Cardiac Resynchronization Therapy Market Size, Share & Industry Analysis, By Product (CRT-Defibrillator and CRT-Pacemakers), By Application (Heart Failure Management, Arrhythmia Management, and Others), By End-user (Hospitals and ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

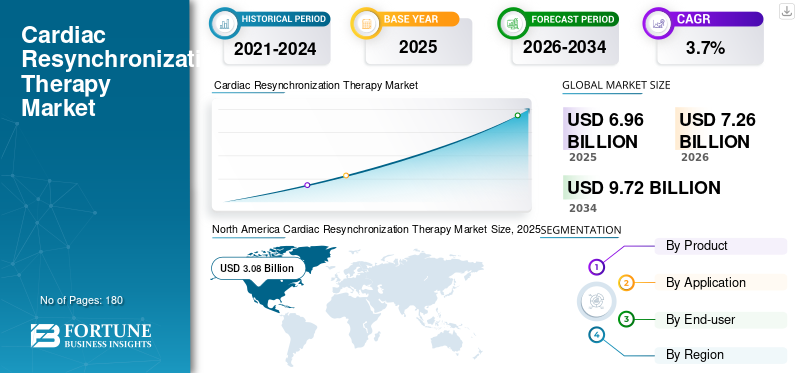

The global cardiac resynchronization therapy market size was valued at USD 6.96 billion in 2025. The market is projected to grow from USD 7.26 billion in 2026 to USD 9.72 billion by 2034, exhibiting a CAGR of 3.7% during the forecast period. North America dominated the global cardiac resynchronization therapy market with a market share of 44.25% in 2025.

Cardiac resynchronization therapy (CRT) is an implantable pacing therapy designed to re-coordinate the heart’s pumping in patients whose ventricles beat out of sync, most commonly in advanced heart failure with electrical dyssynchrony. By delivering precisely timed impulses typically to both ventricles, CRT can improve symptoms, exercise capacity, and, in selected patients, survival. The market is growing as health systems diagnose heart failure earlier and expand access to device-based therapies, while manufacturers continue to improve longevity, connectivity, and patient management workflows. The rising burden of heart failure remains the central driver of demand.

- For example, HF Stats 2025 estimates ~6.7 million Americans over age 20 live with heart failure, with prevalence expected to increase in the coming years.

Medtronic plc, Abbott, Boston Scientific, and BIOTRONIK SE & Co. KG held dominance, attributed to surging investments and planned initiatives, including new product introductions, alliances, and partnerships.

Download Free sample to learn more about this report.

Cardiac Resynchronization Therapy Market Key Takeaways

- 2025 Market Size: USD 6.96 billion

- 2026 Market Size: USD 7.26 billion

- 2034 Forecast Market Size: USD 9.72 billion

- CAGR: 3.7% from 2026-2034

- North America dominated the cardiac resynchronization therapy market with a 44.25% share in 2025.

- The arrhythmia management segment is projected to hold an 80.0% share in 2026.

- The specialty clinics segment is set to hold a 90.6% share in 2026.

North America

North America led with USD 3.08 billion in 2025, driven by advanced cardiac care infrastructure.

Europe

Europe is projected at USD 1.85 billion in 2026, supported by rising cardiovascular disease cases.

Asia Pacific

Asia Pacific is expected at USD 0.53 billion in 2026, driven by improving healthcare access.

U.S.

USD 2.92 billion in 2026, supported by high adoption of advanced cardiac devices.

Japan

USD 0.29 billion in 2026, driven by an aging population and cardiac care demand.

Read More

CARDIAC RESYNCHRONIZATION THERAPY MARKET TRENDS

Device Connectivity, Remote Follow-Up, and Smarter Therapy Optimization Likely to Boost Overall Market

The CRT market is increasingly shaped by what happens after implantation. Providers want systems that reduce clinic burden while maintaining high-quality follow-up, especially as heart failure volumes rise and electrophysiology workforces remain constrained. Remote monitoring and app-based connectivity are becoming default expectations, not premium add-ons, as they can streamline alerts, reduce routine visits, and support earlier intervention when patients destabilize. Continuous remote monitoring reflects the broader industry's move toward consumer-style communication and “always-on” device surveillance.

