Connectivity Module Market Size, Share & Industry Analysis, By Connectivity Technology (Cellular (WWAN), LPWA (Cellular), LPWAN (Non-cellular), Short-Range (WLAN/PAN), & Positioning), By Form Factor (LGA/SMT Modules, Mini-PCIe, uBlox-style castellation, Plug-in, and Combo Modules), By Deployment (On-premises & Cloud) By Power (Low, Medium, High) By Industry Vertical (Automotive & Transportation, Manufacturing, Energy & Utilities, Healthcare, Retail & E-commerce, Residential/Commercial Buildings, Government & Public Sector/Smart Cities, IT-Telecom, & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

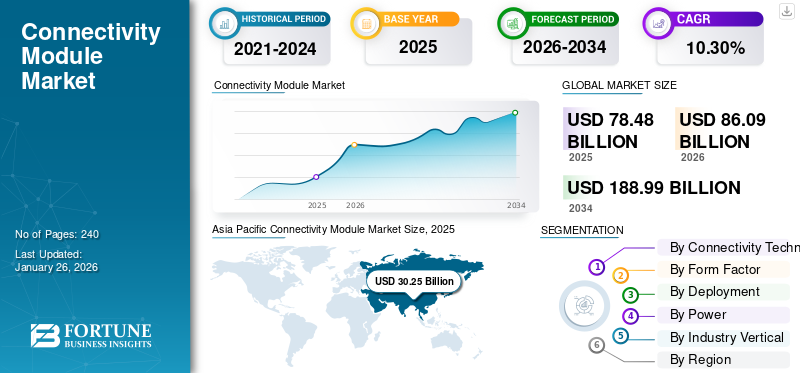

The global connectivity module market size was valued at USD 78.48 billion in 2025. The market is projected to grow from USD 86.09 billion in 2026 to USD 188.99 billion by 2034, exhibiting a CAGR of 10.30% during the forecast period. Asia Pacific dominated the global market with a share of 38.50% in 2025.

Connectivity module is a hardware component that enables wireless communication between the devices through standards such as Wi-Fi Bluetooth, 5G, LTE and NB-IoT. This is highly crucial for IoT ecosystems across industries including healthcare, automotive, and industrial automation.

The market is growing steadily due to growing IoT adoption, demand for different vehicle connectivity, advancements in 5G technology, surge in smart infrastructure, and consumer preference for seamless communication.

Few prominent key players operating in the market include Sierra Wireless, Murata Manufacturing Co., Ltd, Quectel Wireless Solutions, Fibocom Wireless Inc., SIMCom Wireless Solutions, Nordic Semiconductor, Sequans Communications, and Ezurio. These players are adopting different strategies including development of compact multi-protocol modules, partnerships with various telecom operators and others.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Generative AI Drives Smarter Edge Processing, Boosting Connectivity Module Demand

Generative AI is changing the connectivity module landscape by allowing smarter edge devices to process data locally instead of depending solely on cloud computing. This tends to reduce latency, minimize bandwidth consumption and promotes real-time decision-making.

With AI models becoming more efficient, these are increasingly adopted in devices, thus driving the demand for advanced connectivity modules that aids in faster data exchange and on-device intelligence. Similarly, manufacturers are also developing AI based modules that are optimized for 5G and IoT applications, thus enabling an improved network efficiency, wider adoption across industries and enhanced security.

MARKET DYNAMICS

Market Drivers

Growing Adoption of IoT Devices Drives Market Development

The rapid expansion of Internet of Things (IoT) is significantly driving the connectivity module market growth. With growing connected industries, smart homes and intelligent urban infrastructure, the need for reliable wireless communication has grown.

- For instance, according to OCED, IoT-related patent applications grew by close to 20% a year in 2010-18 and accounted for over 11% of all patenting activity worldwide at the end of the period. Venture capital investment in IoT firms also increased dramatically in the last decade, reaching USD 8 billion in 2020. Additionally, according to the estimates by National Cybersecurity Center of Excellence, there will be more than 75 billion IoT devices in use by 2025.

IoT enabled devices including smart appliance, vehicle, wearable, and industrial sensor needs a connectivity module to transfer data and interact with networks. This leads to increased integration of IoT technology, further fueling the demand for modules supporting Bluetooth, Wi-Fi, LTE, and 5G.

Market Restraints

Global Supply Chain Disruptions Hampers the Market Growth

The market faces crucial challenges due to supply chain disruptions globally. Ongoing semiconductor shortage, transportation issues, and growing geopolitical issues have led to interruptions in production and increase in manufacturing costs. Such challenges affect the accessibility of different components including sensors, and chips. This slowdown the product launches and reducing in profit margins for manufacturers.

Additionally, the dynamic raw and material prices as well as trade restrictions also challenges the operational efficiency and hinders timely deliveries. This results in companies struggling to meet the growing demand, impacting the overall market expansion and innovation in the industry.

