Credit Default Swap (CDS) Market Size, Share & Industry Analysis, By Type (Single-Name CDS, Index CDS, Basket and Structured CDS), By Entity Type (Corporate CDS, Sovereign CDS, Financial Institution CDS), By End User (Banks and Dealers, Hedge Funds, Asset Managers and Insurance Firms), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

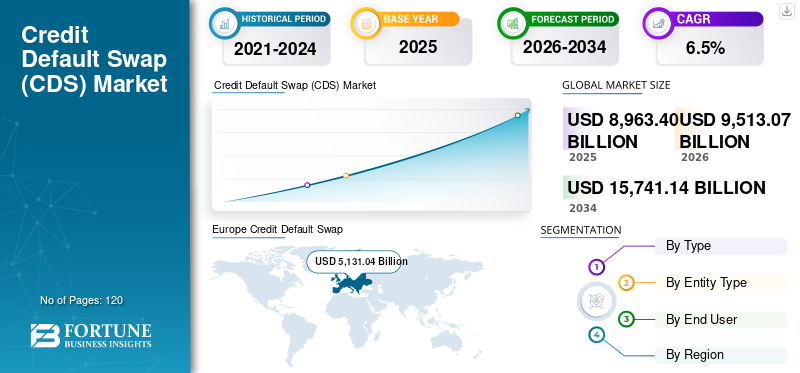

The global credit default swap (CDS) market size was valued at USD 8,963.40 billion in 2025. The market is projected to grow from USD 9,513.07 billion in 2026 to USD 15,741.14 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period. Europe dominated the global credit default swap (CDS) market with a market share of 57.24% in 2025.

The Credit Default Swap (CDS) market is gaining stronger momentum as investors, banks, and institutional portfolios increasingly focus on protecting themselves against credit deterioration and sudden changes in default risk. As global credit markets face frequent fluctuations due to interest-rate cycles, corporate leverage, refinancing pressure, and geopolitical uncertainty, CDS instruments are being used more actively to hedge bond exposures, manage portfolio risk, and express credit views without directly trading the underlying debt. This rising emphasis on credit-risk management is strengthening demand for both single-name and index CDS contracts.

- For instance, during periods of heightened fiscal or macro uncertainty, CDS activity typically increases as market participants look for immediate protection. A widely observed example is the sharp increase in sovereign and corporate CDS spreads during event-driven credit stress periods such as government debt-ceiling debates, banking sector concerns, or recession expectations.

Furthermore, major market participants such as JPMorgan Chase, Goldman Sachs, Morgan Stanley, Citi, Barclays, Deutsche Bank, and BNP Paribas continue to strengthen their CDS trading, clearing, and credit risk-management capabilities to meet rising institutional demand. Alongside these dealers, hedge funds and asset managers are expanding their CDS use for relative-value strategies, portfolio hedging, and credit-spread positioning, supported by improved market infrastructure such as central clearing, standardized contracts, and post-trade reporting systems.

Download Free sample to learn more about this report.

Credit Default Swap (CDS) Market Takeaways

- 2025 Market Size: USD 8,963.40 billion

- 2026 Market Size: USD 9,513.07 billion

- 2034 Forecast Market Size: USD 15,741.14 billion

- CAGR: 6.5% from 2026–2034

- Europe dominated the credit default swap (CDS) market with a 57.24% share in 2025.

- The Index CDS segment is projected to grow at a CAGR of 7.4% during the forecast period.

- The Financial Institution CDS segment is expected to expand at a CAGR of 8.0% through 2034.

North America

North America recorded a market value of USD 2,457.34 billion in 2025 and is projected to grow at a CAGR of 6.3%.

Europe

Europe maintained its leading position, reaching USD 5,131.04 billion in 2025.

Asia Pacific

Asia Pacific reached USD 994.85 billion in 2025, making it the third-largest regional market.

U.S.

The market was valued at USD 2,127.86 billion in 2025, accounting for approximately 24.0% of global CDS revenues.

Japan

The market reached USD 277.26 billion in 2025, representing roughly 3.0% of global CDS revenues.

Read More

CREDIT DEFAULT SWAP (CDS) MARKET TRENDS

Increasing Shift Toward Central Clearing is a Prominent Trend Observed in Market

Central clearing enhances transparency by improving trade reporting and making pricing and volume information more structured for regulators and institutional users. It streamlines post-trade processing through standardized documentation and lifecycle management, reducing operational disputes and settlement delays. As more buy-side firms adopt CDS for hedging and portfolio strategies, clearing offers a more efficient and compliant route for participation. Over the long term, the growth of clearing is expected to support higher institutional confidence, greater liquidity in index CDS, and more scalable risk transfer across global credit markets.

