Data Warehouse as a Service Market Size, Share & Industry Analysis, By Deployment (Public Cloud, Private Cloud, and Hybrid/Multi-Cloud), By Service Type (Enterprise DWaaS, Operational Data-store as a Service, Data Lakehouse as a Service, and Analytics Acceleration Services), By Enterprise Type (Large Enterprises and SMEs), By Industry (BFSI, IT & Telecom, Manufacturing, Healthcare, Retail & E-commerce, and Others), and Regional Forecast, 2026-2034

DATA WAREHOUSE AS A SERVICE MARKET SIZE AND FUTURE OUTLOOK

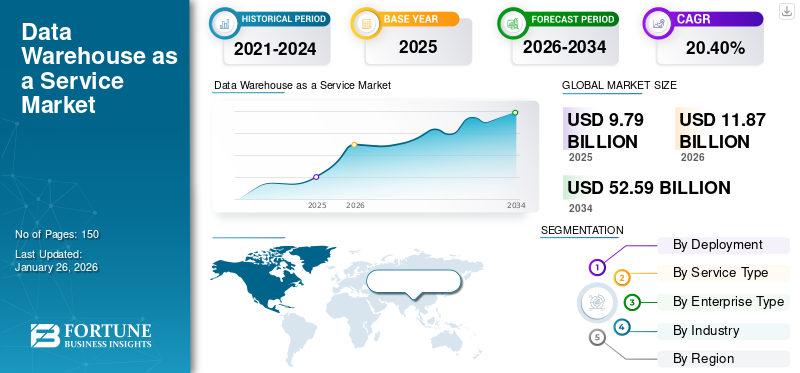

The global data warehouse as a service market size was valued at USD 9.79 billion in 2025. The market is projected to grow from USD 11.87 billion in 2026 to USD 52.59 billion by 2034, exhibiting a CAGR of 20.40% during the forecast period. North America dominated the data warehouse as a service market with a market share of 40.20% in 2025.

Data warehouse as a service is a cloud service that allows companies to manage, store, and analyze a large amount of data without the need for maintaining a physical infrastructure. It also offers higher scalability, flexibility, and cost efficiency via on-demand access to data warehousing resources. The market is driven by the increase in volume of big data, adoption of cloud technologies, and need for real time analytics. Firms are also looking to enhance the operational efficiency and decision making through improved data integration.

Few prominent key players operating in the market are Amazon Web Services, Inc., Snowflake Inc., Google LLC, Microsoft Corporation, IBM Corporation, Oracle Corporation, and Teradata. Key strategies implemented by these players include strategic partnerships, technological advancements, mergers and acquisitions. They also focus on adopting AI, improved data security and automation features to strengthen their market position and meet the growing customer needs.

Download Free sample to learn more about this report.

Data Warehouse as a Service Market Key Takeaways

- 2025 Market Size: USD 9.79 Billion

- 2026 Market Size: USD 11.87 Billion

- 2034 Forecast Market Size: USD 52.59 Billion

- CAGR: 20.40% from 2026–2034

- North America dominated the data warehouse as a service market with a 40.20% share in 2025.

- The public cloud segment is projected to lead the market with a 63.39% share in 2026.

- The enterprise DWaaS segment is expected to account for 53.33% of the market in 2026.

North America

North America reached USD 3.94 billion in 2025 and accounted for 40.20% of the global market.

Asia Pacific

Asia Pacific generated USD 2.58 billion in 2025, representing 26.30% of global revenue.

Europe

Europe recorded USD 2.20 billion in 2025 and contributed 22.50% of the global market.

U.S.

The market is projected to reach USD 3.23 billion in 2026, supported by strong cloud analytics investments.

Japan

Growing cloud adoption and digital transformation initiatives are supporting market expansion.

