Construction Aggregates Market Size, Share & Industry Analysis, By Type (Crushed Stone, Sand & Gravel, and Others), By End-Use Industry (Residential, Commercial, and Others), and Regional Forecast, 2026-2034

Construction Aggregates Market Size and Future Outlook

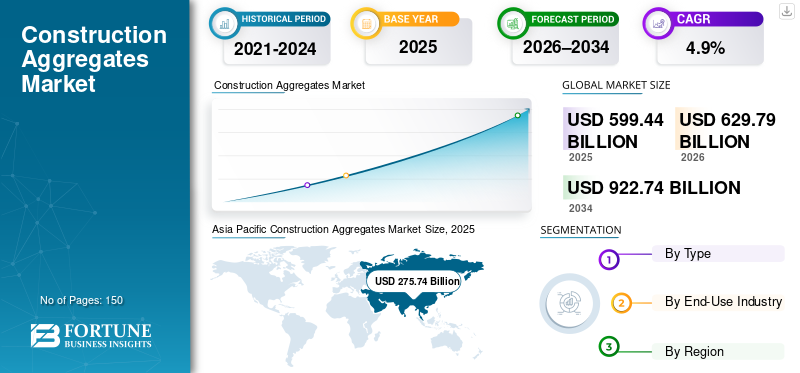

The global construction aggregates market size was valued at USD 599.44 billion in 2025. The market is projected to grow from USD 629.79 billion in 2026 to USD 922.74 billion by 2034, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the construction aggregates market with a market share of 46.% in 2025.

Construction aggregates, such as crushed stone, sand, and gravel, are essential materials widely used in concrete, asphalt, and road base applications. Demand for aggregates is directly linked to construction activity across residential, commercial, and infrastructure projects, where strength, availability, and cost efficiency are critical. The market is supported by urban development, transport network expansion, and continuous maintenance of existing infrastructure. Globally, aggregate demand is driven more by replacement and project-based consumption than rapid capacity expansion, resulting in a high-volume, locally supplied market characterized by stable, predictable demand and limited long-term volatility across key construction regions.

The market is dominated by a limited number of large, vertically integrated producers with extensive quarrying assets and established processing capabilities. Major players such as Holcim, Heidelberg Materials, CEMEX, Vulcan Materials, and CRH Americas Materials, Inc. focus on secure reserves, efficient logistics networks, and consistent supply reliability, resulting in a moderately consolidated market characterized by steady demand, high transportation-related switching costs, and tightly controlled regional capacity.

Download Free sample to learn more about this report.

Construction Aggregates Market Key Takeaways

- 2025 Market Size: USD 599.44 billion

- 2026 Market Size: USD 629.79 billion

- 2034 Forecast Market Size: USD 922.74 billion

- CAGR: 4.9% from 2026–2034

- Asia Pacific dominated the construction aggregates market with a 46.0% share in 2025.

- The crushed stone segment accounted for the largest market share in 2025.

- The residential segment accounted for the largest market share in 2025.

North America

North America accounted for a significant share in 2025, valued at USD 131.88 billion.

Asia Pacific

Asia Pacific held a 46.0% share in 2025, valued at USD 275.74 billion.

Europe

Europe held a substantial share in 2025, valued at USD 107.90 billion.

U.S.

The market valued at USD 116.05 billion in 2025.

Japan

The market growth is supported by infrastructure modernization, urban development projects, and ongoing demand for residential and commercial construction materials.

Read More

CONSTRUCTION AGGREGATES MARKET TRENDS

Greater Focus on Sustainable and Compliant Aggregate Production Is Shaping Market

A stronger focus on sustainability and regulatory compliance increasingly shapes the market. Producers are adopting practices such as recycled aggregate use, improved quarry restoration, and more energy-efficient processing to meet environmental and land-use requirements. These changes reflect a shift in how aggregates are produced and managed rather than a change in demand levels. From a business perspective, sustainability is becoming an important factor in maintaining operating licenses, controlling costs, and ensuring long-term production continuity.

- According to the U.S. Environmental Protection Agency (EPA), the U.S. generated over 600 million tons of construction and demolition debris, with a significant portion reused or recycled, supporting the growing shift toward recycled aggregates and more sustainable production practices.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Public Infrastructure Projects Support Steady Aggregate Demand

The market is driven by public infrastructure projects, including roads, bridges, airports, rail networks, and urban transit systems. Aggregates are essential materials in concrete, asphalt, and structural base layers as they provide strength, stability, and long-term durability. Continued government investment in infrastructure development, rehabilitation, and maintenance sustains aggregate consumption, as these projects require large and consistent volumes of stone, sand, and gravel. Unlike short-cycle construction activities, public infrastructure projects are typically long-term and funding-backed, which helps maintain steady, predictable demand for the product across regions.

- According to the Ministry of Road Transport and Highways (MoRTH), Government of India, the country’s national highway network exceeds 146,145 km, highlighting sustained public infrastructure development that directly drives large-scale demand for construction aggregates.

