cancer patients require blood transfusion. Thus, a large patient pool of cancer coupled with an increase in accidental cases are generating a high demand for blood for their treatment and subsequently increasing the adoption of blood screening tests during the forecast period.

MARKET RESTRAINT

High Cost of Instruments and Inadequate Infrastructure for Blood Screening to Limit the Growth in Emerging Countries

Despite an increasing incidence of transfusion-transmissible infections (TTIs), and higher prevalence of HIV, hepatitis B, hepatitis C, syphilis in emerging countries like India, China, and Africa, there are certain factors that are limiting the blood screening market growth. One of the major factors restraining the market growth is lack of spending on healthcare infrastructure in emerging countries for blood screening procedures. Added to this, is the high cost associated with the test instruments and stringent regulatory policies, are some of the factors expected to hamper the growth of the market during the forecast period.

SEGMENTATION ANALYSIS

By Product Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Reagents & Kits Segment Dominated the Market in 2018

Based on product type, the blood screening market is segmented into reagents & kits, and instruments. The reagents & kits are used to detect the presence of disease associated antigens in a blood sample. Also, the segment dominated the market in 2018 due to its high accuracy for blood testing coupled with the cost effectiveness for customers. Despite lower cost of reagents & kits as compared to instruments, higher volume consumption of these for tests, is responsible for the dominant share of the segment in the market.

- By product type, the reagents segment is expected to hold a 83.5% share in 2025.

Besides, the instruments segment is projected to register a comparatively lower CAGR during the forecast period. Reusable nature of these instruments and a longer life cycle associated with these instruments are some of the factors attributed to the slow growth of the segment during 2019-2026.

By Technology Analysis

Clinically Proven Efficiency of NAT tests in Blood Screening to Aid Dominance of the Molecular Tests Segment

In terms of technology, the market is segmented into molecular tests and serology tests. The tests included under serology are used to detect serum antibodies that are associated with certain types of diseases like HIV, Hepatitis B, Hepatitis C, Zika virus, Syphilis, etc. Among serological tests, Enzyme-Linked Immunosorbent Assay (ELISA), Chemiluminescence Immunoassay (CLIA), and western blotting techniques are generally preferred to screen the blood units. The Serology tests segment is expected to grow at a steady CAGR in the forecast period owing to its lower cost in comparison to NAT and other molecular tests and higher adoption of ELISA, and CLIA tests in emerging countries.

- By technology, the molecular test segment is projected to generate USD 2,190.2 million in revenue by 2025.

However, molecular tests occupied a dominant share of the global market in 2018. The dominance is attributed to the high sensitivity of nucleic acid amplification test (NAT) for detection of viral nucleic acids in blood samples. Additionally, NAT test is proved to be clinically effective for early detection of HIV, HBV and HCV virus and hence, is penetrating at a faster pace among the clinical laboratories globally.

By End User Analysis

Independent Clinical Laboratories Segment Held a Dominant Share of the Market in 2018

Increasing number of stand-alone clinical laboratories in developed and emerging countries, coupled with the high expenditure on its infrastructure is leading to more number of blood screening procedures in such facilities. Additionally, increasing partnerships between blood centers and clinical laboratories, is further fueling the adoption of blood screening tests in these settings and thus, driving the growth of the blood screening market during the forecast period.

Similarly, hospital-based laboratories are projected to gain market share by the end of 2026, owing to the increasing number of blood transfusion procedures in these settings. Many hospitals worldwide are also implementing various patient blood management programs to facilitate transfusion and screening practices, primarily to improve patient outcomes, reduce costs, and conserve blood units. Hence, such initiatives by hospitals are expected to drive the growth of this segment during the forecast period.

REGIONAL ANALYSIS

North America Blood Screening Market Size, 2021-2034 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The blood screening market size in North America stood at USD 967.0 million in 2018. The dominance of this region is attributed to the increasing number of blood donors, high adoption of blood screening processes and greater patient affordability. Also, high awareness among people towards blood safety, is responsible for the dominant share of the region in the global market. For instance, according to The American National Red Cross, it was estimated that every year around 6.8 million people in the U.S donate blood. Introduction of new systems with advanced technologies in European market is anticipated to drive the demand for screening systems during the 2019-2026 period.

