Champagne Market Size, Share & Industry Analysis, By Color (Rosé and White), By Sweetness Level (Brut, Extra Brut, Demi-Sec, and Doux), By Price Range (Economy, Mid-Premium, and Luxury), By Distribution Channel (On-Trade and Off-Trade) and Regional Forecast, 2026–2034

(Offer valid till 15th Jul 2026)

Champagne Market Overview

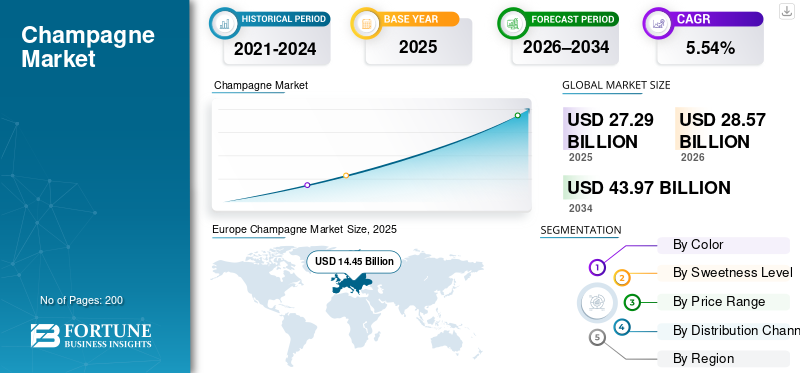

The global champagne market size was valued at USD 27.29 billion in 2025. The market is projected to grow from USD 28.57 billion in 2026 to USD 43.97 billion by 2034, exhibiting a CAGR of 5.54% during the forecast period. Europe dominated the champagne market with a market share of 52.94% in 2025.

Champagne is a sparkling wine made in the Champagne region of northeastern France. The Emerging consumer shift towards premium, authentic, and luxury products is primarily driving demand for the product. Increasing disposable income among younger demographics, particularly Millennials, and growing wine tourism also contribute to this rise, along with trends in health-conscious options.

Moët & Chandon, Comité Champagne, G.H. Mumm & Cie, Laurent-Perrier, and Piper-Heidsieck, among others, dominate the market.

Download Free sample to learn more about this report.

Champagne Market Takeaways

- 2025 Market Size: USD 27.29 billion

- 2026 Market Size: USD 28.57 billion

- 2034 Forecast Market Size: USD 43.97 billion

- CAGR: 5.54% from 2026–2034

- Europe dominated the champagne market with a 52.94% share in 2025.

- The rose color segment is projected to grow at the fastest CAGR of 8.18% during 2026–2034.

- The extra brut segment is expected to register the fastest CAGR of 9.03% over the forecast period.

North America

North America accounted for USD 2.74 billion in 2025 and is projected to grow at a CAGR of 5.16% through 2034.

Europe

Europe led the global market with a valuation of USD 14.45 billion in 2025 and is expected to expand at a CAGR of 4.46%.

Asia Pacific

Asia Pacific reached USD 7.31 billion in 2025 and is projected to be the fastest-growing regional market with a CAGR of 7.24%.

U.S.

The champagne market was valued at approximately USD 2.40 billion in 2025 and is expected to expand at a CAGR of 5.39% during the forecast period.

Japan

The market reached USD 2.43 billion in 2025, supported by strong demand from gifting, weddings, festivals, and corporate celebrations.

Read More

Champagne Market Trends

Collaboration Strategy to Promote the Luxury Product to Change the Market Landscape

Champagne is a luxury alcoholic beverage that has recently become more popular across Asian countries such as China, India, and Japan. LVMH, owner of Moët & Chandon and Veuve Clicquot, claimed that China is the 14th-largest importer of Champagne, just behind Denmark. China’s wine-buying habits have historically lagged those of the West, leaving the region with massive long-term upside. Since the demand for the product is increasing gradually, companies are focusing on collaborating with celebrities and fashion influencers to promote their luxury product categories to their target consumer group. It is significantly contributing to changing the global champagne market landscape in the forecast period.

