Clinical Trial Supplies Market Size, Share & Industry Analysis By Type (Products [Investigational Medicinal Products, Comparator Drugs, Ancillary Supplies, and Others] and Services [Manufacturing Services, Packaging, Labeling & Blinding Services, Storage & Distribution Services]), By Phase (Phase I, Phase II, Phase III, and Phase IV), By Modality (Small Molecules, Biologics, Medical Devices), By Therapeutic Area (Oncology, Infectious Diseases, Neurology, Cardiology), By End User (Pharmaceutical & Biotechnological Companies, Medical Device Companies, CROs), & Regional Forecast, 2026-2034

Clinical Trial Supplies Market Overview

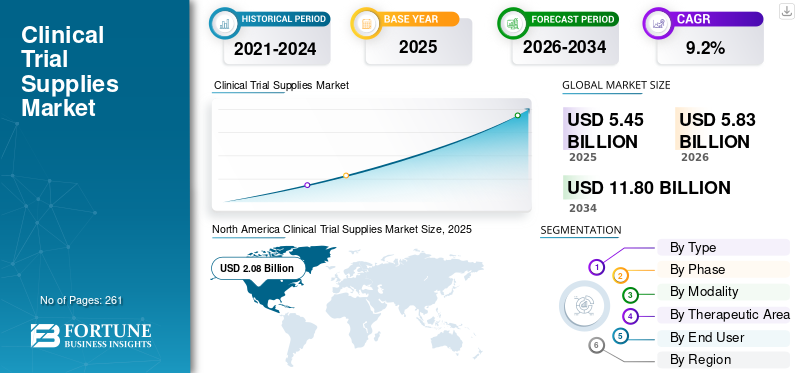

The global clinical trial supplies market size was valued at USD 5.45 billion in 2025 and is projected to grow from USD 5.83 billion in 2026 to USD 11.80 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period. North America dominated the clinical trial supplies market with a market share of 38.16% in 2025.

Clinical trial supplies refer to materials or devices required to conduct medical research across various modalities including biologics, medical devices and others. These supplies encompass the end-to-end management including packaging, labeling, storing, and distribution to ensure patient safety and trial accuracy. The growing number of clinical trials, growing R&D investment among pharmaceutical and biotechnological companies, and the expansion of hybrid clinical trials are resulting in a rising adoption rate of these products and services in the market. The growth of biologics, biosimilars, and cell gene therapies and others is further boosting the adoption of clinical trial supplies in the market.

- For instance, according to 2025 statistics published by the World Health Organization (WHO), about 162,704 clinical trials were conducted in China.

Furthermore, the companies putting a growing emphasis toward offering innovative services, including Thermo Fisher Scientific Inc., and Parexel International (MA) Corporation, among others, are further contributing to the demand for these products and services in the market.

Download Free sample to learn more about this report.

Clinical Trial Supplies Market Trends

Adoption of Digital and Automation Technologies to Drive the Demand

The growing digitalization of tools among contract research organizations, supply-chain partners, and manufacturers are shifting toward integrated digital solutions. Incorporation of technologies including electronic data capture, RTSM/IRT systems, eCOA/ePRO, real-time temperature monitoring, cloud-based clinical supply dashboards, digital inventory management, and others is enhancing trial visibility and automating resupply decisions. Additionally, these technologies help minimize drug wastage and effectively manage complex global clinical trials.

Moreover, digital solutions enable sponsors to track inventory across trial sites, monitor shipment conditions, analyze demand based on patient enrollments, and minimize the risk of overproduction. The incorporation of digital tools also helps in patient-centric supply models, including home delivery, remote dispensing, digital accountability, and real-time shipment tracking, and others.

- According to a 2024 survey published by Medrio, it was reported that 98% of studies used multiple clinical trial technologies in over half of the studies deployed by among 150 respondents.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Increasing Number of Clinical Trials to Boost Market Growth

The growing number of clinical trials among pharmaceutical, biotechnology, and medical device companies to boost drug and devices manufacturing for various therapeutic areas. It is further increasing the demand of clinical trial supply products and services including reliable supply planning, packaging, labeling, temperature monitoring, among others across various regions.

- For instance, according to 2026 data published by the National Center for Biotechnology Information (NCBI), it was reported that about 583,905 clinical trial studies were registered globally.

