Cellular Module Market Size, Share & Industry Analysis, By Module Type (2G / 3G, 4G LTE, LTE-M, NB-IoT, and 5G), By Form Factor (Surface Mount (LGA, BGA), Plug-in Card (M.2, mini-PCIe), USB / Dongle, and Others), By Application (Automotive & Transportation, Industrial & Manufacturing, Smart Utilities, Healthcare, Consumer Electronics, Smart Cities & Infrastructure and Others) and Regional Forecast, 2026-2034

CELLULAR MODULE MARKET SIZE AND FUTURE OUTLOOK

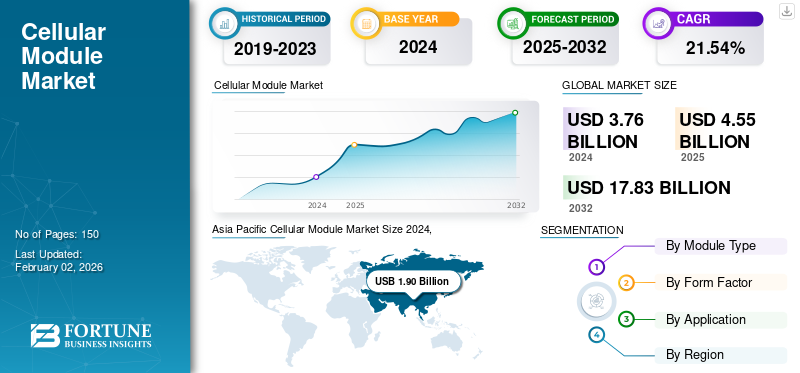

The global cellular module market size was valued at USD 4.55 billion in 2025. The market is projected to grow from USD 5.52 billion in 2026 to USD 23.55 billion by 2034, exhibiting a CAGR of 19.89% during the forecast period. Asia Pacific dominated the cellular module market with a market share of 50.52% in 2025.

A cellular module is referred to a compact device that allows machines and IoT systems to connect with cellular networks such as 4G, LTE-M, and 5G for data communication without Wi-Fi. These are crucial for vehicles, smart devices and industrial usage.

The market is experiencing a steady growth owing to the increasing adoption of IoT technology, development of smart cities, expansion of 5G network and surging demand for connected automotive and healthcare solutions. Additionally, the growth of low-power wide area (LPWA) technologies is also fueling the demand for energy efficient modules.

Various key players including Quectel Wireless Solutions Co., Ltd., Fibocom Wireless Inc., Telit Cinterion, China Mobile IoT Company Limited and LG Innotek Co., Ltd. are thriving to gain leading position in the market by adopting various strategies such as mergers, adoption of innovative technologies, and new launches.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Growing IoT Device Adoption and Industrial Digitalization Drives the Market Development

The increase in adoption of industrial digitalization and IoT devices boosts the cellular module market growth. With industries looking for smart manufacturing, automation and real-time monitoring, an effective and reliable connectivity is becoming highly crucial. Cellular modules have emerged as a feasible solution as it enables seamless machine to machine communication across a large scale operation without requiring Wi-Fi. Additionally, Industry 4.0 initiatives and different smart factories depend on cellular modules to connect with equipment, sensors, and control systems, thus enhancing efficiency, productivity and decision making.

- For instance, according to the National Institute of Standards and Technology, by 2025, the overall impact of IoT devices on the global economy will be between USD 4 trillion and USD 11 trillion.

Market Restraints

Certification Complexity and High Integration Costs Hampers the Market Growth

Certification complexity and the higher integration costs are major restraints for the market growth. Every module is required to comply with the regional regulatory standards and network certifications that could vary across operators and countries, resulting in an expensive and time-consuming approval procedures.

Additionally, device manufacturers are also required to ensure compatibility with different cellular technologies, thus increasing the design complexity and expenses of testing. Integrating such modules into the diverse IoT devices thus demanding customized hardware and software adaptations, further adding to the development costs.

Market Opportunities

Expansion of 5G RedCap, Private Networks, and Automotive IoT Offers Lucrative Growth Opportunities

The growth of 5G private networks and the surge in automotive IoT offers a significant opportunity for the market. 5G private networks provide improved reliability, speed, and low latency, thus enabling industries to deploy customized and secure connectivity for smart factories, utilities and logistics. Cellular modules are crucial components for integrating such networks into machinery and devices.

CELLULAR MODULE MARKET TRENDS

Integration of 5G, eSIM/iSIM, and AI-Driven Edge Computing Has Emerged as a Prominent Market Trend

Integration of 5G, AI driven edge computing, and Esim/iSIM to improve flexibility, connectivity and performance. 5G allows for low latency communication for real time applications, whereas Esim/iSIM technologies tend to simplify device activation and remote management, aiding global scalability.