- In February 2025, Dom Pérignon, a LVMH champagne brand, collaborated with Japanese artist Takashi Murakami to develop a creative and luxury packaging for its limited edition product - Vintage 2015 and Rosé Vintage 2010.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Premiumization and Rising Demand for Luxury Alcoholic Beverages Driving Market Growth

The ongoing premiumization trend within the alcoholic beverages industry primarily drives the global champagne market. Champagne’s strong cultural association with celebrations, weddings, corporate events, fine dining, and festive occasions continues to underpin stable baseline demand. Increasing consumer disposable income shifted their purchasing behavior. Further, consumers from North America and Asian countries are focusing on making their special occasions more premium and memorable. This factor is likely to push up the price of luxury alcoholic beverages, such as Champagne. Growth in the global hospitality sector, including luxury hotels, premium restaurants, cruise tourism, and destination weddings, directly supports champagne sales through on-trade channels. Changes in consumer purchasing behavior reflect changes in market growth. Thus, several champagne manufacturers are experiencing strong sales of their vintage champagne and special-edition products in Asian countries, especially in China.

- According to Thibaut Le Mailloux, a marketing director at one of the popular champagne-making companies, Champagne Gosset, their limited-edition and vintage champagne collection véCuvée e, 15 Ans de Caà Minaima, has sold out in China.

Market Restraints

High Pricing, Production Constraints, and Limited Geographic Supply Restricting Market Expansion

Champagne production is legally restricted to the Champagne region of France and governed by strict appellation rules, yield limits, and aging requirements. These structural constraints limit scalability and create supply rigidity. Combined with high grape prices, long maturation cycles, labor-intensive production, and rising logistics costs. The product remains significantly more expensive than alternatives such as Blanc de blancs, Prosecco, and Cava. This restricts penetration in price-sensitive markets and limits volume growth outside premium consumer segments.

Market Opportunities

E-commerce Sales and Popularity of the Product in Emerging Economies to Change the Industry Landscape.

The expansion of online alcohol retail, direct-to-consumer sales models, and curated premium gifting platforms is significantly improving accessibility and brand visibility for champagne producers. Digital channels enable producers to reach younger, affluent consumers, offer limited editions, and personalize gifting experiences—supporting incremental volume and margin growth.

Additionally, developing nations such as China, India, and Brazil are importing the product for domestic consumption, as it has become a popular option for celebrating special occasions. Furthermore, millennial consumers' preferences for luxury alcohol beverages are fueling the global champagne market growth.

- According to the World Integrated Trade Solutions, a trade-related wing of the World Bank, India imported 431,914 liters of the product from France, Italy, the U.K., Australia, and Spain in 2023.

SEGMENTATION ANALYSIS

By Color

Broader Acceptance and the Availability of the White Champagne to Hold the Largest Share

On the basis of color, the champagne market is segmented into white and rosé.

The white segment dominated the market in 2025, valued at USD 23.31 billion, and accounts for the majority of global consumption due to its broad consumer acceptance, versatility across occasions, and strong alignment with traditional champagne preferences. It is widely consumed in both on-trade and off-trade channels, making it the default choice for celebrations, hospitality, gifting, and everyday premium consumption. Also, the wide acceptance and availability of the product across multiple channels will drive the segment’s growth.

The rosé color segment is projected to grow at the fastest CAGR of 8.18% during 2026–2034. Rosé champagne remains a premium, niche segment driven by aesthetics and exclusivity rather than volume-led demand.

By Sweetness Level

Balanced Taste and Lower Sugar to Drive the Brut Segment Growth

Based on the sweetness level, the market is segmented into brut, extra brut, demi-sec, and doux.