This, along with, rising healthcare investments and expansion of decentralized trials is rising demand for biologics and personalized medicine. However, it is also increasingly outsourcing supply chain management, packaging, labeling, and logistics services, boosting the adoption rate of these products and services in the market. Therefore, the factors above, along with the rising number of key companies offering novel services to fuel the development of drugs and devices, further expected to contribute to the global market size.

Market Restraints

High Cost Associated with Clinical Trial Supply Management to Hamper the Market Growth

The increasing complexity of clinical trials and focus toward personalized medicine is resulting in rising demand for specialized clinical trial supply services. This includes investigational product manufacturing, packaging, comparator sourcing, labeling, storage, import/export documentation, temperature controlled logistics, depot management, site-level inventory tracking, returns, reconciliation, and others. These factors are further raising the cost of these services in the market.

Furthermore, supply forecasting remains challenging as clinical trials often face uncertain patient recruitments, protocol amendments, patient dropouts, site activation delays, cohort expansions, and country-specific regulatory frameworks. The clinical trial sponsors may overproduce or oversupply investigational products to avoid stockouts, which increases inventory holding costs and also contributes to drug wastage, thereby hindering the market growth.

- For instance, according to the 2025 statistics published by the Sensos, it was reported that the pharmaceutical sector loses approximately USD 20.0 billion to USD 35.0 billion in spoiled or wasted products caused by temperature deviations.

Market Opportunities

Expansion of Clinical Trials in Emerging Countries to Create Market Opportunities

The expansion of laboratory networks in developing countries presents a major opportunity in the global market. The clinical trial sponsors are expanding studies beyond conventional trial hubs. Along with this, large patient populations, improving clinical research infrastructure, lower operational costs, increasing patient recruitment potential, and rising development of regulatory compliance across emerging countries, including Brazil and Mexico, is boosting the adoption for these supplies in the market. Furthermore, growing healthcare expenditure, among others, is resulting in growing demand for clinical trial supply products and services in the market.

- According to the 2025 data published by the International Trade Administration (ITA), the healthcare expenditure is about USD 135.0 billion in Brazil.

Market Challenges

Limited Clinical Trials in Developing Countries to Limit the Market Growth

There is an increasing demand for novel clinical trial supplies among the patient population. However, limited healthcare access in developing nations remains a major challenge in the global market. The lack of developed clinical trials infrastructure and logistics networks, trained specialists, and supply chain disruptions is resulting in reduced conduction of clinical trials among the companies and sponsors. Other such restraints include challenges in compliance and limited number of sponsors and contract research organizations, thereby hampering the market growth.

- For instance, according to 2025 data published by the World Health Organization (WHO), only 317 clinical trials were conducted in Qatar.

SEGMENTATION ANALYSIS

By Type

Increasing Demand Among Participants for DTP Services Led to Segment Dominance

Based on the type, the market is bifurcated into products and services. Products are further classified into investigational medicinal products, comparator drugs, ancillary supplies and others. Services are further classified into manufacturing services, packaging, labeling, & blinding services, storage & distribution services and others.

The services segment held the largest revenue share in 2025. The growth is owing to the increasing adoption for outsourcing services resulting in rising demand of services including clinical supply planning, blinding, storage, cold-chain distribution, comparator sourcing, depot management, import/export support, Direct-To-Patient (DTP) delivery, and others. Additionally, growing number of companies and contract research organizations providing innovative services, is further expected to contribute to the global clinical trial supplies market growth.

- According to a 2024 survey published by DIA, about 93% of clinical trial participants, who had received DTP deliveries, found that these shipments made their clinical trial experience more convenient across demographic factors and study parameters.

The products segment is expected to grow at a CAGR of 9.0% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Phase

Growing Number of Phase III Clinical Trials Led to Dominance of the Segment

Amongst phase, the market is segmented into phase I, phase II, phase III, and phase IV.

The phase III segment dominated the global market in 2025, holding a share of 51.4%. The growth is due to the increasing number of phase III clinical trials, resulting in an increasing demand for clinical trial-based supplies including inventory management, and others, thereby contributing to the segmental growth.

- According to the 2025 statistics published by the World Health Organization (WHO), about 17,360 phase III clinical trials were conducted in India.