Another visible trend is the push toward approaches that support more physiologic activation and broader feasibility in complex cases, as seen in the growing interest in conduction-system pacing concepts and devices engineered to fit new implant techniques. Finally, guidelines continue to influence trend lines by reinforcing systematic, evidence-based selection and follow-up, such as a guideline update that anchors heart failure pathways where device therapy is considered alongside modern pharmacotherapy.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Guideline-Based Eligibility and a Growing Heart Failure Pool are Likely to Boost the Overall Market

The cardiac resynchronization therapy market growth is primarily driven by the steady increase in heart failure cases and by clearer, guideline-led decision-making that pushes eligible patients toward device evaluation rather than prolonged “watchful waiting.” As heart failure programs mature, referrals increasingly come from multidisciplinary teams that coordinate imaging, guideline-directed medical therapy optimization, and electrophysiology assessment, helping reduce the number of missed CRT candidates. This is reinforced by professional guidance that continues to update how clinicians stage and treat heart failure, including when to escalate to device-based care.

In Europe, the 2021 ESC heart failure guideline similarly provides detailed recommendations across diagnosis, pharmacotherapy, and device therapy, helping standardize decision-making across diverse care settings. Demand is also supported by the broader cardiovascular burden tracked by major statistical bodies; the American Heart Association published its 2024 Heart Disease and Stroke Statistics, underscoring persistent cardiovascular morbidity and the long runway for heart failure-related care capacity.

MARKET RESTRAINTS

High Procedural Complexity, Variable Response, and Total Cost of Care, which is Likely to Limit Market Growth

Even when patients are clinically eligible, CRT is not a “simple add-on” therapy. Implantation requires specialized operators, careful lead placement, and post-implant optimization, often through repeated follow-ups and programming. These requirements translate into higher procedural and infrastructure costs versus standard pacing and can slow adoption in price-sensitive systems. Another practical restraint is that outcomes can vary: a meaningful subset of patients do not respond as expected, and clinicians must invest time to troubleshoot issues such as suboptimal lead position, scar-related non-capture, atrial fibrillation management, or suboptimal biventricular pacing percentages.

Device and lead complications, while continually reduced by better tools and training, still influence physician and payer confidence, especially in regions with limited access to high-volume centers. On the commercial side, adoption can be constrained when next-generation features raise unit prices faster than reimbursement updates, pushing hospitals to ration implants or delay upgrades. As a reminder of how closely market momentum can align with reimbursement and procurement realities, many manufacturers now highlight remote monitoring and workflow efficiency to help providers manage long-term follow-up costs.

MARKET OPPORTUNITIES

Serving Non-traditional Candidates and Hard-to-Treat Anatomies with Newer CRT Approaches to Create Significant Growth Opportunities

A major opportunity lies in expanding the use of effective CRT to patients who are difficult to treat with conventional coronary sinus lead placement, including those with challenging venous anatomy, prior infections, or failed prior CRT attempts. Leadless and alternative pacing strategies can open a new addressable segment by improving feasibility and potentially enabling more physiologic activation patterns in select patients.

Beyond technology, opportunities are emerging in care models, such as better remote monitoring, earlier identification of decompensation signals, and tighter coordination between heart failure clinics and electrophysiology teams, which can reduce missed referrals and improve time-to-therapy. As access expands, the fastest “white space” remains outside mature markets, such as building implant capacity, training pathways, and structured referral networks, which can materially increase CRT penetration in parts of Asia Pacific, Latin America, and the Middle East & Africa where eligible patients are under-treated.

