Clinical Alarm Management Market Size, Share & Industry Analysis, By Component (Software/Platforms {Alarm Management Platforms, Clinical Communication & Collaboration Platforms, Alarm Analytics & Reporting Tools, Clinical Surveillance & Early Warning Systems, and Others} and Services), By Deployment (Cloud-based, On-premise, and Hybrid), By Alarm Source (Patient Monitoring Systems, Ventilators, Infusion Pumps, Nurse Call Systems, Telemetry Systems, and Others), By End User (Hospitals & ASCs, Long-term Care & Post-acute Care Facilities, and Others), and Regional Forecast, 2026-2034

Clinical Alarm Management Market Size and Future Outlook

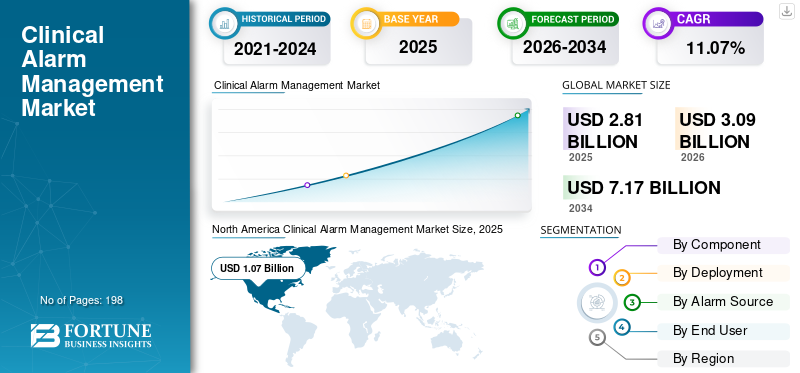

The global clinical alarm management market size was valued at USD 2.81 billion in 2025 and is projected to grow from USD 3.09 billion in 2026 to USD 7.17 billion by 2034, exhibiting a CAGR of 11.07% during the forecast period. North America dominated the clinical alarm management market with a market share of 38.08% in 2025.

Clinical alarm management systems are employed to collect, prioritize, direct, and escalate alarms produced by various connected clinical devices. These solutions aid in minimizing alarm fatigue, enhancing caregiver response rates, promoting patient safety, and bolstering workflow efficiency in hospitals, ambulatory surgical facilities, and post-acute care environments. The market is growing as healthcare organizations boost investments in alarm management solutions, tools for clinical communication and collaboration, middleware for medical device integration, alarm analytics, and clinical surveillance systems to handle increasing alarm levels in ICUs, emergency departments, operating rooms, telemetry units, and general wards. The market is further bolstered by rising demand for both centralized and decentralized alarm workflows, heightened adoption of mobile alerting and virtual nursing approaches, an increased emphasis on minimizing non-actionable alarms, and growing utilization of cloud-based and hybrid solutions that enhance interoperability, reporting, and overall alarm visibility across the enterprise.

Key players operating in the global market include Stryker, GlobeStar Systems, Inc., Ascom, Koninklijke Philips N.V., Baxter, and others. These firms are focusing on platform enhancement, medical device and EHR integration, alarm analytics expansion, clinical surveillance capabilities, strategic acquisitions, and workflow automation initiatives to strengthen their market presence.

Download Free sample to learn more about this report.

CLINICAL ALARM MANAGEMENT MARKET TRENDS

Increasing Adoption of Connected Medical Devices is a Major Trend

The growing use of interconnected medical devices is emerging as a significant trend in the clinical alarm management industry. Hospitals are employing additional patient monitors, ventilators, infusion pumps, nurse call systems, smart beds, telemetry systems, and wearable monitoring devices, leading to a rise in the volume of alarms produced throughout care environments. With the rise of alarm sources, hospitals require middleware and alarm management systems that can gather device information, eliminate non-actionable alerts, and direct essential notifications to the appropriate caregiver. This is also raising the need for clinical communication platforms, as alarms must now be sent via mobile devices, badges, dashboards, and centralized monitoring systems.

The trend is particularly prominent in ICUs, emergency departments, telemetry units, operating rooms, and virtual monitoring systems, where numerous devices link to each patient. Consequently, vendors are concentrating on device compatibility, immediate alert distribution, and monitoring features to assist hospitals in diminishing alarm fatigue and enhancing response times. Throughout the forecast period, this trend is anticipated to facilitate increased adoption of middleware for medical device integration, alarm analytics, and platforms for clinical surveillance. These factors are supporting the overall global clinical alarm management market growth.

