Defense Logistics Market Size, Share & Industry Analysis, By Commodity (Armament, Technical Support & Maintenance, Medical Aid, and Others), By Mode of Transport (Roadways, Waterways, Airways, and Railways), By End-Use (Army, Navy, and Air Force), and Regional Forecast, 2026-2034

DEFENSE LOGISTICS MARKET SIZE AND FUTURE OUTLOOK

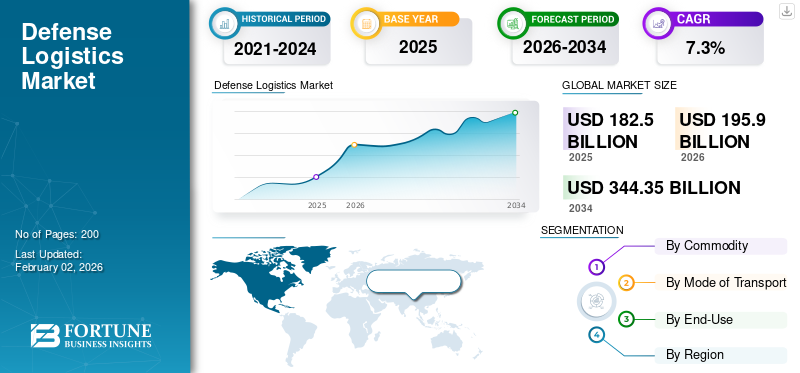

The global defense logistics market size was valued at USD 182.50 billion in 2025 and is projected to grow from USD 195.90 billion in 2026 to USD 344.35 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period. North America dominated the global market with a share of 33.19% in 2025.

The defense logistics market is a critical pillar of military readiness and operational success, encompassing the planning, movement, storage, and sustainment of personnel, equipment, and supplies. Unlike commercial logistics, defense logistics operates in complex environments where supply lines may be contested, and resilience and speed are as important as cost efficiency. The scope includes transportation of armaments, fuel, spare parts, medical supplies, technical maintenance, and forward base support. With the growing complexity of modern weapon systems and multi-domain warfare, logistics has shifted from being a supporting function to a strategic enabler of force projection.

Nations are increasingly focusing on distributed logistics, rapid deployment, and digitization of supply chains, supported by predictive maintenance, additive manufacturing, and real-time asset tracking. Recent conflicts, particularly in Eastern Europe, have reinforced the need for flexible and resilient supply chains, pre-positioned stockpiles, and secure IT systems. Furthermore, partnerships between defense agencies and private contractors are expanding, as militaries are outsourcing functions such as base operations, sustainment services, and secure transport. The market is evolving toward integrated solutions combining physical logistics, digital visibility, and security, ensuring armed forces remain mission-ready under contested conditions.

The market is served by both defense primes and specialized logistics providers. Lockheed Martin, Boeing, RTX (Raytheon Technologies), and Northrop Grumman are key players in integrated sustainment and lifecycle management. Companies such as General Dynamics and BAE Systems offer platform-specific logistics and depot-level maintenance. KBR, Amentum, and Leidos provide outsourced logistics services, base operations, and contract sustainment. On the commercial side, DHL and Kuehne + Nagel have carved niches in defense transport and supply-chain management. Collaboration between primes and commercial logistics specialists is growing, offering military end-to-end, technology-enabled logistics solutions.

Download Free sample to learn more about this report.

Defense Logistics Market KEY TAKEAWAYS

- 2025 Market Size: USD 182.50 billion

- 2026 Market Size: USD 195.90 billion

- 2034 Forecast Market Size: USD 344.35 billion

- CAGR: 7.3% from 2026–2034

- North America dominated the defense logistics market with a 33.19% share in 2025.

- The roadways segment is projected to hold a 53.49% market share in 2026.

- The armament segment is anticipated to dominate with a 52.86% share in 2026.

North America

North America held a 33.19% share in 2025, valued at USD 60.57 billion, and is projected to reach USD 64.53 billion in 2026.

Europe

Europe accounted for 21.57% of the global market in 2025, generating USD 39.37 billion in revenue and reaching USD 42.29 billion in 2026.

Asia Pacific

Asia Pacific captured a 29.23% share in 2025, valued at USD 53.34 billion, and is expected to reach USD 57.95 billion in 2026.

U.S.

U.S. The defense logistics market is estimated to reach USD 52.95 billion in 2026.

Japan

Japan The market is projected to reach USD 14.34 billion by 2026.