MARKET CHALLENGES

Uneven Infrastructure, Workforce Constraints, and Reimbursement Differences across Countries Complicate Market Growth

Even when the clinical case for CRT is strong, real-world delivery depends on whether a region has enough implanting sites, trained allied professionals, and funding mechanisms that support both the procedure and long-term follow-up. Infrastructure gaps can cap volumes, while reimbursement variability can shift device mix and delay upgrades. Europe is a good illustration of how access can vary within a generally advanced region. The ESC-EHRA Atlas paper published in the 2025 edition reported a median of 3.3 hospitals per million performing EP/CIED procedures and also flagged obstacles to guideline implementation, such as shortages of allied professionals and dissatisfaction with reimbursement systems, as well as practical constraints that directly affect CRT throughput and follow-up capacity. At the same time, ESC eAtlas data on CRT implantations show wide differences by country and year, reinforcing that “global” demand is not limited by need alone but by delivery capability and funding.

Segmentation Analysis

By Product

CRT-Defibrillator to Lead Market Due to Its Growing Usage in Ischemic Cardiomyopathy and Higher-risk Profiles

Based on product, the market is segmented into CRT-Defibrillator and CRT-Pacemakers.

CRT-Defibrillator is expected to hold a larger share, as many CRT candidates also carry an elevated risk of malignant ventricular arrhythmias, making “resynchronization plus defibrillation” a compelling one-procedure solution. In markets with broader reimbursement, clinicians often prefer CRT-D for eligible patients where sudden cardiac death prevention remains a priority, particularly in ischemic cardiomyopathy and higher-risk profiles.

The CRT-Pacemakers segment is projected to grow at a CAGR of 5.7% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Wide Utilization of CRT Products in Heart Failure Management Propels Segment Growth

By application, the market is classified into heart failure management, arrhythmia management, and others.

Heart failure management dominates as CRT’s primary clinical role is to improve mechanical efficiency in patients with symptomatic heart failure and dyssynchrony, thereby reducing symptoms and supporting functional improvement when optimized medical therapy is insufficient. In practice, CRT is embedded within heart failure pathways that include imaging, medication optimization, and specialist referral, so most implants are directly tied to heart failure programs rather than “arrhythmia-only” care. Moreover, the segment is projected to hold an 80.0% share in 2026.

The arrhythmia management segment is estimated to grow at a CAGR of 1.7% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals & ASCs Propels Segment Growth

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, and others.

Hospitals and ASCs account for the largest cardiac resynchronization therapy market share as CRT implantation requires a sterile procedural environment, imaging and device-testing capabilities, emergency cardiac backup, and specialized electrophysiology teams. Post-implant care, such as programming, optimization, and complication management, also typically falls within hospital-based device clinics or affiliated networks, reinforcing hospital dominance even as parts of care shift to the outpatient setting. Furthermore, the segment is set to hold a 90.6% share in 2026.

The specialty clinics segment is projected to grow at a CAGR of 6.2% during the forecast period.

Cardiac Resynchronization Therapy Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cardiac Resynchronization Therapy Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 2.97 billion, and is expected to reach USD 3.08 billion in 2025. Growth in North America is being driven by a large and growing heart failure population, strong referral pathways, and faster adoption of technologies that improve long-term follow-up. The region also benefits from mature implant infrastructure, which supports replacement demand and steady upgrades. On the innovation side, new options for patients previously considered “hard-to-treat” can expand the treated population.

U.S. Cardiac Resynchronization Therapy Market

In 2026, the U.S. market is forecasted to represent USD 2.92 billion, capturing 40.2% of total global revenue.

Europe

Europe is expected to achieve a 2.9% growth rate in the coming years, the second-highest globally, reaching USD 1.85 billion by 2026. Structured guideline-led care pathways support Europe’s growth, broad hospital-based EP infrastructure, and continued efforts to reduce inter-country treatment gaps. Ongoing modernization of device follow-up also helps expand capacity as implant volumes rise. Moreover, growth is also supported by continued refresh cycles and upgrades in high-volume centers. At the same time, Central & Eastern Europe and parts of Southern Europe provide additional upside as access improves.

U.K. Cardiac Resynchronization Therapy Market

The U.K. market is projected to reach USD 0.26 billion by 2026, accounting for 3.5% of the global market revenue.