- For instance, in March 2025, Stryker launched the Sync Badge, a hands-free wearable communication device for care teams. The company stated that, through integration with Vocera Engage middleware, the device can receive information from the EHR, nurse call systems, patient monitoring systems, medical devices, connected beds, stretchers, and other systems, allowing care teams to receive actionable alarms and notifications directly on the badge.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Alarm Fatigue across Hospitals to Boost Market Growth

Rising alarm fatigue is one of the strongest drivers for the market, as hospitals are dealing with a high number of alarms from patient monitors, ventilators, infusion pumps, telemetry systems, nurse call systems, and other connected devices. Many of these alarms are non-actionable or low priority, which can make clinicians less responsive and increase the risk of delayed intervention. This is pushing hospitals to adopt alarm management platforms that can filter unnecessary alarms, prioritize critical alerts, route alarms to the right caregiver, and escalate alerts when there is no response. The need is especially high in ICUs, emergency departments, telemetry units, operating rooms, and high-acuity wards where alarm volumes are heavy. As hospitals focus more on patient safety, staff efficiency, and nurse burnout reduction, demand is increasing for alarm analytics, clinical communication platforms, and medical device integration middleware. Therefore, alarm fatigue is directly supporting the growth of software-led alarm management solutions across hospitals and health systems.

- For instance, in October 2025, Nihon Kohden launched AlarmSense, a data-driven analytics platform designed to streamline hospital response management and reduce alarm fatigue for clinical teams.

MARKET RESTRAINTS

High Implementation and Integration Complexity to Limit Market Growth

Significant complexity in implementation and integration serves as a key limitation for the market, as these systems need to interface with various hospital technologies simultaneously, such as patient monitors, ventilators, infusion pumps, nurse call systems, telemetry systems, EHRs, mobile devices, and hospital networks. Numerous hospitals continue to rely on outdated infrastructure and equipment from various vendors, complicating interoperability and prolonging deployment time. When alarms are not integrated correctly, hospitals could encounter repeated alerts, postponed notifications, overlooked alarms, or diminished caregiver confidence in the system. This also heightens the demand for personalization, interface evaluations, clinical process reengineering, cybersecurity assessments, and employee training, which elevates overall implementation expenses. Consequently, smaller hospitals and facilities with restricted IT resources might postpone adoption or only implement alarm management in specific departments. This complexity may hinder market penetration despite a strong demand for reducing alarm fatigue.

- For instance, in June 2024, a qualitative ICU alarm management study published in the National Center for Biotechnology Information (NCBI) highlighted that alarm-management improvement is difficult due to the fact that ICU environments are complex sociotechnical systems.

MARKET OPPORTUNITIES

Expansion of Remote Monitoring and Clinical Surveillance to Generate New Growth Prospects

The growth of remote monitoring and clinical oversight is establishing a significant opportunity for the clinical alarm management sector. Hospitals are progressively moving away from bedside-only monitoring to centralized monitoring units, virtual care centers, and comprehensive surveillance systems. This generates a need for platforms capable of gathering alerts from connected devices, assessing real-time patient information, prioritizing notifications, and escalating urgent alarms to the appropriate care team. The potential is particularly substantial in telemetry, ICU, step-down units, and virtual nursing programs, as hospitals need to oversee more patients while having fewer staff.

With healthcare systems grappling with workforce shortages and increased patient acuity, remote monitoring can enhance response times, minimize unnecessary bedside distractions, and promote safer patient care. This is anticipated to boost the uptake of clinical monitoring systems, alarm analysis tools, middleware for medical device integration, and cloud/hybrid alarm management solutions. All these factors are expected to drive the market growth in the coming years.

- For instance, in October 2025, West Tennessee Healthcare launched a Centralized Monitoring Unit and eICU powered by Philips to strengthen patient safety, improve response times, and support clinical teams across the health system.

MARKET CHALLENGES

High Upfront Cost and Unclear ROI for Smaller Facilities Pose a Prominent Challenge to Market Growth

Significant initial expenses and ambiguous return on investment continue to be major hurdles for the market, particularly for smaller hospitals, ASCs, long-term care facilities, and post-acute care providers. These facilities might require investment not just in alarm management software, but also in device integration, interface creation, mobile communication tools, training for staff, cybersecurity measures, and continuous support. In contrast to large health systems, smaller facilities may lack sufficient monitored beds or organization-wide use cases to warrant a significant implementation budget promptly. Measuring the financial return is challenging as advantages such as a decrease in missed alarms, enhanced response times, lower nurse workload, and improved patient safety are often indirect. Consequently, purchasers might postpone adoption, initiate with restricted departmental implementations, or select more affordable basic alerting solutions rather than comprehensive alarm management systems. This obstacle can hinder market penetration despite a significant clinical demand for reducing alarm fatigue. All the factors cumulatively affect the market growth.

- For instance, in June 2024, a qualitative ICU alarm management study published in the National Center for Biotechnology Information (NCBI) stated that effective alarm management requires more than technology alone; it depends on workflow redesign, staff interaction with monitoring systems, and sustainable implementation practices.