- For instance, in September 2024, ICE Clear Credit announced that it processed a record of more than USD 1.1 trillion in CDS notional in a single day, marking the highest one-day CDS clearing volume recorded by any CDS clearinghouse.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Credit-Risk Uncertainty and Spread Volatility is Accelerating Market Growth

When interest-rate expectations, inflation pressures, and economic outlooks change quickly, corporate and sovereign credit spreads tend to reprice sharply, exposing investors to sudden mark-to-market losses. In such conditions, CDS becomes a preferred hedging tool as it allows institutions to reduce credit exposure without selling the underlying bonds, which may be illiquid or costly to exit. Higher spread volatility also encourages more tactical trading activity, as market participants use CDS to express short-term credit views or protect portfolios during macro events. This is bolstering the credit default swap (CDS) market growth.

- For instance, in May 2025, Reuters reported that policy uncertainty and renewed concerns around U.S. fiscal risks drove a surge in demand for CDS on the U.S. government debt. The article noted that U.S. sovereign CDS spreads widened to their highest levels since the 2023 debt ceiling episode, and it also highlighted that both the size of the market and trading volumes had increased recently, reflecting stronger hedging demand during macro uncertainty.

MARKET RESTRAINTS

Regulatory Burden and Higher Compliance Costs Restricting Market Growth

Regulatory burden and higher compliance costs are restricting CDS market growth as trading and holding CDS positions now require significantly stronger capital, collateral, and reporting discipline than in earlier years. Central clearing mandates for standardized CDS contracts increase margin posting requirements, while non-cleared trades are subject to bilateral margin rules that can tie up liquidity and raise the cost of participation. In addition, detailed trade reporting obligations and ongoing regulatory surveillance add operational workload and technology investment needs for both dealers and buy-side firms. Higher capital charges for certain derivative exposures also reduce the appetite of banks and dealers to intermediate large CDS positions, which can limit liquidity in parts of the market.

These costs are especially challenging for smaller institutions, reducing overall participant diversity and slowing adoption beyond the largest global players. As a result, while CDS remains an important hedging tool, regulatory-driven cost pressures can constrain market expansion and limit growth.

MARKET OPPORTUNITIES

Shifting Focus Toward Electronification and Automation in Credit Derivatives Trading to Offer Market Growth Opportunities

As more CDS transactions move to electronic platforms, participants gain easier access to liquidity, tighter bid-ask spreads, and more consistent pricing across dealers. Automated workflow tools also reduce manual processing in trade confirmation, compression, clearing submission, and lifecycle servicing, lowering operational risk and settlement delays. This is especially important for buy-side firms, as streamlined electronic execution makes it simpler to scale hedging strategies and manage portfolios during volatile credit cycles. Increased electronification further supports regulatory requirements by improving audit trails, trade reporting quality, and transparency for market oversight.

- For instance, in March 2025, ISDA’s SwapsInfo announced the expansion of its derivatives trading database to include European CDS trading activity, creating a more comprehensive view of credit derivatives trading in the European Union, U.K., and U.S. This development supports the broader trend toward better electronic trade data visibility and more structured market transparency, which strengthens adoption of automated and electronic workflows.

Segmentation Analysis

By Type

Rising Shift Toward Central Clearing and Electronic Trading to Propel Index CDS Segment Growth

Based on the type, the market is divided into Single-Name CDS, Index CDS, and Basket and Structured CDS.

The Index CDS segment accounted for the largest credit default swap (CDS) market share and is anticipated to rise with a CAGR of 7.4% over the forecast period as it offers the most liquid and standardized way to hedge broad credit exposure. Investors prefer index CDS as it enables fast portfolio-level protection with tighter spreads and easier execution compared to many single-name contracts.

The growing shift toward central clearing and electronic trading further strengthens index CDS adoption by improving transparency and reducing counterparty and operational risks. In addition, index products are widely used during volatile credit cycles, supporting recurring demand from banks, asset managers, and hedge funds. These factors together support stronger growth momentum for index CDS over the forecast period.

By Entity Type

Rising Usage of Corporate CDS to Hedge Against Default Risk Boosted Segmental Growth

Based on entity type, the market is segmented into Corporate CDS, Sovereign CDS, and Financial Institution CDS.