Europe

- Europe is anticipated to grow at a CAGR of 7.3% during the forecast period.

For instance, in December 2019, F. Hoffmann-La Roche launched its cobas Zika test in Europe, used for screening blood donations. The market in Asia-Pacific is projected to grow at a faster pace during the forecast period. Increasing investment by key players in emerging markets, expected regulatory approvals, rising patient affordability are anticipated to drive the demand for blood screening in Asia Pacific during the forecast period.

- The blood screening market in Japan is expected to reach USD 208.2 million by 2025.

- China is projected to witness a strong CAGR of 11.30% during the forecast period.

Latin America and the Middle East & Africa

Also, Latin America and the Middle East & Africa accounts for comparatively lower market share owing to presence of large underpenetrated markets among these regions. Thus, it is expected to register a comparatively lower CAGR during the forecast period.

KEY INDUSTRY PLAYERS

Grifols, S.A., and F. Hoffmann-La Roche Ltd., Dominated the Global Market in 2018

A diversified product portfolio of diagnostic systems, along with acquisitions and constant innovations by the company leading to new system launch are major factors responsible for the market position of the Grifols, S.A. For instance, in January 2017, Grifols, S.A. acquired Hologic’s manufacturing plant that was engaged in development of instruments based on NAT technology and was used in transfusion screening.

However, other key players such as F. Hoffmann-La Roche, Bio-Rad Laboratories, Inc., BD, QUOTIENT, Abbott, Beckman Coulter, Inc., and DiaSorin S.p.A. have entered in the blood screening market competition with innovative transfusion screening systems. This is projected to positively impact the market as these companies are anticipated to increase their market share during the forecast period.

LIST OF KEY COMPANIES PROFILED:

- Bio-Rad Laboratories, Inc.

- Grifols, S.A.

- F. Hoffmann-La Roche

- Ortho Clinical Diagnostics

- BD

- DiaSorin S.p.A.

- Thermo Fisher Scientific Inc.

- Abbott

- QUOTIENT

- Other Players

KEY INDUSTRY DEVELOPMENTS:

- Grail, an American biotechnology and pharmaceutical company, announced the launch of the Galleri blood test, the company’s innovative multi-cancer screening diagnostic capable of detecting the presence of multiple cancers. This test will help the company screen around 50 million people after its launch and pursue a full FDA approval by 2023.

- Tzar Labs, a molecular diagnostic company and Epigeneres Biotechnology, announced early-detection cancer tests. This test will help determine the different stages of the disease and will be launched by the end of this year. The company’s accuracy rates are very high for screening tests of cancer and had shown results for all types of cancers.

- B.D. (Becton, Dickinson, and Company) a prominent worldwide medical technology company and BioMedomics announced the release of a new point-of-care test that can detect antibodies in blood to verify current or past exposure to COVID-19 in less than 15 minutes.

- Siemens Healthineers announced shipping worldwide its laboratory-based total antibody test1 to detect the presence of SARS-CoV-2 IgM and IgG antibodies in the blood. The complete antibody test permits the identification of patients who have developed an adaptive immune response.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The blood screening market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over the recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product Type

|

|

By Technology

|

|

|

By End User

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global blood screening market was valued at USD 3.9 billion in 2026 and is projected to reach USD 8.2 billion by 2034, growing at a steady pace due to rising demand for safe blood transfusions and advancements in screening technologies.

The blood screening market is expected to expand at a compound annual growth rate (CAGR) of 9.73% between 2026 and 2034.

Blood screening primarily uses two types of technologies: molecular tests, such as NAT, which are highly sensitive for detecting infections at an early stage, and serology tests, including ELISA and CLIA, which remain widely adopted for broader screening due to cost-effectiveness.

Reagents & kits is expected to be the leading segment in this market during the forecast period.

Globally, increasing number of blood donations is fuelling the demand for blood screening tests.

Grifols, S.A., F. Hoffmann-La Roche, BD, DiaSorin S.p.A. are some of the companies included in the blood screening market.

North America dominated the market share in 2025.

Increasing number of blood donations coupled with increasing prevalence of transfusion-transmissible infections (TTI’s) are expected to drive the adoption of blood screening tests.

- 2021-2034

- 2025

- 2021-2024

- 125

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us