Segmentation Analysis

By Component

Software/Platforms Segment Dominated Due to Need for Real-time Alarm Routing and Integrated Clinical Workflows

In terms of component, the market is divided into software/platforms, and services.

The software/platforms segment led the global clinical alarm management market share in 2025. Hospitals are increasingly dependent on these platforms to minimize alarm fatigue, deliver actionable alerts to the appropriate caregiver, and enable quicker responses throughout ICUs, emergency departments, operating rooms, telemetry units, and general wards. The prevalence of this segment is further reinforced by the increasing utilization of clinical communication platforms, medical device integration middleware, alarm analytics dashboards, and clinical surveillance systems. As a result, ongoing software licenses, platform subscriptions, and organization-wide alarm management modules maintain the software/platforms segment's lead in terms of market value.

- For instance, in May 2025, AirStrip introduced AirStrip Alarm Management, an FDA-approved integrated platform designed to transform clinical alarm management of vital signs.

The services segment is anticipated to rise with a CAGR of 9.69% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Strong Need for Local Device Connectivity and Real-time Alarm Reliability Allowed On-premise Segment to Dominate

Based on deployment, the market is classified into cloud-based, on-premise, and hybrid.

The on-premise segment accounted for the dominant market share in 2025, driven by the high reliability, low latency, and uninterrupted access within ICUs, emergency departments, operating rooms, and telemetry units of these solutions. Additionally, on-premise systems also allow hospitals to maintain greater control over patient data, device interfaces, cybersecurity settings, and clinical workflow configuration. Furthermore, the segment is set to hold 40.7% share in 2026.

- For instance, in July 2025, Connexall announced that it became available in Epic Toolbox as an Alert Manager Integration solution.

The cloud-based segment is anticipated to rise with a CAGR of 15.31% over the forecast period.

By Alarm Source

High Alarm Volume from Bedside and Multiparameter Monitors Boosted Patient Monitoring Systems Segment Growth

On the basis of alarm source, the market is divided into patient monitoring systems, ventilators, infusion pumps, nurse call systems, telemetry systems, and others.

In 2025, the market share was primarily led by the patient monitoring systems segment. This is due to bedside monitors, multiparameter monitors, central monitoring stations, and vital-sign monitors being used across high-acuity and general care settings. The dominance of this segment is further supported by the growing use of continuous monitoring and connected patient monitoring platforms that require alarm routing, escalation, and analytics. Furthermore, the segment is set to hold 32.8% share in 2026.

- For instance, in February 2024, Philips announced the global availability of Philips Sounds, following FDA 510(k) clearance of its latest IntelliVue patient monitor software.

The telemetry systems segment is anticipated to rise with a CAGR of 13.19% over the forecast period.

By End User

Hospitals & ASCs Led Demand Due to High Alarm Burden Across Acute-care Settings

Based on end user, the market is segmented into hospitals & ASCs, long-term care & post-acute care facilities, and others.

The hospitals & ASCs segment dominated the market share in 2025. The dominance of the segment is attributed to the fact that these facilities manage the highest concentration of alarm-generating devices, including patient monitors, ventilators, infusion pumps, telemetry systems, nurse call systems, anesthesia machines, and recovery-room monitoring equipment. The dominance of this segment is further supported by larger IT budgets, stronger medical device integration needs, and enterprise-wide clinical communication programs in hospitals and health systems. Furthermore, the segment is set to hold 82.4% share in 2026.

- For instance, in October 2025, West Tennessee Healthcare launched a new Centralized Monitoring Unit and eICU powered by Philips iCareManager. The system was implemented to support real-time patient monitoring across the health system, improve response times, and strengthen patient safety.

Long-term care & post-acute care facilities are projected to grow at a 16.91% CAGR during the forecast period.

Clinical Alarm Management Market Regional Outlook

Based on region, the global market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Clinical Alarm Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 0.98 billion in 2024 to dominate the clinical alarm management industry. In 2025, the region maintained its dominance, with a market valuation of USD 1.07 billion. North America is expanding due to high adoption of clinical communication platforms, strong hospital IT infrastructure, and greater focus on patient safety. The region has a large base of acute-care hospitals using patient monitors, telemetry systems, nurse call systems, and connected medical devices, which creates strong demand for alarm routing and analytics.

U.S. Clinical Alarm Management Market

The U.S. market led the North American region and is projected to be approximately USD 1.04 billion in 2026, representing about 33.7% of global revenues.

Europe

The market in Europe is set to grow at a CAGR of 10.11% during the forecast period. Europe’s growth is supported by increasing hospital digitalization, stronger interoperability programs, and the adoption of connected clinical workflows across Western European healthcare systems.

U.K. Clinical Alarm Management Market

The U.K. market in 2026 is estimated at around USD 0.16 billion, representing roughly 5.2% of global revenues.