Read More

IMPACT OF GENERATIVE AI

Gen AI Reshapes Market Due to its Growing Demand for Scalable and Governed Access to Wide Datasets

Generative AI workloads including vector search, retrieval augmented generation (RAG), and fine tuning, are driving the market growth through increased adoption of these platforms and investments. Such advanced AI applications need a scalable, governed and low latency access to a complex and wide datasets. In order to meet these needs, companies are shifting to innovative data warehouses as a service platform that integrate AI based architectures, vector databases, and real time analytics capabilities.

These platforms also enable an effective retrieval, storage and processing of raw and unstructured data that are crucial for performance of Gen AI.

MARKET DYNAMICS

Market Drivers

Rapid Time-To-Value and OPEX Flexibility Drives Market Growth

Faster time-to-value and OPEX flexibility as major key drivers for data warehouse as a service market growth. Unlike the conventional on premise systems that demanded crucial capital expenditure and longer deployment cycles, data warehouse as a service solutions use serverless, cloud based and consumption based models. For instance, according to ABD.org, in 2021, governments and organizations that moved to the cloud saved as much as USD 2 billion over 5 years. Such models allow organizations to pay only for resources that are used, thus lessening the upfront costs and offering operational expenditure (OPEX) flexibility. This enables quicker implementation, rapid data gathering, and enhanced scalability, thus making it ideal for dynamic business settings.

Additionally, the ability to adapt and deploy the data solutions improves the business agility and competitiveness. As a consequence, companies are also increasingly adopting data warehouses as a service to fasten the analytics driven decision making and aiding in sustained market growth.

Market Restraints

Data Sovereignty & Residency Constraints Hampers the Market Growth

Data sovereignty and residency challenges act as crucial factors hampering the market growth. Surging national and sector specific rules demand data to be stored and processed with particular geographic limits, thus leading to a growing independent cloud model. Such regulations add to the complexity of deployment, design and operations of these services for firms with global reach.

Additionally, cross border data transfer also becomes a restraint due to different privacy and security standards, thus slowing down the international reach and increasing operational costs. This also decreases the flexibility and scalability advantages that are offered by cloud based architectures.

Market Opportunities

Healthcare Interoperability Mandates Offers Lucrative Growth Opportunities

Healthcare interoperability obligations present a major opportunity for the market. Regulations including U.S. ONC Cures Act and CMS API regulation need healthcare providers and end users to adopt a standardized data exchange framework which aids in ensuring a transparent and secure patient information exchange. This drives the improvement and migration of conventional systems to cloud based and compliant data solutions.

Data Warehouse as a service platforms offer higher flexibility, scalability, compliance, and integration capability which aligns with such mandates, thus enabling a seamless interoperability across various healthcare networks. Hence, this offers lucrative opportunities for market growth.

DATA WAREHOUSE AS A SERVICE MARKET TRENDS

Hybrid/Multi-Cloud & Sovereign Cloud Acceleration Has Emerged as a Prominent Market Trend

The adoption of multi/hybrid and sovereign cloud is a prominent trend reshaping the market. For instance, according to the World Bank, the global cloud and data infrastructure industry has grown by approximately 35% each year since 2016 and was valued at USD 600 billion in 2022. It is projected to grow at about 20% annually until 2025, with a similar growth rate expected to persist until 2030. The private sector makes up 96% of total investment, whereas government spending represents only 4%.

Rapid growth in data sovereignty, residency, and portability needs are enabling firms to distribute the workloads across various cloud environments or manage hybrid architectures that integrate private and public cloud. This ensures regulatory compliance while strengthening performance, cost efficiency and security.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Deployment

Rapid Time to Value and Elastic Scaling Boosts Public Cloud Segment Growth

Based on the deployment, the market is segmented into public cloud, private cloud, and hybrid/multi-cloud.

In 2026, the public cloud segment is projected to lead the market with a 63.39% share. This dominance is attributed to its rapid time to value and flexible scaling with less upfront hardware. Public cloud is also cost efficient and easy to deploy. Public cloud offers advanced analytics, global accessibility, and AI integration with faster insights for data driven decision making. These factors together lead to the segment’s dominance in the market.