Market Opportunities

Expansion of 5G & Advanced Cellular Networks Offers Lucrative Growth Opportunities

The ongoing global rollout of 5G and advanced cellular networks create a significant opportunity for the market growth. 5G’s ultra-low latency, massive device connectivity, and high-speed data transfer allows seamless communication for application such as autonomous vehicles, smart city infrastructure and industrial robots.

Additionally, this growing ecosystem has also driven the demand for 5G compatible modules which is capable of handling complex data processing and real time responsiveness. With industries adopting digital transformation and IoT solutions, manufacturers are highly investing in advanced 5G modules to meet the evolving connectivity needs, thus paving ways for scalability, innovation and long term market expansion.

CONNECTIVITY MODULE MARKET TRENDS

Smart Cities & Infrastructure Projects Has Emerged as a Prominent Market Trend

The ongoing development of smart cities has emerged as a major market trend. Urban infrastructure dynamically relies on the modules with the use of LPWAN, Wi-Fi and cellular technologies to manage and connect devices effectively. These modules allow for real time data collection, control and monitoring of essential systems including street lights, traffic management, public safety and waste disposal.

Additionally, government and private sectors are investing in connected infrastructure to enhance energy efficiency, sustainability, and citizen services. This integration of IoT and connected technologies is crucially boosting demand for scalable, reliable and secure connectivity modules globally.

IMPACT OF RECIPROCAL TARIFF

Reciprocal Traffics Disrupt Global Supply Chains and Slow Downs Market Growth

Reciprocal tariffs between major trading countries increase the cost of importing significant components used in manufacturing connectivity modules. As these modules increasingly rely on complex, globally embedded supply chains, the augmented import duties increase the production costs and postponement component availability.

Manufacturers are forced to pass these costs to customers, thus leading to a higher end-product prices. This is resulting in demand from key sectors including consumer electronics, automotive and industrial IoT weakens. This hampers the global trade efficiency, reduces the competitiveness, leading to slower market growth.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Connectivity Technology

Growing Wider Applications of Short-Range Modules Boosts Segment Growth

Based on connectivity technology, the market is segmented into Cellular (WWAN), LPWA (Cellular), LPWAN (Non-cellular), Short-Range (WLAN/PAN), and Positioning.

The short-range (WLAN/PAN) connectivity technology segment is projected to dominate the market with a share of 50.36% in 2026. This segment growth is driven by its wider applications across different industries. These industries could include smart homes, consumer electronics and offices where Bluetooth and Wi-Fi due to its cost effectiveness and convenience.

Cellular (WWAN) segment held the highest CAGR of 13.8% in 2024. These modules are growing faster with 5G rollout. Additionally, the increasing IoT use cases including automotive, smart cities, and remote monitoring demand wide-area coverage.

By Form Factor

Easy Integration and Highly Reliable Manufacturing for Mass Production Drives LGA/SMT Segment Growth

The market is divided into LGA/SMT Modules, Mini-PCIe, uBlox-style castellation, plug-in, and combo modules, based on form factor.

The LGA/SMT modules form factor segment is expected to lead the market, accounting for 50.44% of the total market share in 2026. These surface mount modules tend to offer easy integration and highly reliable manufacturing for mass production. Additionally, compact size and cost efficiency promotes its adoption in automated manufacturing processes.

Additionally, the combo modules segment grew with a highest CAGR of 15.2% in 2024. This supports various protocols including cellular, Bluetooth, and Wi-Fi in a single package, thus meeting the growing need for global and flexible connectivity. These factors collectively contribute to the segment’s growth.

By Deployment

Higher Scalability and Remote Management in IoT and Connected Devices Enhances Cloud Segment Growth

Based on the deployment, the market is divided into on premise and cloud.

The cloud-based deployment segment is anticipated to hold a dominant market share of 65.32% in 2026. This growth is due to its higher scalability, remote management in IoT and connected devices, and its easy updates. It also enables real time data access, faster updates and remote monitoring without the need for heavy investments.

On the other hand, the on premise segment held highest CAGR of 12.9% in 2024. The demand for on premise deployment based solutions is increasing in industries that require low latency, data privacy, and regulatory compliance, including manufacturing and healthcare. These factors are driving the segment’s growth.

By Power

Capability of Extending Battery Life and Supporting Long Term Data Transmission Supplements Low Power Segment Growth

Based on the power, the market is segmented into low, medium, and high.

The low power segment held the highest market share in 2024 contributing a revenue of USD 34.83 billion. As various IoT devices focus on battery life, opting for low-power modules for sensors, asset tracking and wearables. These modules are capable of extending battery life, supporting long term data transmission and reducing maintenance costs.

