Commercial Aircraft Bleed Air Systems Aftermarket, Size, Share, and Industry Analysis, By Component (General, Engine Anti-Icing, Cooling, Compressor Control, Indicating, By Offering (MRO Services and Refurbished Parts), By Aircraft Family (A220, A320, A330, A350, A380, ATR 42/72, B737, B747, B767, B777, B787, Bombardier CRJ, COMAC C919, De Havilland Dash 8, Embraer E-Jets, and Sukhoi Superjet 100), and Regional Forecast, 2025-2045

KEY MARKET INSIGHTS

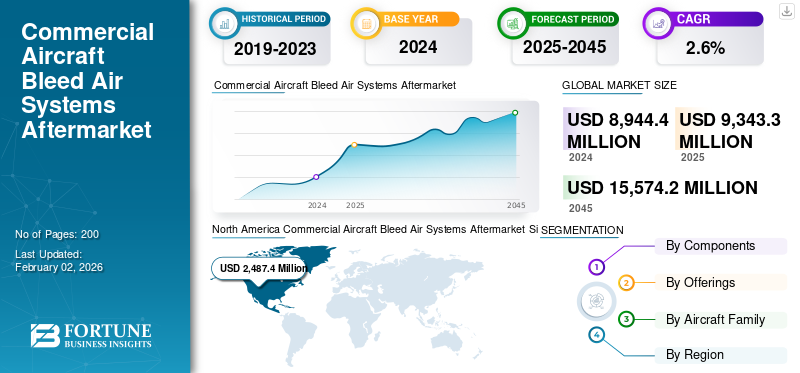

The commercial aircraft bleed air systems aftermarket size was valued at USD 8,944.4 million in 2024. The market is projected to grow from USD 9,343.3 million in 2025 to USD 15,574.2 million by 2045, exhibiting a CAGR of 2.6% during the forecast period. North America dominated the global aircraft bleed air systems aftermarket with a market share of 27.8% in 2024.

Commercial aircraft bleed air systems aftermarket comprises a network of ducts, valves, and regulators that extract high-pressure, high-temperature air from an aircraft engine or auxiliary power unit. Commercial aircraft bleed air systems focus on maintaining, repairing, and overhauling the systems that use compressed air bled from aircraft engines. Meanwhile, the refurbished market includes pre-owned or used aircraft components or parts, such as bleed air duct check valve, engine anti-icing, and others from bleed air systems, that are restored to meet like-new or serviceable standards.

Major players in the commercial aircraft bleed air systems aftermarket include AAR Corp and HAECO Group. These companies are driving market growth through digital technologies initiatives, integrating advanced technologies such as AI, machine learning, and predictive maintenance, which is revolutionizing the MRO process. Increasing demand for in-flight travel, expanding aircraft fleet, and continuous technological developments in non-destructive testing technology, and focus on digital transformation, are further shaping market growth.

Download Free sample to learn more about this report.

Commercial Aircraft Bleed Air Systems Aftermarket Key Takeaways

- 2025 Market Size: USD 8,944.4 million

- 2026 Market Size: USD 9,343.3 million

- 2034 Forecast Market Size: USD 15,574.2 million

- CAGR: 2.6% from 2025–2045

- North America dominated the commercial aircraft bleed air systems aftermarket with a 27.8% share in 2024.

- The cooling segment is expected to hold the largest share during the forecast period.

- The MRO service segment dominated the market, while refurbished parts are projected to grow at the fastest rate.

North America

North America led the market in 2024, supported by a large commercial fleet and strong MRO capabilities.

Europe

Europe remained a mature market, driven by OEM-led MRO networks and steady fleet recovery.

Asia Pacific

Asia Pacific is expected to witness strong growth due to rapid fleet expansion.

U.S

The market is supported by high MRO spending and fleet maintenance demand.

Japan

The market is expected to grow steadily with rising aftermarket demand.

