Central Lab Services Market Size, Share & Industry Analysis By Service Type (Safety Testing, Biomarker Testing, Genetic Testing, Immunology Testing, Anatomic Pathology & Histology, Microbiology & Infectious Disease Testing, Bioanalytical Testing, & Others), By Phase (Phase I, Phase II, Phase III, & Phase IV), By Modality (Small Molecules, Biologics, Medical Devices, & Others), By Therapeutic Area (Oncology, Infectious Diseases, Neurology, Cardiology, & Others), By End User (Pharmaceutical & Biotechnological Companies, Medical Device Companies, CROs, & Others), and Regional Forecast, 2026-2034

Central Lab Services Market Size and Future Outlook

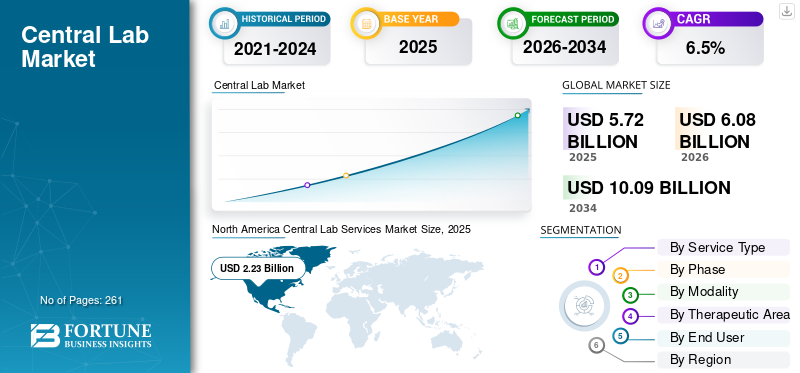

The global central lab services market size was valued at USD 5.72 billion in 2025 and is projected to grow from USD 6.08 billion in 2026 to USD 10.09 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. North America dominated the central lab market with a market share of 38.99% in 2025.

Central lab services are centralized, specialized facilities that deal with the management and analysis of biological samples collected during clinical trials. Increasing number of clinical trials, rising demand for standardized laboratory testing, outsourcing by pharmaceutical and biotechnological companies, and advancements in diagnostic technologies are resulting in the adoption rate of these services in the market. The growing clinical trials for rare diseases, oncology, and others are further boosting the adoption in the market.

- For instance, according to 2025 statistics published by the World Health Organization (WHO), about 35,499 clinical trials were conducted in Australia.

Furthermore, the rising focus towards expansion of service capabilities among companies, including Thermo Fisher Scientific Inc., Labcorp, among others, further contributing to the demand for these services in the market.

Download Free sample to learn more about this report.

Central Lab Services Market Trends

Increasing Adoption of Digital Tools and Real-Time Sample Tracking to be a Prominent Trend

The increasing adoption of AI, digital portals, and real-time data tracking systems is becoming a major trend in the global market. The integration of digital portals enables continuous visibility into every stage of the sample journey; from kit shipment and patient sample collection to transportation, lab receipt, testing, analysis, data management, and sample reconciliation.

Additionally, real-time devices also enhance partnerships among laboratories, trial sites, sponsors, and contract research organizations by providing a single view of sample status and laboratory data. This is especially important for rare disease, oncology, immunology, and personalized medicine trials, where biomarker samples can be central to patient eligibility, dosing decisions, endpoint assessment, and regulatory submissions.

- For instance, according to a 2024 survey published by the National Center for Biotechnology Information (NCBI), it was reported that the difference between current and aimed adoption of remote technologies in 5 years is large, with respondents expecting a 40% or increased adoption of 8 out of 11 enabling technologies.

Other Prominent Trends

- Development of decentralized and virtual clinical trials

- Growth in genomic and molecular diagnostic testing

- Expansion of cloud-based laboratory data management systems

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Number of Multi-Site Clinical Trials to Boost Market Growth

The increasing number of multi-site clinical trials among pharmaceutical, biotechnology, and medical device companies for boosting drug manufacturing is resulting in the expansion of patient recruitment, further supporting regulatory submissions across various regions.

