Chemical Logistics Market Size, Share & Industry Analysis, By End-User Industry (Basic/Commodity Chemicals, Specialty Chemicals, and Oil & Gas/Petrochemicals), By Mode of Transport (Road, Rail, Sea/Waterways, and Air), By Service Type (Transportation & Distribution, Storage & Warehousing, Green Logistics Services, and Consulting & Management Services), By Cargo Form (Bulk Form, Packaged Form, and Temperature-Controlled Form), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

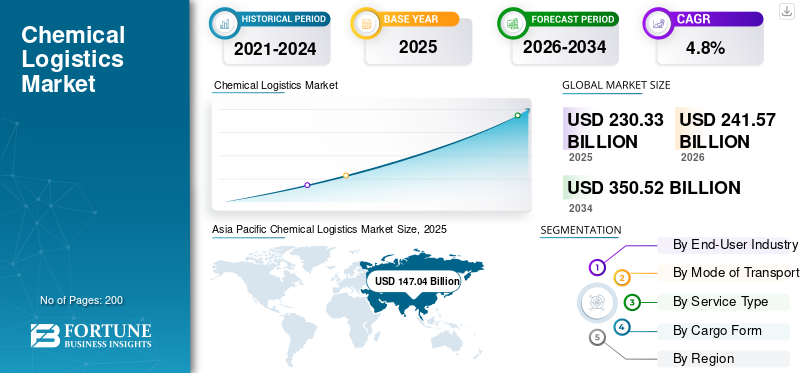

The global chemical logistics market size was valued at USD 230.33 billion in 2025. The market is projected to grow from USD 241.57 billion in 2026 to USD 350.52 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. Asia Pacific dominated the global chemical logistics market with a market share of 63.83% in 2025.

The global market growth is experiencing a steady rise, driven by expanding chemical production and trade, stricter safety and environmental compliance requirements, and increasing demand for specialized handling of hazardous and temperature-sensitive products. Chemical manufacturers are increasingly relying on specialist logistics providers for end-to-end solutions that cover bulk liquids, ISO tanks, warehousing, and compliant cross-border distribution, aiming to reduce risk, improve service reliability, and manage complex multimodal networks. Growth in life sciences and high-value specialty chemicals is also increasing the need for traceability, controlled environments, and higher service intensity. At the same time, digitalization (including real time tracking, visibility, and planning) and terminal/asset investments are enhancing efficiency and resilience across chemical supply chains.

For instance, in 2025, DHL Supply Chain entered into a multi-year Lead Logistics Partner (LLP) agreement with Sanyo Chemical Industries in Japan, with logistics personnel expected to transfer to DHL in October of that year, thereby strengthening DHL’s chemical logistics operating model and expanding managed logistics capabilities for a major chemical manufacturer.

Furthermore, leading players such as DHL Supply Chain, HOYER Group, and Bertschi continue to expand their capabilities through partnerships and infrastructure investments. For example, Bertschi inaugurated a new chemical logistics terminal in Antwerp in 2025 to support intermodal chemical supply chains.

Download Free sample to learn more about this report.

CHEMICAL LOGISTICS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 230.33 Billion

- 2026 Market Size: USD 241.57 Billion

- 2034 Forecast Market Size: USD 350.52 Billion

- CAGR: 4.8% from 2026–2034

- Asia Pacific dominated the global chemical logistics market with a 63.83% share in 2025.

- The oil & gas/petrochemicals segment held the largest share of the market in 2025.

- Road transport segment dominated the market as the leading mode of transport.

Asia Pacific

Asia Pacific accounted for 63.83% of the global chemical logistics market in 2025.

North America

North America remained a key market supported by large-scale chemical production and distribution networks.

Europe

Europe continued to witness steady growth, led by Germany and the U.K. with strong cross-border chemical trade.

U.S.

Remained the largest market in North America, supported by extensive petrochemical and freight transportation infrastructure.

Japan

Maintained a strong position in Asia Pacific with demand driven by specialty and high-value chemical logistics.

Read More

CHEMICAL LOGISTICS MARKET TRENDS

Expansion of Digital and Automated Chemical Supply Chains Enhances Logistics Efficiency

Chemical logistics providers are increasingly adopting digital tools, such as real-time shipment tracking, warehouse management systems, and predictive analytics, to enhance visibility, safety, and efficiency across complex supply chains. Automation in terminals and warehouses reduces manual handling risks, while digital documentation supports regulatory compliance for hazardous chemicals. These technologies enable logistics operators to optimize routing, reduce delays, and enhance asset utilization, particularly for bulk and temperature-sensitive chemicals. As chemical trade becomes more global and compliance-driven, digital integration is becoming a structural trend rather than an optional upgrade.

