Data Centers Liquid Immersion Cooling Market Size, Share & Industry Analysis, By Cooling Type (Single-Phase and Two-Phase) By Equipment Type (Immersion Cooling Tanks, Coolant, Distribution Units (CDUs), Heat Exchangers, Pumps & Fluid Circulation Systems and Monitoring & Control Systems), By Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers and Edge Data Centers) By Application (High-Performance Computing, Artificial Intelligence & Machine Learning, Cloud Computing Infrastructure, & Others), and Regional Forecast, 2026-2034

Data Centers Liquid Immersion Cooling Market Size and Future Outlook

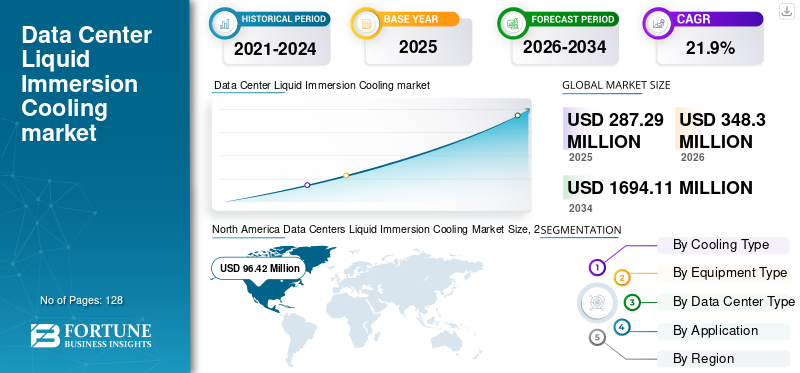

The data centers liquid immersion cooling market size was valued at USD 287.29 million in 2025. The market is projected to grow from USD 348.30 million in 2026 to USD 1,694.11 million by 2034, exhibiting a CAGR of 21.9% during the forecast period. North America dominated the data centers' liquid immersion cooling market with a market share of 33.56% in 2025.

Liquid immersion cooling equipment refers to advanced thermal management and liquid cooling systems designed to submerge IT hardware, including servers, GPUs and high-performance computing units, directly into thermally conductive dielectric fluid to dissipate heat efficiently. These systems are critical for supporting next-generation global data center infrastructure across hyperscale data centers, colocation facilities, enterprise environments and edge data centers, where rising compute densities, expanding Artificial Intelligence (AI) workloads, and growing demand for energy efficient data centers cooling directly influence performance and operational costs. Compared to conventional air cooling, immersion-based liquid cooling solutions enable higher thermal transfer efficiency, reduced energy consumption, improved Power Usage Effectiveness (PUE) and optimized high density computing within compact data center footprints. As a result, the market is expected to grow as data center operators and cloud service providers increasingly move toward advanced cooling architectures to support next-generation edge computing and AI-driven infrastructure.

- For instance, in February 2025, Submer announced expansion of SmartPod immersion cooling systems across AI-focused data center facilities in Europe, while LiquidStack strengthened its hyper-scale partnerships in North America to support high-density GPU cluster installations, reflecting sustained investment in next-generation cooling technologies for AI and HPC-driven infrastructure.

Submer Technologies, LiquidStack, GRC (Green Revolution Cooling), Asperitas, Iceotope Technologies, DCX - The Liquid Cooling Company, Midas Immersion Cooling, Fujitsu Limited, and Vertiv Holdings Co., are among the key players holding a significant share of the market. Their competitive positioning is supported by established hyperscale and colocation partnerships, strong deployment track records in AI and HPC environments, proprietary dielectric fluid optimization capabilities and integrated system architectures spanning immersion tanks, cooling distribution units and intelligent monitoring platforms.

Download Free sample to learn more about this report.

Data Centers Liquid Immersion Cooling Market Key Takeaways

- 2025 Market Size: USD 287.29 million

- 2026 Market Size: USD 348.30 million

- 2034 Forecast Market Size: USD 1,694.11 million

- CAGR: 21.9% from 2026–2034

- North America dominated the data centers liquid immersion cooling market with a 33.56% share in 2025.