Read More

Market Dynamics

Market Drivers

Increasing Demand for Air Travel and the Rising Need for Aircraft Maintenance Upgrades Boost Market Development

The continuous growth in global air travel and the expansion of connecting new routes are driving higher aircraft utilization rates and accelerating wear and tear of critical aircraft components, including bleed air systems components, aircraft cabin, air conditioning, and cabin pressurization. Resulting need for efficient and cost-effective MRO services and refurbished parts utilization, driving market growth. Additionally, the average age of the existing fleet is resulting in more frequent and extensive maintenance, repair, and overhaul to ensure continued airworthiness and safety of the passengers, which further fuels market growth.

As global air connectivity continues to expand, the commercial aircraft bleed air systems aftermarket is expected to witness significant growth during the forecast period.

Growing Dependency on Optimized Bleed Air Systems to Fuel Market Progress

Airlines and OEMs are under pressure to ensure that the engine- extracted bleed air and cabin-supplied air are safe, clean, and well-controlled. Modern bleed air architectures feed fresh air through advanced filtration and temperature-control packs to balance passenger comfort with fuel burn. Even as electric aircraft concepts gain traction, conventional and hybrid platforms still rely on optimized bleed air systems to manage pressurization, anti-icing, and environmental control, sustaining demand for higher-efficiency valves, ducts, and control units.

Market Restraints

High Cost of Skilled Labor to Hinder Market Growth

Commercial aircraft bleed air systems aftermarket MRO requires highly trained and certified technicians and engineers, and the cost of employing and training these personnel requires high expenses and investment in time to train them, which can hinder the budget and timeline of the MRO service provider. Moreover, bleed air systems involve complex components that are expensive to source and replace, especially for older and less common aircraft models.

Increasing Adoption of Advanced Technologies in Aircraft Design to Obstruct Industry Development

The increasing adoption of advanced technologies in aircraft design is acting as a double-edged sword for bleed air system integrators. While these solutions improve efficiency, reliability, and create new revenue opportunities, they also require significant investment in specialized training, tools, and digital infrastructure to adapt to the increased complexity of modern aircraft and their maintenance requirements. The higher investment associated with training new skilled labor and procurement of new technology and systems puts pressure on the profit margin of MRO service providers, hindering the commercial aircraft bleed air systems aftermarket growth.

Market Opportunities

Digitalization and Automation in Component Health Checking to Offer New Market Opportunities

Digitalization and automation in component health checking and service delivery offer a significant opportunity for both new and established players to gain a competitive edge in the market. By leveraging technologies such as AI, IoT, and data analytics, MRO providers can improve efficiency, reduced cost, and improve safety. Additionally, new players can leverage digital technologies to offer innovative solutions and services, differentiating themselves from traditional MRO providers.

For instance, in September 2024, Asia Digital Engineering (ADE) and Liebherr-Aerospace signed an agreement during the event MRO Asia Pacific 2024. Under this partnership, ADE would help Liebherr-Aerospace with predictive maintenance algorithms and trend-monitoring applications with advanced technical support, for maintenance of the full scope of Liebherr products, including bleed, air management, and flight control components on board Airbus A320 / A321 aircraft.

Commercial Aircraft Bleed Air Systems Aftermarket Trends

Digital & Predictive Maintenance are Shaping the Market Development

Carriers and MROs are adopting aircraft health monitoring and QAR/ACARS-based analytics to identify bleed-air leaks or valve issues early. This approach helps reduce removals and unexpected aircraft on ground (AGOs). For instance, in March 2022, IATA estimated that predictive maintenance could save airlines about USD 3 billion a year in maintenance costs. Moreover, OEM/MRO-led programs, such as APU trend monitoring, are increasing the volume and quality of operational data used for bleed-air health models. Ongoing investment in sensors and forecasting analytics, integrated work scopes, and parts sharing programs is further driving market growth.

For instance, in July 2021, Honeywell introduced Predictive Trend Monitoring and Diagnostic (PTMD) service, which provides real-time APU usage data, status information, and estimates time-to-failure. This capability reduces aircraft downtime while lowering overall maintenance and replacement costs.