In 2025, the Corporate CDS dominated the global market. The Institutional investors, banks, and asset managers actively use corporate CDS to hedge against default risk, downgrade risk, and spread widening across investment-grade and high-yield issuers. Corporate CDS also benefits from the strong liquidity of well-followed corporate names and the ability to apply hedges quickly without restructuring underlying bond holdings. In addition, corporate credit is highly sensitive to interest-rate changes and refinancing conditions, which increases hedging demand during volatile periods. The broad range of corporate issuers across sectors further expands the addressable market, strengthening corporate CDS usage across global regions.

The financial Institution CDS segment is projected to grow at a CAGR of 8.0% over the forecast period. Banks and financial institutions are closely interconnected with capital markets, which increases demand for protection during periods of systemic uncertainty.

By End User

To know how our report can help streamline your business, Speak to Analyst

Rising Adoption of Credit Default Swap (CDS) in Banks and Dealers Propelled Segment Growth

Based on the end user, the market is segmented into banks and dealers, hedge funds, and asset managers and insurance firms.

The banks and dealers segment dominated market share in 2025, owing to their central role as market makers and liquidity providers across both single-name and index CDS contracts. These institutions intermediate the majority of CDS flows, manage large trading books, and support price discovery through continuous quoting and risk warehousing. Their dominance is further reinforced by their direct access to clearing infrastructure, advanced risk management capabilities, and the ability to structure customized hedging solutions for institutional clients.

Hedge funds are projected to grow at a CAGR of 9.4% over the forecast period as they increasingly use CDS for relative-value trading, macro hedging, and credit-spread positioning strategies.

Credit Default Swap (CDS) Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Credit Default Swap (CDS) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant share in 2024, valued at USD 4,882.05 billion, and also maintained the leading share in 2025, with USD 5,131.04 billion. The EU market growth is owing to a large corporate bond and sovereign debt base, which creates sustained demand for credit-risk hedging across investment-grade, high-yield, and government exposures. A strong presence of global banks and dealer networks supports active CDS trading and liquidity, particularly in widely used index products linked to European credit.

U.K Credit Default Swap (CDS) Market

The U.K. market in 2025 reached a valuation of around USD 3,387.67 billion, representing roughly 38.0% of global Credit Default Swap (CDS) revenues.

Germany Credit Default Swap (CDS) Market

Germany’s market reached a valuation of approximately USD 450.74 billion in 2025, equivalent to around 5.0% of global Credit Default Swap (CDS) sales.

North America

North America is projected to record a growth rate of 6.3% in the coming years and reached a valuation of USD 2,457.34 billion in 2025. The North America market growth is driven by the region’s deep and highly liquid credit markets, where institutional investors and banks actively use CDS to hedge corporate and financial-sector exposure. Strong participation from major dealer banks and market makers supports efficient pricing and consistent liquidity, encouraging wider usage of both single-name and index CDS contracts.

U.S Credit Default Swap (CDS) Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market reached a valuation of around USD 2,127.86 billion in 2025, accounting for roughly 24.0% of global Credit Default Swap (CDS) sales.

Asia Pacific

Asia Pacific reached a valuation of USD 994.85 billion in 2025 and secured the position of the third-largest region in the market. In the region, India and China reached a valuation of USD 103.16 billion and USD 220.40 billion, respectively, in 2025.

Japan Credit Default Swap (CDS) Market

The Japan market in 2025 reached a valuation of around USD 277.26 billion, accounting for roughly 3.0% of global Credit Default Swap (CDS) revenues. This growth is attributed to the country’s mature bond market and the increasing need among institutional investors to manage credit exposure efficiently during shifting interest-rate and macroeconomic conditions. As Japanese banks, insurers, and asset managers hold large fixed-income portfolios, CDS provides a flexible tool to hedge against potential spread widening and issuer-specific credit deterioration without liquidating bond positions.

China Credit Default Swap (CDS) Market

China’s market is projected to be one of the largest globally, with 2025 revenues estimated at around USD 220.40 billion, representing roughly 2% of global Credit Default Swap (CDS) sales.

India Credit Default Swap (CDS) Market

The India market in 2025 reached a valuation of USD 103.16 billion, accounting for roughly 1% of global Credit Default Swap (CDS) revenues.

