Cooler Box Market Size, Share & Industry Analysis, By Product Type (Reusable and Disposable), By Raw Material (Plastic, Metal, and Fabric), By End-Use (Household, Food & QSRs, Pharmaceutical, and Others), By Distribution Channel (Mass Retail, Specialty Retail, E-commerce, and B2B), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

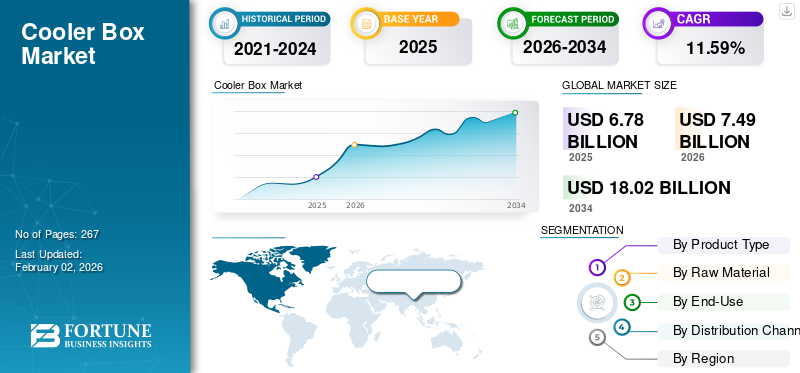

Cooler Box Market Size and Future Outlook

The global cooler box market size was valued at USD 6.78 billion in 2025 and is projected to grow from USD 7.49 billion in 2026 to USD 18.02 billion by 2034, exhibiting a CAGR of 11.59% during the forecast period. North America dominated the cooler box market with a market share of 41.43% in 2025.

Cooler boxes are portable insulated containers designed to keep the contents cold. Typical product features include insulation core type, shell material, capacity bands, lid seals/gaskets, drain plugs, and for powered models compressors/batteries and temperature control. They serve diverse applications including household recreation, outdoor sports and boating, foodservice and catering, last-mile cold food delivery, among others. Cooler boxes are mainly used for storing processed and fresh fruits, vegetables, dairy products and other perishable food. Manufacturers differentiate on hold-time performance, weight per litre, ruggedness, portability features, and added value such as integrated cool packs, USB ports, antibacterial liners.

Rising outdoor and mobile lifestyles, growth in food delivery and cold-chain logistics, and premiumisation/feature convergence (battery-powered portable fridges) drives market growth. Furthermore, sustainability pressures pushing alternatives to single-use Expanded Polystyrene (EPS) and tech advances that drop costs or improve hold times also contributes to the market growth. For example, expanded vaccine campaigns and decentralized healthcare needs during recent public-health efforts illustrated the importance of validated, high-performance portable coolers, driving procurement of VIP/XPS-lined or compressor-based medical carriers and accelerating uptake of higher-spec products in institutional channels.

Major players, including YETI, ORCA, RTIC., Igloo, and Coleman are some of the well-established brands in the market. Premiumisation & product innovation, channel mix optimization, along with regional and segment expansion such as institutional & cold-chain solutions are the major strategies adopted by these players in cooler box industry.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Mobile Lifestyles & Electrification to Boost Demand for Higher-Performance Coolers

Consumers and businesses are moving toward more mobile, outdoor and delivery-centric lives, thus shifting demand from simple to higher-performance coolers, often powered by premium solutions (12V/compressor units, battery packs, better insulation). As more people spend time outdoors, more on-the-go food delivery, last-mile cold logistics, and technological improvements (and falling costs) for portable refrigeration, have combined to make portability and active cooling drive the cooler box market growth.

- For instance, outdoor recreation participation in the U.S. reached 175.8 million in 2023, showing a large and growing pool of consumers who regularly need portable cooling for trips, boating, tailgates and camping.