The segment of phase II is set to flourish with a growth rate of 10.0% across the forecast period.

By Modality

Growing Approval of Small Molecules Led to Dominance of the Segment

Based on modality, the market is classified into small molecules, biologics, medical devices, and others.

The small molecules segment dominated the global market in 2025, holding a share of 44.1%. The growth is mainly due to the growing prevalence of chronic diseases and advantages of small molecule therapies including easy manufacturing, formulation, packaging, labeling, and others. Further, resulting in rising approval of small molecule therapies, thereby contributing to the segmental growth in the market.

- According to the 2024 data published by the Cambridge Crystallographic Data Centre (CCDC), the Food and Drug Administration (FDA) approved 34 new small molecule drugs in 2023 as compared to 21 in 2022.

The segment of medical devices is set to flourish with a growth rate of 9.9% across the forecast period.

By Therapeutic Area

Increasing Prevalence of Various Types of Cancer Led to Oncology Segment Dominance

Amongst therapeutic area, the market is divided into oncology, infectious diseases, neurology, cardiology, and others.

The oncology segment dominated the market in 2025. The growing prevalence of various types of cancer, including lung cancer, the rising demand for clinical trial supplies, and the growing number of CROs, are some of the crucial factors contributing to the segment’s growth. Furthermore, the segment is set to hold a 40.9% share in 2026.

- According to the 2026 data published by American Cancer Society (ACS), it was reported that about 229,410 new cases of lung cancer were estimated to occur in the U.S.

In addition, the cardiology segment is projected to grow at a CAGR of 8.1% during the forecast period.

By End User

Growing Number of Pharmaceutical & Biotechnological Companies Led to Segmental Dominance

Based on end user, the market is divided into pharmaceutical & biotechnological companies, medical device companies, CROs, and others.

The pharmaceutical & biotechnological companies dominated the market in 2025. The increasing number of clinical trials, growing adoption for clinical trial supplies, and rising number of pharmaceuticals and biotechnology companies, among others, are some of the crucial factors contributing to the segment’s growth. Furthermore, the segment is set to hold a 59.0% share in 2026.

- According to 2026 statistics published by Cross River Therapy, there are about 5,000 pharmaceutical companies in the U.S.

In addition, medical device companies are projected to grow at a 10.0% CAGR during the forecast period.

Clinical Trial Supplies Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Clinical Trial Supplies Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market held the dominant share in 2024, valued at USD 1.92 billion, and also continued to maintain its leading position in 2025 with USD 2.08 billion. Some of the key factors contributing to the growth of this region in the market are the increasing number of clinical trials and growing number of pharmaceutical and biotechnological companies. Additional factors include rising adoption of clinical trial supply products and services, among others.

- For instance, according to 2025 statistics published by the World Health Organization (WHO), about 22,683 phase III clinical trials were conducted in the U.S.

U.S. Clinical Trial Supplies Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.99 billion in 2026, accounting for roughly 34.1% of global sales.

Europe

Europe is projected to record a growth rate of 8.4% in the coming years, which is the second-highest among all regions, and reach a valuation of USD 1.79 billion by 2026. The increasing number of clinical trials is expected to support the market growth.

U.K. Clinical Trial Supplies Market

The U.K. market in 2026 is estimated at around USD 0.36 billion, representing roughly 6.2% of global revenues.

Germany Clinical Trial Supplies Market

Germany’s market is projected to reach approximately USD 0.35 billion in 2026, equivalent to around 5.9% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 1.30 billion in 2026 and secure the position of the third-largest region in the market. The increasing healthcare expenditure and growing demand for clinical trial supplies are anticipated to support the growth of the market.

Japan Clinical Trial Supplies Market

The Japan market in 2026 is estimated at around USD 0.32 billion, accounting for roughly 5.5% of global revenues. Japan is expected to grow due to the growing focus of key companies toward the provision of novel services in the market.

China Clinical Trial Supplies Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.48 billion, representing roughly 8.2% of global sales.

India Clinical Trial Supplies Market

The Indian market size in 2026 is estimated at around USD 0.10 billion, accounting for roughly 1.8% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.29 billion in 2026. The growth is due to the growing healthcare investment in the region. The Middle East & Africa region is also expected to grow due to the increasing number of key companies strengthening their brand presence in the market. In the Middle East & Africa, the GCC is set to reach a value of USD 0.11 billion in 2026.

