Dark Soy Sauce Market Size, Share & Industry Analysis, By Process (Brewed and Blended), By End-Use (Processed Foods, Prepared Foods, and Households), By Distribution Channel (Supermarkets, Hypermarkets, Convenience Stores, Online Retail, HoReCa, and QSR), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

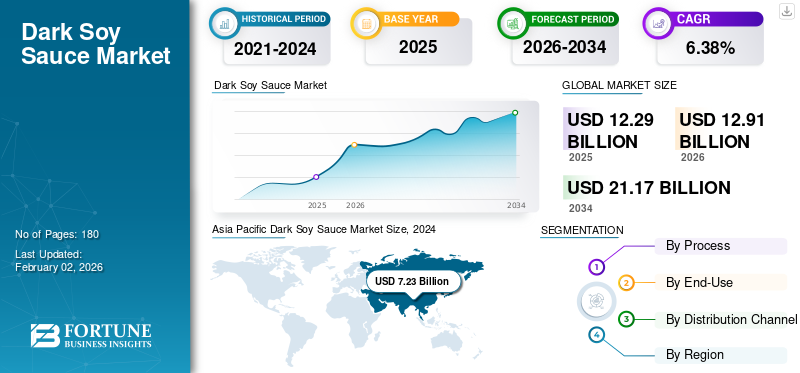

The global dark soy sauce market size was valued at USD 12.29 billion in 2025 and is projected to grow from USD 12.91 billion in 2026 to USD 21.17

billion by 2034, exhibiting a CAGR of 6.38% during the forecast period. Asia Pacific dominated the dark soy sauce market with a market share of 28.85% in 2025.

Some key players in the industry include Lee Kum Kee, Foshan Haitian Flavoring & Food Co., and YAMASA Corporation, among others.

Dark soy sauce, also called black sauce, is a darker, thicker type of sauce extracted from soybeans. This sauce is primarily used in Chinese cuisine and is mainly added at the end of cooking to improve flavor and color. Similarly, light sauce, dark sauce comprise wheat, salt, and numerous other ingredients, but they undergo a longer fermentation process. Compared to other sauces, this black sauce is sweeter, has a hint of malt flavor, and is less salty. Globally, this sauce is famous in Asian countries, specifically China, Japan, and South Korea, among others.

The surging popularity of traditional Chinese cuisines and increasing home cooking trend bolsters the global market growth.

Download Free sample to learn more about this report.

Dark Soy Sauce Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 12.29 billion

- 2026 Market Size: USD 12.91 billion

- 2034 Forecast Market Size: USD 21.17 billion

- CAGR: 6.38% from 2026–2034

Market Share & Segmentation:

- Asia Pacific dominated the dark soy sauce market with a 28.85% share in 2025, driven by its cultural significance as a staple ingredient in traditional cuisines, the expansion of the foodservice industry, and rising consumer health consciousness.

- By process, the brewed segment held the largest market share, valued for its unique, complex flavor profile derived from a long fermentation process and its associated health benefits, such as boosting digestive health.

- By distribution channel, the HoReCa (Hotels, Restaurants, Catering) segment led the market, fueled by the growing popularity of Asian cuisine in restaurants and the cost-effectiveness of purchasing the sauce in bulk for culinary use.

Key Regional Highlights:

- Asia Pacific: Leads the global market, with China being the top consumer. The region's growth is supported by strong cultural culinary traditions and continuous product innovation.

- North America: The fastest-growing region, driven by the expanding presence of Asian food chains, consumer willingness to explore unique flavors, and high demand for convenient packaged sauces.

- Europe: The third-largest market, with growth attributed to the rising preference for plant-based condiments and innovations in organic and gluten-free sauce variants to meet specific dietary needs.

- South America: An emerging market with high growth potential, supported by increasing local soybean production and rising disposable income.

MARKET DYNAMICS

Market Drivers

Rising Inclination toward Asian Cuisines Strengthens the Use of Sauce

The growing inclination toward Asian dishes is a pivotal driver in improving sauce usage. As most individuals experiment with Asian dishes, the need for sauce, especially soybean-sourced, a main ingredient, also soars. This trend is highly evident in Asian countries such as China, Vietnam, and Indonesia, where it is recognized as a staple ingredient. Along with this, its popularity is rising in North America and European regions as the majority of consumers are seeking Asian dishes offering diversified flavors. Predominantly, the umami flavor and versatility of the sauce are the key reasons behind the market expansion. Thus, this increasing demand for Asian dishes enables growth opportunities for the sauce market.