The brut segment led the global champagne market share in 2025, reaching USD 18.94 billion. The segment dominated the international market due to its balanced dryness, broad palate appeal, and suitability across a wide range of occasions and food pairings. Brut’s alignment with evolving consumer preferences toward lower sugar and cleaner taste profiles further strengthens its dominance.

The extra brut segment is expected to grow at the fastest CAGR of 9.03%. Extra brut aligns well with the broader premiumization trend, as it is perceived as more refined, authentic, and terroir-driven compared to sweeter styles. Fine-dining restaurants and sommeliers increasingly promote extra brut for food pairings, supporting on-trade demand growth.

To know how our report can help streamline your business, Speak to Analyst

By Price Range

Affordability Pricing and High Volume consumption to lead the Mid-Premium Category Segment Growth

By price range, the market is categorized into economy, mid-premium, and luxury.

The mid-premium segment held the largest share of the champagne market in 2025, valued at USD 10.16 billion. The mid-price point segment is rising due to a balance of brand prestige, quality assurance, and relative affordability, making it accessible to a broad consumer base across both on- and off-trade channels. This segment includes non-vintage and well-known house labels that are widely used for celebrations, gifting, and hospitality, ensuring consistent volume demand.

The luxury segment is projected to grow at the fastest CAGR of 7.12%. The segment is emerging rapidly, driven by premiumization, rising high-net-worth populations, and increasing demand for vintage, prestige cuvée, and limited-edition champagnes.

By Distribution Channel

High Presence of the Product in Off-Trade Channels Holds the Highest Market Shares

Based on the distribution channel, the market is segmented into on-trade and off-trade.

Off-trade channels accounted for the largest share in 2025, valued at USD 14.04 billion. Off-trade channels, including supermarkets, hypermarkets, specialty wine stores, and online retail, dominate champagne sales due to greater product availability, competitive pricing, and strong home consumption trends. The shift toward at-home celebrations, gifting, and e-commerce has further strengthened off-trade channel growth.

On-trade channels are projected to witness the fastest CAGR of 6.94%. On-trade channels, such as hotels, restaurants, bars, clubs, and luxury hospitality venues, are experiencing more rapid growth as global tourism, fine dining, and experiential consumption rebound. Premium champagne consumption is robust in on-trade settings, where brand visibility, curated menus, and social experiences drive higher per-unit value.

Champagne Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

Europe Champagne Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 2.74 billion in 2025 and is projected to grow at a CAGR of 5.16% (2026–2034). Increasing lifestyle-driven alcohol consumption at home, along with the strong influence of celebrity & social media, and rapid expansion of online alcohol sales, is driving the market in the region.

U.S. Champagne Market

The U.S. champagne market was valued at approximately USD 2.40 billion in 2025 and is expected to expand at a CAGR of 5.39% during the forecast period. The U.S. represented the largest share, driven by at-home luxury consumption, including brunch culture, casual entertaining, and premium gifting, rather than being limited to formal celebrations.

Europe

Europe dominates the market in both value and volume consumption of the product, accounting for USD 14.45 billion in 2025 and expanding at a CAGR of 4.46%. Deep-rooted cultural consumption is driving product consumption in the region. Due to the entrenched wine culture and routine social dining occasions, the consumption of the product is increasing beyond major celebrations.

France Champagne Market

France accounted for approximately USD 6.55 billion in 2025, driven by cultural factors, along with inbound tourism and luxury travel, which are driving champagne sales in hotels, fine dining restaurants, and experiential venues across

Asia Pacific

Asia Pacific reached USD 7.31 billion in 2025 and is the fastest-growing region, with a 7.24% CAGR. Rapid urbanization, rising middle-class income, and the emergence of premium beverages and the expansion of Western dining habits are expected to drive the market growth in the region.

China Champagne Market

China was valued at USD 2.18 billion in 2025, driven by increasing luxury alcohol consumption patterns paired with the rapid development of upscale restaurants, luxury hotels, and international hospitality chains to drive the industry in the country.