- For instance, according to 2024 data published by the World Health Organization (WHO), approximately 197,090 clinical trials were conducted in the U.S.

This, along with growing demand for precision medicine and biomarker research, expansion of R&D investments among pharmaceutical and biotechnological companies, and rising outsourcing services for drug and medical device development, is further boosting the adoption rate of these services in the market. Therefore, the factors above, along with the growing focus of key companies on providing innovative services are further likely to contribute to the central lab services market growth.

Market Restraints

High Cost Associated with Advanced Testing to Limit the Market Growth

The complexity of clinical trials and focus towards tailored medicine is resulting in growing demand for specialized laboratory services, including next-generation sequencing, genomic testing, immunogenicity testing, biomarker analysis, pharmacokinetic/pharmacodynamic testing, and others, which require advanced instruments, assays, and professionals, further increasing the cost of these services in the market.

Additionally, central lab operations involve high operating costs arising from cold-chain logistics, regional laboratory infrastructure, sample storage, kit production, cross-border specimen transport, quality audits, digital data systems, and regulatory documentation, making it challenging for small and mid-sized companies to provide novel services, thereby hindering market growth.

- For instance, according to the 2025 statistics published by the Snic Solutions, it was reported that the average cost of laboratory information management systems is around USD 20,000 for smaller setups.

Market Opportunities

Expansion of Regional Laboratory Networks to Create Lucrative Market Growth Opportunities

The expansion of laboratory networks in emerging nations presents a lucrative opportunity in the global market. There is an increasing development of structured pre-hospital emergency response portals, ambulance networks, centralized dispatch solutions, trained paramedic specialists, and trauma referral pathways in the developing nations, including Brazil, Mexico, and others. Additionally, increasing development of healthcare infrastructure, along with growing healthcare expenditure, is resulting in growing demand for central labs, advanced life support units, organized ambulance services, and interfacility transport services in the market.

- According to 2025 statistics published by the International Trade Administration (ITA), it was reported that the healthcare expenditure is about USD 135.0 billion in the U.S.

Market Challenges

Limited Number of Clinical Trials in Emerging Countries to Hamper the Market Growth

There is a growing demand for novel central lab services among the patient population. However, limited healthcare access in emerging countries remains a major challenge in the global market. Lack of well-developed diagnostic infrastructure and efficient sample collection and logistics networks, limited trained professionals, and a lack of a strong clinical trial system are resulting in a reduced number of clinical trials among the companies, thereby hampering the market growth.

- For instance, according to 2025 data published by the World Health Organization (WHO), only 55 clinical trials were conducted in Yemen.

Other Prominent Challenges

- Data security and patient privacy concerns

SEGMENTATION ANALYSIS

By Service Type

Increasing Number of Safety Testing Tests Led to the Segmental Dominance

Based on the service type, the market is classified into safety testing, biomarker testing, genetic testing, immunology testing, anatomic pathology & histology, microbiology & infectious disease testing, bioanalytical testing, and others.

The safety testing segment held the largest revenue share in 2025. The growth is owing to the rise in the number of developments related to drugs and medical devices, consequently increasing the demand for routine and specialized safety tests, including clinical chemistry, hemoatology, and others, among the patient population. This, along with the rising number of companies and CROs offering novel services, is further anticipated to contribute to the overall global market growth.

- For instance, according to 2026 data published by the American Clinical Laboratory Association (ACLA), more than 7.0 billion lab tests are performed each year in the U.S.

The genetic testing segment is expected to grow at a CAGR of 8.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Phase

Increasing Number of Phase III Clinical Trials Led to Its Governance in the Market

Based on the phase, the market is segmented into phase I, phase II, phase III, and phase IV.

The phase III segment dominated the global market in 2025, holding a share of 45.5% in 2025. The growth is due to the growing number of phase III clinical trials, resulting in growing testing volumes and adoption of digital tools, robust logistics, temperature-controlled sample transport systems, and others, thereby contributing to the segmental growth in the market.

- For instance, according to 2025 statistics published by the World Health Organization (WHO), about 94,465 phase III clinical trials were conducted globally.

