Direct Air Capture Market Size, Share & Industry Analysis, By Technology (CO2 Concentrating DAC, Reactive DAC, and Direct Storage DAC), By Sorbent Type (Solid Sorbent, Liquid Solvent, Membrane, and Electrochemical), By Application (Carbon Capture and Permanent Storage, and Carbon Utilization), By End-User (Chemical, Oil and Gas, and Others), and Regional Forecast, 2026-2034

Direct Air Capture Market Overview

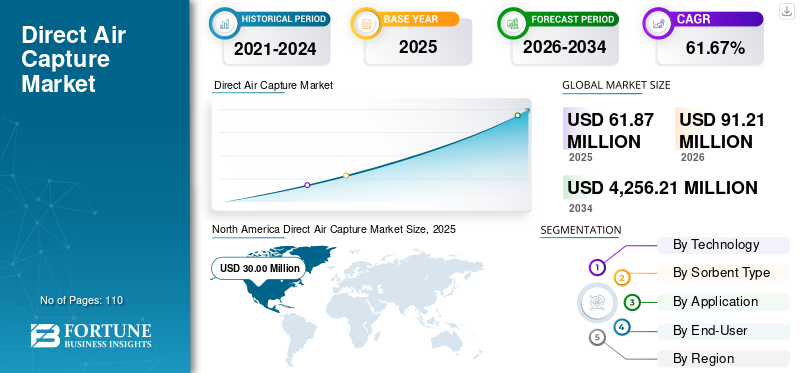

The global direct air capture market size was valued at USD 61.87 million in 2025. The market is projected to grow from USD 91.21 million in 2026 to USD 4,256.21 million by 2034, exhibiting a CAGR of 61.67% during the forecast period. North America dominated the direct air capture market with a market share of 48.48% in 2025.

Direct Air Capture (DAC) is a carbon removal technology that involves capturing carbon dioxide (CO₂) directly from ambient air using chemical or physical processes, and then either storing it permanently underground or utilizing it in industrial applications. The growing global urgency to attain net-zero emissions and tackle hard-to-abate CO₂ emissions from industries such as cement, aviation, and heavy industry is the main factor driving the rapid expansion of the industry. Regulatory agencies and governments throughout regions such as Europe and North America are implementing helpful legislation, tax credits, and financial instruments such as carbon pricing and incentives for carbon removal technologies that are greatly encouraging investment in DAC initiatives. Thus, the market is further gaining momentum with the growing focus on carbon reduction technologies such as DAC. DAC systems actively remove CO₂ directly from the atmosphere, creating a strong need for accurate monitoring, measurement, and verification (MMV) of captured emissions.

Climeworks, Carbon Engineering ULC, and Zero Carbon Systems are considered major vendors in the market due to their strong technological capabilities, early-mover advantage, and active involvement in scaling commercial carbon removal projects. Climeworks has established itself as a global leader by successfully deploying operational DAC plants, particularly in Europe, and securing long-term carbon removal agreements with corporate clients, demonstrating both technological maturity and market trust.

The market is witnessing increasing global momentum as countries and corporations intensify efforts to achieve net-zero emissions and deploy scalable carbon removal technologies. Strategic collaborations, particularly in regions with abundant renewable or low-cost energy resources, are becoming a key approach to improving the economic viability and large-scale deployment of DAC systems. These partnerships not only support technological advancement but also enable geographic expansion into high-potential markets.

In February 2026, to grow DAC technology in the area, Climeworks established a larger partnership with the Royal Commission for Jubail and Yanbu (RCJY) of Saudi Arabia. The action indicates an interest in using DAC in areas with significant renewable or low-cost energy resources.

Download Free sample to learn more about this report.

Direct Air Capture Market Key Takeaways

- 2025 Market Size: USD 61.87 Million

- 2026 Market Size: USD 91.21 Million

- 2034 Forecast Market Size: USD 4,256.21 Million

- CAGR: 61.67% from 2026–2034

- North America dominated the direct air capture market with a 48.48% share in 2025.

