Collagen Supplements Market Size, Share & Industry Analysis, By Source (Bovine, Marine, Porcine, Poultry, and Others), By Function (Skin Health, Joint & Bone Health, Hair & Nail Health, Sports Nutrition, General Wellness, Gut Health, and Others), By Form (Powder, Capsules/Tablets, Liquid, Gummies, Softgels, and Others), By Collagen Type (Type I, Type II, Type III, Type IV & V, and Multi-collagen Blends), By Distribution Channel (Supermarkets/Hypermarkets, Pharmacies & Drug Stores, Specialty Stores, Online Retail, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

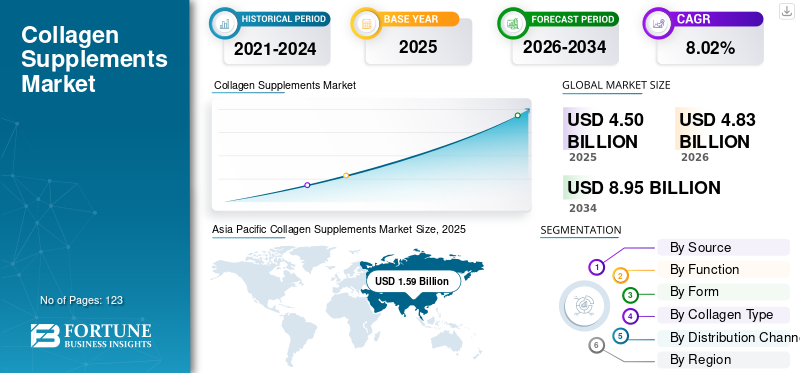

Collagen Supplements Market Size and Future Outlook

The global collagen supplements market size was valued at USD 4.50 billion in 2025. The market is projected to grow from USD 4.83 billion in 2026 to USD 8.95 billion by 2034, exhibiting a CAGR of 8.02% during the forecast period.

Collagen supplements are dietary products that provide collagen peptides to support human protein needs. These supplements are mainly positioned for joint comfort, healthy aging, hydration, and skin elasticity. The key raw materials used in collagen production include porcine skin, eggshell membrane, fish scales and skin, and bovine hides. Some of the popular supplements include collagen tablets, marine collagen powder, and ready-to-drink collagen shots. Regarding end users, this product caters to active-lifestyle users, beauty-conscious individuals, and aging adults. The growing dependency on preventive wellness supplements and new product innovation are key drivers in the global industry.

Companies such as Nestle S.A., GNC Holdings, LLC, and Shiseido Company, Limited are prominent players in the market. New product launches are a pivotal strategy adopted by key players to improve their position.

Download Free sample to learn more about this report.

COLLAGEN SUPPLEMENTS MARKET TRENDS

Rising Demand for Beauty-from-within Products to Drive Industry Growth

The rising demand for beauty-from-within products is one of the strongest trends influencing the market. Consumers are increasingly shifting from topical skincare alone to ingestible beauty products that support skin hydration, elasticity, firmness, and wrinkle reduction from within. This trend is particularly strong among women, aging consumers, urban professionals, and younger wellness-focused consumers who prefer preventive skincare solutions rather than corrective cosmetic products alone. Collagen peptides are widely used in nutraceutical and cosmetic products as they are associated with skin structure, dermal hydration, and anti-aging benefits. A growing number of clinical reviews and randomized controlled trials have examined oral collagen supplementation for skin hydration and elasticity, helping strengthen consumer confidence in collagen-based beauty supplements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Aging Population Augments the Consumption of Collagen Supplements

The rising global aging population is a major driver of the collagen supplements market growth, as collagen is closely associated with skin elasticity, bone strength, cartilage support, and joint mobility. As individuals age, the body’s natural collagen synthesis gradually declines, which contributes to visible signs of skin aging such as wrinkles, dryness, and reduced firmness, along with a higher risk of joint discomfort and reduced mobility. This has encouraged consumers, especially middle-aged and older adults, to adopt collagen peptides, hydrolyzed collagen powders, and functional beverages as preventive wellness products. Furthermore, growing awareness of osteoarthritis, musculoskeletal weakness, and skin aging among elderly consumers is encouraging supplement manufacturers to develop targeted collagen formulations with vitamin C, calcium, hyaluronic acid, and other supportive ingredients.

MARKET RESTRAINTS

Regulatory Restrictions in the Supplements Sector Impede Growth

Regulatory restrictions are one of the key restraints that limit the way collagen brands can communicate product benefits. In the U.S., dietary supplements are not approved by the FDA for safety and effectiveness before marketing, which places responsibility on manufacturers to ensure product safety, label accuracy, and compliant claims. In the European Union, health claims must be authorized and listed in the EU Register of Nutrition and Health Claims. This restricts aggressive claims related to skin rejuvenation, joint repair, or disease-related benefits unless supported by approved claim language. In the European Union, the challenge is even greater, as collagen brands can use health claims only if authorized under the EU Nutrition and Health Claims Regulation. As a result, the above-mentioned factors can hamper the global collagen supplements market share.

