Cell Counting Market Size, Share & Industry Analysis, By Product Type (Instruments {Flow Cytometers, Hemocytometers, Automated Cell Counters, and Others}, and Consumables & Accessories), By Application (Research Applications, Clinical & Diagnostic Applications, Biopharmaceutical Manufacturing, and Others), By End-user (Academic & Research Institutes, Hospitals & Diagnostic Laboratories, Pharmaceutical & Biotechnology Companies, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

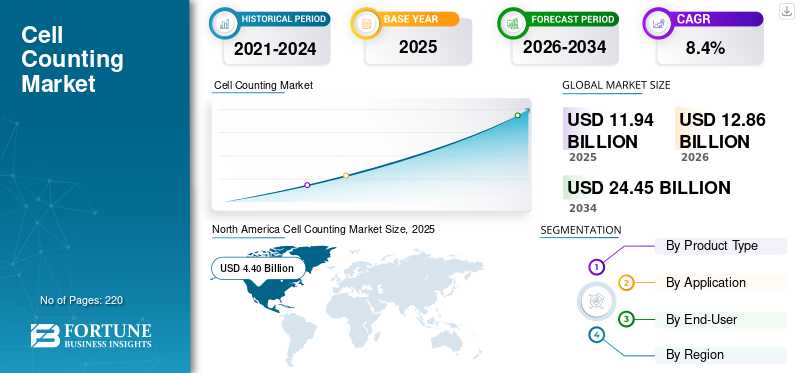

The global cell counting market size was valued at USD 11.94 billion in 2025. The market is projected to grow from USD 12.86 billion in 2026 to USD 24.45 billion by 2034, exhibiting a CAGR of 8.4% during the forecast period. North America dominated the global cell counting market with a share of 36.85% in 2025.

Cell counting is the process of measuring the number of cells present in a sample along with analysis of its vitality and mobility. It is a basic step in research labs and also a routine check in bio manufacturing in order to understand growth of cells in a culture. The market is expected to rise due to increase in cell-based across drug discovery, biologics, vaccines, and especially cell & gene therapy. Moreover, in manufacturing, cell counts are checked repeatedly to keep processes stable and avoid waste. In addition, market players are also emphasizing on the introduction of technologically advanced systems, further propelling the market growth.

- For instance, in May 2023, Sysmex Corporation announced the launch of its new clinical flow cytometer in Japan. The newly introduced system allows in-detailed cell counting functionality.

Moreover, different key industry players, such as Thermo Fisher Scientific Inc., Danaher Corporation, BD, Merck KGaA, Bio-Rad Laboratories, Inc., and Agilent Technologies, Inc., operating in the market, are focusing on developing various innovative technologies to offer better efficiency.

Download Free sample to learn more about this report.

CELL COUNTING MARKET TRENDS

Rising Preference for Automation of Consistent Cell Counting Results is Prominent Trend Observed in Market

The market is witnessing rising demand for automated cell counting systems in order to get consistent cell counting results. Moreover, these systems significantly reduce variation in results, enabling superior outcomes. In addition, automated counters reduce dependence on manual handling and help standardize workflows across teams and shifts. As cell-based work scales up, especially in biopharmaceutical manufacturing, companies are choosing automated tools to improve repeatability and support higher sample volumes without slowing operations.

- For instance, in September 2022, PerkinElmer, Inc. announced the launch of its new cell analysis solution with an aim to streamline processes in cell and gene therapy manufacturing.

Download Free sample to learn more about this report.

Cell Counting Market Key Takeaways

- 2025 Market Size: USD 11.94 billion

- 2026 Market Size: USD 12.86 billion

- 2034 Forecast Market Size: USD 24.45 billion

- CAGR: 8.4% from 2026–2034

- North America dominated the cell counting market with a 36.85% share in 2025.

- Pharmaceutical & biotechnology companies are projected to hold a 39.1% share in 2026.

- Consumables & accessories accounted for the leading product type segment share due to repetitive purchasing demand in cell processing workflows.

North America

North America was valued at USD 4.40 Billion in 2025, supported by rising pharmaceutical manufacturing activities and increasing investments in research and development.

Europe

Europe is projected to reach USD 3.47 Billion in 2026, driven by expanding pharmaceutical manufacturing capacities and new production facility developments.

Asia Pacific

Asia Pacific is projected to reach USD 3.25 Billion in 2026, supported by expanding biotechnology industries and increasing healthcare investments across the region.

U.S.

The U.S. market was valued at USD 4.03 Billion in 2026, owing to its strong dominance in biopharmaceutical manufacturing activities.