- The CO₂ concentrating DAC segment accounted for a 42.43% share in 2025.

- The carbon capture and permanent storage segment held a 67.03% share in 2025.

Asia Pacific

Asia Pacific generated USD 8.18 million in 2025 and is projected to reach USD 13.24 million in 2026.

North America

North America generated USD 30.00 million in 2025 and is projected to reach USD 43.22 million in 2026.

Europe

Europe generated USD 18.66 million in 2025 and is projected to reach USD 27.61 million in 2026.

U.S.

The direct air capture market generated USD 26.63 million in 2025.

Japan

Growing government support for carbon removal technologies and investments in pilot DAC projects continue to drive market growth.

Read More

DIRECT AIR CAPTURE MARKET TRENDS

Increasing Urgency to Mitigate Climate Change Drive Market Growth

A significant factor in the expansion of the DAC market is the rising need to address climate change. In order to achieve international climate goals such as the Paris Agreement, which seeks to keep the global temperature increase to 1.5°C, governments, businesses, and organizations around the world are facing increasing pressure to lower atmospheric carbon dioxide levels. Although energy efficiency improvements and the adoption of renewable energy are crucial emissions reduction methods, they are frequently inadequate to counteract the existing and difficult-to-reduce emissions from sectors including cement, aviation, and heavy industry. Consequently, DAC technology has attracted attention as a viable method for actively extracting CO2 directly from the atmosphere.

In September 2024, the U.S. Department of Energy (DOE) announced a plan to offer up to USD 1.8 billion in funding to support the construction, development, and operation of large-scale Direct Air Capture facilities. The goal of the effort is to speed the creation of carbon removal technologies that help reduce atmospheric CO2 levels and support ongoing climate change mitigation activities. The financing provided offers flexible and comprehensive strategies for promoting the development of commercial DAC facilities, including those on a medium to large scale, as well as supporting infrastructure, with the aim of expanding into Regional DAC Hubs. The Regional DAC Hubs program's inaugural solicitation, which took place in August 2023 and selected 21 projects for award discussions, including two Regional DAC Hubs in Louisiana and Texas, served as the basis for OECD (Office of Clean Energy Demonstration).

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Carbon Removal Technologies to Drive the Market Growth

The primary driver behind the expansion of the DAC industry is the rising need for carbon removal technologies. Governments, businesses, and organizations are now more aware that just cutting emissions might not be enough to meet climate targets as carbon emissions worldwide keep increasing. Technologies for removing carbon, such as DAC, are becoming more and more important since they have the ability to directly eliminate carbon dioxide that is already in the atmosphere. This is especially true for industries that are difficult to reduce, such as aviation, cement, steel, and heavy manufacturing, where completely eliminating emissions is still difficult. Moreover, several businesses are acquiring carbon removal credits from DAC projects in order to fulfill their net-zero and sustainability pledges. The market is expanding as a result of the rising demand for carbon removal solutions, which is fueled by increased investments, favorable regulations, and increased understanding of the necessity for negative emission technologies.

In September 2024, in order to support Microsoft's carbon removal plan, 1PointFive, a business that specializes in carbon capture, use, and sequestration (CCUS), has agreed to sell Microsoft 500,000 metric tons of Carbon Dioxide Removal (CDR) credits over six years. The deal is the largest single purchase of CDR credits ever made possible by DAC, and it illustrates how more and more businesses are using this climate technology to reach net zero emissions. The first industrial-scale DAC facility that 1PointFive is constructing in Texas, STRATOS, will give Microsoft CDR credits. The carbon dioxide (CO2) that forms the basis of the credits will be safely stored underground in saline formations rather than utilized to produce oil and gas, in accordance with the agreement with Microsoft, which has promised to achieve carbon negativity by 2030. Direct Air Capture offers a straightforward, long-term method for addressing emissions on a broad scale, particularly from hard-to-reduce industries.