- Immersion cooling tanks accounted for the largest share of the market in 2025.

- Robotic arm-based AFP machines are projected to witness the highest growth during the forecast period.

North America

North America generated USD 96.42 million in revenue in 2025, supported by strong AI, cloud, hyperscale, and colocation data center infrastructure.

Europe

Europe held a significant market share in 2025, driven by its extensive hyperscale, colocation, and enterprise data center ecosystem.

Asia Pacific

Asia Pacific generated USD 90.95 million in revenue in 2025 and remains the fastest-growing regional market.

U.S.

U.S. The market is projected to reach approximately USD 100.19 million in 2026, maintaining its leadership in North America.

Japan

Japan The market is estimated at around USD 12.99 million in 2026, representing approximately 3.7% of the global market.

Read More

DATA CENTERS LIQUID IMMERSION COOLING MARKET TRENDS

Shift from Pilot-Scale Deployments to Modular, Scalable Immersion Cooling Architectures is an Emerging Market Trend

Data center operators are increasingly shifting from fixed, pilot-scale immersion cooling installations toward modular and scalable immersion cooling architectures to manage fluctuating AI workload intensity, multi-tenant colocation requirements and evolving rack power densities. Immersion cooling equipment providers are responding by offering tank-based and containerized systems with flexible layouts, scalable cooling distribution infrastructure and software-enabled thermal monitoring platforms. These modular configurations enable hyperscale and colocation facilities to expand high-density capacity incrementally, retrofit brownfield environments and optimize energy efficiency without undertaking full facility redesigns. This improves equipment utilization, reduces capital deployment risk, and supports phased AI cluster expansion strategies across major data center regions.

- For instance, in April 2025, Submer emphasized growing demand for modular immersion cooling pods designed for phased hyperscale AI deployments, while LiquidStack expanded its scalable tank-based systems to support incremental capacity additions within existing high-density data center environments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Integrated Thermal Management Portfolios Enable End-to-End Immersion Cooling Deployment

Strategic portfolio expansion by leading immersion cooling equipment manufacturers is driving data centers liquid immersion cooling market growth. Hyperscale operators and colocation providers increasingly prefer vendors capable of delivering integrated solutions spanning immersion tanks, coolant distribution units, heat rejection systems, dielectric fluid management and intelligent monitoring platforms, thereby reducing system integration complexity and improving operational reliability. This shift is encouraging immersion cooling suppliers to strengthen complementary engineering, controls and lifecycle service capabilities, supporting investments in both greenfield hyperscale facilities and phased retrofits across existing high-density data center environments.

- For instance, in May 2024, Schneider Electric expanded its liquid cooling portfolio through deeper integration of monitoring and thermal management platforms to support high-density AI deployments, while LiquidStack enhanced its turnkey immersion cooling infrastructure offerings for large-scale hyperscale data center projects.

MARKET RESTRAINTS

High Capital Intensity and Infrastructure-Specific Qualification Requirements Limiting Flexible Immersion Cooling Adoption

Unlike conventional air-based cooling systems, data center liquid immersion cooling equipment requires high upfront capital investment and extensive facility-level integration tied to specific rack densities, power configurations and IT hardware compatibility requirements. Variations in server architecture, GPU configurations and workload profiles across hyperscale, colocation and enterprise environments often necessitate customized tank layouts, coolant management systems and heat rejection designs, increasing deployment complexity and limiting redeployability. For operators facing uncertain AI workload scaling timelines or phased capacity planning cycles, the risk of underutilization and extended validation processes can delay immersion cooling adoption, particularly where return on investment is highly sensitive to long-term compute density requirements and sustained high-performance infrastructure utilization.

MARKET OPPORTUNITIES

Expansion of Immersion Cooling Adoption Beyond Hyperscale Operators Unlocks Demand from Colocation and Enterprise Data Centers

A growing opportunity for the market lies in the gradual expansion of immersion cooling deployment beyond large hyperscale operators into colocation providers, enterprise data centers and edge facilities. Rising AI inference workloads, high-performance computing applications and sustainability mandates are encouraging mid-sized operators to transition from conventional air and indirect liquid cooling systems toward compact and energy-efficient immersion platforms. This shift is driving demand for modular, scalable and cost-optimized immersion cooling solutions that offer lower facility modification requirements, smaller deployment footprints and phased expansion capabilities, enabling incremental upgrades without the complexity or capital intensity of full-scale hyperscale infrastructure builds.