MARKET OPPORTUNITIES

Functional Food and Beverage Integration Creates Growth Opportunities

Functional food and beverage integration presents a major growth opportunity for the market. Collagen is no longer limited to capsules and powders; it is increasingly incorporated into coffee creamers, protein bars, juices, RTD beverages, dairy alternatives, bakery products, and meal replacement products. This allows brands to reach consumers who prefer to obtain nutrition through regular food and beverage consumption rather than through conventional pills. The opportunity is supported by the growing consumer focus on protein intake. The International Food Information Council’s 2025 Food & Health Survey reported that 70% of the U.S. consumers were trying to consume more protein in 2025, an increase from 67% in 2023. Manufacturers can capture this opportunity by developing collagen-enriched beverages, protein snacks, low-sugar gummies, fortified coffee products, and functional hydration drinks.

Segmentation Analysis

By Source

Bovine Category Dominated the Market Due to Cost-Effectiveness

Based on the source, the market is segmented into bovine, marine, porcine, poultry, and others.

Bovine segment led the global market in 2025, as it is widely available, cost-effective, and can be used across many product types. Most bovine collagen is derived from cattle hides, bones, and connective tissues, which are readily available through existing meat-processing supply chains. This makes bovine gelatin more economical than marine collagen, especially for mass-market powders, capsules, gummies, and functional nutrition blends. Its neutral taste profile after hydrolysis, solubility, and suitability for high-dose collagen peptide formulations further makes it attractive for daily supplement products.

The marine segment is projected to grow at a high CAGR of 8.34% over the forecast period.

By Function

Skin Health Function Led the Market Owing to High Adoption Among Beauty-Conscious Consumers

Depending on the function, the market is distributed into skin health, joint & bone health, hair & nail health, sports nutrition, general wellness, gut health, and others.

In 2025, the skin health segment led the global market share, as it is the most established, consumer-recognized, and commercially scalable use case. Collagen is strongly associated with skin elasticity, firmness, hydration, wrinkle reduction, and overall youthful appearance, making it highly captivating to beauty-conscious consumers. The rise of beauty-from-within products has helped skin health, as more people now choose supplements that work alongside their regular skincare routines.

The joint & bone health segment is projected to grow at a CAGR of 8.10% over the forecast period.

By Form

Powder Segment Led the Industry Due to Portability

Based on form, the market is divided into powder, capsules/tablets, liquid, gummies, softgels, and others.

The powder segment dominated the industry in 2025, accounting for the largest market share, as collagen is typically consumed at gram-level dosages, which are easier and more economical to deliver in powder form than in capsules or tablets. Hydrolyzed collagen peptides are commonly used at higher serving sizes, and powder formats allow brands to provide meaningful doses without requiring consumers to take multiple pills per day.

The gummies segment is projected to grow at a high CAGR of 9.28% over the forecast period.

By Collagen Type

Type I Collagen Segment Dominated the Industry Due to Wide Availability

On the basis of collagen type, the market is segmented into type I, type II, type III, type IV & V, and multi-collagen blends.

The type I collagen segment accounted for the highest market share in 2025, as it is the most abundant collagen type in the human body and is strongly associated with skin, tendons, ligaments, bones, and connective tissues. Type I collagen is available in both bovine and marine sources, making it suitable for both affordable and premium products. Type I collagen is well-suited for powders, capsules, gummies, sachets, and liquids. This lets brands create products for different budgets and customer needs.

The type II segment is projected to grow at a CAGR of 8.06% over the forecast period.

By Distribution Channel

To know how our report can help streamline your business, Speak to Analyst

Online Retail Segment Dominated the Industry Due to Ease of Ordering

Based on distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies & drug stores, specialty stores, online retail, and others.

The online retail segment accounted for the highest market share in 2025, as the category is highly influenced by consumer education, comparison shopping, social media marketing, and direct-to-consumer brand engagement. People can investigate various factors, such as the source, type, dosage, added ingredients, flavor, reviews, certifications, and price per serving, on these platforms. Online retail makes it easier and faster to launch new products, such as powders, gummies, sachets, capsules, and ready-to-drink options.

The specialty stores segment is projected to grow at a CAGR of 8.12% over the forecast period.

Collagen Supplements Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Collagen Supplements Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market and was estimated at USD 1.59 billion in 2025. The growing use of collagen for anti-aging purposes and the expanding dietary supplements sector support market growth.

India Collagen Supplements Market

The Indian market size in 2025 was estimated at around USD 0.05 billion, accounting for roughly 1.10% of the global market revenues.