In June 2024, BASF highlighted the use of digital supply chain platforms to improve transparency and logistics efficiency across its global chemical operations.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Chemical Production Drives Demand for Specialized Logistics Services

Growth in chemical production directly increases the need for transportation, storage, and handling of hazardous and non-hazardous materials. Expanding output in petrochemicals, specialty chemicals, and industrial intermediates requires reliable logistics partners capable of managing bulk movements, adhering to compliance requirements, and facilitating multimodal transport. As production scales in both mature and emerging markets, logistics demand rises in volume and in complexity, supporting the chemical logistics market growth. Chemical producers increasingly rely on third-party logistics providers to ensure continuity of supply and cost efficiency.

In September 2024, the American Chemistry Council reported continued growth in U.S. chemical production, reinforcing downstream logistics demand.

MARKET RESTRAINTS

Stringent Safety and Environmental Regulations Increase Operational Constraints

Chemical logistics operations are subject to strict safety, environmental, and transportation regulations governing the handling of hazardous materials, emissions, and waste. Compliance increases costs through the use of specialized equipment, trained personnel, documentation, and regular audits. Regulatory complexity across borders further constrains operational flexibility and slows network expansion, particularly for smaller logistics providers. These factors can limit scalability and margin growth despite rising demand. Regulatory requirements burdens are especially pronounced in cross-border transport involving chemicals classified as dangerous goods.

In January 2023, the European Chemicals Agency updated guidance on hazardous chemical transport compliance under REACH and CLP regulations.

MARKET OPPORTUNITIES

Growth of Specialty Chemicals and Life Sciences Creates High-Value Logistics Opportunities

The increasing share of specialty chemicals, pharmaceuticals, and performance materials is generating demand for high-value logistics services, including temperature-controlled transport, secure warehousing, and advanced traceability. These products typically move in smaller volumes but require higher service intensity, allowing logistics providers to capture greater value per shipment. The expansion of healthcare, agrochemicals, and advanced manufacturing creates long-term opportunities for specialized chemical logistics solutions. Providers with ensured compliance expertise and dedicated infrastructure are best positioned to reap the benefits.

In April 2024, Lonza announced investments to expand life-sciences manufacturing capacity, implying higher demand for compliant and temperature-controlled logistics.

MARKET CHALLENGES

Infrastructure Gaps and Asset Intensity Pose Long-Term Operational Challenges

The chemical logistics sector requires capital-intensive assets, including tank terminals, ISO containers, specialized vehicles, and compliant warehouses. In many emerging markets, limited port capacity, inadequate rail connectivity, and insufficient hazardous material infrastructure restrict the efficient movement of chemicals. These gaps increase transit times, handling risks, and operating costs. Even in developed regions, upgrading aging infrastructure to meet sustainability and safety standards remains a significant challenge. High upfront investment and long payback periods can deter rapid expansion.

In February 2024, UNCTAD highlighted infrastructure and port-capacity constraints affecting chemical and bulk trade flows in developing economies.

Download Free sample to learn more about this report.

Segmentation Analysis

By End-User Industry

Large-Scale Petrochemical Supply Chains Sustain Oil & Gas/Petrochemicals Segment Dominance

Based on end-user industry, the market is segmented into basic/commodity chemicals, specialty chemicals, and oil & gas/petrochemicals.

The oil & gas/petrochemicals segment dominates the chemical logistics market share due to consistently high volumes of feedstocks, intermediates, and derivatives that require continuous movement between refineries, crackers, terminals, and downstream manufacturers. These products are largely hazardous and bulk in nature, demanding specialized tankers, terminals, and strict compliance, which increases logistics intensity and spend. Strong integration of upstream and downstream operations further sustains repeat, long-haul logistics demand across regions.

In March 2024, Saudi Aramco announced the advancement of multiple petrochemical expansion projects, underscoring the long-term demand for bulk petrochemical movements in logistics.

The specialty chemicals segment is anticipated to rise with a CAGR of 6.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Mode of Transport

Extensive Domestic Distribution Networks Drive Road Transport Supremacy

Based on mode of transport, the market is segmented into road, rail, sea/waterways, and air.

Road transport dominates chemical logistics due to its unmatched flexibility and ability to connect production plants, warehouses, ports, and end users. It is essential for first-mile and last-mile delivery, particularly for domestic and regional chemical distribution. Despite higher per-unit costs compared to rail or sea, road transport remains indispensable for time-sensitive deliveries, smaller shipment sizes, and markets with limited rail or pipeline access.

In July 2023, the U.S. Department of Energy highlighted that trucking accounts for nearly three-fourths of the freight value moved nationwide.

The rail segment is projected to grow at a CAGR of 5.5% over the forecast period.

