Canned Alcoholic Beverages Market Size, Share & Industry Analysis, By Product Type (Canned Beer, Canned Wine, Canned Cocktail, and Others), By Alcohol Type (Malt-Based, Spirit-Based, and Wine-Based), By Alcohol Content (Low ABV (Below 5%), Medium ABV (5–10%), and High ABV (Above 10%)), By Distribution Channel (On-Trade and Off-Trade), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

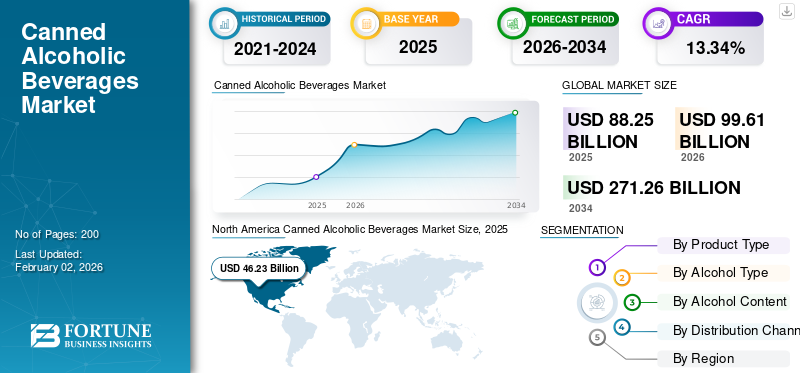

The global canned alcoholic beverages market size was valued at USD 88.25 billion in 2025. The market is projected to grow from USD 99.61 billion in 2026 to USD 271.26 billion by 2034, exhibiting a CAGR of 13.34% during the forecast period. North America dominated the Canned Alcoholic Beverages Market with a market share of 52.39% in 2025.

Canned alcoholic beverages include ready-to-drink (RTD) cocktails, hard seltzers, canned wines, and spirits-based drinks, all packed in metal cans for convenience, sustainability, and portability. The global market growth is driven by shifting consumer lifestyles, rising demand for low-alcohol and innovative flavors, as well as the adoption of sustainable packaging solutions. The global canned alcohol beverages appeal to Millennials and Gen Z consumers seeking convenient, portable, and trendy beverage options. Furthermore, premiumization, eco-friendly aluminum packaging, and online retail availability have significantly boosted global consumption.

The global market is dominated by key players, including Anheuser-Busch InBev SA/NV, Diageo plc, Pernod Ricard SA, Brown-Forman Corporation, Asahi Group Holdings, Ltd., and others.

Download Free sample to learn more about this report.

Canned Alcoholic Beverages MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 88.25 billion

- 2026 Market Size: USD 99.61 billion

- 2034 Forecast Market Size: USD 271.26 billion

- CAGR: 13.34% from 2026–2034

- North America dominated the canned alcoholic beverages market with a 52.39% share in 2025.

- Canned beer segment led the market with a 45.71% share in 2026.

- Malt-based segment dominated the market with a 52.93% share in 2026.

North American

North America generated USD 46.23 billion in 2025, driven by strong demand for RTD beverages and premium alcohol formats.

Europe

Europe shows steady growth supported by premiumization trends and strong demand in the U.K., Germany, and France.

Asia Pacific

Asia Pacific reached USD 16.39 billion in 2025, driven by urbanization and rising adoption of canned RTD cocktails.

U.S.

Market expected to reach USD 43.46 billion in 2026, led by strong hard seltzer and RTD cocktail consumption.

Japan

Market projected to reach USD 2.88 billion in 2026, supported by growing acceptance of canned alcoholic beverages.

Read More

MARKET DYNAMICS

Market Drivers

Rising Popularity of Ready-to-Drink (RTD) and Convenient Alcoholic Formats to Drive Market Growth

The rising popularity of Ready-to-Drink (RTD) and convenient alcoholic beverage formats is a key driver of global canned alcoholic beverages market growth. RTDs are premixed and packaged, allowing consumers to enjoy cocktails, mixed drinks, and flavored alcoholic beverages straight from the can or bottle without preparation. This ease of consumption suits busy, on-the-go lifestyles, outdoor events, social gatherings, and travel, thereby fueling the global demand for the canned alcoholic market.