On the other hand, the hybrid/multi cloud segment is growing with the highest CAGR of 24.78% in 2024. This segmental growth is driven by its capability to meet data sovereignty and resilience demands. It also aids in avoiding vendor lock-in and optimizing costs for companies. This has accelerated its adoption across smaller businesses with less capital.

To know how our report can help streamline your business, Speak to Analyst

By Service Type

Growing Demand for Mature and Highly Managed Cloud Warehouses to Drive Enterprise DWaaS Segment Growth

The market is divided into enterprise DWaaS, operational data-store as a service, data lakehouse as a service, and analytics acceleration services, based on service type.

Among these, the enterprise DWaaS segment dominated the market with a revenue share of USD 4.38 billion in 2024. Various core BI/SQL analytics are pervasive and standardized, thus making it attractive for large enterprises. Additionally, enterprises also favor mature and highly managed cloud warehouses, thus leading to the increased adoption of Enterprise DWaaS service type. The enterprise DWaaS segment is projected to dominate the market with a share of 53.33% in 2026.

Consequently, the data lakehouse as a service segment held the largest CAGR of 24.07% in 2024. This growth is attributed to the growing need for compliance support, integration of data lakehouse as a service platform and managed biometric operations across various regulated industries.

By Enterprise Type

Increasing Demand Data Warehouse as a Service Solution by Large Enterprises Drives Segment Growth

Based on the enterprise type, the market is divided into large enterprises and SMEs.

The large enterprises segment is expected to lead the market, contributing 59.30% globally in 2026. The large enterprises segment held the highest market share with a revenue share of USD 4.93 billion. Large enterprises across government, BFSI and healthcare sectors are increasingly demanding data warehouse as a service solution. This is majorly due to the need to meet stringent regulatory compliance, advanced security requirements and high transaction volumes by these companies.

Similarly, the SMEs segment grew with a fastest CAGR of 24.29% in the year 2024. This is due to the growing need for scalable, affordable and easy to deploy data solutions. SMEs need to manage increasing data volumes without investing in overpriced on premises infrastructure. This has significantly augmented the SMEs segment growth.

By Industry

Increasing Investment in Advanced Data Warehouse as a Service Solution by BFSI Industry Drives the Segment Growth

By industry, the market is divided into BFSI, IT & telecom, manufacturing, healthcare, retail & e-commerce, and others.

Among these, the BFSI industry secured the largest share of USD 1.86 billion in 2024. Banks and insurers tend to run highly regulated analytics related to fraud, risks, and reporting. This allows BFSI to constantly invest in advanced data warehouse as a service solution, leading to the segment’s growth.

The healthcare segment held highest CAGR of 25.32% in 2024. With digitized patient data, use of AI or precise medicine, and interoperability mandates, different hospitals, particularly small clinics, are modernizing analytics in the cloud form, driving the segment growth.

DATA WAREHOUSE AS A SERVICE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America Data Warehouse as a Service Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America maintained a strong presence in the global market, reaching USD 3.94 billion in 2025, accounting for 40.20% share, and is expected to reach USD 4.69 billion in 2026. This growth is majorly due to highly increased budgets and deployment of data warehouse as a service solution across the region. Additionally, enterprises across major countries including the U.S. lead in cloud analytics investments and operate in hyperscaler areas. The U.S. is expected to contribute a revenue share of USD 3.23 billion in 2026.

To know how our report can help streamline your business, Speak to Analyst

Europe

In 2025, Europe generated USD 2.2 billion, contributing 22.50% to global market revenue, and is projected to grow to USD 2.63 billion in 2026. This is attributed to the growing focus of the region on data protection, cloud adoption and focus on data protection. Additionally, the growing investment in analytics, AI and Industry 4.0 initiatives boosts the regional market growth. U.K., Germany, and France are some of the major contributors to the regional market growth with an expected revenue share of USD 0.5 billion, USD 0.49 billion in 2026, and USD 0.36 billion respectively by 2025.