MARKET RESTRAINTS

High Capital and Operational Costs Associated with DAC Technologies to Restrain Market Growth

The significant expenditures associated with DAC technologies are a major barrier to the market. Its high capital and operational costs largely constrain the market. Creating DAC facilities necessitates a large upfront expenditure in sophisticated machinery such as carbon separation systems, chemical sorbents, and air contactors, as well as the infrastructure needed for CO2 compression, transportation, and storage. Furthermore, DAC technology is energy-intensive since it requires significant amounts of electricity and heat to capture and treat carbon dioxide from the atmosphere.

Another challenge affecting market growth is the uncertainty surrounding policy frameworks and carbon pricing mechanisms in several regions. The economic viability of DAC projects often depends on supportive government policies, tax incentives, and well-established carbon markets. In regions where these mechanisms are underdeveloped or inconsistent, investors hesitate to fund DAC infrastructure due to uncertain financial returns. This policy uncertainty slows project development and hinders broader adoption of DAC technologies. Furthermore, public awareness and acceptance of large-scale carbon removal technologies remain limited in some regions. Concerns related to land use, energy consumption, and the long-term safety of CO₂ storage create resistance among communities and stakeholders. Addressing these concerns through transparent regulations, environmental assessments, and stakeholder engagement is essential for accelerating DAC deployment and market growth.

MARKET OPPORTUNITIES

Expansion of Voluntary Carbon Market (VCM) to Drive the Market Growth

A key driver behind the direct air capture market growth is the development of the Voluntary Carbon Market (VCM). Companies in sectors such as energy, aviation, manufacturing, and technology are increasingly dedicated to net-zero and carbon neutrality goals, which has led to a significant demand for premium carbon removal credits. DAC is considered as one of the most dependable methods for removing carbon since it physically removes CO₂ directly from the atmosphere and can offer verifiable credits for carbon removal.

Consequently, businesses are buying carbon credits from DACs in order to comply with environmental, social, and governance (ESG) requirements and to make up for their unavoidable emissions. Furthermore, the increasing involvement of private investors, climate initiatives, and sustainability programs in the voluntary carbon market is contributing to greater financing for carbon removal projects. Investments are aiding the expansion of the industry as a whole in DAC technology, which is a credible carbon offset solution that is increasingly sought after.

In September 2025, to expand its carbon credit and afforestation programs in the U.S., the carbon removal company Chestnut Carbon raised USD 250 million. The investment highlights the growing demand for carbon removal credits from companies seeking to meet their climate targets and shows renewed investor faith in voluntary carbon markets.

MARKET CHALLENGES

Technological Complexity and Performance Challenges to Hamper Market Growth

As capturing CO2 directly from ambient air is inherently challenging due to its low concentration (about 0.04%), technological complexity, and performance issues, it presents a major barrier to the expansion of the market. This necessitates extremely sophisticated materials, such as liquid solvents or solid sorbents that can selectively adsorb CO2 while retaining their strength throughout many cycles. But these materials sometimes have problems, including degradation, decreased efficiency with time, and high regenerative energy needs, which raise operating expenses.

Furthermore, the complicated integration of air contactors, chemical treatment devices, and heat management in DAC systems makes widespread installation technically difficult. Additional challenges arise when scaling up from pilot projects to commercial facilities, including system optimization, dependability, and consistent performance across a range of environmental circumstances.

Segmentation Analysis

By Technology

Ability to Produce High-Purity CO₂ for Efficient Storage and Industrial Utilization Led to the Dominance of CO2 Concentrating DAC Segment

Based on the technology, the market is classified into CO2 concentrating DAC, reactive DAC, and direct storage DAC.