MARKET RESTRAINTS:

Regulatory Pressure and Rising Compliance and Input-Costs to Restrict Market Expansion

The cooler-box market is increasingly constrained by environmental regulation and sustainability expectations (targeting single-use EPS and problematic plastics), tighter safety and transport rules for powered units (lithium batteries), and volatile input costs for key plastics and foams. Together these forces raise compliance and redesign costs, shrink the low-cost disposable segment, and slow replacement/purchase decisions as manufacturers pass higher costs to price-sensitive buyers all of which suppress near-term unit growth and margin expansion.

- For instance, several U.S. jurisdictions have banned or restricted EPS foodware and related products. In 2024, the New York Department of Environmental Conservation, amended a law to include a ban on certain expanded polystyrene foam containers that are used for cold storage. Moreover, Washington State and multiple other states have enacted portable-cooler or EPS restrictions that directly reduce demand for low-cost disposable coolers.

MARKET OPPORTUNITIES:

Electrified Portable Coolers for Mobile Last-Mile Delivery to Create Lucrative Growth Opportunities

The most promising growth opportunity for market is electrified portable coolers i.e., battery-assisted/12V/compressor-based refrigerators and hybrid systems that combine high-performance insulation with active cooling, integrated batteries, and telematics i.e. temp monitoring and fleet tracking. These products unlock new value by adding features such as reliable temperature control, longer hold times without ice, and integration into vehicle or fleet workflows. Electrified coolers also enable premium direct-to-consumer offers, such as attachments including solar chargers or swap-batteries and open institutional channels, including medical sample/vaccine transport, and mobile clinics where validated temperature control is required. Thus, developed modular batteries along with cooler platforms and selling to delivery fleets creates lucrative growth opportunities for product adoption.

COOLER BOX MARKET TRENDS:

Sustainability Shift Toward Recyclable/Bio-Based Materials is an Emerging Market Trend

Regulation and consumer pressure are forcing manufacturers to make a material shift across the market. Expanded-polystyrene (EPS) disposables are being phased out in many jurisdictions pushing manufacturers and distributors to adopt recyclable liners, biodegradable alternatives, or fully reusable designs. As an alternative, Expanded Polypropylene (EPP) are being preferred due to their superior impact resistance, resilience, BPA-free, non-toxic, and 100% recyclable features.

At the same time, both demand and supply-side signals favour greener products. The global sustainable-packaging solutions industry is large and growing, creating material-innovation and supply-chain opportunities for alternative cooler liners and recyclable assemblies. Consumers are also evidently willing to pay a huge amount for sustainable goods and many companies are ramping up sustainability investments. Together these forces constrain the low-cost disposable EPS segment and open higher-value opportunities, such as reusable hard and soft side coolers, recyclable/compostable single-use designs, and take-back or rental models.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Higher Lifetime Value, Premium Pricing and Sustainability Contributes to Larger Market Share of Reusable Product Types

On the basis of product type, the market is classified into reusable and disposable.

To know how our report can help streamline your business, Speak to Analyst

Reusable product type account for the largest cooler box market share share of revenue and is the fastest-growing segment. Reusable coolers carry higher ASPs and deliver lower cost-per-use over years so revenue concentrates in reusable even if disposables have high unit counts. This is reflected in market breakdowns showing two-thirds of revenue in reusable types. Moreover, medical cold-chain needs, food-delivery fleets and commercial catering increasingly require validated or powered solutions, pulling large B2B purchases into the reusable side. Moreover, EPS/disposable coolers face bans and restrictions in many jurisdictions (U.S. states, regions), accelerating the shift to reusable or recyclable alternatives reducing future disposable volumes and boosting demand for cooler boxes.

The disposable cooler is projected to expand at a CAGR of 10.72% over the projected years.

By Raw Material

Material Versatility, Cost-Efficiency, and Large-Scale Factors Contributes to Plastic Segment Growth

By raw materials, the market is categorized into plastic, metal, and fabric.