By Service Type

Core Movement of Chemicals Sustains Transportation & Distribution Service Dominance

Based on service type, the market is segmented into transportation & distribution, storage & warehousing, green logistics services, and consulting & management services.

The transportation & distribution segment dominates the market as the physical movement of chemicals is the foundation of the supply chain. Every chemical produced must be transported at least once, ensuring this service captures the largest share of logistics spending. High safety requirements, hazardous material regulations, and multimodal coordination further elevate service value, particularly for bulk and regulated chemicals.

In December 2024, DHL Supply Chain expanded its chemical transport fleet and distribution capabilities to support growing customer demand.

The green logistics services segment is projected to grow at a CAGR of 6.9% over the forecast period.

By Cargo Form

High-Volume Liquid and Gas Shipments Reinforce Bulk Form Leadership

Based on cargo form, the market is segmented into bulk form, packaged form, and temperature-controlled form.

The bulk form dominates chemical logistics, as the majority of global chemical volumes, including crude derivatives, solvents, acids, and industrial gases, are transported in liquid or gaseous states. Bulk logistics benefits from economies of scale, standardized handling infrastructure, and direct integration with production and export facilities. Continuous demand from the petrochemical and basic chemicals industries ensures stable utilization of tank trucks, rail tank cars, pipelines, and tank terminals.

In November 2023, Royal Vopak reported sustained demand for bulk liquid storage linked to global chemical and energy supply chains.

The temperature-controlled form segment is projected to grow at a CAGR of 7.0% over the forecast period.

CHEMICAL LOGISTICS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Chemical Logistics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the fastest-growing chemical logistics region, driven by expanding chemical production, export-oriented supply chains, and infrastructure investment. China, Japan, and India collectively drive demand through large volumes of petrochemicals, rising specialty output, and increasing outsourcing to professional logistics providers.

China Chemical Logistics Market

Massive petrochemical production, strong export flows, and extensive port infrastructure lead China’s market. High volumes of bulk chemical movements and the growth of specialty segments drive demand for logistics.

Japan Chemical Logistics Market

Japan’s chemical logistics growth is supported by specialty and high-value chemicals, which require reliable, compliant, and maritime-focused transport solutions across both domestic and international routes.

India Chemical Logistics Market

India is experiencing rapid growth due to the expansion of chemical manufacturing, improvements in port and rail infrastructure, and an increasing need for organized logistics to support both domestic and export-oriented chemical flows.

North America

North America exhibits stable growth in chemical logistics, driven by a robust petrochemical base, integrated cross-border trade, and advanced logistics infrastructure. The U.S. drives regional demand through large-scale chemical production, extensive domestic distribution networks, and high outsourcing to specialized logistics providers. Growth is reinforced by railroad intermodal connectivity, port modernization, and rising shipments of specialty and regulated chemicals that require compliant transport and storage solutions.

U.S. Chemical Logistics Market

Large petrochemical clusters, high domestic freight activity, and strong adoption of third-party logistics drive the U.S. market. Continued investment in rail, pipelines, and port infrastructure supports the movement of long-haul bulk and specialty chemicals.

Europe

Europe’s market is growing steadily, driven by a strong mix of specialty chemicals, stringent safety regulations, and cross-border intra-EU trade. Germany and the U.K. anchor regional demand through advanced manufacturing, high logistics compliance intensity, and multimodal transport networks. Growth is increasingly supported by rail and inland waterways as companies optimize costs and emissions.

U.K. Chemical Logistics Market

Specialty chemicals, pharmaceuticals, and port-centric distribution support the U.K. market. A strong reliance on road and maritime logistics, combined with regulatory compliance requirements, sustains demand for value-added chemical logistics services.

Germany Chemical Logistics Market

Germany dominates Europe’s chemical logistics through its large industrial base, dense rail network, and central location. Strong intermodal connectivity enables efficient distribution of bulk and specialty chemicals across domestic and cross-border corridors.

Rest of the World

The Rest of the World market, comprising Latin America, the Middle East & Africa, continues to grow steadily, driven by petrochemical exports, industrialization, and improved trade infrastructure. The Middle East drives bulk chemical logistics through large petrochemical hubs, while Latin America and Africa contribute through rising chemical consumption and port-based trade flows.

COMPETITIVE LANDSCAPE

Key Industry Players

Specialized Asset Networks, Compliance Expertise, and Digital Integration Shape Chemical Logistics Competitiveness

The global chemical logistics market trends are characterized by high entry barriers, primarily driven by the intensity of assets, regulatory compliance, and the critical nature of safety operations. Leading players, including DHL Supply Chain, CEVA Logistics, Kuehne + Nagel, DB Schenker, Bertschi, Hoyer Group, and Mitsui O.S.K. Lines, compete through extensive tank container fleets, dedicated chemical warehouses, terminal access, and multimodal networks. Investments in digital platforms, safety protocols, systems, and sustainability initiatives increasingly shape competitiveness. Companies strengthen market position through long-term contracts with chemical producers, geographic expansion near production hubs, and partnerships across shipping, rail, and terminal operators.