Market Restraints

Variations in Raw Material Prices and Intense Competition Affect Market Growth

One of the crucial obstacles sauce producers face is the surging fluctuations in raw material prices. Factors such as trade restrictions, supply chain disruptions, and variations in climatic conditions are the key components responsible for increased costs, ultimately affecting manufacturing costs. Moreover, natural disasters and geopolitical events can hamper the supply chain for numerous raw ingredients, leading to high prices of finished products. As a result, such factors impede the global market share.

Robust market competition is another hurdle that inhibits the dark soy sauce market growth. The sauce market faces stiff competition from both emerging and established players. This situation requires producers to differentiate their finished items and satisfy diverse consumer requirements.

Market Opportunities

Technological Advancements in Production of Sauces Unlock Growth Possibilities

Technological advancements in the soy sauce production process are known to provide lucrative growth opportunities. One main technology used for sauce is low-salt fermentation and high-temperature fermentation. This technique utilizes starter culture at a higher fermentation temperature (40-55°C), which boosts production and minimizes cost. Moreover, genetic engineering is becoming popular, and techniques such as mutagenesis and genome shuffling are being explored to optimize microbial strains for sauces. Additionally, bioreactor technology and the use of large-scale fermentation tanks can be used to produce high-quality products.

Dark Soy Sauce Market Trends

Surging Demand for Gluten-Free Sauces is the Current Trend

The global sauce market is witnessing a robust trend toward gluten-free sauces. These sauces are gaining huge traction in household and foodservice sectors as health-centric individuals seek allergen-free alternatives. Also, compared to conventional sauces, gluten-free sauce provides numerous health advantages and suits consumers following a healthy lifestyle. Similarly, traditional, gluten-free soy sauce has a refined flavor and can be purchased from retailers. Thus, this trend opens chances for food innovation, with producers launching a wide range of gluten-free variants.

SEGMENTATION ANALYSIS

By Process

Brewed Segment Led the Market Owing to its Health Advantages

On the basis of process, the market is bifurcated into brewed and blended.

Out of all, the brewed sector dominated the market and generated the largest share. Brewed soy sauce, also referred to as naturally brewed sauce, provide a unique and complex flavor profile owing to the long fermentation process. Moreover, this sauce offers numerous health advantages, such as boosting the immune system and enhancing digestive health.

Blended emerged as the fastest-growing segment and is anticipated to soar at a higher pace in the future. This sauce is economical in nature and can be produced at a faster pace, which adds value to the growth.

By End-Use

Prepared Foods Dominate the Market Owing to Increased Dining-Out Culture

Depending on end-use, the market is distributed into processed foods, prepared foods, and households.

Amongst all, the prepared foods sector leads in the global market, and is backed by convenience. Prepared food is a fully or partially prepared meal that requires minimal preparation before consumption. To enhance the flavor of culinary preparation, soy sauce can be used in stir-fried dishes, sushi, and barbecued meats.

The household sector is predicted to hold the highest CAGR during the forecast period. The trend of consuming home-cooked meals and the increasing availability of sauces via retailers will likely facilitate the industry’s growth.

By Distribution Channel

HoReCa Segment Leads Due to Increasing Popularity of Asian Cuisine

Based on distribution channel, the market is segmented into supermarkets, hypermarkets, convenience stores, online retail, HoReCa, and QSR.

The HoReCa category led the market and is projected to soar at the same pace in the near term. In this sector, this sauce is used as a dip, marinade, or as an ingredient in dressings and sauces. Restaurants can easily purchase this sauce in bulk quantities, which can be affordable compared to others. Moreover, the augmented demand for Asian cuisine and the growing socializing culture leads to rising utilization of sauce from culinary establishments.

The online retail channel is the fastest-growing segment and is expected to bolster at a higher pace in the future. The vast availability of sauces through local/international brands and easy return/exchange options collectively propels the segment’s growth.

Dark Soy Sauce Market Regional Outlook

Based on regions, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Dark Soy Sauce Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific led the global market and held a notable dark soy sauce market share in 2024. This region is considered a pivotal market for dark sauce and is driven by cultural significance and expansion of the foodservice industry. The majority of Asian individuals rely on Asian dishes such as noodles, ramen, and sushi, which use soy sauce in larger amounts. Moreover, the growing health consciousness influences food producers to introduce new sauce variants such as low-salt and gluten-free. Additionally, the increasing retailers of sauces and surging demand for premium sauces further bolster the regional growth. The Asia Pacific market accounted for USD 7.23 billion in 2025, representing 28.85% of the global industry, and is expected to reach USD 7.6 billion in 2026.

Amongst all Asian countries, China secured the foremost position, owing to surging demand for packaged ingredients and established production infrastructure.

Download Free sample to learn more about this report.