The plastic segment captured largest share of the market in 2026. In 2026, the segment is anticipated to dominate with a 64.55% share. Plastic combines the biggest installed base, the widest average selling price (ASP) span from economy to premium, and the most scalable, low-cost manufacturing and supply chain. The material delivers best cost-to-thermal-performance when paired with PU foam, are easy to mold into high-value designs or low-cost injection SKUs, and fit every channel from big-box to specialty DTC, thus they capture both unit volume and a large share of revenue.

The metal segment is expected to grow at a CAGR of 12.44% over the forecast period. Metal remains an attractive but much smaller premium/niche segment due to high ASP and lower unit volumes.

By End-Use

Homeowners Drive High-Volume Demand for Personalized Décor Leading to Segment Growth

Based on end-use, the market is segmented into household, food & QSRs, pharmaceutical, and others.

The Household segment will account for 58.97% market share in 2026 due to its vast consumer base, driven by everyday uses such as picnics, camping, tailgating, beach outings, and family storage needs. Its dominance comes from sheer scale i.e. billions of global households, high outdoor participation rates, and consistent replacement or upgrade cycles making it the largest contributor in both unit volumes and overall revenue compared to food & QSRs, pharmaceutical, or other specialized applications.

The pharmaceutical industry segment is projected to grow at a fastest rate as global healthcare systems expand vaccine programs, biologics, and temperature-sensitive drug distribution. Large-scale immunization campaigns, the rise of biologics requiring strict cold-chain handling, and investment in decentralized healthcare and clinical trials are accelerating demand for validated, high-performance cooler boxes.

By Distribution Channel

High-Value Bulk Orders and Specification-Driven Demand Supplements B2B/Contract Channel Growth

Based on distribution channel, the market is segmented into mass retail, specialty stores, e-commerce, and B2B sales.

In 2024, the global market was dominated by mass retail channels as supermarkets, hypermarkets, and big-box chains provide the broadest consumer access and stock the largest volume of economy and mid-range coolers. Their dominance is reinforced by impulse and seasonal buying and established supply chains that place coolers alongside camping, picnic, and household goods. For instance, Coleman and Igloo coolers are widely distributed through Walmart, Target, and Costco in the U.S., enabling massive unit turnover. Furthermore, the segment is set to hold a 47.36% share in 2025.

In addition, e-commerce is the fastest-growing channel and is projected to grow at a CAGR of 12.63% during the study period.

Cooler Box Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Cooler Box Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 2.81 billion to the global market in 2025, accounting for 41.43% share, and is expected to reach USD 3.11 billion in 2026. The factors fostering the dominance of the region include deeply ingrained outdoor and adventures activities, such as camping, tailgating, boating, road trips, high disposable income, and the dominance of premium brands such as YETI, Coleman, and Igloo. The region is home market for most leading cooler brands, which leverage strong direct-to-consumer channels and specialty/outdoor retail networks, further cementing the region’s market leadership. In 2025, U.S. market is estimated to reach USD 2.36 billion.

Europe

In 2025, the Europe market stood at USD 1.84 billion, representing 27.12% of global demand, and is projected to grow to USD 2.01 billion in 2026. Other regions such as Europe and Asia Pacific are anticipated to witness a notable growth in the coming years. During the forecast period, European region is projected to record the growth rate of 10.12%, which is the second highest amongst all the regions and touch the valuation of USD 1.68 billion in 2025. Growth is supported by strong outdoor tourism, including camping, caravanning, and marine activities, a mature specialty retail network, and early adoption of eco-friendly materials. Backed by these factors, countries including U.K. anticipates to record the valuation of USD 0.38 billion, Germany to record USD 0.43 billion in 2026, and France to record USD 0.32 billion in 2025. After Europe, the market in Asia Pacific is estimated to reach USD 1.53 billion in 2025 and secure the position of third-largest region in the market. In the region, India and China both are estimated to reach USD 0.31 and 0.84 billion each in 2026. Asia Pacific is a high-potential region with rising household disposable incomes and growing participation in outdoor and leisure activities. Expanding food delivery services and rapid cold-chain infrastructure growth fuel strong commercial demand.