Japan Champagne Market

Japan reached USD 2.43 billion in 2025, supported by high-value gifting during festivals, weddings, and corporate events, which is accelerating champagne demand.

South America and the Middle East & Africa

South America accounted for USD 1.04 billion in 2025, growing at a CAGR of 6.80%. Market expansion is supported by strong social media influence and an increased urban population with higher income levels.

The Middle East & Africa market was valued at USD 1.75 billion in 2025, expanding at a CAGR of 6.18%. The concentration of luxury hospitality and high-end tourism drives growth.

South Africa Champagne Market

The South African champagne market was valued at approximately USD 0.39 billion in 2025 and is projected to grow at a CAGR of 6.67% during 2026–2034. The market is driven by the growing popularity of established Western dining and entertainment habits.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Are Focused on Innovation, Portfolio Expansion, and Strategic Partnerships

The global champagne market share is highly consolidated, dominated by a limited number of large, heritage-driven champagne houses alongside a fragmented base of small and grower-producers. Key players such as Moët & Chandon, Comité Champagne, G.H. Mumm & Cie, Laurent-Perrier, and Piper-Heidsieck are dominating the market and strategically emphasize flagship non-vintage labels to stabilize volume, complemented by vintage, rosé, and prestige cuvées to drive margin expansion. These key players' strong heritage, craftsmanship, and vineyard provenance to reinforce long-term brand equity and premium pricing are strengthening their shares in the global market.

Key Players in the Champagne Market

|

Rank |

Company Name |

|

1 |

Moët & Chandon |

|

2 |

Comité champagne |

|

3 |

G.H. Mumm & Cie |

|

4 |

Laurent-Perrier |

|

5 |

Piper-Heidsieck |

List of Key Champagne Companies Profiled

- Moët & Chandon (France)

- Comité champagne (France)

- H. Mumm & Cie (France)

- Laurent-Perrier (France)

- Piper-Heidsieck (France)

- Taittinger (France)

- Bollinger (France)

- Louis Roederer (France)

- Univins et Spiritueux (Canada)

- Cook's Champagne (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Laurent-Perrier, one of the key brands, launched its new cuvée, Héritage, which blends innovation and tradition to reinvigorate Champagne. The latest product is launched to target a budget-conscious consumer group.

- July 2025: Champagne Telmont, a France-based company, redeveloped its packaging with new technology. The company introduced ultra-lightweight bottles for its product. The company reshaped its packaging to align with the market's sustainable packaging trend.

- June 2025: Champagne EPC, one of the sparkling wine manufacturing companies, acquired Champagne Charles Mignon, a renowned family-owned house in the heart of Épernay. The acquisition will help the company strengthen its production and supply chain operations.

- October 2024: Castel Group, a French-based multinational beverages company, acquired the Champagne house Malard for an undisclosed amount. The acquisition helps the company expand its presence in the champagne category.

- May 2024: Aurélie Ponnavoy, a trained oenologist from France, launched her own champagne brand, Mademoiselle Marg’O.

REPORT COVERAGE

The market industry report analyzes the market in depth. It highlights crucial aspects such as global champagne market trends, supply chain, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the research report also provides insights into the global Champagne market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2024 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.54% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Color

|

|

By Sweetness Level

|

|

|

By Price Range

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 27.29 billion in 2025 and is anticipated to reach USD 43.97 billion by 2034.

At a CAGR of 5.54%, the global market will grow steadily over the forecast period.

By sweetness level, the brut segment led the market.

Europe held the largest market share in 2025.

Premiumization and rising demand for luxury alcoholic beverages are driving market growth.

Moet & Chandon, Comite Champagne, G.H. Mumm & Cie, Laurent-Perrier, and Piper-Heidsieck, among others, are the leading companies in the market.

A collaboration strategy to promote the luxury product to change the market landscape.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us