Cesium Market Size, Share & Industry Analysis, By Grade (Technical, Pharmaceutical, and Optical), By End-Use Industry (Oil & Gas, Healthcare, Chemical, and Others), and Regional Forecast, 2026-2034

Cesium Market Size and Future Outlook

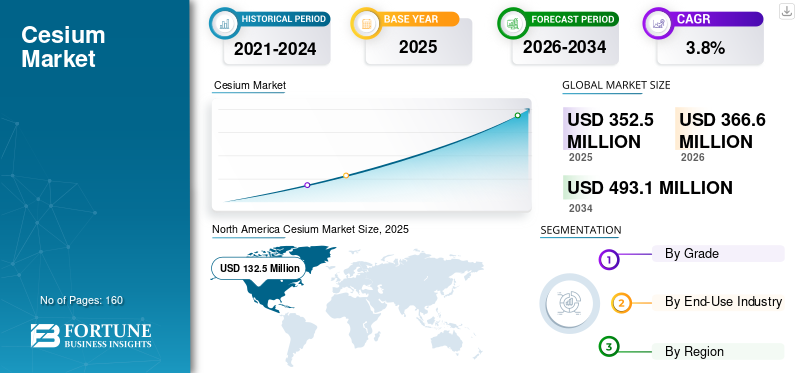

The global cesium market size was valued at USD 352.5 million in 2025. The market is projected to grow from USD 366.6 million in 2026 to USD 493.1 million by 2034, exhibiting a CAGR of 3.8% during the forecast period. North America dominated the global cesium market with a market share of 37.59% in 2025.

Cesium (Cs) is a chemical element classified as a metal with atomic number 55. It is a soft, silver-gold-colored alkali metal with a very low melting point compared to other metals. It has chemical and physical properties similar to those of metals such as rubidium and potassium. It is highly reactive, pyrophoric, and is the least electronegative metal. It is generally employed in various end-uses, including petroleum exploration, electronics, chemicals, medical, and industrial sectors.

Market growth is driven by rising demand across multiple end-use sectors, which is likely to accelerate. The increasing use as a feedstock for a wide range of compounds and derivatives shall boost market growth. Additionally, increasing adoption of cesium compounds for cancer treatment shall bolster the market growth.

Furthermore, the market comprises several major players, including Sinomine Resource Group, Tantalum Mining Corp. of Canada Ltd (Tanco), Thermo Fisher Scientific, American Elements, and Strem Chemicals. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Cesium Market Key Takeaways

- 2025 Market Size: USD 352.5 million

- 2026 Market Size: USD 366.6 million

- 2034 Forecast Market Size: USD 493.1 million

- CAGR: 3.80% from 2026–2034

- North America dominated the market with a 37.59% share in 2025.

- Technical segment dominated with a 60.6% share in 2025.

- Oil & Gas segment led the market with a 55.7% share in 2025.

North America

Valued at USD 132.5 million in 2025 and projected to reach USD 138.8 million in 2026.

Asia Pacific

Expected to reach USD 99.3 million in 2026, driven by electronics and optics manufacturing.

Europe

Projected to reach USD 82.1 million in 2026, supported by precision optics and metrology applications.

U.S.

The U.S. market was valued at USD 117.3 million in 2025.

Japan

The Japan market is witnessing steady growth, driven by high-precision electronics and optical component demand.

Read More

CESIUM MARKET TRENDS

HPHT Well Complexity, Circular Brine Management, and Precision Timing Infrastructure are the Significant Market Trends

Cesium demand continues to be shaped by the oil and gas industry’s need for reliable well control fluids in narrow mud-window and High Pressure High Temperature (HPHT) environments, where high-density, clear brines can reduce solids-related formation damage. At the same time, suppliers are strengthening circularity models for cesium formate through reclamation and reconditioning services, thereby improving economics and extending access to a resource with constrained primary supply. In parallel, high-precision timing remains a stable technology anchor for cesium, as the SI second is defined via the unperturbed hyperfine transition frequency of the cesium-133 atom, supporting long-lived demand in metrology, telecom synchronization, and navigation.