On the other hand, the high power segment held highest CAGR of 16.2% in 2024. The application of high power modules is growing due as it covers higher data rates including video streaming, industrial automation and autonomous vehicles.

By Industry Vertical

To know how our report can help streamline your business, Speak to Analyst

Expanding Adoption of Sensors and Connected Devices Augments the Manufacturing Segment Growth

Based on the industry vertical, the market is segmented into automotive & transportation, manufacturing, energy & utilities, healthcare, retail & e-commerce, residential/commercial buildings, government & public sector/smart cities, IT and telecom, and others.

The manufacturing segment held the highest market share in 2024 contributing a revenue of USD 12.31 billion. This segmental growth is attributed to the widespread adoption of automation, sensors and connected machines across manufacturing sectors in different industries, driving the large volume module use.

On the other hand, the healthcare segment held highest CAGR of 15.1% in 2024. This growth is due to the growing adoption of connected devices in healthcare sector for telehealth, remote monitoring, and wearables is accelerating the growth prominently from a smaller base.

CONNECTIVITY MODULE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

Asia Pacific Connectivity Module Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market is growing with an expected share of USD 21.88 billion in 2025. This growth is owing to the increasing adoption of IoT technology, effective 5G infrastructure, and growing demand for connected vehicles and smart devices. Additionally, supportive government initiatives and presence of major key players across the U.S. also boosts the market growth. The U.S. market is projected to reach USD 20.01 billion by 2026. In 2025, North America generated USD 21.88 billion, contributing 27.90% to global market revenue, and is projected to grow to USD 23.82 billion in 2026.

Europe

The European market is substantially growing and predicted to contribute to a revenue share of USD 16.71 billion in 2025. This growth is attributed to the expansion of smart city projects, connected vehicles and rapid adoption of IoT technology across the region. U.K., Germany, and France are some of the major contributors to the market growth with an expected revenue share of USD 2.71 billion, USD 2.96 billion, and USD 2.91 billion respectively by 2025. The Europe market accounted for USD 16.71 billion in 2025, representing 21.30% of the global industry, and is expected to reach USD 18.32 billion in 2026.

The UK market is projected to reach USD 3.32 billion by 2026, while the Germany market is projected to reach USD 2.29 billion by 2026.

Asia Pacific

Asia Pacific dominates the market with a revenue share of USD 27.46 billion in 2024, and USD 24.96 billion in 2023. This regional growth is due to the presence of large manufacturing base, massive smart city projects, ongoing IoT adoption and industrial automation programs that drives the high demand for connectivity modules. The Japan market is projected to reach USD 5.1 billion by 2026, the China market is projected to reach USD 15.77 billion by 2026, and the India market is projected to reach USD 3.93 billion by 2026. Asia Pacific recorded a market size of USD 30.25 billion in 2025, capturing 38.50% of the global market share, and is projected to reach USD 33.42 billion in 2026.

Latin America

The markets of South America and Middle East & Africa are growing with an expected share of USD 6.64 billion and USD 3.00 billion respectively in 2025. The Middle East & Africa region is growing with highest CAGR of 8.5% in 2025. This growth is driven by the growing investments in digital infrastructure and smart city programs that creates new market opportunities and accelerates the module adoption. GCC countries are predicted to have a market share of USD 0.92 Billion by 2025. Latin America accounted for USD 6.64 billion in 2025, representing 8.50% of the global market share, and is projected to reach USD 7.22 billion in 2026.

Middle East & Africa

The Middle East & Africa market generated USD 3 billion in 2025, representing 3.80% of the global market landscape, and is expected to reach USD 3.32 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Key Players on Innovation and New Launches Leads to their Governing Market Positions

The global connectivity module industry is highly competitive featuring a mix of key players Sierra Wireless, Murata Manufacturing Co., Ltd, Quectel Wireless Solutions, Fibocom Wireless Inc., SIMCom Wireless Solutions, Nordic Semiconductor, Sequans Communications, and Ezurio. These companies are focusing on extensive research and development, product innovation, and enhancing global distribution networks.

LIST OF KEY CONNECTIVITY MODULE COMPANIES PROFILED

- Sierra Wireless (Canada)

- Murata Manufacturing Co., Ltd (Japan)

- Quectel Wireless Solutions (China)

- Fibocom Wireless Inc. (China)

- SIMCom Wireless Solutions (China)

- Nordic Semiconductor (Norway)

- Sequans Communications (France)

- Ezurio (U.S.)

- Telit Communications (U.K.)

- Huawei Technologies (China)

- U-blox (Switzerland)

- Queclink Wireless Solutions (China)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, MikroElektronika, the Serbian embedded solutions manufacturer, has launched a new low-power wireless connectivity module aimed at accelerating the development of Internet of Things (IoT) and Industrial IoT (IIoT) applications.