MARKET RESTRAINTS

High Dependence on Construction Cycles Creates Demand Volatility for Aggregates

The demand is constrained by its strong dependence on construction and infrastructure activity, which is highly sensitive to economic cycles. Slowdowns in residential construction, delays in public infrastructure projects, or reduced private investment can quickly lower demand for concrete, asphalt, and road base materials. Unlike manufactured materials, which allow flexible end-use substitution, aggregate consumption is directly tied to project execution and capital spending. As a result, periods of economic uncertainty, budget tightening, or interest rate increases can lead to short-term demand volatility in regional aggregates markets.

- According to the U.S. Census Bureau, privately owned housing starts in October 2025 were at a seasonally adjusted annual rate of 1,246,000 units, which was 7.8% below the October 2024 level, highlighting volatility in residential construction activity that can weaken demand for aggregates.

MARKET OPPORTUNITIES

Urban High-Rise and Mixed-Use Developments are Creating Growth Opportunities

Urbanization and increasing land constraints are creating opportunities for the construction aggregates market growth as high-rise and mixed-use buildings are increasingly developed. These projects require higher volumes of concrete and reinforced structural materials per unit area than low-rise construction, increasing aggregate use per project. As cities continue to favor vertical development to optimize land use and support population density, aggregate consumption intensity rises, generating incremental demand beyond baseline construction activity.

- According to the World Bank, over 56% of the global population lived in urban areas in 2022, and this share is projected to continue rising, supporting increased development of high-density residential and mixed-use buildings that require higher aggregate intensity per project.

MARKET CHALLENGES

High Operating and Transportation Costs Limit Margin Stability

Producers face challenges from high operating and transportation costs. Quarrying, crushing, and hauling aggregates require significant energy and labor, while fuel prices directly affect delivery costs. As aggregates are low-value, high-volume materials, producers have limited ability to pass rising costs on to customers. As a result, even when construction demand remains steady, profit margins can come under pressure, making cost control and operational efficiency critical for long-term viability.

- According to the U.S. Federal Highway Administration (FHWA), the National Highway Construction Cost Index increased by around 70% between 2020 and 2024, reflecting sharp rises in material, energy, and transportation costs that are putting pressure on margins for aggregate producers.

Segmentation Analysis

By Type

Crushed Stone Segment Held Dominance as It is Widely Used in Concrete Production

Based on type, the market is segmented into crushed stone, sand & gravel, and others.

The crushed stone segment accounted for the largest construction aggregates market share in 2025. Crushed stone leads aggregate consumption as it is a critical input in concrete production, road base layers, and large-scale infrastructure projects where strength, load-bearing capacity, and durability are essential. Demand for crushed stone is largely non-discretionary, particularly in highways, bridges, and heavy construction, creating a strong volume pull across infrastructure-led projects. As public infrastructure investment and heavy construction activity continue to dominate aggregate usage, crushed stone remains the most structurally anchored and consistently consumed aggregate type.

The sand & gravel segment is expected to grow at a steady CAGR of 4.8% in the coming years, supported by consistent demand from residential construction, concrete production, and repair activities driven by stable building and maintenance requirements.

To know how our report can help streamline your business, Speak to Analyst

By End-Use Industry

Residential Segment Dominated Market Due to Rising Need for Concrete and Mortar in Housing Projects

By end-use industry, the market is segmented into residential, commercial, and others.

The residential segment accounted for the largest share in 2025. Residential construction increases aggregate demand as housing projects require large volumes of concrete and mortar for foundations, structural elements, and finishing work. Aggregates are essential, non-substitutable materials in housing construction, making demand closely tied to new homebuilding and renovation activity. Ongoing urbanization, population growth, and housing replacement needs support steady aggregate consumption, positioning residential construction as a stable and structurally important demand base for the market.

- According to Eurostat, construction production in the EU increased by 0.1% month-on-month in July 2024, indicating continued residential and building activity that supports steady demand for construction aggregates.

The commercial segment is expected to grow at a CAGR of 4.8% over the forecast period.

Construction Aggregates Market Regional Outlook

By region, the market is divided into Latin America, Europe, Asia Pacific, North America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Construction Aggregates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in 2025, valued at USD 275.74 billion, and is expected to maintain its leading role in 2026, reaching USD 291.10 billion. The region’s leadership is driven by large-scale infrastructure development, rapid urbanization, and high construction activity across major economies. Strong demand from residential housing, transportation infrastructure, and public works supports sustained aggregate consumption, particularly in high-volume, cost-sensitive construction applications where local sourcing and material availability are critical.

China Construction Aggregates Market

Based on Asia Pacific’s strong contribution and China’s large-scale construction footprint, the China construction aggregates market was valued at USD 151.66 billion in 2025, accounting for approximately 55.0% of regional revenues. Demand is supported by extensive residential and infrastructure construction activity, including highways, urban housing, and public works projects, along with a well-developed domestic quarrying and materials supply base that enables high-volume aggregate production and consumption.

India Construction Aggregates Market

The India market was valued at around USD 55.15 billion in 2025. Growth is supported by expanding residential construction, rising infrastructure investment, and ongoing road and urban development projects. Strong demand from housing, transportation networks, and public infrastructure continues to drive aggregate consumption.