CO2 concentrating DAC segment dominated the market, with a 42.43% share in 2025. The growth is primarily due to the more practical and scalable pathway these technologies offer for carbon removal by producing a high-purity, concentrated CO₂ stream that can be easily transported, stored, or utilized. Unlike passive or low-concentration capture approaches, CO₂-concentrating systems, typically based on liquid solvents or solid sorbents, are specifically designed to capture and then release CO₂ in a purified form. Further, making them highly compatible with existing carbon storage (CCS) infrastructure and industrial utilization processes such as synthetic fuels and chemicals.

- In March 2026, the Mammoth facility in Iceland, developed by Climeworks, became one of the largest DAC plants globally, designed to capture around 36,000 tons of CO₂ per year. What makes this facility significant is the way it captures and concentrates CO₂ from ambient air, which contains only about 0.04% carbon dioxide. In practice, the plant uses large fans to draw in air and pass it over specialized solid sorbent filters that selectively bind with CO₂ molecules. Once the filters are saturated, heat is applied to release the captured CO₂ in a highly concentrated and purified form. This concentration step is critical as it transforms dilute atmospheric CO₂ into a usable stream that can be efficiently handled.

Direct storage DAC is the second-dominant segment in the market, and is growing at a CAGR of 62.50% during the forecast period. The segment’s growth is driven by its ability to provide a complete and permanent carbon removal solution, which is increasingly preferred by governments and corporations aiming to achieve verifiable net-zero targets. Unlike utilization pathways, where captured CO₂ may eventually be re-released, direct storage involves injecting concentrated CO₂ into geological formations such as saline aquifers or basalt rock, ensuring long-term sequestration.

By Sorbent Type

Solid Sorbent Segment Dominates the Market due to High Capture Efficiency and Lower Energy Requirements

By sorbent type, the market is categorized into solid sorbent, liquid solvent, membrane, and electrochemical.

The solid sorbent segment dominated the market, accounting for a 41.85% of the direct air capture market share in 2025. The segment’s growth is driven by its high efficiency, modular design, and lower energy requirements compared to alternative technologies. Solid sorbent systems use advanced materials that selectively bind CO₂ from ambient air and release it upon low-temperature heating, making the process more energy-efficient and cost-effective. Additionally, these systems are highly scalable and can be deployed in modular units, enabling flexible installation across different locations, including remote or renewable energy-rich regions.

- The U.S. Department of Energy’s (DOE) NETL examined the performance and cost of different sorbent-based DAC system configurations that remove carbon dioxide from the atmosphere. DAC is an emerging CDR technology that concentrates CO2 found in ambient air rather than a large point source, thereby addressing both current and legacy emissions. Atmospheric concentrations of CO2 (~415 parts per million) are much lower than those found in effluent streams from point sources in the power and industrial sectors. Further, presenting greater technical and cost challenges for technologies that must concentrate CO2 to the degree necessary for storage or utilization. The DOE prioritizes DAC, and it plays a significant role in the Bipartisan Infrastructure Law (BIL). The law allocates USD 3.5 billion for the establishment of regional DAC Hubs, each designed to remove at least 1,000,000 metric tons of CO2 from the atmosphere.

Membrane is the fastest-growing segment in the market and is estimated to record a CAGR of 63.33% during the forecast period. The growth is primarily driven by its potential for lower energy consumption, continuous operation, and simplified system design compared to conventional solvent- and sorbent-based technologies.

By Application

Ability to Provide Durable and Long-Term CO₂ Removal Aligned with Net-Zero Targets Led to the Dominance of Carbon Capture and Permanent Storage

By application, the market is categorized into carbon capture and permanent storage and carbon utilization.

The carbon capture and permanent storage segment dominated the market, accounting for a 67.03% share in 2025. The segment is witnessing growth due to the increasing demand for durable and verifiable carbon removal solutions. Unlike carbon utilization pathways, permanent storage ensures that captured CO₂ is securely sequestered in geological formations such as saline aquifers or basalt rock, preventing its re-release into the atmosphere. This permanence is highly valued by governments and corporations aiming to meet stringent net-zero targets and participate in high-quality carbon credit markets.