Read More

RUSSIA-UKRAINE WAR ANALYSIS

Russia-Ukraine War Fuels Demand for Reshaping Global Defense Logistics Priorities

The Russia-Ukraine war has reshaped the global defense logistics landscape by highlighting both vulnerabilities and innovations in sustainment. Russia’s initial offensive revealed major logistics shortcomings: long-exposed supply lines, insufficient fuel and spare parts, and weak maintenance planning, all of which slowed advances and eroded combat effectiveness. In contrast, Ukraine’s distributed and adaptive logistics relying on small, mobile repair teams, pre-positioned stocks, and even civilian support networks demonstrated the importance of agility. These operational lessons have not gone unnoticed, prompting militaries worldwide to reassess doctrines and invest in redundant, resilient supply networks.

At the industrial level, sanctions on Russia disrupted traditional supply flows of fuels, metals, and components, accelerating a shift toward regionalized supply chains. Since then, European and allied countries have prioritized secure sourcing and stockpiling of critical defense materials, reducing reliance on contested or politically unstable regions. This realignment has created new demand for logistics providers able to offer compliant, secure, and rapid solutions.

The war also underscored the importance of coalition logistics. Massive Western aid flows into Ukraine required coordination across borders, highlighting bottlenecks in customs, transport capacity, and inland distribution. Airlift and sealift capacity were heavily stressed, forcing reliance on commercial freight charters and temporary logistics hubs. These lessons are shaping procurement strategies, with NATO and partners exploring expanded strategic transport fleets and better crisis surge mechanisms.

The adoption of technology has increased as drones were used not only for reconnaissance but also for limited resupply, highlighting future potential for unmanned logistics. Additive manufacturing and contractor provided forward repair kits gained attention as methods to reduce supply-line dependencies. Cybersecurity also became a priority as logistics networks faced cyber disruption attempts.

The Russia-Ukraine war elevated logistics from a support function to a decisive factor in warfare. The conflict’s lessons are driving investments in distributed sustainment, secure supply chains, digital visibility, and strategic transport, reshaping the global defense logistics market share for the foreseeable future.

DEFENSE LOGISTICS MARKET TRENDS

Digitization, Autonomy, and Sustainable Logistics is a Significant Trend in the Market

Defense logistics is undergoing a transformation led by digitization and technology adoption. Real-time asset tracking, predictive maintenance, and integrated logistics management systems are rolled out more widely. Autonomous systems including drones and unmanned ground vehicles are increasingly tested for frontline resupply, reducing risks to personnel. Additive manufacturing is gaining traction, enabling on-demand parts production close to operational theaters, which reduces supply-line vulnerabilities. Another trend is the rise of “logistics-as-a-service,” where militaries outsource entire sustainment packages to industry, shifting risk, and ensuring performance outcomes.

Resilience and regionalization of supply chains are accelerating, with nations moving to reduce dependence on single suppliers or hostile regions, particularly for critical materials. Cybersecurity is also becoming central, with tamper-proof tracking, encrypted logistics systems, and hardened IT infrastructure as standard requirements. Finally, sustainability is slowly being integrated into defense logistics from biofuels and hybrid fleets to energy-efficient base operations as militaries respond to both cost pressures and climate mandates. Together, these trends signal a shift toward smarter, more resilient, and more sustainable logistics systems.

Download Free sample to learn more about this report.

MARKET DRIVERS

Rising Budgets, Platform Complexity, and Digitization Will Drive Market Expansion

Several key factors are driving the defense logistics market growth. First, increasing global defense budgets, particularly in NATO countries, the Indo-Pacific, and the Middle East, are generating greater demand for sustainment and supply-chain support. Second, the complexity of modern platforms, advanced fighter jets, naval vessels, and unmanned systems require sophisticated maintenance, spare-parts forecasting, and integrated logistics support, fueling demand for specialized contractors.

Third, geopolitical tensions and lessons from conflicts highlight the importance of readiness and agile resupply, prompting investments in distributed logistics nodes, pre-positioned supplies, and rapid-deployment capabilities. Fourth, digitization is enabling smarter logistics: predictive analytics reduce equipment downtime, while blockchain and secure communication networks ensure supply-chain transparency and integrity.

Fifth, technology advances such as autonomous ground vehicles, resupply drones, and 3D printing of spare parts are pushing militaries toward new logistics models that increase efficiency and resilience. Finally, joint and coalition operations drive the need for interoperable logistics systems that allow allied forces to share resources and information securely. Collectively, these drivers position defense logistics as a growth area within the broader defense industry.