China Collagen Supplements Market

China's market is projected to be one of the largest worldwide, with revenues estimated at around USD 0.69 billion in 2025, accounting for roughly 15.29% of global sales.

Japan Collagen Supplements Market

The Japan market in 2025 was valued at around USD 0.32 billion, accounting for approximately 7.15% of the global market growth.

North America

North America reached a valuation of USD 1.50 billion in 2025 and secured the second position in the market. The market in the region is expected to grow due to rising beauty consciousness and the large-scale production of clean label collagen products.

U.S. Collagen Supplements Market

Given North America's strong contribution and the U.S. dominance in the region, the U.S. market was valued at around USD 1.38 billion in 2025, accounting for roughly 30.68% of global sales.

Europe

Europe reached USD 1.03 billion in 2025, with a growth rate of 7.37% over the coming years, and ranked third in the market. The adoption of advanced technologies and the growing inclination toward type II collagen for joint health are boosting the region’s growth potential.

Germany Collagen Supplements Market

The German market size in 2025 is estimated at around USD 0.16 billion, representing roughly 3.54% of the global market revenues.

U.K. Collagen Supplements Market

The U.K. market value reached approximately USD 0.13 billion in 2025, equivalent to around 2.87% of the global market sales.

South America and the Middle East & Africa

South America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market reached a valuation of USD 0.24 billion in 2025. The growing number of local supplement producers and the launch of plant based collagen blends are expected to drive demand. The Middle East & Africa market reached USD 0.14 billion in 2025.

South Africa Collagen Supplements Market

The South African market is projected to reach around USD 0.02 billion in 2025, representing roughly 0.45% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Development Helps Brands to Enhance Market Penetration

The collagen supplements industry is moderately competitive, with supplement retailers and multinational beauty nutrition firms, such as Nestle S.A. and Shiseido Company, Limited, competing on strong distribution networks and formats. All these players in the market are mainly focusing on new product launches across packaging, flavors, or formats. Moreover, the enterprises are seeking ways to expand their bases through partnerships and collaborations, further boosting growth opportunities.

LIST OF KEY COLLAGEN SUPPLEMENTS COMPANIES PROFILED

- Codeage LLC (U.S.)

- Shiseido Company, Limited (Japan)

- Meiji Holdings Co., Ltd. (Japan)

- GNC Holdings, LLC (U.S.)

- Kirin Holdings Company, Limited (FANCL Corporation) (Japan)

- Piping Rock Health Products, Inc. (U.S.)

- Nestle S.A. (Switzerland)

- Rejuvenated Ltd. (U.K.)

- Sports Research Corporation (U.S.)

- Amway (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Meiji Holdings Co., Ltd., a health and wellness group in Japan, expanded its Amino Collagen brand by launching Amino Collagen NMN across Japan.

- August 2025: Vital Proteins, a brand of Nestle S.A., a Swiss food and beverages manufacturing company, collaborated with the 2025 U.S. Open Mixed Doubles Championship and emerged as the first-ever official collagen partner of the U.S. Open.

- August 2025: Sports Research Corporation, a U.S.-based nutrition and wellness company, released two new products at Sam’s Club, a U.S.-based retailer in Arizona. The supplements launched include organic collagen peptides and magtein (magnesium L–threonate), which support healthy hair, skin, and cognitive function.

- January 2025: GNC Holdings, LLC, an American-origin wellness and health manufacturer, released a beauty supplement line, “Premier Collagen,” across the U.S. market.

- August 2024: Vital Proteins, a subsidiary of Nestle S.A., a food conglomerate in Switzerland, released a new paper-based canister for its collagen peptides.

REPORT COVERAGE

The global market provides an in-depth study of the market size & forecast by all the market segments included in the market reports. The global market forecast analysis includes details on the market dynamics and global market trends expected to drive the market during the forecast period. The global collagen supplements market analysis offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The industry forecast also encompasses a detailed competitive landscape with information on the market segmentation, market share, and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.02% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Source, Function, Form, Collagen Type, Distribution Channel, and Region |

| By Source |

|

| By Function |

|

| By Form |

|

| By Collagen Type |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.50 billion in 2025 and is projected to reach USD 8.95 billion by 2034.

In 2025, the market value stood at USD 1.59 billion.

The market is expected to exhibit a CAGR of 8.02% during the forecast period.

By source, the bovine segment led the global market in 2025.

Increasing aging population augments the consumption of collagen supplements.

Nestle S.A., GNC Holdings, LLC, and Shiseido Company, Limited are among the key players in the market.

Asia Pacific held the largest market share in 2025.

Rising demand for beauty-from-within products to drive the industry growth.

- 2021-2034

- 2025

- 2021-2024

- 123

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us