Introduction of Stricter Inspection Cycles Propels Industry Progress

Worldwide, regulatory agencies such as the EASA and FAA, along with other national authorities, are introducing stricter inspection cycles and replacement requirements for bleed-air valves, anti-ice systems, and related ducts. These regulations are increasing the need for regular shop visits for both commercial and defense fleets. These requirements, along with safety initiatives driven by ICAO, are raising maintenance intensity globally rather than being limited to specific regions. Moreover, the aviation industry supply chain continues to face pressure from labor shortages, raw material shortages, and longer lead times for OEM parts. These challenges are broadly consistent across North America, Europe, Asia Pacific, and the Middle East.

For instance, in April 2025, EASA issued AD 2025-0096 mandating ongoing airworthiness measures for Airbus A319, A320, and A321 aircraft. This directive highlights increased oversight that impacts various aircraft systems, including bleed-air components.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine Conflict

Bleed air aftermarket activities, including ducts, manifolds, high-temp valves, brackets, and related hardware, are highly dependent on the availability of titanium and the capacity of qualified mills. The Russia-Ukraine conflict has significantly exposed this supply chain vulnerability. In response, Boeing decided to stop buying Russian titanium, while Airbus has reduced its reliance on stockpiles and accelerated its suppliers diversification efforts. Russia’s VSMPO-AVISMA is the largest supplier of aerospace-grade titanium. This material is commonly found in components such as bleed-air ducts, engine structural, and valves. Additionally, about 50% of Airbus's titanium (according to Reuters report), 35% of Boeing's titanium (according to EFESO report), and all of Embraer’s titanium in their aircraft have been sourced from Russia. As sanctions, waivers, and evolving trade rules continue to reshape the market, MROs and operators are required to invest more time and resources in proving material origin and ensuring parts traceability. This is especially important for safety-critical, high-temperature pneumatic components, where metallurgical integrity and process control are crucial to maintaining operational safety.

For instance, in June 2025, Quest Global reported that Boeing had stopped all Russian titanium imports, while Airbus had increased its titanium stockpiles but is still somewhat dependent. As a result of these disruptions, titanium prices have increased by about 90%, greatly increasing the cost of part procurement and maintenance across the aerospace aftermarket.

Sanctions-Induced Spare Parts Shortfalls & Unconventional Sourcing

China blocked supplies to Russia, and Boeing, Airbus, and Bombardier stopped providing Russian carriers with parts and maintenance services. Access to OEM spare parts, including bleed-air valves, has been severely limited due to Western conflict sanctions.

Due to a lack of parts, Russian airlines have cannibalized serviceable aircraft in order to keep active fleets operational. To postpone grounding, some airworthiness certifications have been extended. At the same time, indirect import routes developed via the UAE, Turkey, China, and Aeroflot has reportedly explored maintenance support from Iran to sustain operations amid ongoing supply restrictions.

SEGMENTATION ANALYSIS

By Component

Cooling Systems Segment to Dominate Due to High Installed Base of Engines Featuring ACC Systems

By component, the market is divided into general, engine anti-icing (anti-ice valve, bleed air duct, temperature sensor, nacelle anti-icing control valve, and engine anti-icing shutoff valve), Cooling (HP Turbine Active Clearance Control (HPTACC), LP Turbine Active Clearance Control (LPTACC), turbine clearance control valve, cooling air manifold, and cooling air distributor), compressor control (Variable Stator Vane (VSV) System, Variable Bleed Valve (VBV) System, VSV Actuator, Bellcrank Assembly, Transient Bleed Valve (TBV), 5th Stage Bleed Valve, and Bleed Bias Sensor), indicating (pressure sensor/transmitter, temperature indicator, Position Indicator (LVDT/RVDT), Control Panel/Display Unit, ANTI-ICE ON indicator light, and bleed air pressure gauge).