MARKET RESTRAINTS

Budget Volatility, Compliance, and Cyber Risks Restrain Market Expansion

Despite growth, the defense logistics sector faces several restraints. Budget volatility remains a major concern, as governments must balance logistics investment with procurement of new weapons systems, sometimes leading to underfunded sustainment programs. Lengthy procurement processes and regulatory compliance requirements raise barriers for commercial entrants and slow innovation adoption. Export controls, sanctions, and strict sourcing rules complicate global supply chains, increasing cost and reducing flexibility. Workforce shortages, especially for skilled maintainers and cleared technicians, pose operational risks. Cybersecurity threats also loom large, as logistics IT systems present attractive targets for adversaries; securing these networks adds cost and complexity. Integrating advanced technologies such as predictive analytics or additive manufacturing into legacy systems is another challenge, as militaries often operate with outdated infrastructure. Additionally, political considerations and industrial base policies limit supplier diversification, leaving some critical parts and materials dependent on single sources. These restraints collectively slow the pace of transformation in defense logistics and raise entry barriers for new players.

MARKET OPPORTUNITIES

Expanding Avenues through Modernization and Technology Drive’s Opportunities in Defense Logistics

Opportunities in defense logistics are expanding as militaries modernize forces and adapt to emerging threats. With rising geopolitical tensions, governments are prioritizing resilient and distributed logistics networks capable of supporting multi-domain operations. This creates openings for companies offering mobile depots, rapid-deployment warehousing, and unmanned resupply systems. Digitization is another growth avenue: predictive maintenance, blockchain-enabled supply chains, and digital twins allow forces to minimize downtime and enhance readiness. The increasing reliance on contractors for base operations, sustainment services, and training creates opportunities for commercial logistics firms with secure, dual-use capabilities.

Additive manufacturing allows parts to be produced near the battlefield, reducing reliance on long supply lines. Furthermore, sustainability initiatives such as alternative fuels, hybrid military vehicles, and energy-efficient base infrastructure present new niches for innovation. Countries are also exploring “logistics-as-a-service,” contracting full supply-chain packages from industry rather than building them internally, providing long-term opportunities for providers capable of integrated delivery. Overall, firms that combine agility, technology integration, and compliance with defense regulations stand to benefit significantly.

MARKET CHALLENGES

Balancing Agility, Security, and Interoperability are Key Challenges to the Market

The central challenge in defense logistics lies in balancing agility with security. Militaries must ensure that supply chains are protected against disruption, sabotage, or cyber-attacks while remaining flexible enough to support fast-changing operational requirements. In coalition operations, interoperability becomes a major hurdle differing logistics standards, incompatible IT systems, and political sensitivities hinder joint sustainment. Operating in contested environments also presents challenges: resupply convoys and depots are vulnerable to long-range precision strikes, requiring new tactics such as dispersed caches, hardened logistics hubs, and stealthy delivery systems. Introducing technologies such as autonomous resupply vehicles or additive manufacturing requires doctrinal changes, training, and regulatory frameworks that take years to evolve. Supply-chain fragility is another challenge, with many high-tech components dependent on limited suppliers or vulnerable transport routes. Environmental and infrastructure constraints such as damaged ports, disrupted fuel supplies, or contested maritime choke points add further complexity. Overcoming these challenges demands long-term investments, policy reform, industry partnerships, and new operating concepts validated through joint exercises.

SEGMENTATION ANALYSIS

By Mode of Transport

High Demand for Roadways Due to Critical Role in Mobility and Resupply

By mode of transport, the segment is categorized into roadways, waterways, airways, and railways.

The roadways segment captured the largest share of the market in 2025 and in 2026 it is anticipating to dominate with a 53.49% market share. The segment holds strong demand in defense logistics due to its critical role in troop mobility, equipment transport, and supply distribution across diverse terrains. Armies rely on military trucks, armored transport, and fuel convoys for rapid resupply and operational flexibility. Road logistics remains vital for both domestic training missions and overseas deployments, ensuring accessibility where airlift or rail options are limited.

The airways segment is expected to grow at a CAGR of 7.4% over the forecast period.

By Commodity

Strong Demand for Armament Logistics is Driven by Security and Readiness Needs

By commodity, the market is classified into armament, technical support & maintenance, medical aid, and others.

The armament segment captured the largest share of the market in 2025. In 2026, the segment is anticipating to dominate with 52.86% share. The armament segment commands significant demand in defense logistics, as militaries prioritize secure, timely, and efficient transport of weapons, ammunition, and explosives. With rising global tensions and modernization of armed forces, the need for specialized storage, handling, and distribution systems has increased. Advanced tracking, safety protocols, and rapid replenishment capabilities are essential to ensure operational readiness and sustained firepower in both peacetime and combat scenarios.