- In September 2025, Digi International, a leading global provider of Internet of Things (IoT) connectivity products and services, announced the Digi XBee 3 BLU module. This latest addition to the award-winning Digi XBee family of embedded wireless modules delivers reliable, secure Bluetooth Low Energy (LE) 5.4 connectivity for connected products with provisioning, edge processing, and mobile management capabilities in industrial, healthcare, retail, and smart building applications.

- In March 2025, Lantronix Inc., a global contributor of compute and connectivity for Internet of Things (IoT) solutions enabling Edge AI Intelligence, announced its new Open-Q 8550CS System-on-Module (SOM). Powered by the Qualcomm Dragonwing QCS8550 processor, this production-ready module provides low-power, on-device Artificial Intelligence (AI) and Machine Learning (ML) capabilities, simplifying design and empowering developers to more quickly bring edge products to market.

- In November 2024, Qualcomm introduced new micro-powered Wi-Fi and programmable IoT connectivity modules. These modules are perfectly suited for IoT applications in the smart home, smart appliances and more. QCC730M is a dual-band, micro-power Wi-Fi 4 module offering a dedicated MCU at 60MHz, 640kB SRM and 1.5 RRAM, integrated hardware crypto accelerator, and secure boot, debug, and storage. QCC730M leading micro-power Wi-Fi can be the prime component for battery-powered IoT applications especially IP cameras, sensing, and smart locks. QCC74xM is the first programmable connectivity module, offering flexibility to run applications with the RISC-V. It offers comprehensive connectivity including technology support for Wi-Fi, Bluetooth, Thread and Zigbee-ready.

- In June 2022, TOKYO, Renesas Electronics Corporation, a premier supplier of advanced semiconductor solutions, announced two new cloud development kits, CK-RA6M5 and CK-RX65N, providing a complete connectivity solution for the RA and RX Families of 32-bit microcontrollers (MCUs). The cloud kits are the first to be equipped with Renesas’ RYZ014A Cat-M1 module, a certified LTE cellular module that offers the ability to establish wireless connection between MCUs and cloud services quickly and securely without a gateway.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the connectivity module market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021–2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 10.30% from 2026-2034 |

| Historical Period | 2019-2023 |

| Unit | Value (USD billion) |

| Segmentation |

By Connectivity Technology · Cellular (WWAN) · LPWA (Cellular) · LPWAN (Non-cellular) · Short-Range (WLAN/PAN) · Positioning By Form Factor · LGA/SMT Modules · Mini-PCIe · uBlox-style castellation · Plug-in · Combo Modules By Power · Low · Medium · High By Deployment · On-premises · Cloud By Industry Vertical · Automotive & Transportation · Manufacturing · Energy & Utilities · Healthcare · Retail & E-commerce · Residential/Commercial Buildings · Government & Public Sector/Smart Cities · IT and Telecom · Others (Education, Agriculture, etc.) By Region · North America (By Connectivity Technology, Form Factor, Deployment, Power, Industry Vertical and Country/Sub-region) o U.S. (By Industry Vertical) o Canada (By Industry Vertical) o Mexico (By Industry Vertical) · Europe (By Connectivity Technology, Form Factor, Deployment, Power, Industry Vertical and Country/Sub-region) o U.K. (By Industry Vertical) o Germany (By Industry Vertical) o France (By Industry Vertical) o Italy (By Industry Vertical) o Spain (By Industry Vertical) o Russia (By Industry Vertical) o Benelux (By Industry Vertical) o Nordics (By Industry Vertical) o Rest of Europe · Asia Pacific (By Connectivity Technology, Form Factor, Deployment, Power, Industry Vertical and Country/Sub-region) o China (By Industry Vertical) o Japan (By Industry Vertical) o India (By Industry Vertical) o South Korea (By Industry Vertical) o ASEAN (By Industry Vertical) o Oceania (By Industry Vertical) o Rest of Asia Pacific · South America (By Connectivity Technology, Form Factor, Deployment, Power, Industry Vertical and Country/Sub-region) o Argentina (By Industry Vertical) o Brazil (By Industry Vertical) o Rest of South America · Middle East & Africa (By Connectivity Technology, Form Factor, Deployment, Power, Industry Vertical and Country/Sub-region) o Turkey (By Industry Vertical) o Israel (By Industry Vertical) o North Africa (By Industry Vertical) o GCC (By Industry Vertical) o South Africa (By Industry Vertical) o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 78.48 billion in 2025 and is projected to reach USD 188.99 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 10.30% during the forecast period.

Rise in the demand for IoT devices drives the market growth.

Sierra Wireless, Murata Manufacturing Co., Ltd, Quectel Wireless Solutions, Fibocom Wireless Inc., SIMCom Wireless Solutions, Nordic Semiconductor, Sequans Communications, and Ezurio are some of the top players in the market.

The Asia Pacific region held the largest market share.

North America was valued at USD 21.88 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 240

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us