Germany Cardiac Resynchronization Therapy Market

Germany's market is forecasted to reach about USD 0.37 billion by 2026, representing roughly 5.1% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 0.53 billion, ranking as the third-largest globally. Asia Pacific typically grows faster as CRT penetration is still catching up with clinical need, and the region continues to add implant capability, such as more trained operators, more implanting sites, and improved reimbursement in select markets. Technology tailored to evolving implant techniques is also helping drive adoption, particularly as physicians seek more physiologic pacing strategies.

Japan Cardiac Resynchronization Therapy Market

Japan is projected to generate approximately USD 0.29 billion in revenue by 2026, contributing nearly 4.0% to the global market.

China Cardiac Resynchronization Therapy Market

China’s market is expected to reach approximately USD 0.52 billion by 2026, contributing about 7.1% to global revenues.

India Cardiac Resynchronization Therapy Market

India is predicted to contribute approximately USD 0.15 billion to the market by 2026, corresponding to about 2.1% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to witness moderate market growth. Latin America is expected to reach around USD 0.45 billion by 2026. Latin America’s growth is driven by improving access to electrophysiology services, gradual expansion of implanting centers in major metros, and increasing awareness/referral for advanced heart failure therapies. Moreover, the Middle East & Africa market growth is shaped by two factors: high-capability hubs expanding advanced cardiac care, and broader regions gradually building infrastructure and referral pathways.

GCC Cardiac Resynchronization Therapy Market

By 2026, the GCC is expected to generate approximately USD 0.10 billion in the market, accounting for nearly 1.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce Market Position of Prominent Players

The CRT market is highly consolidated and technology-led. A small group of global cardiac rhythm management (CRM) manufacturers controls most generator volumes, largely as CRT systems require deep capabilities across high-voltage/low-voltage platforms, leads, programmer ecosystems, remote monitoring infrastructure, and long clinical validation cycles. Medtronic, Abbott, and Boston Scientific anchor much of the premium segment globally, with BIOTRONIK SE & Co. KG and MicroPort Scientific providing strong alternatives in select geographies.

Other key players, such as EBR Systems, MEDICO S.p.A., and OSYPKA, compete through ongoing technological advancements, the growing demand for improved healthcare infrastructure, and efforts to improve therapy outcomes.

LIST OF KEY CARDIAC RESYNCHRONIZATION THERAPY COMPANIES PROFILED

- Medtronic plc (Ireland)

- Abbott (U.S.)

- Boston Scientific (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- MicroPort Scientific (France)

- EBR Systems (U.S.)

- MEDICO S.p.A. (Italy)

- OSYPKA (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2025: The FDA granted Premarket Approval (PMA) to EBR Systems for its WiSE CRT System, marking it as the world’s first leadless left ventricular endocardial pacing device for cardiac resynchronization therapy (CRT).

- July 2024: BIOTRONIK announced Amvia Sky launch in Canada, highlighting CRT-P features and workflow tools. First Implant of Amvia Sky in Canada Performed at the Centre Hospitalier de l'Université de Montréal

- April 2024: MicroPort CRM launched TALENTIA & ENERGYA ICD/CRT-D ranges in Europe, including connectivity/workflow positioning.

- March 2024: BIOTRONIK announced a complete CSP system, fully CE-approved for LBBAP, including tools for physiologic pacing alternatives to conventional BiV CRT in some patients.

- February 2024: MicroPort CRM announced the launch of GALI SonR CRT-D and NAVIGO 4LV LV pacing leads in Japan.

- January 2024: MicroPort CRM reported dual CE marks (MDR) for TALENTIA & ENERGYA ICD/CRT-D ranges and programmer user interface.

- May 2023: BIOTRONIK announced CE approval for Amvia Sky/Amvia Edge, including CRT-P, approved for left bundle branch pacing.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.96 billion in 2025 and is projected to reach USD 9.72 billion by 2034.

In 2025, the market value in North America stood at USD 3.08 billion.

The market is expected to exhibit a CAGR of 3.7% during the forecast period of 2026-2034.

The CRT-Defibrillator segment led the market by product.

The key factors driving the market are the expanding guideline-based eligibility and a growing heart failure pool.

Medtronic plc, Abbott, Boston Scientific, and BIOTRONIK SE & Co. KG are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us