Others segment is expected to grow at a CAGR of 8.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-Use

Army Segment is in High Demand Owing to Large-Scale Operations and Sustainment

The market by end-use is sub-segmented into army, navy, and air force.

The army segment captured the largest share of the market in 2025 and is estimated to continue its dominance with a 52.51% market share in 2026. The army segment generates the largest demand in the defense logistics market, driven by its extensive need for troop movement, equipment sustainment, and continuous resupply in diverse terrains. Large-scale land operations, training exercises, and border security missions require robust logistics support, including fuel, armament, and maintenance services. With modernization efforts and evolving combat doctrines, armies worldwide increasingly depend on agile and technology-enabled logistics systems to maintain readiness.

Air force segment is expected to grow at a CAGR of 8.0% over the forecast period.

DEFENSE LOGISTICS MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, the Middle East and the rest of the world.

North America

In 2025, the North America market stood at USD 60.57 billion, representing 33.19% of global demand, and is projected to grow to USD 64.53 billion in 2026, driven by strong adoption across defense, infrastructure, utilities, and smart cities. The demand for defense logistics in North America is driven primarily by the U.S., which maintains the world’s largest defense budget and extensive global military presence. The U.S. Department of Defense invests heavily in sustainment, supply-chain modernization, and pre-positioned assets to support overseas operations and alliances. Canada also contributes through NATO missions and Arctic defense initiatives, focusing on fuel, maintenance, and infrastructure logistics. Growing emphasis on advanced technologies such as predictive analytics, unmanned resupply systems, and cybersecurity resilience further strengthens regional demand, positioning North America as the largest and most technologically advanced market for defense logistics solutions.

In 2026, the U.S. market is estimated to reach USD 52.95 billion. The U.S. is the largest single-country market for defense logistics, accounting for nearly half of global demand. The U.S. defense logistics market stands at the forefront due to its scale, technological advancements, and global commitments. Pentagon’s logistics operations cover everything from continental sustainment to rapid deployment worldwide, relying on a blend of military depots, commercial contractors, and strategic transport fleets. High demand is observed for predictive maintenance, additive manufacturing for spare parts, and unmanned resupply to enhance operational efficiency. Increasing focus on contested logistics, cyber-secure supply chains, and distributed bases in the Indo-Pacific are shaping new procurement trends, while major defense contractors and logistics firms continue to play central roles in supporting U.S. forces.

Europe

The Europe region captured 21.57% of the global market in 2025, generating USD 39.37 billion in revenue, and is projected to reach USD 42.29 billion in 2026. In Europe, the demand for defense logistics is accelerating due to NATO modernization, the Russia-Ukraine war, and commitments to collective defense. Germany, France, and the U.K. are expanding investments in strategic airlift, armored vehicle sustainment, and fuel supply infrastructure to ensure readiness in case of high-intensity conflicts. The EU’s defense initiatives are also encouraging shared logistics frameworks, joint procurement, and cross-border coordination among member states. Contractors and industry partners are increasingly involved in providing maintenance, training, and digital solutions, reflecting Europe’s focus on resilience, interoperability, and rapid response to regional security threats. The UK market is projected to reach USD 9.99 billion by 2026, and the Germany market is projected to reach USD 8.32 billion by 2026.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 53.34 billion in 2025, accounting for 29.23% share, and is expected to reach USD 57.95 billion in 2026. The region is experiencing strong growth fueled by rising military modernization, territorial disputes, and the strategic competition in the Indo-Pacific. China, India, Japan, South Korea, and Australia are heavily investing in sustainment infrastructure, supply-chain resilience, and logistics technologies to support large standing forces and maritime operations. With vast geographies and contested environments, demand is high for distributed depots, rapid transport, and advanced supply management systems. The U.S. alliance network in the region also drives collaborative logistics, while indigenous innovation such as India’s focus on self-reliant defense manufacturing adds further momentum to the regional market. The Japan market is projected to reach USD 14.34 billion by 2026, the China market is projected to reach USD 19.26 billion by 2026, and the India market is projected to reach USD 9.87 billion by 2026.

Middle East & Africa

Latin America in 2025 is set to record USD 13.93 billion, while the Middle East & Africa is set to reach USD 15.29 billion in 2025. In the rest of the world, demand for defense logistics is growing steadily, driven by modernization efforts in the Middle East, Africa, and Latin America. Saudi Arabia and the UAE emphasize logistics infrastructure, contractor sustainment, and secure supply networks to support advanced weapons platforms and regional operations. African countries face unique challenges of geography and limited infrastructure, prompting investments in mobility and maintenance support. In Latin America, Brazil and others are upgrading logistics to strengthen peacekeeping and border security operations. Overall, demand centers around modernization, supply resilience, and collaboration with international defense partners.