- The U.S. Department of Energy’s investment in large-scale DAC hubs in Texas and Louisiana reflects a strategic effort to accelerate the commercialization of carbon removal combined with permanent storage (DACCS). These hubs are designed to capture up to 1 million tons of CO₂ per year, which is significantly larger than most existing DAC facilities, indicating a shift from pilot-scale to industrial-scale deployment. The captured CO₂ will be transported and injected into deep geological formations such as saline aquifers, where it can be securely stored for thousands of years without re-entering the atmosphere. This initiative demonstrates a strong government push to build an integrated ecosystem that includes CO₂ capture, transport infrastructure, and long-term storage, rather than focusing on capture alone. By providing large-scale funding and policy support, the DOE is reducing financial risks for private players and encouraging investments in DAC technologies. It also highlights the growing importance of permanent carbon removal solutions, which are essential for achieving net-zero targets and generating high-quality carbon credits.

Carbon utilization was the second-dominant segment in the market, accounting for a 32.97% share in 2025, and is estimated to register a CAGR of 61.03% during the forecast period. The segment is growing due to its ability to convert captured CO₂ into valuable products, creating economic incentives alongside environmental benefits. Instead of solely storing CO₂, industries are increasingly utilizing it in applications such as synthetic fuels, chemicals, building materials, and food & beverage carbonation, which helps offset capture costs and improve project viability.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Strong Investment Capacity and Existing CO₂ Storage Infrastructure Enabling Large-Scale Deployment Led to the Dominance of Oil & Gas Segment

By end-user, the market is categorized into chemical, oil and gas, and others.

The oil and gas segment dominated the market, accounting for a 46.72% share in 2025. The growth is due to its strong financial capacity, existing expertise in subsurface operations, and strategic need to decarbonize its operations. Major oil and gas companies are actively investing in DAC technologies to offset emissions, meet regulatory requirements, and align with net-zero commitments.

- In March 2026, the STRATOS direct air capture facility in Texas, being developed by Occidental Petroleum's subsidiary 1PointFive, represented a significant advancement in the field of commercial-scale carbon removal. STRATOS is considerably larger than most currently operating DAC facilities, with a planned capacity of up to 500,000 tons of CO2 annually, indicating a shift from modest pilot studies to industrial-scale implementation. By promoting economies of scale and operational efficiency, this scale is crucial in lowering the cost per ton of CO2 captured. The project also highlights how oil and gas companies are leveraging their existing expertise in large infrastructure projects, subsurface geology, and CO₂ handling to accelerate DAC adoption. Once captured, the CO₂ can be transported and permanently stored underground using infrastructure and expertise already developed for oil and gas operations. This integration makes large-scale deployment more feasible and cost-effective.

Chemical is projected to be the fastest-growing segment in the market, with a CAGR of 65.79% during the forecast period. The segment plays a significant role in the market due to its ability to utilize captured CO₂ as a feedstock for producing value-added products. Chemical companies are increasingly adopting DAC to convert CO₂ into synthetic fuels, methanol, polymers, and specialty chemicals, thereby supporting the transition toward a circular carbon economy.

Direct Air Capture Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Direct Air Capture Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America is the dominating region and holds the largest market share. North America was valued at roughly USD 30.00 million in 2025 and is estimated to reach USD 43.22 million in 2026. Due to its robust policy incentives, extensive project rollout, and early commercialization in comparison to other parts of the world, North America's market is expanding quickly. The U.S. is the world leader in programs that enhance project economics, such as the 45Q tax credit, which provides up to USD 180 per ton of CO₂ for permanent storage. Furthermore, the U.S. Department of Energy has pledged over USD 3.5 billion for DAC hubs, each of which aims to capture around one million tons of CO2 annually. This is far more than the hundreds of tons of modular systems in China or the tens of thousands of tons of plants in Europe, such as Climeworks' Mammoth, which has a capacity of 36,000 tons per year.