Additionally, AI-powered edge computing enables data processing directly within the devices, thus decreasing the cloud dependency and enhancing response time. These factors collaboratively transform the cellular module market.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Module Type

Increasing demand for Growing Network Coverage Boosts 4G LTE Segment Growth

Based on module type, the market is segmented into 2G / 3G, 4G LTE, LTE-M, NB-IoT, and 5G.

In 2024, 4G LTE segment is projecteed to dominate the market with a share of 52.02% in 2026. This segment growth is attributed to the growing network coverage, and lower module costs. Additionally, this module type also provides a mature certification ecosystem that helps in meeting most of the IoT performance needs.

Additionally, 5G segment held the highest CAGR of 24.69% in 2024. This growing is majorly driven by the increasing use cases of RedCap and private 5G unlock mid-tier IoT. This demands a higher throughput, longer device lifecycles and lower latency.

By Form Factor

Rugged and Compact Designs of Surface Mount (LGA, BGA) to Drive the Segment Growth

The market is divided into Surface Mount (LGA, BGA), Plug-in Card (M.2, mini-PCIe), USB / Dongle, and others, based on form factor.

Among these, Surface Mount (LGA, BGA) segment is projecteed to dominate the market with a share of 68.14% in 2026. The segment also held a highest CAGR of 22.43% in 2024. This form factor allows for rugged and compact designs and higher volume SMT manufacturing for cost sensitive and space constrained IoT endpoints.

On the other hand, the Plug-in Card (M.2, mini-PCIe) segment is growing significantly. The growth is due to industrial gateways, and PCs favor field-replaceable modules for generational upgrades and flexibility across carriers.

By Application

Strict and Mandated Safety or Telematics Capabilities Drive Automotive & Transportation Segment Growth

The market is divided into automotive & transportation, industrial & manufacturing, smart utilities, healthcare, consumer electronics, smart cities & infrastructure, and others, based on application.

Among these, the automotive & transportation segment is projecteed to dominate the market with a share of 22.26% in 2026. This segmental growth is attributed to the strict and mandated safety or telematics capabilities, growing C-V2X readiness and effective fleet management.

On the other hand, the smart utilities segment held highest CAGR of 25.07% in 2024. This growth is attributed to the large scale AMI rollouts and rapid grid modernization that adopt LTE-M/NB-IoT/5G for metering low power, long life and infrastructure monitoring.

To know how our report can help streamline your business, Speak to Analyst

CELLULAR MODULE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

In 2025, North America held 14.82% of the global market share, reaching a valuation of USD 0.67 Billion, and is projected to grow to USD 0.81 Billion in 2026. supported by early adoption of advanced connectivity technologies and a well-established ecosystem of telecommunications, automotive, and industrial manufacturers. The region benefits from widespread deployment of 5G infrastructure, enabling greater integration of connected devices across enterprise and consumer applications. Regulatory initiatives aimed at accelerating digital transformation and connected mobility further support market expansion. The U.S., projected to generate USD 0.48 billion in revenue by 2026, remains the dominant contributor owing to its strong technology adoption rates, extensive network investments, and growing demand for next-generation connectivity solutions.

Europe

The market in Europe reached USD 0.88 Billion in 2025, representing 19.24% of total market revenue, and is projected to reach USD 1.05 Billion in 2026. driven by increasing investments in digital infrastructure and the rapid adoption of connected technologies across industrial and automotive sectors. The region’s regulatory framework continues to encourage innovation in smart mobility, industrial automation, and secure connectivity deployments. Strong demand for advanced communication modules is supported by ongoing modernization initiatives and the expansion of connected ecosystems across multiple industries. The U.K., Germany, and France are expected to contribute significantly to regional growth, with projected revenues of USD 0.25 billion, USD 0.22 billion by 2026 and USD 0.16 billion respectively in 2025.

Asia Pacific

Asia Pacific contributed approximately USD 2.3 Billion to the global market in 2025, accounting for 50.52% share, and is expected to reach USD 2.79 Billion in 2026. The region’s leadership is primarily attributed to its extensive module manufacturing base, strong electronics production capabilities, and growing demand for connected solutions across major economies. Government support for 4G and 5G deployments, combined with favorable industrial policies, continues to accelerate market development. Rising digitalization, expanding IoT adoption, and increasing investments in telecommunications infrastructure further strengthen regional demand. The Japan market is valued at USD 0.66 billion by 2026, the China market is valued at USD 0.80 billion by 2026 and the India market is valued at USD 0.52 billion by 2026., supported by large-scale network expansion and growing adoption of connected technologies.