Rest of the World

The Rest of the World market generated USD 29.22 billion in 2025, representing 16.01% of the global market landscape, and is expected to reach USD 31.13 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Driving the Global Defense Logistics Ecosystem with Advanced Defense Systems

The defense logistics market is shaped by a diverse set of players that bring together defense primes, specialized contractors, and global logistics providers. Leading defense companies such as Lockheed Martin, Boeing, Raytheon Technologies (RTX), Northrop Grumman, General Dynamics, and BAE Systems dominate the integrated sustainment and lifecycle support domain. These firms leverage decades of platform expertise to provide end-to-end logistics solutions, including maintenance, spare parts forecasting, training, and integrated logistics support for complex aircraft, naval vessels, and land systems.

LIST OF KEY DEFENSE LOGISTICS COMPANIES:

- Lockheed Martin Corporation (U.S.)

- Raytheon Technologies (RTX) (U.S.)

- Northrop Grumman Corporation (U.S.)

- Boeing Defense, Space & Security (U.S.)

- General Dynamics (U.S.)

- BAE Systems (U.K.)

- KBR Inc. (U.S.)

- Amentum (U.S.)

- Leidos Holdings (U.S.)

- Fluor Corporation (U.S.)

- Kuehne + Nagel (Switzerland)

KEY INDUSTRY DEVELOPMENTS:

- August 2025 - The Defense Logistics Agency has chosen Google Public Sector to enhance its global supply chain operations – marking the agency's inaugural partnership with a commercial cloud provider that is AI-ready.

- March 2025- The Defense Logistics Agency ("DLA") and the Veterans Health Administration ("VHA") have established a new interagency agreement. The agencies have declared that the objective of this 10-year, USD 3.6 billion agreement is to synchronize supply chain needs and consolidate logistical support that DLA will extend to all VHA healthcare facilities across the country.

- March 2025 - AAR CORP., a prominent supplier of aviation services to both commercial and government entities, MROs, and OEMs, has expanded its distribution support for certain Unison parts as part of its Supplier Capabilities Contract with the Defense Logistics Agency (DLA) Aviation.

- May 2024 - The Defense Logistics Agency (DLA), along with the Land and Maritime Directorates of Supplier Operations and ASRC Federal, has established a partnership focused on enhancing supply chain support for our nation's warfighters. The objective of this collaboration is to execute joint strategies and process improvements that aim to boost responsiveness to the warfighter, which encompasses customer deliverables and administrative efficiency.

- February 2023- HII announced that its Mission Technologies division received a recompete contract worth USD 21 million from the Defense Logistics Agency (DLA). This contract aims to research and develop technical solutions designed to enhance the efficiency of product and material delivery to the warfighter, thereby supporting DLA’s global mission.

REPORT COVERAGE

The defense logistics market is witnessing steady growth, driven by its increasing role as a strategic enabler of military readiness and efficiency. The sector is not only advancing through strong research and development initiatives but also by enhancing the optimization of operational services to meet evolving defense requirements. With rising global investments, the market reflects robust opportunities, supported by emerging trends, regional developments, and innovations in technology. Competitive dynamics showcase how leading companies are driving progress through modernization and integration of advanced logistics solutions. Overall, defense logistics has become a critical contributor to strengthening armed forces, ensuring supply-chain resilience, and shaping the future of defense operations.

Request for Customization to gain extensive market insights.

Key Segments within the Defense Logistics Market

| ATTRIBUTE |

DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.3% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | Commodity, Mode of Transport, End-Use, and Geography |

|

By Commodity

|

|

|

By Mode of Transport

|

|

|

By End-Use

|

|

| By Geography |

|

Frequently Asked Questions

As per Fortune Business Insights study, the market size was USD 182.50 billion in 2025.

The market is likely to grow at a CAGR of 7.3% over the forecast period (2026-2034).

The market size of North America stood at USD 60.57 billion in 2025.

Some of the top players in the market are Lockheed Martin Corporation (U.S.), Raytheon Technologies (RTX, U.S.), Northrop Grumman Corporation (U.S.), Boeing Defense, Space & Security (U.S.), General Dynamics (U.S.), BAE Systems (U.K.), and KBR Inc. (U.S.).

The U.S. dominated the market for defense logistics in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us