Japan

The Japan market was valued at USD 0.57 Billion in 2026, supported by technological advancements and increasing adoption of automated cell analysis systems.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Pharmaceutical and Biopharmaceutical Manufacturing Volumes to Accelerate Market Growth

Rise in biopharmaceutical manufacturing volumes are eventually increasing as more biologics, vaccines, and cell-based therapies move into commercial production. As pharmaceutical and biopharmaceutical production expands, the number of batches, lines, and routine in-process checks will increase eventually. Cell counting is one of the most common checks used during these processes, as it helps teams monitor growth and decide when to move to the next step.

This directly increases demand for cell counting instruments.

- For instance, in April 2024, Fujifilm announced its plan to invest USD 1.2 billion in order to expand its biopharmaceutical manufacturing facility in North Carolina.

MARKET RESTRAINTS

Requirement of Additional Cost for System Upgradation to Deter Market Growth

Requirement of additional investments for cell counting system upgradation is one of the prominent restraints hampering the global cell counting market growth. Many laboratories and manufacturing sites already have functional cell counting setups that meet their current needs. Investing in new instruments and compatible consumables requires budget allocation, which is often delayed in favor of other priorities. As a result, organizations tend to extend the use of existing systems rather than replacing them immediately. This cost sensitivity slows the adoption of newer cell counting solutions, especially in facilities focused on cost control and operational stability.

MARKET OPPORTUNITIES

Growing Adoption of Cell-based Therapies to Offer Lucrative Market Growth Opportunities

The rising adoption of cell-based therapies to offer a favorable environment for market growth. These cell therapies rely heavily on living cells, which need to be monitored closely during development and manufacturing. Furthermore, as more companies move cell-based therapies from trials to commercial production, the number of samples and checks increases. This creates steady demand for reliable cell counting tools and consumables.

- For instance, in November 2023, Bristol Myers Squibb announced an expansion of its cell therapy manufacturing capabilities in the U.S. The new infrastructure will be utilized to accelerate commercial production of CAR-T and other cell-based therapies.

MARKET CHALLENGES

Managing Routine Cell Counting Alongside Daily Operations to Pose a Critical Challenge to Market Growth

Managing routine cell counting activities alongside other daily laboratory and manufacturing tasks to offer challenges for the market. Laboratories often handle multiple responsibilities at the same time, such as sample preparation, process monitoring, and documentation. Adding frequent cell counting can increase workload and coordination efforts, especially when sample volumes rise. In addition, if workflows are not well organized, cell counting may slow down other activities or create delays.

Segmentation Analysis

By Product Type

Significant Adoption of Consumables Due to Cell Processing to Propel Segmental Growth

Based on the product type, the market is divided into instruments and consumables & accessories.

The consumables & accessories segment is anticipated to account for the largest cell counting market share. The high segmental share is primarily attributed to its repetitive purchase, and cell counting processes. In addition, growth in biopharmaceutical manufacturing is also projected to drive segment growth.

- For instance, in August 2024, DeNovix announced the launch of the CellDrop FLi Automated Cell Counter with enhanced hardware and multiple new cell counting applications.

The instruments segment is anticipated to rise with a CAGR of 7.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Investments in Biopharmaceutical Manufacturing to Boost Segment Growth

Based on application, the market is segmented into research applications, clinical & diagnostic applications, biopharmaceutical manufacturing, and others.

In 2025, the biopharmaceutical manufacturing segment dominated the global market. Biopharmaceutical manufacturing needs frequent cell counts to ensure processes are stable and to avoid costly batch issues. In addition, rising investments by market players in order to expand manufacturing capacities is also projected to accelerate segment growth.

- For instance, in November 2025, Novartis announced its plan to build a manufacturing hub in North Carolina. The company has plans to invest USD 23 billion.

The research applications segment is projected to grow at a CAGR of 8.3% over the forecast period.

By End-User

Higher Adoption of Cell Counting Systems in Pharmaceutical & Biotechnology Companies due to Pharmaceutical Production to Lead Segment

Based on end-user, the market is segmented into academic & research institutes, hospitals & diagnostic laboratories, pharmaceutical & biotechnology companies, and others.

The pharmaceutical & biotechnology companies dominated the global market. These companies perform cell counting during early research, process development, scale-up, and routine manufacturing, which increases overall usage. Unlike academic labs that may count cells occasionally, pharma and biotech companies rely on repeated and standardized cell counts to support decision-making and documentation. Furthermore, the segment is set to hold 39.1% share in 2026.

In addition, academic & research institutes are projected to grow at a CAGR of 8.4% during the study period.

Cell Counting Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cell Counting Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 4.10 billion, and also maintained the leading share in 2025, with USD 4.40 billion. The market in North America is expected to increase due to extensive rise in pharmaceutical manufacturing and substantial investments for research & development activities. These factors, coupled with robust healthcare and substantial technological advancements are enabling market growth.

U.S Cell Counting Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 4.03 billion in 2026, accounting for roughly 31.4% of global cell counting sales.