South America and Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The South America market reached a valuation of USD 105.84 billion in 2025. The growth of South America and the Middle East & Africa is owing to the gradual deepening of sovereign and corporate debt markets, which increases the need for tools that help investors manage default risk and spread volatility. In the Middle East & Africa, the GCC reached a valuation of USD 124.93 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Expansion of Index-based and Cleared CDS Offerings by Key Players to Propel Market Progress

A key strategy adopted by leading CDS players is expanding index-based and cleared CDS offerings to improve scalability, liquidity access, and capital efficiency for clients. Major dealer banks and platforms are prioritizing central clearing participation, portfolio compression services, and standardized contract structures to reduce counterparty risk and lower operational friction. At the same time, they are investing in electronic execution and automated post-trade workflows to provide faster pricing, tighter spreads, and improved transparency.

- For instance, in March 2025, ISDA expanded its SwapsInfo derivatives database to include European CDS trading activity, adding European Union and U.K. index and single-name traded notional and trade counts. This development reflects the broader shift toward structured transparency and standardized trade data.

Many players also strengthen risk analytics and client advisory capabilities to support hedging needs during volatile credit cycles, which helps deepen long-term client engagement.

LIST OF KEY CREDIT DEFAULT SWAP COMPANIES PROFILED

- JPMorgan Chase & Co. (U.S.)

- Goldman Sachs Group (U.S.)

- Morgan Stanley (U.S.)

- Citigroup (U.S.)

- Bank of America (U.S.)

- Barclays (U.K.)

- Deutsche Bank (Germany)

- BNP Paribas (France)

- UBS (Switzerland)

- HSBC (U.K.)

- Credit Suisse (legacy positions integrated into UBS) (Switzerland)

- Société Générale (France)

- Nomura (Japan)

- Wells Fargo (U.S.)

- Standard Chartered (U.K.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: FICO partnered with Plaid to deliver the next generation of the cash flow UltraFICO Score. This innovative solution will combine the proven reliability of the FICO Score, used by 90% of top US lenders, with real-time cash-flow data from Plaid to provide lenders with a single, enhanced credit score.

- October 2025: Barclays announced the signing of a new multi-year strategic agreement with SIX, the global financial data and market infrastructure provider. The multi-year collaboration will help in spanning investment banking, retail banking, wealth management, and corporate services.

- September 2025: Experian announced that Oakbrook, a non-bank provider of consumer lending solutions, will use Experian Boost data in its process for personal loan applications. This partnership will increase access to credit for customers who traditionally may not have been eligible.

- May 2025: UBS Group AG and General Atlantic partnered to focus on private credit opportunities. The collaboration between UBS and General Atlantic Credit (GA Credit) aims to enhance investing clients’ and borrowers’ access to a broader set of direct lending and other credit products.

- January 2024: CME Group announced that its enhanced cross-margining arrangement has gone live. This will enable capital efficiencies for clearing members that trade and clear both U.S. Treasury securities and CME Group Interest Rate futures.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.5% from 2025-2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, By Entity Type, By End User, and Region |

|

By Type |

· Single-Name CDS · Index CDS · Basket and Structured CDS |

|

By Entity Type |

· Corporate CDS · Sovereign CDS · Financial Institution CDS |

|

By End User |

· Banks and Dealers · Hedge Funds · Asset Managers and Insurance Firms |

|

By Region |

· North America (By Type, By Entity Type, By End User, and Country) o U.S. o Canada o Mexico · Europe (By Type, By Entity Type, By End User, and Country) o Germany o U.K. o France o Spain o Italy o Russia o Benelux o Nordics o Rest of Europe · Asia Pacific (By Type, By Entity Type, By End User, and Country) o China o Japan o India o South Korea o ASEAN o Oceania o Rest of Asia Pacific · South America (By Type, By Entity Type, By End User, and Country) o Brazil o Argentina o Rest of South America · Middle East & Africa (By Type, By Entity Type, By End User, and Country) o Turkey o Israel o GCC o South Africa o North Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8,963.40 billion in 2025 and is projected to reach USD 15,741.14 billion by 2034.

In 2025, the market value stood at USD 2,457.34 billion.

The market is expected to exhibit a CAGR of 6.5% during the forecast period of 2026-2032.

By type, the index CDS segment is expected to lead the market.

Rising credit-risk uncertainty and spread volatility is accelerating market growth.

JPMorgan Chase & Co., Goldman Sachs Group, Morgan Stanley, and Citigroup are the major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us