U.S. Direct Air Capture Market

The U.S. market was valued at around USD 26.63 million in 2025. The U.S. benefits from extensive CO₂ pipeline networks and geological storage capacity, particularly in regions such as Texas and Louisiana, enabling seamless integration of capture and storage. Moreover, strong participation from major oil & gas companies such as Occidental (STRATOS plant ~500,000 tons/year) and ExxonMobil is accelerating large-scale deployment. This combination of high-value incentives, industrial-scale projects, and existing infrastructure positions the U.S. as the most advanced and fastest-scaling DAC market globally.

Asia Pacific

Asia Pacific accounted for an estimated USD 8.18 million in 2025 and is estimated to reach USD 13.24 million in 2026. The Asia Pacific market is growing due to increasing government focus on net-zero targets, rising industrial emissions, and expanding investments in carbon removal technologies. Countries such as Japan, China, and Australia are actively supporting DAC through policy initiatives, research funding, and pilot projects, while the region’s growing availability of renewable energy and large industrial base further support scalable deployment of DAC solutions.

China Direct Air Capture Market

In 2025, the China market size reached USD 2.68 million. China’s market is growing due to a distinct combination of industrial policy alignment, coal-based emissions pressure, and state-led CCUS scaling, which differs from Western markets driven mainly by voluntary carbon markets.

Firstly, China’s carbon neutrality target (2060) is heavily dependent on negative emissions technologies, with DAC being identified in national research programs such as the Key R&D Program on Carbon Neutrality Technologies. Unlike Europe or especially the U.S., where DAC is still largely pilot-driven, China is integrating DAC into its broader CCUS deployment roadmap, which already includes millions of tons of CO₂ capture capacity annually from industrial sources.

In July 2024, China's "CarbonBox" DAC system passed reliability tests as it shows that the technology is capable of functioning reliably and effectively in real-world settings, which is a necessary prerequisite for widespread adoption. The system, which was created jointly by Shanghai Jiao Tong University and China Energy Engineering Corporation, demonstrates China's increasing capacity to create and commercialize cutting-edge carbon removal technology within the nation.

With a purity of approximately 99%, each module can capture more than 100 tons of CO2 annually, demonstrating that the system is capable of producing a high-quality, concentrated CO2 stream that can be used for both industrial applications and long-term geological storage. The existing scale (about 600 tons per year for a complete system) is less than that of Western large-scale facilities. Still, the modular design allows for the use of numerous units to increase capacity.

India Direct Air Capture Market

The India market in 2025 was valued at around USD 1.05 million, accounting for roughly 12.82% of the global market. India's market is expanding as a result of its unique combination of policy-driven climate commitments, water-energy restrictions, and decentralized industrial structure, all of which set it apart from Western and China-led models. Unlike areas that concentrate on massive, isolated DAC plants, India is looking at DAC as a component of decentralized deployment across industrial hubs, notably in industries such as cement, refining, and chemicals, which continue to struggle with emissions.

Europe

The Europe market in 2025 was valued at USD 18.66 million and is estimated to reach USD 27.61 million in 2026. The region is growing due to its strong regulatory framework, carbon pricing mechanisms, and focus on high-quality carbon removal standards, which set it apart from other regions. The European Union’s Emissions Trading System (EU ETS) and evolving carbon removal certification frameworks are creating structured demand for verified and permanent carbon removal solutions, including DAC.