The cooling segment is anticipated to hold the largest commercial aircraft bleed air systems aftermarket share. This segment includes high- and low-pressure turbine active clearance control (HPTACC/LPTACC) and turbine clearance control valves. As worldwide narrow-body fleets, particularly the Airbus A320neo and Boeing 737 MAX, continue to expand, the high installed base of engines featuring ACC systems will sustain segment growth. Moreover, next-gen engines such as the CFM LEAP and Pratt & Whitney GTF depend on turbine clearance control to realize double-digit fuel consumption, resulting in more operations and higher frequency MRO experience on these components, resulting in repeat aftermarket demand.

For instance, in November 2022, according to Aviation Industry Week reports, engine OEMs stated that clearance-control valves ranked among the leading removals in early-service LEAP and GTF fleets owing to thermal stress and seal wear, resulting in repeat aftermarket demand.

The compressor-control (VSV, VBV, and TBV) is anticipated to be the fastest-growing segment during the forecast period. Operators are forced to invest in repairs, spare parts pools, and OEM/authorized distribution agreements for these components due to stretched engine MRO queues and parts shortages. Moreover, modern engine designs and retrofits increasingly use active clearance control and new-aged bleed-flow management to fuel consumption improvements. As a result, there is increases in the incidence of shop visits and specialized repairs for actuators, bell cranks, and VBV/VSV hardware, positioning this segment for accelerated growth over the study period.

For instance, in August 2025, the Defense Logistics Agency Aviation reported the procurement of 53 units of manual bleed valves under NSN 1270005610060 through a Request for Quote (RFQ) solicitation. This procurement involves specialized aircraft parts classified under NAICS code 336413 for Other Aircraft Parts and Auxiliary Equipment Manufacturing and PSC category 12 for Fire Control Equipment.

By Offering

MRO Service Segment Dominates the Market due to High Operating Rates

By offering, the market is divided into MRO Services and Refurbished Parts (USM and PMA).

MRO service segment dominates the commercial aircraft bleed air system market, as airlines worldwide continue to stretch fleet lifecycles and delay aircraft retirements. As a result, the global market is expected to grow steadily, supported by high operating rates and regulatory requirements for recurrent checks of bleed-air and anti-ice valves.

For instance, in April 2024, Lufthansa Technik expanded its capabilities for environmental control and bleed-air component maintenance at its Hamburg facility in response to sustained demand.

Moreover, in May 2020, AAR Corp announced USD 1.5 million contract awards from the U.S. DoD worth for valve and duct overhauls under multi-year sustainment contracts, displaying the ongoing demand for MRO service.

The refurbished parts segment, including Used Serviceable Material (USM) and Parts Manufacturer Approval (PMA) items, is aimed to show the fastest growth with the highest CAGR during the forecast period. Growth in this segment is attributed to rising material and labor costs, which are pushing operators to seek more economical alternatives. Moreover, USM parts provide 30 to 40% cost savings compared with factory-new parts.

Additionally, amid global supply chain tension stemming from the Russia & Ukraine conflict and OEM lead-time, USM and PMA are increasingly important for maintaining fleet availability.

By Aircraft Family

To know how our report can help streamline your business, Speak to Analyst

Boeing 737 (Classic/NG/MAX) Segment Dominates the Market due to its Large In-Service Fleet Size

As per aircraft family, the market is segmented into Airbus A220 (ex-CSeries), Airbus A320 Family (ceo/neo), Airbus A330 (ceo/neo), Airbus A350, Airbus A380, ATR 42/72, Boeing 737 Family (Classic/NG/MAX), Boeing 747, Boeing 767, Boeing 777, Boeing 787, Bombardier CRJ Series, COMAC C919, De Havilland Dash 8 (Q-Series), Embraer E-Jets (E1/E2), and Sukhoi Superjet 100.

The Boeing 737 (Classic/NG/MAX) segment holds the largest share of the global commercial aircraft bleed air systems aftermarket due to its large in-service fleet size of more than 7,000 active aircraft, placing it as the world's most flown narrow-body platform globally. Its heavy flight-cycle usage on short- and medium-haul flights speeds up wear on bleed air items such as valves, ducts, and sensors, necessitating frequent replacements and maintenance. Furthermore, FAA airworthiness directives related to 737NG/MAX anti-ice and check-valve on the 737 family generate the highest share of worldwide demand for bleed air system integrators, MRO services, and replacement parts over other aircraft families.