- For instance, in August 2024, GRC (Green Revolution Cooling) expanded its engagement with regional colocation providers deploying modular immersion cooling systems to support high-density GPU workloads while improving energy efficiency and rack-level performance reliability.

MARKET CHALLENGES

Fluid Compatibility Risks and Long-Term Operational Uncertainty Limiting Large-Scale Immersion Standardization

Despite accelerating adoption, long-term material compatibility, fluid lifecycle management and IT hardware warranty considerations continue to challenge the scalable deployment of immersion cooling systems across data center environments. Unlike conventional air or indirect liquid cooling systems, immersion platforms require direct submersion of servers and high-value GPU hardware into dielectric fluids, raising concerns around component degradation, fluid contamination, maintenance complexity and OEM warranty alignment. Variations in dielectric fluid chemistry, supplier standards and hardware validation protocols across vendors further complicate ecosystem-wide standardization. For hyperscale and colocation operators managing multi-vendor server fleets, uncertainty around long-term operational performance, residual asset value and cross-platform interoperability can delay large-scale standardization of immersion cooling architectures and slow transition from pilot deployments to fleet-wide rollouts.

Segmentation Analysis

By Cooling Type

Single-Phase Immersion Cooling Systems Dominate Due to Broader Commercial Deployment and Lower Operational Complexity

The market, based on cooling type, is segmented into single-phase immersion cooling systems and two-phase immersion cooling systems.

Single-phase immersion cooling systems hold the highest data centers liquid immersion cooling market share as they remain the preferred solution for hyperscale, colocation, and enterprise deployments requiring reliable, cost-efficient, and operationally stable thermal management. These systems utilize dielectric fluids that remain in liquid form during operation, simplifying infrastructure design, fluid management and long-term maintenance. Their dominance is further reinforced by wider hardware compatibility, lower integration risk and established deployment track records across AI, High Performance Computing (HPC), and cloud infrastructure environments. As operators prioritize scalable, modular architectures with predictable performance and reduced technical complexity, single-phase systems continue to account for the majority of installed immersion cooling capacity.

- For instance, in October 2024, GRC (Green Revolution Cooling) expanded deployments of its single-phase immersion cooling systems across North American colocation facilities supporting high-density AI workloads, reinforcing the widespread commercial adoption of single-phase architectures.

Robotic arm-based AFP machines are witnessing the highest growth, registering a CAGR of 7.7%, driven by increasing demand for flexible, space-efficient and reconfigurable composite manufacturing solutions. These systems are gaining higher traction among Tier-2 suppliers, regional composite manufacturers and industrial users producing complex-geometry parts with lower volume variability. Their ability to support multi-part production, faster redeployment and lower upfront investment compared to gantry systems is accelerating adoption, particularly in brownfield facilities and emerging composite applications. Growing use in thermoplastic AFP processing and non-aerospace structural components is further strengthening the growth outlook for robotic AFP architectures.

To know how our report can help streamline your business, Speak to Analyst

By Equipment Type

Immersion Cooling Tanks Dominate Owing to Core System Functionality and Infrastructure Centrality

Based on equipment type, the market is segmented into immersion cooling tanks, coolant distribution units (CDUs), heat exchangers, pumps & fluid circulation systems, and monitoring & control systems.

Immersion cooling tanks account for the largest share of the market as they form the core structural and functional component of immersion cooling infrastructure. These tanks house IT hardware directly within dielectric fluids and are engineered to support high rack densities, structural stability and optimized fluid dynamics. As the primary hardware interface between servers and the cooling medium, tanks represent the highest-value component within immersion deployments. Their dominance is further reinforced by widespread adoption across hyperscale AI clusters, colocation GPU deployments and high-performance computing environments where scalable tank-based architectures enable modular capacity expansion and high thermal transfer efficiency.