North America

North America remains a significant market, valued at USD 131.88 billion in 2025. Residential construction, infrastructure repair, and transportation network upgrades support demand. The region benefits from an established quarrying and distribution base and steady replacement demand, although overall growth remains moderate due to market maturity and limited large-scale capacity additions.

U.S. Construction Aggregates Market

The U.S. market was valued at USD 116.05 billion in 2025, representing approximately 88.0% of regional revenues. Consumption is driven by residential and commercial construction, highway and infrastructure projects, and ongoing repair and replacement of roads, bridges, and public assets requiring large volumes of concrete and asphalt.

Europe

Europe is projected to record modest growth over the forecast period. It was valued at USD 107.90 billion in 2025. Strict environmental and permitting regulations, high energy costs, and limited availability of new quarry sites characterize the region. Despite these constraints, ongoing demand from residential construction, infrastructure maintenance, and renovation activity continues to support steady consumption of construction aggregates across major European markets.

Germany Construction Aggregates Market

Germany’s market was valued at USD 21.58 billion in 2025, accounting for around 20.0% of regional demand. Residential construction, infrastructure maintenance, transportation projects, and ongoing urban renovation activity across the country support consumption.

U.K. Construction Aggregates Market

The U.K. market was valued at USD 18.34 billion in 2025, accounting for roughly 17.0% of regional revenues. Consumption is concentrated in residential construction, infrastructure maintenance, roadworks, and public building projects requiring concrete and asphalt materials.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth during the forecast period. The Latin America market was valued at USD 47.96 billion in 2025, supported by residential construction, infrastructure development, and transportation projects across major economies. Demand is also aided by gradual urban expansion and public investment programs. In the Middle East & Africa, aggregate consumption is driven by urban development, large-scale infrastructure projects, and ongoing investment in roads, housing, and public facilities. The Middle East & Africa market was valued at USD 35.97 billion in 2025, supported by long-term, regionally focused government-led development initiatives.

GCC Construction Aggregates Market

The GCC market accounted for around USD 16.18 billion in 2025, representing approximately 45.0% of regional revenues. Demand is supported by large-scale construction activity, infrastructure development, and ongoing investment in roads, housing, and commercial projects across the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Asset Control and High Capital Requirements Shape Industry Rivalry

Significant capital requirements continue to shape the competitive landscape, as quarry development, permitting complexities, and heavy investments in extraction and distribution infrastructure create high entry barriers. These dynamics concentrate market supply within a small group of established, regionally integrated aggregate manufacturers with proven operating capabilities and secured reserves.

Industry leaders, including Holcim, Heidelberg Materials, CEMEX, Vulcan Materials, and CRH Americas Materials, Inc., are focusing on maximizing the value of their current quarry portfolios and solidifying logistics and reserve strategies rather than aggressively expanding capacity. Their recent strategic moves highlight a commitment to efficiency improvements, cost leadership, and compliance readiness to reinforce long-term market strength.

LIST OF KEY CONSTRUCTION AGGREGATE COMPANIES PROFILED

- Holcim (Switzerland)

- Martin Marietta Materials (U.S.)

- Heidelberg Materials (Germany)

- CEMEX (Mexico)

- LSR group (Russia)

- Sika AG (Switzerland)

- Vulcan Materials (U.S.)

- UltraTech Cement Ltd. (India)

- CRH Americas Materials, Inc. (U.S.)

- SCG International Corporation (Thailand)

KEY INDUSTRY DEVELOPMENTS

- December 2025: CRH Americas Materials acquired North American Aggregates (NAA), expanding its aggregates business in New York and New Jersey and adding valuable waterfront aggregate reserves to its Tilcon NY operations.

- February 2024: Martin Marietta Materials announced the acquisition of 20 aggregates operations from Blue Water Industries across the U.S. Southeast, expanding its crushed stone and sand & gravel footprint and reinforcing long-term reserve availability.

- January 2023: Holcim completed the acquisition of 13 sand and aggregates quarries in the U.S. from Pioneer Landscape Centers, strengthening its aggregates reserve base and improving regional supply security across Colorado and Arizona.

- January 2023: CEMEX approved the acquisition of Atlantic Minerals Limited, securing a large-scale limestone quarry and marine aggregates supply to enhance its aggregates availability for North American construction markets.

- January 2022: Heidelberg Materials completed the acquisition of Corliss Resources in the U.S., adding significant sand-and-gravel capacity and strengthening its vertically integrated construction materials position in the Pacific Northwest.

- June 2021: Vulcan Materials Company announced the acquisition of U.S. Concrete, Inc., adding a large portfolio of aggregates operations, including crushed stone, sand, and gravel facilities, to strengthen its aggregates-led position in key metropolitan and coastal U.S. markets.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The construction aggregates market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.9%from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, End-Use Industry, and Region |

| By Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 599.44 billion in 2025 and is projected to reach USD 922.74 billion by 2034.

Recording a CAGR of 4.9%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

By end-use industry, the residential segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Sustained public infrastructure and construction activity drive aggregate consumption.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us