South Africa Clinical Trial Supplies Market

The South Africa market is projected to reach around USD 0.07 billion in 2026, representing roughly 1.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Number of Acquisitions Among Other Companies to Support Dominance of Key Players

A strong products and services portfolio, along with a significant emphasis on inorganic growth strategies globally, is one of the key factors contributing to the dominance of these companies in the market. Thermo Fisher Scientific Inc. and Parexel International (MA) Corporation are reported as the major companies in the market in 2025. Furthermore, the growing focus of major companies on acquisitions and mergers among the other companies are anticipated to strengthen their presence, further contributing to the global clinical trial supplies market share.

- For instance, in October 2025, Thermo Fisher Scientific Inc., acquired Clario Holdings, Inc., a provider of endpoint data solutions for clinical trials, to accelerate innovation with deeper clinical insights.

Other key players, including Catalent Inc., and others, are also growing in the market, primarily due to their increasing focus toward expansion of their service channels in order to strengthen market presence.

List of Key Clinical Trial Supplies Companies Profiled

- Thermo Fisher Scientific Inc. (U.S.)

- Parexel International (MA) Corporation (U.S.)

- Catalent Inc. (U.S.)

- Almac Group (U.K.)

- PCI Pharma Services (U.S.)

- Clinigen Limited (U.K.)

- Myonex (U.S.)

- Biocair (U.K.)

- Oximio (U.K.)

- KLIFO (Denmark)

KEY INDUSTRY DEVELOPMENTS

- April 2026: PCI Pharma Services, a company integrated global Contract Development and Manufacturing Organization (CDMO) focused on innovative biologic and small molecule therapies, expanded its sterile fill-finish advanced drug delivery capabilities in the U.S.

- April 2026: Suvoda, a global clinical trial technology company in the Randomization and Trial Supply Management (RTSM) space, launched agentic RTSM: the next evolution of Suvoda IRT. The newly launched RTSM uses agentic AI to take a study from project kickoff to User Acceptance Testing (UAT) in as little as two weeks.

- March 2026: Suvoda, a global company in clinical trial technology, got its recognition as the Most Innovative Clinical Trial Technology Firm of 2026 in the Global Excellence Awards presented by Global Health & Pharma magazine.

- September 2025: Clinigen, the global pathfinder accelerating patient access to critical medicines across the lifecycle, acquired SSI Strategy. It is a trusted strategic company with an aim to create a comprehensive global partner for the biopharma industry from early-stage strategy to commercialization.

- August 2025: Biocair, an established global company in life science logistics, expanded its operations in the Asia Pacific region with the opening of a new office in Shanghai, China.

- June 2025: Myonex, a global company in integrating clinical trial and commercial pharmaceutical services, announced that The Leukemia & Lymphoma Society (LLS) has selected Myonex as its preferred partner. The announcement was made in order to support patients participating in the LLS-sponsored Beat AML Master Clinical Trial through its CTRx solution.

- December 2024: KLIFO launched a new state-of-the-art clinical trial supply facility in the Copenhagen area. This helped the company to strengthen its brand presence.

REPORT COVERAGE

The report provides a detailed global clinical trial supplies market analysis and focuses on key aspects such as leading companies and market segmentation, including type, phase, modality, therapeutic area and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Phase, Modality, Therapeutic Area, End User, and Region |

| By Type |

|

| By Phase |

|

| By Modality |

|

| By Therapeutic Area |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 5.45 billion in 2025 and is projected to reach USD 11.80 billion by 2034.

In 2025, the market value stood at USD 2.08 billion.

Growing at a CAGR of 9.2%, the market will exhibit steady growth over the forecast period.

By type, the services segment is the leading segment in this market.

The introduction of novel clinical trial supply services is one of the major factors driving the market's growth.

Thermo Fisher Scientific Inc. and Parexel International (MA) Corporation are the major players in the global market.

North America dominated the market share in 2025.

The growing number of clinical trials, rising demand of clinical trial supplies, growing outsourcing of laboratory services, among others, are some of the key factors expected to boost the adoption of these services globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us