- According to a DISCUS Annual Economic Briefing, premixed cocktails, including spirit-based RTDs, in the U.S. saw significant revenue growth of 26.8% in 2023 compared to the previous year, reaching USD 2.8 billion.

Market Restraints

Stringent Alcohol Regulations and Taxation to Impede Market Growth

Stringent alcohol regulations and taxation are significant challenges hampering the growth of the global canned alcoholic beverages market. Many countries impose strict laws on the production, distribution, advertising, and sale of alcoholic beverages, especially RTDs and canned formats, to address public health concerns. Age restrictions, labeling requirements, and limits on alcohol content can restrict market access and product innovation.

- For instance, in India, state-level taxation results in price disparities of up to 40%, while in Europe, excise taxes on RTDs are often higher than those on beer.

Market Opportunities

Growth of E-Commerce and Direct-to-Consumer (DTC) Channels to Unlock New Growth Opportunities

The growth of e-commerce and Direct-to-Consumer (DTC) channels is creating significant new opportunities in the global canned alcoholic beverages market. E-commerce platforms enable brands to reach broader geographic markets, including consumers in regions where physical stores may be limited. DTC channels allow for direct customer engagement and bypass traditional retail intermediaries. The shift toward digital retail, accelerated by the COVID-19 pandemic, continues, with increased acceptance of buying alcohol online. Younger demographics, especially Millennials and Gen Z, demonstrate a strong preference for digital shopping and brand interaction.

Canned Alcoholic Beverages Market Trends

Innovation in Flavors and Low-Alcohol Variants to Shape Industry

Innovation in flavors and the development of low-alcohol variants are prominent recent trends driving growth and diversification in the global canned alcoholic beverages market. Brands are introducing a wide variety of novel and sophisticated flavor profiles to appeal to evolving consumer preferences and tastes. This includes botanical infusions, exotic fruit blends, spiced variations, herbal and floral notes, and globally inspired cocktail flavors. Such innovation attracts both adventurous consumers and those seeking premium, bar-quality experiences in convenient canned formats.

- For instance, in August 2025, Malibu, a brand owned by Pernod Ricard, partnered with Dole, a producer of fresh fruit and vegetables, to launch a new line of ready-to-drink (RTD) cocktails set to debut in the U.S. market in early 2026. The product lineup would include a variety of 8-packs of 12-oz cans with four flavors, including pineapple, pineapple mango, pineapple strawberry, and pineapple dragon fruit

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Longstanding Popularity to Lead Canner Beer Segment’s High Market Proportion

Based on product type, the market is segmented into canned beer, canned wine, canned cocktails, and others.

The canned beer segment holds the largest global canned alcoholic beverages market share, with a 46.02% share in 2024 and a projected compound annual growth rate CAGR of 12.67% through 2025-2032. Beer is one of the oldest and most widely consumed alcoholic beverages globally, with a deeply established consumer base across diverse regions and demographics, resulting in large and consistent demand. The canned beer segment is projected to dominate the market with a share of 45.71% in 2026.

The canned cocktail segment is expected to grow significantly during the forecast period with a CAGR of 13.90% from 2026 to 2034.

By Alcohol Type

Flavor Versatility and Innovation to Lead Malt-based Segment Growth

Based on alcohol type, the market is segmented into malt-based, spirit-based, and wine-based.

The malt-based category remains the largest contributor to market value in 2025, accounting for over 53.41% of global revenue, owing to its affordability and established production infrastructure. Malt beverages serve as a versatile base for flavor innovation, encompassing non-alcoholic malt drinks, flavored malt coolers, and alcoholic malt beverages, including malt beers and ciders. This variety appeals to consumers seeking diverse taste options and low-alcohol-by-volume (ABV) drinks. The malt-based segment is projected to dominate the market with a share of 52.93% in 2026.

The spirit-based segment is expected to grow significantly at a CAGR of 13.93% during the forecast period.