Europe

Europe is projected to record a growth rate of 7.8% in the coming years, which is the second highest among all regions, and reach a valuation of USD 3.47 billion by 2026. The region is estimated to have widespread expansion of pharmaceutical manufacturing capacities along with commencement of new production facilities.

U.K Cell Counting Market

The U.K. market in 2026 is estimated at around USD 0.57 billion, representing roughly 4.4% of global cell counting revenues.

Germany Cell Counting Market

Germany’s market is projected to reach approximately USD 0.78 billion in 2026, equivalent to around 6.1% of global cell counting sales.

Asia Pacific

Asia Pacific is estimated to reach USD 3.25 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.72 billion and USD 1.08 billion, respectively in 2026.

Japan Cell Counting Market

The Japan market in 2026 is estimated at around USD 0.57 billion, accounting for roughly 4.4% of global cell counting revenues.

China Cell Counting Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 1.08 billion, representing roughly 8.4% of global cell counting sales.

India Cell Counting Market

The India market in 2026 is estimated at around USD 0.72 billion, accounting for roughly 5.6% of global cell counting revenues.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.82 billion in 2026. In the Middle East & Africa, the GCC is set to reach a value of USD 0.22 billion in 2026.

South Africa Cell Counting Market

The South Africa market is projected to reach around USD 0.09 billion in 2026, representing roughly 0.7% of global cell counting revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Introduction of New Products with Advanced Technologies by Key Players to Propel Market Progress

The global cell counting market holds a semi-consolidated market structure, constituting prominent players such as Thermo Fisher Scientific Inc., Danaher Corporation, BD, Merck KGaA, Bio-Rad Laboratories, Inc., and Agilent Technologies, Inc. The significant market share of these companies is due to numerous strategic activities, including collaboration among operating entities to advance research activities.

- For instance, in October 2024, Thermo Fisher Scientific showcased its expanded portfolio of biopharmaceutical services at CPHI Milan.

Other notable players in the global market include PerkinElmer Inc., Nexcelom Bioscience LLC, Logos Biosystems, Inc., ChemoMetec A/S, and Sysmex Corporation. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY CELL COUNTING COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher Corporation (U.S.)

- BD (U.S.)

- Merck KGaA (Germany)

- Bio-Rad Laboratories, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Revvity (U.S.)

- Nexcelom Bioscience LLC (U.S.)

- Logos Biosystems, Inc. (South Korea)

- ChemoMetec A/S (Denmark)

- Sysmex Corporation (Japan)

- Miltenyi Biotec (Germany)

KEY INDUSTRY DEVELOPMENTS

- December 2025: BD announced launch of its new BD FACSDiscover A8 cell analyzers for cell imaging and counting. The instrument is useful in cancer immunotherapy, cell biology, and research in immunology.

- August 2024: DeNovix launched an automated hepatocytes counting application for CellDrop.

- June 2024: Horiba announced the introduction of its new hematology analyzer with combined ESR and CBC/Diff functionality.

- April 2024: METTLER TOLEDO launched the CytoDirect stain-free automated cell counter, which enables faster and more consistent cell counting.

- April 2021: CytoSMART Technologies introduced a new automated cell counting instrument with new fluorescence cell counter capability.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, End-User, and Region |

|

By Product Type |

· Instrument o Flow Cytometers o Hemocytometers o Automated Cell Counters o Others · Consumables & Accessories |

|

By Application |

· Research Applications · Clinical & Diagnostic Applications · Biopharmaceutical Manufacturing · Others |

|

By End-User |

· Academic & Research Institutes · Hospitals & Diagnostic Laboratories · Pharmaceutical & Biotechnology Companies · Others |

|

By Region |

· North America (By Product Type, Application, End-User, and Country) o U.S. § Product Type o Canada § Product Type · Europe (By Product Type, Application, End-User, and Country/Sub-region) o Germany § Product Type o U.K. § Product Type o France § Product Type o Spain § Product Type o Italy § Product Type o Scandinavia § Product Type o Rest of Europe § Product Type · Asia Pacific (By Product Type, Application, End-User, and Country/Sub-region) o China § Product Type o Japan § Product Type o India § Product Type o Australia § Product Type o Southeast Asia § Product Type o Rest of Asia Pacific § Product Type · Latin America (By Product Type, Application, End-User, and Country/Sub-region) o Brazil § Product Type o Mexico § Product Type o Rest of Latin America § Product Type · Middle East & Africa (By Product Type, Application, End-User, and Country/Sub-region) o GCC § Product Type o South Africa § Product Type o Rest of Middle East & Africa § Product Type |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.94 billion in 2025 and is projected to reach USD 24.45 billion by 2034.

In 2025, the market value stood at USD 4.40 billion.

The market is expected to exhibit a CAGR of 8.4% during the forecast period.

By product type, the consumables & accessories segment is expected to lead the market.

The increasing investments for pharmaceutical and biopharma production are driving market expansion.

Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc., and Cytiva are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us