- For instance, formate fluid providers have expanded digital engineering tools (density, PVT, and buffer calculators) to support field design and reduce operational risk, aligning with multi-year procurement cycles for complex offshore wells.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

HPHT Well Control Needs and Zinc-Free High-Density Fluids are Supporting Cesium Formate Adoption, Driving Market Growth

Cesium formate brines are among the few commercially available clear brines capable of achieving very high densities, enabling pressure control in challenging HPHT and deepwater wells. Asset owners value their solids-free nature, potential to minimize formation damage, and suitability for completion and workover operations where productivity and clean-up time are critical. The service model around cesium formate (including engineering support, laboratory testing, and reclamation) further reduces operational uncertainty, which can outweigh the higher upfront cost in high-stakes wells.

- For instance, Sinomine Specialty Fluids reported a contract award for cesium formate completion fluids for Neptune Energy’s Seagull HPHT development, reflecting continued demand for high-density fluids in complex North Sea wells.

MARKET RESTRAINTS

Supply Concentration, Reuse of Brines, and Qualification Burdens Can Limit Market Expansion

The cesium market growth is constrained by limited pollucite-based supply and concentrated processing capacity, which can restrict rapid scale-up. In addition, widespread reuse and reclamation of cesium formate brines reduces annual net make-up volumes, moderating volume-driven growth. For high-purity grades (pharmaceutical and optical), end users often require tight impurity control, documentation, and qualification testing, which extend lead times and increase switching costs.

MARKET OPPORTUNITIES

Radiation Detection Growth and Advanced Timing to Create Lucrative Growth Opportunities

The rising deployment of radiation monitoring systems across healthcare, security, and industrial inspection is driving demand for cesium iodide and related scintillator materials. In precision timing, upgrades in telecom networks, satellite navigation, and national metrology infrastructure sustain demand for cesium-based standards and supporting materials. Opportunities also exist for improved recycling and supply assurance models that expand accessible volumes without relying solely on new mining output.

- For example, the international metrology community continues to refine time and frequency infrastructure and roadmaps, reinforcing the strategic role of cesium-based standards in time dissemination.

MARKET CHALLENGES

Substitution Risk in Some Uses and Oil and Gas Cyclicality to Hamper Market Growth

In certain detection and optics applications, alternative materials and architectures can compete with cesium-based compounds based on cost, afterglow behavior, or integration preferences. For the largest use case (oil and gas), demand can be project-driven and sensitive to operator capex cycles, even if cesium formate remains technically advantaged in select HPHT scenarios. Finally, supply security and compliance requirements increase the importance of long-term contracting and robust quality systems across the value chain.

Segmentation Analysis

By Grade

Technical Segment Led Market Due to Rise in Drilling and Completion Operations

Based on grade, the market is segmented into technical, pharmaceutical, and optical.

The technical segment accounted for the largest cesium market share in 2025. The segment is driven by cesium formate brines used in drilling and completion operations. This grade benefits from performance requirements in HPHT wells and from service-backed supply models that emphasize reuse and reclamation. Furthermore, the segment held 60.6% share in 2025.

The growth of the pharmaceutical segment is supported by regulated healthcare and diagnostic uses, where documentation and impurity control are critical. The pharmaceutical segment is projected to grow at a 3.3% CAGR during the study period.

The optical segment is expected to grow favorably throughout the forecast period, driven by increasing use in radiation detectors, medical imaging, and security screening, where sensitivity and light output matter.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Oil & Gas Segment Dominated Market Due to Extensive Use of the Product

By end-use industry, the market is categorized into oil & gas, healthcare, chemical, and others.

The oil & gas segment accounted for the largest share in 2025, due to the use of cesium formate brines in high-density drilling and completion fluid systems for complex wells. Furthermore, the segment held a 55.7% share in 2025.

The healthcare segment is also expected to experience favorable growth over the projected period. The segment's growth is supported by radiation detection and diagnostic imaging, while other applications include timing, optics, electronics, and scientific instrumentation. The segment is expected to grow at a CAGR of 3.5% over the forecast period.

The chemicals segment is expected to experience favorable growth throughout the forecast period, driven by rises from high-purity electronics/optics precursor chemistries and R&D-driven specialty formulations where substitution is limited.

Cesium Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cesium Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 132.5 million, and is expected to maintain the leading share in 2026, with USD 138.8 million. The region benefits from strong oil and gas activity in complex wells, as well as stable demand from the aerospace, defense, and timing infrastructure sectors. The U.S. accounts for the majority of regional consumption through upstream activity and high-value technology end uses.