The phase II segment is set to flourish with a growth rate of 7.3% across the forecast period.

By Modality

Small Molecules Modality Takes the Lead Owing to Increasing Approval of Small Molecule Therapies

Based on modality, the market is segmented into small molecules, biologics, medical devices, and others.

The small molecules segment dominated the global market in 2025 with a share of 44.7% in 2025. The growth is due to the rising prevalence of chronic conditions and the benefits of small molecular therapies, including established development pathways, and others, resulting in a growing number of small molecule therapies, thereby contributing to the segmental growth.

- For instance, according to the 2024 data published by the American Chemical Society (ACS), it was reported that the 28 small-molecule therapies approved account for about 56% of new drugs in the U.S.

The medical devices segment is set to flourish with a growth rate of 6.2% across the forecast period.

By Therapeutic Area

Increasing Prevalence of Cancer Propelled the Oncology Segment’s Leadership

Based on therapeutic area, the market is divided into oncology, infectious diseases, neurology, cardiology, and others.

The oncology segment dominated the market in 2025. The increasing prevalence of various types of cancer, growing demand for central lab services, and rising number of clinical trials, among others, are some of the key factors contributing to the growth of the segment. Furthermore, the segment is set to hold an 40.6% share in 2026.

- For instance, according to 2025 statistics published by the National Cancer Institute, it was reported that an estimated 2.0 million cancer cases are projected to occur in the U.S.

In addition, neurology segment is projected to grow at a 6.9% CAGR during the forecast period.

By End User

Rising Development of Medical Devices and Drugs by Pharmaceutical & Biotechnological Companies Led to the Segmental Dominance

Based on end user, the market is segmented into pharmaceutical & biotechnological companies, medical device companies, CROs, and others.

The pharmaceutical & biotechnological companies segment dominated the market in 2025. Increasing development of drugs and medical devices, rising number of clinical trials, and growing number of pharmaceutical and biotechnological companies, among others, are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold an 64.0% share in 2026.

- For instance, according to 2026 data published by Cross River Therapy, it was reported that there are about 5,000 companies in the U.S.

In addition, medical device companies are projected to grow at a 5.3% CAGR during the forecast period.

Central Lab Services Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Central Lab Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant central lab services market share in 2024, valued at USD 2.12 billion, and also took the leading share in 2025 with USD 2.23 billion. Growing number of clinical trials, rising adoption rate of testing services, increasing number of pharmaceutical and medical device companies, among others, are some of the factors contributing to the growth of the regional market.

- For instance, according to 2025 statistics published by the World Health Organization (WHO), about 197,090 clinical trials were conducted in the U.S.

U.S. Central Lab Services Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 2.06 billion in 2026, accounting for roughly 33.9% of global market sales.

Europe

Europe is projected to record a growth rate of 5.7% in the coming years, which is the second highest among all regions, and reach a valuation of USD 1.63 billion by 2026. The growing number of clinical trials is likely to support the regional market growth.

U.K Central Lab Services Market

The U.K. market in 2026 is estimated at around USD 0.29 billion, representing roughly 4.8% of global market revenues.

Germany Central Lab Services Market

Germany’s market is projected to reach approximately USD 0.30 billion in 2026, equivalent to around 5.0% of global market sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.54 billion in 2026 and secure the position of the third-largest region in the market. The expanding central lab capacity and increasing healthcare expenditure are likely to support the regional growth.

Japan Central Lab Services Market

The Japan market in 2026 is estimated at around USD 0.34 billion, accounting for roughly 5.6% of global revenues. Japan is expected to grow due to the expansion of central lab services and investment in R&D activities among the key companies in the market.

China Central Lab Services Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.49 billion, representing roughly 8.1% of global sales.

India Central Lab Services Market

The India market size in 2026 is estimated at around USD 0.24 billion, accounting for roughly 3.9% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.30 billion in 2026. The growth is due to the increasing number of decentralized and hybrid clinical trials and rising demand for central lab services in the region. The Middle East & Africa region is also anticipated to grow due to the growing number of research institutes and key companies expanding their geographic presence. In the Middle East & Africa, the GCC is set to reach a value of USD 0.12 billion in 2026.