Asia Pacific

The Asia Pacific region captured 22.54% of the global market in 2025, generating USD 1.53 billion in revenue, and is projected to reach USD 1.71 billion in 2026.

In 2025, Middle East & Africa generated USD 0.18 billion, contributing 2.68% to global market revenue, and is projected to grow to USD 0.2 billion in 2026.

South America

South America contributed 6.23% to the global market in 2025, with a valuation of USD 0.42 billion, and is projected to reach USD 0.46 billion in 2026. Rising quick-service restaurant (QSR) expansion adds momentum for commercial cooler use, while outdoor culture and beach tourism drive household demand. In Middle East & Africa, UAE is set to attain the value of USD 0.05 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Competitive Landscape Shaped by Premiumization, Channel Mix, And Innovation

The cooler-box market is moderately fragmented, with global players such as YETI, Dometic/Igloo, Coleman, Pelican, and RTIC competing alongside regional and niche players. Manufacturers are differentiating through premiumization (roto-moulded, powered coolers), channel strategies (direct-to-consumer, e-commerce, and mass retail partnerships), and product innovation (battery-powered, lightweight, and eco-friendly designs). Sustainability is becoming a key focus, with firms phasing out EPS-based disposables in response to regulations. Companies also leverage brand storytelling, collaborations, and lifestyle marketing to strengthen consumer loyalty. Overall, the competitive strategy blends technology upgrades, sustainability, and diversified distribution to capture both mass-market volumes and premium margins.

Apart from this, few other prominent players in the market include Engel, Grizzly, Bison Coolers, IceMule, and Alpicool.

LIST OF KEY COOLER BOX COMPANIES PROFILED:

- YETI Holdings, Inc. (U.S.)

- Dometic Group AB (owns Igloo) (Sweden)

- Igloo Products Corp. (U.S.)

- Coleman (Newell Brands Inc.) (U.S.)

- Pelican Products, Inc. (U.S.)

- RTIC Outdoors (U.S.)

- Engel Coolers (Engel USA, Ltd.) (U.S.)

- IceMule Coolers (U.S.)

- Grizzly Coolers LLC (U.S.)

- Bison Coolers (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: KPS Global has strengthened its U.S. manufacturing footprint by acquiring SRC Refrigeration, a Michigan-based manufacturer of walk-in coolers and freezers. With this move, KPS adds a Midwest facility and gains SRC’s XPS (extruded polystyrene) panel manufacturing capability, expanding both product portfolio and regional reach. The deal also ensures minimal customer overlap, enabling continuity for existing clients while leveraging synergies in custom cold-storage solutions.

- February 2024: Kinzie Capital Partners acquired Arctic Industries, a U.S. manufacturer and distributor of temperature-control and cold-storage solutions, in partnership with Arctic’s management team. This acquisition enables Kinzie to position Arctic as a national prominent player in cold-storage, expanding its product reach, and leverage complementary strength in cooling and logistics infrastructure for further growth.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2026 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.59% from 2026-2034 |

| Unit | Value (USD Billion) |

| By Product Type |

|

| By Raw Material |

|

| By End-Use |

|

| By Distribution Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.49 billion in 2026 and is projected to reach USD 18.02 billion by 2034.

In 2025, the market value stood at USD 1.53 billion.

The market is expected to exhibit a CAGR of 11.59% during the forecast period of 2026-2034.

The reusable segment led the market by product type.

The key factors driving the market are rising outdoor and mobile lifestyles, growth in food delivery and cold-chain logistics, and premiumisation/feature convergence.

YETI, RTIC., Igloo, and Coleman are some of the prominent players in the market.

North America dominated the market in 2025.

Innovation in product such as electrified portable coolers which are battery-assisted / 12V / compressor-based refrigerators and hybrid systems that combine high-performance insulation with active cooling are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 267

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us