U.S. Cesium Market

In 2025, the U.S. market was valued at USD 117.3 million. In the U.S., demand is supported by HPHT well-construction requirements and ongoing needs for precision timing and navigation systems.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

Asia Pacific is also a significant contributor to the market, with the market estimated to reach USD 99.3 million by 2026. The market’s growth is supported by electronics and optics manufacturing, telecom synchronization needs, and expanding healthcare instrumentation in large economies. China remains the largest consumer of cesium compounds in the region, while Japan and South Korea contribute significantly through high-precision electronics and optical components.

China Cesium Market

In 2025, the Chinese market was valued at USD 33.2 million. Electronics, optical materials, and radiation detection components drive China’s market demand. A large downstream manufacturing base for detectors and optoelectronics supports steady consumption of cesium iodide and high-purity cesium compounds.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at 3.2% and reach a valuation of USD 82.1 million in 2026. The region's growth is driven by precision optics, metrology, and high-value electronics applications, with comparatively lower exposure to oil and gas drilling cycles than North America.

U.K. Cesium Market

The U.K. market in 2025 was valued at USD 14.7 million, representing approximately 2.5% of global market revenue.

Germany Cesium Market

Germany’s market was valued at USD 18.6 million in 2025, equivalent to around 4.0% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 18.4 million. The demand in the region is largely import-driven and linked to selective oil and gas projects, industrial uses, and institutional procurement for radiation monitoring.

Middle East & Africa

The Middle East & Africa region is gradually expanding, and was valued at USD 27.9 million in 2025. GCC countries account for the majority of regional demand due to high-pressure well operations where cesium formate fluids can be technically preferred. Outside the GCC, demand is limited and primarily tied to research and radiation detection procurement.

GCC Cesium Market

GCC was valued at USD 17.3 million in 2025, accounting for approximately 2.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Adopting Business Expansion Strategies to Maintain Their Positions in Market

Competition is shaped by access to pollucite-derived feedstock, purification capability, quality systems for high-purity grades, and service models in oil and gas. Upstream supply is highly concentrated, while downstream distribution for research and specialty applications is more fragmented. Some of the key market players include Sinomine Resource Group, Tantalum Mining Corp. of Canada Ltd (Tanco), Thermo Fisher Scientific, American Elements, and Strem Chemicals. Key competitive differentiators include consistency of purity specifications, technical support for application qualification, and circular reclamation capability for cesium formate fluids.

LIST OF KEY CESIUM COMPANIES PROFILED

- Sinomine Resource Group (China)

- Tantalum Mining Corp. of Canada Ltd (Tanco) (Canada)

- Thermo Fisher Scientific (U.S.)

- American Elements (U.S.)

- Strem Chemicals (U.S.)

- ProChem, Inc. (U.S.)

- Sinomine Specialty Fluids Ltd. (Scotland)

- Cabot Corporation (U.S.)

- Avalon Advanced Materials Inc. (Canada)

- GFS Chemicals Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.8% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Grade, End-Use Industry, and Region |

|

By Grade |

· Technical · Pharmaceutical · Optical |

|

By End-Use Industry |

· Oil & Gas · Healthcare · Chemical · Others |

|

By Region |

· North America (By Grade, End-Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Grade, End-Use Industry, and Country) o Germany (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o U.K. (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Grade, End-Use Industry, and Country) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Grade, End-Use Industry, and Country) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America (By End-Use Industry) · Middle East & Africa (By Grade, End-Use Industry, and Country) o GCC (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 352.5 million in 2025 and is projected to reach USD 493.1 million by 2034.

Recording a CAGR of 3.8%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The oil & gas end-use industry segment led in 2025.

North America held the highest market share in 2025.

Sinomine Resource Group, Tantalum Mining Corp. of Canada Ltd (Tanco), Thermo Fisher Scientific, American Elements, and Strem Chemicals are some of the prominent players in the market.

HPHT well control needs and zinc-free high-density fluids are supporting cesium formate adoption, driving market growth.

The major factors expected to favor product adoption in the market are technical performance advantages, reliability, and lifecycle economics enabled by reclamation/reuse services.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us