Asia Pacific Cellular Module Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Latin America

In 2025, Latin America generated USD 0.4 Billion, contributing 8.86% to global market revenue, and is projected to grow to USD 0.5 Billion in 2026, supported by increasing investments in telecommunications infrastructure and expanding digital connectivity initiatives. Demand is being driven by the rollout of greenfield network projects, rising adoption of smart utility solutions, and the growing need for reliable wireless communication technologies. Regulatory efforts focused on improving broadband access and enhancing network coverage are creating favorable conditions for market growth. Continued expansion of 4G and emerging 5G networks is expected to support long-term adoption across both urban and rural areas.

Middle East & Africa

The Middle East & Africa region captured 6.57% of the global market in 2025, generating USD 0.3 Billion in revenue, and is projected to reach USD 0.37 Billion in 2026. Growth in the region is being fueled by ongoing smart city developments, utility modernization projects, and increasing investments in advanced telecommunications infrastructure. Governments and regulatory authorities are actively supporting digital transformation programs, encouraging broader deployment of next-generation connectivity technologies. Expanding 4G, 5G, and non-terrestrial network (NTN) coverage is further enhancing market opportunities. GCC countries are expected to play a key role in regional growth, collectively accounting for USD 0.10 billion of the market in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Adopting Innovative Technologies to Sustain their Dominating Market Positions

The cellular module industry consists of different players operating including Quectel Wireless Solutions Co., Ltd., Fibocom Wireless Inc., Telit Cinterion, China Mobile IoT Company Limited, LG Innotek Co., Ltd. and others. These firms are adopting different key strategies to maintain their market position. These strategies could include mergers and collaborations, adoption of innovative technologies, new product launches and others.

LIST OF KEY CELLULAR MODULE COMPANIES PROFILED

- Quectel Wireless Solutions Co., Ltd. (China)

- Fibocom Wireless Inc. (China)

- Telit Cinterion (U.S.)

- China Mobile IoT Company Limited (China)

- LG Innotek Co., Ltd. (South Korea)

- u-blox Holding AG (Switzerland)

- Sierra Wireless, Inc. (Canada)

- SIMCom Wireless Solutions Limited (China)

- Murata Manufacturing Co., Ltd. (Japan)

- Huawei Technologies Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Seeed Studio launched a new module series based on Nordic Semiconductor’s next generation nRF54L15 ultra-low power wireless SoC. The modules are designed to enable a broad range of IoT applications where compact size, low power consumption, and multiprotocol wireless connectivity are essential – such as wireless sensors, wearables, and smart home devices. The platform also supports ‘Edge AI’ and rapid prototyping, helping developers and startups create compact AIoT (Artificial Internet of Things) projects with onboard processing capabilities.

- In October 2025, MikroElektronika, the Serbian embedded solutions manufacturer, launched a new low-power wireless connectivity module aimed at accelerating the development of Internet of Things (IoT) and Industrial IoT (IIoT) applications.

- In March 2025, Telit Cinterion launched the LE310 LTE Cat 1 bis module series and SL871K2 L1 GNSS module, designed for affordable, low-power asset tracking applications with an ultra-compact form factor.

- In March 2025, u-blox, a global leader in positioning and short-range communication technologies, has announced the transfer of its cellular IoT module business to Trasna, a leading semiconductor and IoT solutions provider. This strategic move reinforces u-blox’s focus on its core locate business while enabling Trasna to strengthen its IoT connectivity chip-to-cloud offering in the OEM sector.

- In September 2024, u-blox launches first satellite IoT-NTN cellular module with embedded GNSS solving remote connectivity challenges. The SARA-S528NM10, powered by the UBX-S52 cellular/satellite chipset and M10 GNSS platform for low-power and concurrent positioning, expands the company’s cellular portfolio for the satellite IoT market based on the 3GPP Rel 17 specification for global connectivity.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent cellular module vendors, deployment modes, types, and end users of the product. Besides this, it offers insights into the cellular module market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 19.89% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD billion) |

| Segmentation | By Module Type, Form Factor, Application and Region |

| By Module Type |

|

| By Form Factor |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 5.52 billion in 2026 and is projected to reach USD 23.55 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 19.89% during the forecast period.

Rising IoT device adoption and industrial digitalization drives the market growth.

Quectel Wireless Solutions Co., Ltd., Fibocom Wireless Inc., Telit Cinterion, China Mobile IoT Company Limited, LG Innotek Co., Ltd. and others are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 2.3 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us