- For instance, in June 2024, LiquidStack expanded deployment of its high-density immersion cooling tank systems across hyperscale AI data center facilities in North America, reflecting sustained demand for tank-centric immersion architectures.

Monitoring & control systems are expected to witness the highest growth, registering a CAGR of 23.3%, driven by increasing emphasis on thermal optimization, predictive maintenance and energy efficiency management in high-density AI environments. As immersion deployments scale, operators require advanced sensing, real-time analytics and automated fluid management platforms to ensure operational stability and performance visibility.

Coolant Distribution Units (CDUs) hold a critical share within immersion cooling infrastructure as they regulate coolant flow, temperature control, and heat exchange between tanks and facility cooling systems. Increasing deployment of high-density AI racks and modular immersion pods is steadily driving demand for scalable and high-capacity CDU platforms across hyperscale and colocation environments.

By Data Center Type

Hyperscale Data Centers Dominate Due to High-Density AI and GPU Infrastructure Expansion

Based on data center type, the market is segmented into hyperscale data centers, colocation data centers, enterprise data centers, and edge data centers.

Hyperscale data centers account for the largest share of the market due to their aggressive deployment of high-density AI training clusters, large-scale GPU infrastructure, and next-generation cloud computing platforms. Immersion cooling is particularly well-suited for hyperscale environments where rack power densities significantly exceed traditional air-cooling thresholds and energy efficiency targets are tightly managed.

- For instance, in July 2024, Submer expanded its immersion cooling deployments across hyperscale AI facilities in Europe and North America, supporting high-density GPU clusters and reinforcing the leading share of hyperscale operators in immersion adoption.

Edge data centers are expected to witness the highest growth, registering a CAGR of 22.3%, driven by increasing demand for low-latency computing, 5G network processing and distributed AI inference workloads. As edge facilities operate within space-constrained and power-limited environments, immersion cooling offers compact, energy-efficient thermal management solutions capable of supporting higher compute densities within smaller footprints.

By Application

Artificial Intelligence & Machine Learning Dominates Owing to Ultra-High Compute Density and Thermal Requirements

Based on application, the market is segmented into High-Performance Computing (HPC), artificial intelligence & machine learning, cloud computing infrastructure, cryptocurrency mining, and 5G & telecom network processing.

Artificial intelligence & machine learning accounts for the largest share of the market, driven by rapid deployment of high-density GPU clusters and accelerator-based computing platforms for large language models, generative AI and advanced analytics workloads. These applications generate significantly higher heat loads per rack compared to traditional cloud workloads, making immersion cooling a critical enabler of sustained performance, thermal stability and energy efficiency. The segment is also expected to witness the highest growth, registering a CAGR of 23.7%, driven by accelerating investment in AI model development, enterprise AI adoption, and next-generation data center buildouts optimized for ultra-high power densities.

Cloud computing infrastructure continues to adopt immersion cooling as hyperscale operators optimize power allocation and floor space efficiency within multi-tenant environments. The shift toward AI-integrated cloud services and higher server consolidation ratios is encouraging deployment of liquid-based cooling to stabilize thermals while supporting elastic compute scaling.

Data Centers Liquid Immersion Cooling Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Data Centers Liquid Immersion Cooling Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 96.42 million revenue in 2025, supported by the region’s large installed base of hyperscale and colocation data centers and strong concentration of AI, cloud and high-performance computing infrastructure. The presence of major hyperscale operators and GPU-intensive AI cluster deployments continues to sustain demand for single-phase and two-phase immersion cooling systems used in high-density rack environments. Increasing rack power densities, rising AI model training requirements and ongoing transition from conventional air-based cooling to advanced liquid-based thermal management solutions are driving steady investment in immersion cooling equipment. In addition, energy efficiency mandates, power availability constraints and the need for scalable, high-performance compute environments are reinforcing immersion cooling adoption across the U.S., Canada and Mexico.