The COMAC C919 is anticipated to be the fastest-growing segment in the global commercial aircraft bleed air systems aftermarket. COMAC C919 is China's first locally designed narrow-body aircraft, which directly competes with the Airbus A320neo and Boeing 737 MAX. With more than 1,000 orders and commitments, primarily by Chinese airlines and leasing companies (COMAC, 2024), the C919 is expected to have a large fleet expansion in the future. Additionally, as deliveries of this aircraft ramp up, it will create demand for bleed air components such as anti-ice valves, ducts, and clearance control systems. And with China's regulatory effort to achieve domestic supply chain independence, local MRO players and component suppliers are ramping up capabilities, establishing a new and fast-expanding aftermarket environment.

This combination of fleet growth, high flight-cycle utilization on dense domestic networks, and state-sponsored investments in aftermarket infrastructure is expected to drive robust growth in bleed air system MRO and parts demand for the C919 aircraft family over the period.

Commercial Aircraft Bleed Air Systems Aftermarket Regional Outlook

By region, the region is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Commercial Aircraft Bleed Air Systems Aftermarket Size, 2024 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America is the dominating region and has the most developed bleed air systems aftermarket, backed by one of the world's largest active aircraft fleets, dominated by the Boeing 737 and Airbus A320 families. The region benefits from high MRO capacity and high PMA and USM components, which help mitigate supply chain disruptions. Demand is further underpinned by U.S. DoD sustainment contracts, which consistently comprise valve and duct overhauling, maintaining institutional activity at high performance.

As per Aviation Week, the North American commercial MRO market is expected to be worth nearly USD 27 billion by 2025, with component repairs, including bleed air systems, continuing to account for a significant share of total spend.

Europe

Europe represents a mature market for commercial aircraft bleed air systems aftermarket services, and is therefore showing steady growth. The region is dominated by OEM-branded MRO providers such as Lufthansa Technik and SR Technics, alongside a strong base of standalone MROs. The region is especially competitive in high-complexity bleed-air parts such as clearance-control valves and cooling air distributors, underpinned by sophisticated DER engineering and EASA's stringent standards.

For instance, in March 2023, Lufthansa Technik revealed a component shop and new digital maintenance solutions to address growing service demand in the 2020s. European fleet recovery has also fueled shop visits, guaranteeing steady bleed-air workload.

Asia Pacific

Asia Pacific is anticipated to record the second-fastest growth during the forecast period, led by rapid fleet expansion across China, India, and Southeast Asia. The introduction of new airplane families such as the COMAC C919 and high-volume A320neo/737 MAX fleets is resulting in rising demand for bleed-air components, especially anti-ice and clearance-control systems. China represents approximately 38% of the regional bleed air system MRO market in 2024, reflecting its dominant fleet size and government-supported efforts to build local supply chains in valves, ducts, and sensors.

Additionally, the expansion of Localized MRO capacity, such as joint ventures between OEMs and independent service providers, is driving aftermarket development across the region.

For instance, in September 2024, Singapore Aero Engine Services (SAESL), a joint venture between Rolls-Royce and SIA Engineering Company, announced a USD 180 million expansion of its engine MRO facility near Changi Airport. The project will add capacity for engine inductions, logistics, and component repairs, including low-pressure turbine components, with completion expected by 2026.

Middle East & Africa

The Middle East & Africa is emerging as a strategic MRO hub, with lead carriers such as Emirates, Qatar Airways, and Saudia making heavy investments in in-house maintenance capabilities. The region benefits from hub-to-hub flight operations, which result in high performance and predictable bleed-air component wear, especially in anti-ice valves due to hot-and-dusty operating conditions. Governments and airlines across the region are expanding hangar capacity and third-party MRO facilities to capture wider regional demand. As a result, the MRO market is expected to grow at the highest CAGR by 2045.