By Alcohol Content

Socially Acceptable and Rising Health Consciousness to Fuel Low ABV (Below 5%) Segment Market Leadership

On the basis of alcohol content, the market is segmented into low ABV (Below 5%), medium ABV (5–10%), and high ABV (Above 10%).

The low ABV (Below 5%) segment accounted for the largest revenue share in 2024 and is expected to maintain dominance with a higher CAGR of 12.66% through 2032. Low-ABV drinks attract a wider range of consumers, including those who do not typically consume stronger alcoholic beverages. They are more socially acceptable for varied occasions, including daytime and casual social settings. Moreover, increasing consumer health consciousness drives demand for lower-alcohol options that allow enjoyment with fewer calories, less intoxication risk, and milder effects, further fueling the segment’s growth. The medium ABV (5–10%) segment is expected to lead the market, contributing 47.11% globally in 2026.

The medium ABV (5–10%) segment is anticipated to grow at a CAGR of 13.43% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Off-Trade Segment Dominated Market as it Offers Convenience and Accessibility

On the basis of the distribution channel, the market is segmented into on-trade and off-trade.

The off-trade segment, which includes retail stores, supermarkets, convenience stores, and online platforms, dominated global sales with a market share of 62.89% in 2024 and is projected to grow at a CAGR of 13.29% through 2032. The surge in home consumption, online retailing, and convenience store distribution has significantly boosted off-trade demand. The off-trade segment will account for 63.15% market share in 2026.

The on-trade segment is expected to grow at a CAGR of 12.67% during the forecast period for the global canned alcoholic beverages market.

Canned Alcoholic Beverages Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, the Middle East and Africa.

NORTH AMERICA

North America Canned Alcoholic Beverages Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 46.23 billion in 2025, representing 52.39% of the global market landscape, and is expected to reach USD 51.9 billion in 2026. The market is expected to grow at a CAGR of around 52.39% over the forecast period. Growth is driven by high consumer spending on alcohol, strong preference for RTD beverages, and innovation in packaging and flavors. The U.S. market leads due to widespread adoption of hard seltzers and premium rtd cocktails. The U.S. market is projected to reach USD 43.46 billion by 2026.

EUROPE

Europe holds a significant market share, driven by increasing consumer demand for convenience beverages and premium products. The CAGR is in the range of 12.71%, fueled by developments in packaged alcohol beverages, particularly in the U.K, Germany, and France. Europe offers moderate to strong growth, supported by mature alcohol markets shifting to newer formats and premiumisation. The UK market is projected to reach USD 5.59 billion by 2026, while the Germany market is projected to reach USD 3.87 billion by 2026.

ASIA PACIFIC

Asia Pacific accounted for USD 16.39 billion in 2025, representing 18.57% of the global market share, and is projected to reach USD 18.8 billion in 2026. The market is the fastest-growing regional market, with a CAGR of 18.57%. Asia Pacific is set to be a dynamic region for canned alcoholic beverages, driven by rising disposable incomes, growing urbanization, increasing acceptance of Western-style RTD cocktails and hard seltzers, and tourism/outdoor consumption culture. Many emerging markets, including India, China, and Southeast Asia, still have lower per-capita alcohol consumption in canned formats, indicating potential growth. The Japan market is projected to reach USD 2.88 billion by 2026, the China market is projected to reach USD 7.97 billion by 2026, and the India market is projected to reach USD 1.79 billion by 2026.

SOUTH AMERICA and MIDDLE EAST & AFRICA

South America exhibits moderate growth, driven by increasing urbanization and lifestyle changes that promote the consumption of canned alcohol beverages. The CAGR is estimated to be around 13.85%. Growth is faster in the Middle East & Africa due to an increase in alcohol consumption in selected countries, such as the UAE, with a CAGR growth of 14.19%. In 2025, Middle East & Africa held 1.33% of the global market, reaching a valuation of USD 1.18 billion, and is projected to grow to USD 1.34 billion in 2026.