U.K. Direct Air Capture Market

The U.K. market in 2025 was valued at around USD 4.16 million, representing roughly 22.32% of the global market. The market is expanding due to its focus on carbon removal, robust financing models, and connection to the national carbon storage system, all of which set it apart from other nations. The U.K. government has pledged USD 22.6 billion to carbon capture and storage (CCS) for over 20 years, with DAC anticipated to have a part in this larger CCUS framework. The country is developing DAC as part of industrial cluster decarbonization initiatives such as the East Coast Cluster and HyNet. This is where captured CO₂ can be transported and stored in the North Sea, which is estimated to have a storage capacity of about 78 billion tons of CO₂. This is in contrast to the U.S., which concentrates on huge, independent DAC hubs.

Germany Direct Air Capture Market

The Germany market in 2025 was valued at around USD 3.61 million, accounting for roughly 19.36% of the global market sales. The country stands apart from other nations owing to its robust industrial decarbonization pressure, sophisticated engineering environment, and integration with European carbon management strategies, which are driving the expansion of its market. As Germany has the largest industrial economy in Europe, it has a structural demand for carbon removal technologies such as DAC due to the high emissions from difficult-to-abate industries such as steel, cement, and chemicals. The nation is aggressively promoting carbon management through its Carbon Management Strategy (CMS) and alignment with the EU's climate neutrality objectives for 2045, which is before the EU's 2050 aim.

Latin America & Middle East & Africa

Latin America and the Middle East & Africa accounted for an estimated USD 2.33 million and USD 2.70 million in 2025. The Latin America’s market is growing due to its unique advantage of abundant low-cost renewable energy and emerging carbon market frameworks, which differentiate it from other regions. Countries such as Chile and Brazil have some of the world’s lowest solar and wind energy costs, making them attractive locations for energy-intensive DAC operations compared to Europe or North America.

The Middle East & Africa's market is expanding due to its distinctive benefit of cheap energy and close connection to the oil and gas industry, which sets it apart from other areas. The Middle East, particularly Saudi Arabia and the UAE, has a significant solar energy potential (with some of the lowest solar generation costs in the world, sometimes below USD 20/MWh), energy-intensive DAC processes are more financially feasible in the region than in Europe or Asia.

GCC Direct Air Capture Market

The GCC market in 2025 was valued at around USD 1.57 million, representing roughly 57.91% of the global market sales. Due to its outstanding low-cost energy advantage, enormous storage capacity, and government-supported investments, the GCC market is expanding, setting it apart from other areas. Solar energy prices in GCC nations, notably Saudi Arabia and the UAE, are among the lowest in the world (sometimes around USD 10–20 per megawatt hour). This is significantly lower than energy prices in Europe (USD 50–100 per megawatt hour) and parts of Asia, DAC's energy-intensive operations are more financially feasible.

COMPETITIVE LANDSCAPE

Key Industry Players

DAC Vendors Focus on Scaling Technologies and Reducing Capture Costs to enable Large-Scale Carbon Removal and Storage Solutions

DAC vendors are primarily focused on developing, scaling, and commercializing technologies that capture CO₂ directly from the atmosphere and enable its storage or utilization. These companies are investing heavily in advanced capture materials (solid sorbents, solvents, membranes) and improving system efficiency to reduce energy consumption and costs. In addition, vendors are forming strategic partnerships with governments, oil & gas companies, and industrial players to deploy large-scale DAC plants and integrate them with carbon storage infrastructure. They are also actively engaging in carbon credit markets by offering carbon removal services to corporations aiming to meet net-zero targets. Furthermore, DAC vendors are expanding geographically into regions with low-cost renewable energy and strong policy support, while focusing on modular and scalable solutions to accelerate the global adoption of carbon removal technologies.

In December 2025, as a major step toward making carbon removal scalable and globally available, Climeworks unveiled the opening of its Direct Air Capture (DAC) Innovation Center. It is the biggest innovation facility of its kind in the world and is focused on cutting-edge DAC technology. Over 50 engineers, chemists, and technology specialists are housed at the Climeworks DAC Innovation Center to tackle the sector’s most pressing challenge: reducing the cost of carbon capture. By accelerating improvements in sorbent performance, energy efficiency, and system design, the center will help Climeworks achieve its latest technological breakthroughs.