For instance, in November 2023, Sanad inaugurated its new LEAP Engine Maintenance, Repair, and Overhaul (MRO) Centre in Abu Dhabi. Spanning over 5,000 square meters, it marked a strategic milestone as the first certified engine MRO facility in South Asia, the Middle East, and North Africa. In December 2024, Sanad expanded its capabilities by launching support for the LEAP-1A engine, complementing its prior focus on the LEAP-1B.

Latin America

Latin America has a smaller MRO base than other regions but is undergoing rapid modernization, reshaping the bleed-air aftermarket. For instance, in August 2024, Carriers such as LATAM Airlines announced USD 2 billion in investment programs focused on Brazil-based MRO facilities and training centers, indicating the region's efforts to decrease dependence on North America and Europe to overhaul components.

Competitive Landscape

Key Industry Players

Key Players are Forging a Partnership to Enhance Logistics Support

The global commercial aircraft bleed air systems aftermarket is influenced by a combination of OEM control, independent MRO alliances, and growing refurbished parts usage. Honeywell, Safran, Liebherr, and Parker Aerospace are among the OEMs that are maintaining control of component design, certification, and repair authority. Liebherr-Aerospace combines in-house manufacturing with overhaul services, providing certified refurbished parts through its worldwide USM network. OEM-supported alliances such as OEMServices further enhance logistics support, parts pooling, and predictive maintenance solutions, improving customer access and service flexibility. This ecosystem allows airlines to benefit from OEM-quality standards with the flexibility to source parts.

Meanwhile, digitalization and regionalization are also shaping the market and providing new growth opportunities. AI, IoT, and digital twin-based predictive maintenance are allowing airlines to track bleed-air components such as anti-ice valves and ducts in real-time, optimizing the replacement cycles. This minimizes surprise downtime and generates demand for overhauled components that reduce lifecycle costs. Regionally, the growth of Asia Pacific, the Middle East, and Latin America is fueled by MRO joint ventures, government incentives, and large airline investments in regional capabilities. This expansion decreases reliance on North America and Europe and reduces turnaround times for carriers with high operational bases. The integration of refurbished parts programs with expanding local MRO capacity is increasing competitiveness while broadening customer choice across the commercial aircraft bleed air systems aftermarket.

LIST OF KEY COMMERCIAL AIRCRAFT BLEED AIR SYSTEMS AFTERMARKET PLAYERS Profiled

|

SR. No |

MRO Service & Refurbished Parts Company |

MRO Service Providers |

Refurbished Parts Suppliers |

|

|

1 |

Honeywell Aerospace (U.S.) |

ST Engineering (Singapore) |

GA Telesis (U.S.) |

|

|

2 |

Safran Aerosystems (France) |

AAR Corp. (U.S.) |

HEICO Aerospace (China) |

|

|

3 |

Liebherr-Aerospace (France) |

Lufthansa Technik (Germany) |

AvAir (U.S.) |

|

|

4 |

Collins Aerospace (U.S.) |

SR Technics (Switzerland) |

AeroTurbine (U.S.) |

|

|

5 |

Parker Aerospace (U.S.) |

HAECO Group (China) |

Wencor Group (U.S.) |

|

|

6 |

|

Delta TechOps (U.S.) |

Air Salvage International (ASI) (U.K.) |

|

|

7 |

|

MTU Maintenance (Germany) |

|

|

KEY INDUSTRY DEVELOPMENTS

- February 2025- TARMAC Aerosave and Safran Aircraft Engines signed a contract extension at the MRO Middle East event to continue the installation of the Reverse Bleed System (RBS) on CFM LEAP-1A engines.

- November 2024- AFI KLM E&M began installing RBS kits on CFM LEAP-1A engines, expanding its MRO capabilities for Airbus A320neo family fleets under the CFM service bulletin SB72-0476.

- February 2025- At MRO Middle East, IndiGo and Air India Express signed MRO agreements with Turkish Technic for redelivery checks and component support, including overhaul, modification, and logistics services for LEAP and 737 engines, which typically encompass bleed-air components.