South Africa Central Lab Services Market

The South Africa market is projected to reach around USD 0.05 billion in 2026, representing roughly 0.9% of global revenues.

Competitive Landscape

Key Industry Players

Expansion of Clinical Research Laboratory and Focus On Strategic Initiatives to Support The Market Positioning of Prominent Market Players

Thermo Fisher Scientific Inc., and Labcorp were the major companies in the market in 2025. Strong services portfolio, along with a significant focus on strategic initiatives globally, is one of the key factors contributing to the dominance of these companies in the market. Furthermore, the growing focus of key companies on the expansion of laboratory services is likely to strengthen their presence, further contributing to the.

- For instance, in June 2024, Thermo Fisher Scientific Inc., expanded its central laboratory operations dedicated to accelerating pharmaceutical and biotech customers’ delivery of safe, effective medicines to patients in the U.S.

Other key players, including ICON plc and others, are also growing in the market, primarily due to their increasing focus on acquisitions to strengthen their presence in the market.

List of Key Central Lab Services Companies Profiled

- Thermo Fisher Scientific Inc. (U.S.)

- ICON plc (Ireland)

- SGS Société Générale de Surveillance SA (Switzerland)

- Labcorp (U.S.)

- IQVIA (U.S.)

- ACM Global Laboratories (U.S.)

- Nordic Bioscience (Denmark)

- Charles River Laboratories (U.S.)

- Eurofins Scientific (Luxembourg)

- Cerba Research (Belgium)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Thermo Fisher Scientific Inc., announced a strategic data collaboration with HealthVerity, a real-world data (RWD) marketplace, to enhance data-driven clinical development and evidence generation for biopharma sponsors.

- March 2026: ICON plc, a clinical research organization, partnered with Advarra, the player in regulatory reviews and a provider of connected, intelligence-powered research technology, to introduce a new ‘research-ready,’ connected site network model for clinical trials.

- August 2025: IQVIA, a global drug discovery and development laboratory services organization, received the award for 2025 Best Central/Specialty Laboratory at the prestigious 2025 Vaccine Industry Excellence (ViE) Awards. This helped the company in strengthening its presence.

- May 2025: Teddy Laboratory, a subsidiary of Tigermed, partnered with LabConnect, LLC, a global company in central laboratory services, to build a full-chain laboratory service system covering both China and international markets to accelerate the development and commercialization of innovative drugs globally.

- March 2025: IQVIA, a global drug discovery and development laboratory services organization, launched Site Lab Navigator, an advanced suite of solutions that automates and streamlines lab workflows for clinical trial sponsors and investigator sites.

- October 2024: Thermo Fisher Scientific Inc., showcased its latest innovations enabling the molecule-to-medicine journey and hosted a series of sessions that featured industry developments during CPHI Milan 2024. This helped the company in strengthening its brand presence.

- October 2024: IQVIA expanded and relocated its central laboratory and biorepository operations in Valencia, California, into a new 134,000 square foot state-of-the-art facility.

REPORT COVERAGE

The report provides a detailed global central lab services market analysis and focuses on key aspects such as leading companies and market segmentation, including service type, phase, modality, therapeutic area, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Phase, Modality, Therapeutic Area, End User, and Region |

| By Service Type |

|

| By Phase |

|

| By Modality |

|

| By Therapeutic Area |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.72 billion in 2025 and is projected to reach USD 10.09 billion by 2034.

In 2025, the North America market value stood at USD 2.23 billion.

Growing at a CAGR of 6.5%, the market will exhibit steady growth over the forecast period.

By service type, the safety testing segment is the leading segment in this market.

Introduction of novel lab services is one of the major factors driving the market growth.

Thermo Fisher Scientific Inc. and Labcorp are the major players in the global market.

North America dominated the market share in 2025.

Growing number of clinical trials, rising expansion of central laboratory facilities, growing outsourcing of laboratory services, among others, are some of the crucial factors expected to boost the adoption of these services globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us