LIST OF KEY DIRECT AIR CAPTURE COMPANIES PROFILED

- Climeworks (Switzerland)

- Carbon Engineering ULC (Canada)

- Zero Carbon Systems (U.S.)

- Heirloom Carbon Technologies (U.S.)

- Skytree (Netherlands)

- Avnos, Inc. (U.S.)

- Carbon Clean (U.K.)

- Deep Sky (Canada)

- Soletair Power (Finland)

- Noya PBC (U.S.)

- Mission Zero Technologies (U.K.)

- Sirona Technologies (Belgium)

- Octavia Carbon (Kenya)

- Kawasaki Heavy Industries, Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Climeworks, a world leader in carbon removal through DAC, signed a significant agreement with Schneider Electric, a multinational corporation that specializes in energy management and automation, in September 2025. According to this agreement, by 2039, Climeworks will utilize its direct air capture technology to remove 31,000 tons of carbon dioxide from the atmosphere. In addition to being Climeworks' largest portfolio agreement to date, this alliance also represents Schneider Electric's first buy of credits for carbon removal with high durability. The agreement emphasizes the increasing significance of long-term business commitments in expanding permanent carbon removal technologies and DAC solutions.

- July 2025: the official opening of Carbon Clean's new Global Innovation Center (GIC) in Navi Mumbai, India, was announced by the company, a worldwide pioneer in carbon capture technology. At about 77,121 square feet, the facility is expected to be one of the biggest research centers in the world devoted to carbon capture. In addition to modern facilities for solvent development, analysis, and testing, the GIC has two carbon capture facilities that allow the business to speed up innovation in carbon capture technologies.

- March 2025: Return Carbon and Skytree partnered with Verified Carbon to work with EDF Renewables North America (EDFR) on the development of DAC facilities in Texas. Return Carbon and EDF Renewables North America (EDFR) have signed a Term Sheet to provide renewable energy to major DAC facilities in Texas, which will generate cost-competitive approved carbon removal credits. Return Carbon is partnering with Verified Carbon, which offers geological sequestration expertise, and Skytree, the DAC technology partner, to generate 500,000 tons of negative emissions each year. This revolutionary partnership aims to revolutionize carbon removal operations by integrating a direct renewable energy source with the Gulf Coast's enormous geological carbon storage capacity and DAC technology.

- February 2025: In order to assist in expanding its direct air capture technology, the United Airlines Sustainable Flight Fund made an investment in Heirloom Carbon Technologies. Additionally, the deal grants the fund an option to buy up to 500,000 tons of CDR from Heirloom in the future. The captured CO₂ may be kept for good underground or used to make Sustainable Aviation Fuel (SAF).

- July 2023: The Los Angeles-based business that is creating Hybrid Direct Air Capture (HDAC) technology has reached an agreement for funding and collaboration with JetBlue Ventures, Shell Ventures, and ConocoPhillips. Avnos intends to use the money to offer commercially viable HDAC equipment by the end of 2025. Avnos has previously received multimillion-dollar contracts from the U.S. Department of Energy and the U.S. Office of Naval Research to test its HDAC solution in the field and to conduct experiments with CO2 capture and the production of e-fuels.

REPORT COVERAGE

The global direct air capture market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 61.67% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Technology, By Sorbent Type, By Application, By End-User, and Region |

| By Technology |

|

| By Sorbent Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 61.87 million in 2025 and is projected to reach USD 4,256.21 million by 2034.

The market is expected to exhibit a CAGR of 61.67% during the forecast period.

The oil and gas industry segment led the market by end-user.

The growing demand for carbon removal technologies to drive the market growth.

Carbon Engineering ULC, Noya PBC, and Mission Zero Technologies are among the prominent players in the market.

North America region dominated the market with the highest share in 2025.

Expansion of the voluntary carbon market to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us