LATIN AMERICA

Latin America contributed approximately USD 4.44 billion to the global market in 2025, accounting for 5.03% share, and is expected to reach USD 5.05 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Focus on New Product Launch and Packaging Innovation to Support Market Growth

Key players in the canned alcoholic beverages market include major global beverage alcohol companies that are increasingly investing in canned RTDs, hard seltzers, and other canned formats. Major players included Diageo plc, Pernod Ricard, Asahi Group Holdings, Ltd., and Bacardi Limited. There is competition from craft/independent producers entering canned formats, as well as premium brands and novel flavor and packaging innovations.

Key Players in the Canned Alcoholic Beverages Market

|

Rank |

Company Name |

|

1 |

Anheuser-Busch InBev SA/NV |

|

2 |

Diageo plc |

|

3 |

Pernod Ricard SA |

|

4 |

Brown-Forman Corporation |

|

5 |

Asahi Group Holdings, Ltd. |

List of Key Canned Alcoholic Beverages Companies Profiled

- Anheuser-Busch InBev SA/NV (Belgium)

- Diageo plc (U.K.)

- Pernod Ricard SA (France)

- Brown-Forman Corporation (U.S.)

- Asahi Group Holdings, Ltd. (Japan)

- Constellation Brands, Inc. (U.S.)

- Bacardi Limited (Bermuda)

- Mark Anthony Brands International (Canada)

- Heineken N.V. (Netherlands)

- Molson Coors Beverage Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Smirnoff introduced three bold new vodka flavors tailored specifically for Indian palates: Minty Jamun, Mirchi Mango, and Zesty Lime. These flavors are designed to resonate with the evolving tastes and cultural preferences of young Indian consumers, particularly Gen Z and millennials, who favor casual social gatherings and home cocktail culture over traditional drinking events.

- January 2025: TÖST Beverages launched a new canned format in the U.S. in early 2025, expanding from their established glass bottle offerings (750ml and 250ml) to a convenient 250ml can format. This launch was timed to align with Dry January and targets consumers seeking a portable, easy-to-enjoy non-alcoholic sparkling beverage suitable for occasions where glass is impractical, such as beaches, boats, concerts, and tailgates.

- March 2025: The Coca-Cola Company unveiled new spirit-based extensions of its Minute Maid brand through its alcohol subsidiary, Red Tree Beverages, marking a significant expansion into the ready-to-drink (RTD) alcoholic beverage market. These new offerings include vodka-infused versions of Minute Maid Lemonade and Pink Lemonade, both featuring 5% alcohol by volume and a non-carbonated formulation, catering to consumers looking for convenient, flavorful, and refreshing RTD cocktails without carbonation.

- December 2024: Suntory expanded its U.S. ready-to-drink (RTD) portfolio, with the launch of MARU-HI, a Japanese-inspired sparkling cocktail brand. The drinks come in flavors such as traditional citrus, strawberry, pineapple, and kiwi, each with 5% ABV, roughly 128 calories, and fewer than 8 grams of carbs per 12-ounce can.

- December 2024: The Coca-Cola Company agreed to acquire Billson’s, a premium Australian ready-to-drink (RTD) alcohol brand known for its popular products, including Vodka with Tangle, Vodka with Grape Burst, and Vodka with Portello. The acquisition allowed Coca-Cola to expand its presence in the growing and dynamic Australian alcoholic RTD market.

REPORT COVERAGE

The global canned alcoholic beverages market report analyzes the market in depth and highlights crucial aspects such as global market trends, secondary research market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.34% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Alcohol Type

|

|

|

By Alcohol Content

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 88.25 billion in 2025 and is anticipated to reach USD 271.26 billion by 2034.

At a CAGR of 13.34%, the global market will exhibit steady growth over the forecast period.

By distribution channel, the off-trade segment leads the market.

North America held the largest market with a share of 52.39% in 2025.

The rising popularity of ready-to-drink (rtd) and convenient alcoholic formats to drive the market growth.

Anheuser-Busch InBev SA/NV, Diageo plc, Pernod Ricard SA, Brown-Forman Corporation, and Asahi Group Holdings, Ltd. are the leading companies in the market.

Innovation in flavors and low-alcohol variants is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us