Asia Pacific

The Asia Pacific market accounted for USD 2.58 billion in 2025, representing 26.30% of the global industry, and is expected to reach USD 3.24 billion in 2026. This regional growth is due to an increase in digitization and expansion in hyperscaler especially across India and Southeast Asia. India and China are expected to contribute to a revenue share of USD 0.46 billion and USD 0.66 billion respectively in 2026.

South America and Middle East & Africa

In 2025, Middle East & Africa represented USD 0.59 billion, accounting for 6.00% of the worldwide market, and is projected to grow to USD 0.73 billion in 2026.

Latin America contributed 4.90% to the global market in 2025, with a valuation of USD 0.48 billion, and is projected to reach USD 0.58 billion in 2026.

Moreover, growing partnerships with global cloud providers and improved internet connectivity across the region has also augmented the market growth. GCC countries are predicted to have a market share of USD 0.18 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Key Players on Innovation and New Launches Leads to their Dominating Market Positions

The global data warehouse as a service market is highly fragmented with different market players operating in the market. These include Amazon Web Services, Inc., Snowflake Inc., Google LLC, Microsoft Corporation, IBM Corporation, Oracle Corporation, Teradata, Alibaba Cloud, Tencent Cloud, Huawei Cloud, and others. These companies implement different strategic initiatives including innovative launches, mergers and acquisitions, and others to sustain the market competition.

LIST OF KEY DATA WAREHOUSE AS A SERVICE COMPANIES PROFILED:

- Amazon Web Services, Inc. (U.S.)

- Snowflake Inc. (U.S.)

- Google LLC (U.S.)

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- Oracle Corporation (U.S.)

- Teradata (U.S.)

- Alibaba Cloud (China)

- Tencent Cloud (China)

- Huawei Cloud (China)

- SAP SE (U.S.)

- Databricks (U.S.)

- SingleStore (U.S.)

- Yellowbrick Data (U.S.)

- Cloudera (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In May 2025, Dassault Systèmes and the FondaMental Foundation announced their collaboration to deploy a nationwide Health Data Warehouse (HDW) in France dedicated to psychiatry. This project aligns with France’s 2025 public health priorities: strengthening diagnostic and therapeutic research and innovation capabilities by structuring and leveraging complex clinical data within a sovereign and highly secure framework, to improve the understanding, diagnosis and treatment of psychiatric disorders.

- In November 2024, Snowflake Computing raised a USD 26 million funding, focusing on modernizing data warehousing with a from-scratch cloud-based approach. The company has introduced a patent-pending architecture that assures to modernize the data warehouse market with a solution that decouples data storage from compute.

- In May 2023, Oracle announced new innovations to Oracle Autonomous Data Warehouse, the industry’s first and only autonomous database powered by machine learning and optimized for analytics workloads. The innovations break through the proprietary and closed nature of traditional data warehouses and data lakes.

- In April 2023, SAP announced the launch of SAP Datasphere, a comprehensive data service built on the SAP Business Technology Platform (SAP BTP) delivering seamless and scalable access to mission-critical business data no matter where it may reside. With the SAP Datasphere, an organization is able to develop innovative strategies to increase profits, create new revenue streams and make better decisions by understanding their data regardless of where it resides.

- In December 2021, SimCorp launched Cloud Data Warehouse, powered by Snowflake, for clients’ investment and analytics needs. Data Cloud Warehouse enables SimCorp clients to access all the data they require when they need it, allowing new sources of data to be rapidly onboarded when required, radically reducing the time to value.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the data warehouse as a service market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE |

DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 20.40% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation |

By Deployment

By Service Type

By Enterprise Type

By Industry

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 11.87 billion in 2026 and is projected to reach USD 52.59 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 20.40% during the forecast period.

Rapid time-to-value and OPEX flexibility drives the market growth.

Amazon Web Services, Inc., Snowflake Inc., Google LLC, Microsoft Corporation, and IBM Corporation, Oracle Corporation are some of the top players in the market.

North America dominated the data warehouse as a service market with a market share of 40.20% in 2025.

North America was valued at USD 3.94 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us