Germany Clinical Alarm Management Market

The German market size is projected to reach approximately USD 0.19 billion in 2026, equivalent to around 6.0% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach a valuation of USD 0.74 billion in 2026. Asia Pacific is expected to show the fastest growth due to hospital expansion, rising smart hospital investments, and growing adoption of connected monitoring in Asian countries. Additionally, the region has a large patient base and expanding private hospital chains, creating opportunities for new clinical communication, device integration, and surveillance deployments.

Japan Clinical Alarm Management Market

The Japanese market in 2026 is estimated at around USD 0.18 billion, accounting for roughly 5.7% of global revenues.

China Clinical Alarm Management Market

China’s market is projected to reach USD 0.24 billion in 2026, representing roughly 7.6% of global sales.

India Clinical Alarm Management Market

The Indian market in 2026 is estimated at around USD 0.08 billion, accounting for roughly 2.5% of global revenues.

Latin America and Middle East & Africa

The growth in the Latin America and Middle East & Africa regions is anticipated to be moderate in the coming years. The growth is driven mainly by private hospitals and large urban health systems in countries. Additionally, New hospital projects, smart hospital programs, digital health initiatives, and command-center models are increasing demand for connected alarm workflows, remote monitoring, and clinical surveillance. The Latin America market in 2026 is estimated at around USD 0.20 billion.

GCC Clinical Alarm Management Market

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.08 billion in 2026, representing about 2.6% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated Alarm Platforms and Clinical Communication Capabilities to Support Players’ Market Positions

The global clinical alarm management market reflects a moderately fragmented competitive landscape, consisting of major companies such as Stryker, GlobeStar Systems, Inc., Ascom, Koninklijke Philips N.V., and Baxter, representing a significant portion of market revenue. The considerable market presence of these companies is owing to their broad portfolios, focus on integrated solutions, which is anticipated to strengthen their competitive position across the forecast period.

- For instance, in August 2025, Ascom and AvaSure signed an agreement to integrate AvaSure’s virtual care platform with Ascom’s Myco devices and Healthcare Platform. The integration was made available to shared hospital customers and can be incorporated into broader alarm management initiatives by connecting virtual care, monitoring, communication, and clinical workflows.

Other significant participants include TigerConnect, Masimo, Spok, and GE Healthcare, among others. These firms are also emphasizing mobile-first clinical communication, cloud/hybrid deployments, alarm analytics, centralized monitoring, technological advancements, and device interoperability to reduce alarm fatigue, improve response times, and expand enterprise-wide adoption.

LIST OF KEY CLINICAL ALARM MANAGEMENT COMPANIES PROFILED

- Stryker (U.S.)

- GlobeStar Systems, Inc. (Canada)

- Ascom (Switzerland)

- Koninklijke Philips N.V. (The Netherlands)

- Bax ter (U.S.)

- TigerConnect (U.S.)

- Masimo (U.S.)

- Spok (U.S.)

- General Electric Company (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Stryker launched its SmartHospital Platform, designed to connect devices, data, and care teams across hospitals. The platform includes clinical communication, prioritized alarms, workflow engine capabilities, virtual care, and ambient intelligence.

- December 2025: TigerConnect Alarm Management received the Epic Toolbox designation within the Alert Manager category. The solution delivers context-rich alerts into Epic applications such as Rover, Haiku, Canto, and Hyperspace.

- January 2025: CalmWave and Oracle collaborated to address hospital alarm fatigue using Oracle Cloud Infrastructure. CalmWave stated that non-actionable alarms make up 80–99% of ICU alarms and that OCI can help scale its AI workloads for hospitals globally.

- November 2024: GE HealthCare published pilot data with the Cleveland Clinic for Portrait Mobile, showing that clinicians found 82% of alarms informative or useful, with less than three alarms per patient per day.

- October 2024: CalmWave advanced a pilot after a proof-of-concept at Wellstar showed potential for a 58% reduction in non-actionable alarms using its Operations Platform. Catalyst by Wellstar also made a strategic investment in the company.

REPORT COVERAGE

The global clinical alarm management market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of key factors, including technological progress, product innovations, the regulatory environment, and new product launches. Additionally, it details partnerships, mergers & acquisitions, and key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.07% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Alarm Source, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Alarm Source |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.81 billion in 2025 and is projected to reach USD 7.17 billion by 2034.

In 2025, the market value in North America stood at USD 1.07 billion.

The market is expected to exhibit a CAGR of 11.07% during the forecast period of 2026-2034.

By component, the software/platforms segment led the market in 2025.

Rising alarm fatigue across hospitals and growing focus on patient safety and regulatory compliance are primarily driving market expansion.

Stryker, GlobeStar Systems, Inc., Ascom, Koninklijke Philips N.V., and Baxter are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us