North America

North America is the fastest-growing region in the global market. In this region, the expanding presence of Chinese and Japanese food chains or restaurants supports the demand for sauces for takeaway and on-site use. Moreover, there is an augmented demand for easy-to-use packaged sauces that can be easily carried and used in several food items. Furthermore, the rising incidences of cardiovascular diseases and high blood pressure increase the need for sodium-free condiments. As a result, such factors improve the North American market expansion.North America maintained a strong presence in the global market, reaching USD 2.55 billion in 2025, accounting for 33.93% share, and is expected to reach USD 2.69 billion in 2026.

The U.S. dominated the global market and is expected to soar faster in the coming years. The growing consumers’ willingness to explore unique flavors and robust e-commerce channels drives the nation’s growth.

Europe

Europe is recognized as the third leading region, and this growth can be attributed to the surging inclination toward plant-based condiments and innovation in sauce variants. Compared to other regions, European countries are always seeking natural and plant-based sauces, free from synthetic ingredients. Moreover, the rising number of celiac patients in the region necessitates food producers to launch gluten-free sauces. Additionally, the growing demand for organic sauces further fuels the production and usage of dark soy sauce. In 2025, Europe generated USD 1.7 billion, contributing 30.99% to global market revenue, and is projected to grow to USD 1.78 billion in 2026.

Latin America

South America is still at its nascent stage and is expected to grow at a higher pace during the forecast period. The increasing soybean production and surging disposable income can improve the regional growing potential. Latin America contributed 33.57% to the global market in 2025, with a valuation of USD 0.44 billion, and is projected to reach USD 0.45 billion in 2026.

Middle East & Africa

The Middle East & Africa is at its developing stage and is predicted to maintain the same pace in the near term. The rising usage of sauces in culinary preparation and improved inclination toward halal soy sauces will likely strengthen the growth. In 2025, Middle East & Africa represented USD 0.37 billion, accounting for 35.18% of the worldwide market, and is projected to grow to USD 0.38 billion in 2026.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Active Players are Focusing on Product Launches to Enhance Consumer Attention

The dominating players in the global industry are Lee Kum Kee, Kikkoman Corporation, Masan Group, Jiajia Food Group Co., Ltd., and others. All these players are aiming toward new product launches which aids in attracting new customers. Moreover, such launches strengthen brand awareness and help gain a competitive advantage globally.

List of Key Dark Soy Sauce Companies Profiled

- Lee Kum Kee (China)

- Kikkoman Corporation (Japan)

- Marunaka Shoyu (Japan)

- The Kraft Heinz Company (U.S.)

- Shoda Shoyu Co., Ltd. (Japan)

- Jiajia Food Group Co., Ltd. (China)

- Mc Cormick & Company Inc. (U.S.)

- Koon Chun Sauce Factory Hong Kong (China)

- Foshan Haitian Flavouring & Food Co. Ltd. (China)

- YAMASA Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2024: Kikkoman Corporation, a Japanese condiments manufacturer, released its first-ever range of dark soy sauce, especially for Indian consumers. This sauce offers flavor and color to dishes, specifically targeting Asian restaurants.

- January 2024: Thean Heong Sauce Industry Bhd, a Malaysian sauce brand, launched a range of premium ethnic sauces which comprises Superfood Dark, Superfood Chilli, Superfood Tomato Sauce, and others. These sauces are made of natural ingredients and are free from artificial preservatives.

- July 2023: Kikkoman Corporation, a renowned sauce producer in Japan, unveiled its new campaign, “Adding Kikkoman for Tastier Chinese Food,” which aims at promoting the use of sauce, including both dark and light soy sauce, in Chinese cuisine across India.

- July 2020: Surya Foods, a U.K.-based bulk and wholesale supplier of sauces, announced the launch of soy sauce through its brand, “Thai Dragon.” The sauces launched include dark and light soy sauce for consumers in the U.K.

REPORT COVERAGE

The global dark soy sauce market report includes quantitative and qualitative insights into the market. It also offers a detailed market analysis of the market size and growth rate for all possible market segments. Key insights presented in the report include an overview of related markets, a competitive landscape, recent industry developments such as mergers & acquisitions, the regulatory environment in critical countries, and current market trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 6.38%% from 2026-2034 |

|

Segmentation |

By Process

|

|

By End-Use

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 12.29 billion in 2025.

The market is expected to grow at a CAGR of 6.38% during the forecast period.

By end use, the prepared foods segment led the market.

Rising inclination toward Asian cuisines strengthens the use of sauce, driving market growth.

Kikkoman Corporation, Lee Kum Kee, and Jiajia Food Group Co., Ltd. are a few of the key players in the market.

Asia Pacific held the highest share of the market.

Technological advancements in the production of sauces is a growth opportunity.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us