U.S. Data Centers Liquid Immersion Cooling Market

The U.S. is projected to dominate the North American market with an estimated revenue of about USD 100.19 million in 2026, supported by its extensive hyperscale infrastructure footprint and leadership in AI, machine learning, and cloud computing deployments. The country hosts a significant share of immersion cooling installations across hyperscale data centers, colocation GPU clusters, and high-performance computing facilities. Strong capital expenditure commitments from leading cloud and AI service providers, combined with accelerated deployment of next-generation accelerator-based servers, continue to drive demand for both modular single-phase systems and high-performance two-phase immersion architectures.

Europe

The European market holds a significant share of the market, supported by a strong concentration of hyperscale, colocation and enterprise data center infrastructure across the region. The product demand in this region is driven by increasing deployment of AI and high-performance computing workloads, stringent energy efficiency regulations, and growing emphasis on sustainable data center operations. Countries such as Germany, France, the U.K., Italy, Spain, BENELUX and the Nordics are leading immersion cooling adoption, supported by expanding hyperscale capacity, renewable energy integration and regulatory pressure to reduce carbon intensity and improve PUE. Ongoing modernization of legacy air-cooled facilities, increasing rack power densities and the need to optimize thermal management in space-constrained environments continue to underpin steady demand for single-phase and two-phase immersion cooling systems across Europe.

U.K. Data Centers Liquid Immersion Cooling Market

The U.K. market in 2026 is estimated at around USD 13.96 million, representing roughly 4.0% of global revenues.

Germany Data Centers Liquid Immersion Cooling Market

Germany’s market is projected to reach approximately USD 14.51 million in 2026, equivalent to around 4.2% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing market, generating revenue of USD 90.95 million in 2025 globally. Market growth is driven by rapid expansion of hyperscale data center capacity, accelerating AI infrastructure deployment and increasing investment in high-density cloud computing facilities across the region. China, India, Japan, South Korea, ASEAN countries and Oceania are key contributors, supported by large-scale hyperscale buildouts, government-backed digital transformation initiatives and growing domestic AI ecosystems. The region is witnessing a structural shift from conventional air-based cooling toward advanced liquid immersion cooling systems, particularly in China, India, and Southeast Asia, as operators seek scalable, energy-efficient, and high-density thermal management solutions capable of supporting next-generation GPU clusters and AI training infrastructure.

China Data Centers Liquid Immersion Cooling Market

China’s market is projected to remain the dominant in the region, with 2026 revenues estimated at around USD 41.20 million, representing roughly 11.8% of global sales.

Japan Data Centers Liquid Immersion Cooling Market

The Japan market in 2026 is estimated at around USD 12.99 million, accounting for roughly 3.7% of the global market.

India Data Centers Liquid Immersion Cooling Market

The India market in 2026 is estimated at around USD 15.90 million, accounting for roughly 4.6% of global revenues.

Middle East & Africa

The Middle East & Africa market is driven by growing investment in hyperscale data center infrastructure, digital transformation programs, and AI-focused technology initiatives, particularly across the GCC countries, Israel, and South Africa. Government-backed smart city projects, cloud localization strategies, and national AI development agendas are supporting demand for data centers liquid immersion cooling systems used in high-density computing environments. The GCC benefits from large-capex, greenfield hyperscale developments optimized for energy efficiency in high ambient temperature conditions, while Israel continues to invest in AI research infrastructure and advanced computing facilities requiring high-performance thermal management solutions.

GCC Data Centers Liquid Immersion Cooling Market

The GCC market is projected to reach around USD 9.23 million in 2026, representing roughly 2.7% of the global market.

South America

The South America market is supported by the region’s expanding data center infrastructure, increasing cloud service penetration, and growing demand for high-density computing environments, led primarily by Brazil and Argentina. Demand for data centers liquid immersion cooling systems in the region is also driven by colocation expansion, localized cloud availability zones, and rising adoption of AI inference and high-performance workloads. Brazil represents the largest market, supported by São Paulo’s established hyperscale and colocation ecosystem and continued investment in next-generation data center capacity, while Argentina contributes through emerging cloud infrastructure and selective high-density computing deployments.