- February 2025- Air Côte d’Ivoire extended its component support contract with AFI KLM E&M for five years, covering its expanding Airbus fleet, including A320 and A330neo aircraft. While not explicitly about bleed-air, this framing includes rotatable systems that often rely on bleed-air integration.

- February 2025- Royal Jordanian signed component services agreements with Boeing, including support for 787-9 components and landing gear exchange programs, components that integrate pneumatic systems such as bleed-air controls.

REPORT COVERAGE

The research report delivers a detailed analysis of the market and emphasizes key aspects such as key players, offerings, objects, and end-users of the aircraft bleed air system. Moreover, the report deals with insights into commercial aircraft bleed air systems aftermarket trends, competitive landscape, market competition, product pricing, regional analysis, market players, competition landscape, and the market status, and highlights key industry growth. In addition to the factors stated above, the report encompasses several direct and indirect influences that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2045 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2045 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 2.6% from 2025 to 2045 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component · General o Bleed Air Duct o Check Valve · Engine Anti-Icing o Anti-Ice Valve o Bleed Air Duct o Temperature Sensor o Nacelle Anti-Icing Control Valve o Engine Anti-Icing Shutoff Valve · Cooling o HP Turbine Active Clearance Control (HPTACC) o LP Turbine Active Clearance Control (LPTACC) o Turbine Clearance Control Valve o Cooling Air Manifold o Cooling Air Distributor · Compressor Control o Variable Stator Vane (VSV) System o Variable Bleed Valve (VBV) System o VSV Actuator o Bellcrank Assembly o Transient Bleed Valve (TBV) o 5th Stage Bleed Valve o Bleed Bias Sensor · Indicating o Pressure Sensor/Transmitter o Temperature Indicator o Position Indicator (LVDT/RVDT) o Control Panel/Display Unit o ANTI-ICE ON Indicator Light o Bleed Air Pressure Gauge |

|

By Offerings · MRO Services · Refurbished Parts o USM o PMA |

|

|

By Aircraft Family · Airbus A220 (ex-CSeries) · Airbus A320 Family (CEO/NEO) · Airbus A330 (CEO/NEO) · Airbus A350 · Airbus A380 · ATR 42/72 · Boeing 737 Family (Classic/NG/MAX) · Boeing 747 · Boeing 767 · Boeing 777 · Boeing 787 · Bombardier CRJ Series · COMAC C919 · De Havilland Dash 8 (Q-Series) · Embraer E-Jets (E1/E2) · Sukhoi Superjet 100 |

|

|

By Region · North America ( By Component, By Offerings, By Aircraft Family, and By Country) o U.S. (By Component) o Canada (By Component) · Europe (By Component, By Offerings, By Aircraft Family, and By Country) o U.K. (By Component) o Germany (By Component) o France (By Component) o Russia (By Component) o Rest of Europe (By Component) · Asia-Pacific (By Component, By Offerings, By Aircraft Family, and By Country) o China (By Component) o India (By Component) o Japan (By Component) o South Korea (By Component) o Rest of Asia-Pacific (By Component) · Middle East & Africa (By Component, By Offerings, By Aircraft Family, and By Country) o Saudi Arabia (By Component) o Israel (By Component) o Turkey (By Component) o Rest of the Middle East (By Component) · Latin America (By Component, By Offerings, By Aircraft Family, and By Country) o Brazil (By Component) o Rest of Latin America (By Component) |

Frequently Asked Questions

According to the Fortune Business Insights study, the global market was valued at USD 8,944.4 million in 2024 and is anticipated to be USD 15,574.2 million by 2045.

The market will likely grow at a CAGR of 2.6% over the forecast period (2025-2045).

The top ten players in the industry are Honeywell Aerospace, Safran Aerosystems, Liebherr-Aerospace, Collins Aerospace (Raytheon Technologies), Parker Aerospace, ST Engineering, AAR Corp., Lufthansa Technik, SR Technics, and HAECO Group.

North America dominates the market.

Increasing demand for air travel is the key factor driving market growth.

High cost of skilled labor is the key restraining factor for market growth.

- 2019-2045

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us