LIST OF KEY CHEMICAL LOGISTICS COMPANIES PROFILED

- DHL Supply Chain (Germany)

- Kuehne+Nagel (Switzerland)

- DB Schenker (Germany)

- DSV (Denmark)

- P. Moller – Maersk (Denmark)

- GEODIS (France)

- CEVA Logistics (France)

- DP World (UAE)

- Bertschi AG (Switzerland)

- HOYER Group (Germany)

- Odyssey Logistics & Technology (U.S.)

- H. Robinson (U.S.)

- XPO Logistics (U.S.)

- Nippon Express (NX Group) (Japan)

- Bulkhaul Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Alexander Chemical Corporation celebrated its 75th anniversary, launching its USD 18 million Alexander Cylinder Solutions division, which focuses on gas cylinder maintenance, lifecycle management, and logistics services. The new division expands the company’s logistics capabilities, supporting chemical handling, storage, and distribution services for industrial gases and related chemicals, thereby reinforcing its service portfolio and regional presence.

- In September 2025, Elemica and Agilis announced a strategic partnership delivering the chemical industry’s first integrated digital commerce and supply chain execution solution. The platform unites digital buyer engagement with a network-enabled execution backbone, enabling seamless order flow from discovery to delivery. This system enhances transparency, lowers cost-to-serve, accelerates growth, and establishes an AI-ready foundation for future planning and decision intelligence across chemical supply chains.

- In September 2025, DHL Supply Chain announced key global leadership appointments to strengthen its customer-centric strategy and logistics capabilities. New roles include a Chief Development Officer and regional Chief Customer Officers for Europe and the Middle East & Africa. These appointments are designed to drive growth, enhance strategic partnerships, and deliver tailored supply chain solutions across diverse global markets.

- In May 2025, GXO Logistics and Blue Yonder entered a strategic global agreement to deploy advanced end-to-end logistics software solutions. The partnership aims to enhance warehouse inventory management systems and supply chain automation, thereby boosting speed, flexibility, and predictability for customers across various industries, including this sector. The deal supports GXO’s scaling ambitions and allows Blue Yonder’s digital tools to improve real-time forecasting and operational insights.

- In April 2025, DHL Express expanded its enhanced Medical Express (WMX) service with a new route from Brazil to the USA. While focused on pharmaceutical logistics, this expansion exemplifies the trend in chemical logistics for expedited, temperature-controlled transport. The service connects Latin American hubs to U.S. laboratories in under 30 hours for urgent, regulated shipments, underscoring the demand for high-precision logistics solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.8% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By End-User Industry, By Mode of Transport, By Service Type, By Cargo Form, and By Region |

|

By End-User Industry |

· Basic/Commodity Chemicals · Specialty Chemicals · Oil & Gas/Petrochemicals |

|

By Mode of Transport |

· Road · Rail · Sea/Waterways · Air |

|

By Service Type |

· Transportation & Distribution · Storage & Warehousing · Green Logistics Services · Consulting & Management Services |

|

By Cargo Form |

· Bulk Form · Packaged Form · Temperature-Controlled Form |

|

By Region |

· North America (By End-User Industry, By Mode of Transport, By Service Type, By Cargo Form, and By Country) o U.S. (By Mode of Transport) o Canada (By Mode of Transport) o Mexico (By Mode of Transport) · Europe (By End-User Industry, By Mode of Transport, By Service Type, By Cargo Form, and By Country) o Germany (By Mode of Transport) o U.K. (By Mode of Transport) o France (By Mode of Transport) o Rest of Europe (By Mode of Transport) · Asia Pacific (By End-User Industry, By Mode of Transport, By Service Type, By Cargo Form, and By Country) o China (By Mode of Transport) o Japan (By Mode of Transport) o India (By Mode of Transport) o South Korea (By Mode of Transport) o Rest of Asia Pacific (By Mode of Transport) · Rest of the World (By End-User Industry, By Mode of Transport, By Service Type, and By Cargo Form) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 230.33 Billion in 2025 and is projected to reach USD 350.52 Billion by 2034.

In 2025, the market value stood at USD 147.04 billion.

The market is expected to grow at a CAGR of 4.8% during the forecast period of 2026-2034.

The transportation & distribution segment leads the market share in the service type segment.

Rising global chemical production drives demand for specialized logistics services.

Top players in the market include DHL Supply Chain, Kuehne + Nagel, DB Schenker, DSV, and A.P. Moller–Maersk.

Asia Pacific accounted for the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us