Brazil Data Centers Liquid Immersion Cooling Market

The Brazil market is projected to reach around USD 13.40 million in 2026, representing roughly 3.8% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Integrated Thermal Management Platforms and Hyperscale Partnerships Intensifies Market Competition

The market is moderately consolidated, characterized by a limited number of global manufacturers offering advanced immersion cooling systems spanning single-phase and two-phase architectures, modular tank platforms, and integrated coolant management infrastructure. Leading players such as Submer Technologies, LiquidStack, GRC (Green Revolution Cooling), Asperitas, Iceotope Technologies, DCX – The Liquid Cooling Company, Midas Immersion Cooling, ExaScaler, Chilldyne, and Schneider Electric hold strong competitive positions, supported by established hyperscale and colocation deployments and long-term partnerships with cloud service providers and AI infrastructure operators.

Competitive differentiation is increasingly driven by system-level integration capability, dielectric fluid optimization, rack density scalability and intelligent monitoring and control platform integration rather than standalone tank hardware. Manufacturers are focusing on modular immersion cooling architectures that enable phased capacity expansion, improved energy efficiency and compatibility with next-generation GPU and accelerator-based servers. This approach allows data center operators to modernize brownfield facilities, support ultra-high-density AI workloads, and improve operational visibility while managing power constraints and long-term sustainability objectives.

- For instance, in May 2024, LiquidStack highlighted the expansion of its modular two-phase immersion cooling platforms with enhanced thermal management controls and hyperscale-ready integration capabilities, supporting large-scale AI data center deployments.

LIST OF KEY DATA CENTERS LIQUID IMMERSION COOLING COMPANIES PROFILED

- Fujitsu Limited (Japan)

- Vertiv Holdings Co. (U.S.)

- STULZ GmbH (Germany)

- Green Revolution Cooling (GRC) (U.S.)

- Submer Technologies (U.S.)

- LiquidStack (U.S.)

- Asperitas (Netherlands)

- Iceotope Technologies (U.K.)

- DCX - The Liquid Cooling Company (Poland)

- Midas Immersion Cooling (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Asperitas and UNICOM Engineering formed a commercial partnership, enabling customers to procure immersion cooling systems and immersion-ready server solutions through a single contract, streamlining procurement and deployment of immersion infrastructure for data centers.

- February 2026: Trane Technologies announced its definitive agreement to acquire LiquidStack, strengthening its end-to-end thermal management portfolio and significantly expanding global reach and production capacity for liquid cooling solutions catering to hyperscale and AI-driven data centers.

- November 2025: Futuriom reported industry activity such as acquisitions and technology integration, noting that liquid cooling vendors including GRC, Schneider Electric, CoolIT Systems, Submer, LiquidStack, and Iceotope are scaling offerings amid rising overall demand for liquid cooling technologies.

- June 2025: LiquidStack unveiled its GigaModular™ coolant distribution unit (CDU), a scalable, multi-megawatt cooling platform designed to support high-density AI and hyperscale data center deployments, reinforcing growing demand for modular liquid cooling infrastructure optimized for next-generation GPU clusters.

- September 2024: LiquidStack secured a USD 20 million Series B extension funding from Tiger Global, expanding its manufacturing footprint, scaling its direct-to-chip and immersion cooling product roadmaps, and broadening commercial and R&D operations to meet growing demand for AI and high-density data center cooling

REPORT COVERAGE

The global data centers liquid immersion cooling market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 21.9% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Cooling Type, Equipment Type, Data Center Type, Application and Region |

| By Cooling Type |

|

| By Equipment Type |

|

| By Data Center Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 348.30 million in 2026 and is projected to reach USD 1,694.11 million by 2034.

In 2025, the North America market value stood at USD 96.42 million.

The market is expected to exhibit a CAGR of 21.9% during the forecast period of 2026-2034.

By application, the artificial intelligence & machine learning is expected to dominate the market.

Rising AI workloads, increasing rack power densities, and growing demand for energy-efficient high-density data center cooling solutions drive market growth.

Fujitsu Limited, Vertiv Holdings Co., STULZ GmbH, Green Revolution Cooling (GRC), Submer Technologies, LiquidStack, and Asperitas are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 128

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us